Flexible Solar Panels Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Amorphous Silicon (a-Si), Cadmium Telluride (CdTe) and Copper Indium Gallium Selenide (CIGS)), By Application (Residential, Commercial, Automotive and Portable), By End-User (Residential, Commercial, Industrial, Automotive, Aerospace & Defense, and Others), and Geography

2025-11-28

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Flexible Solar Panels Market Overview

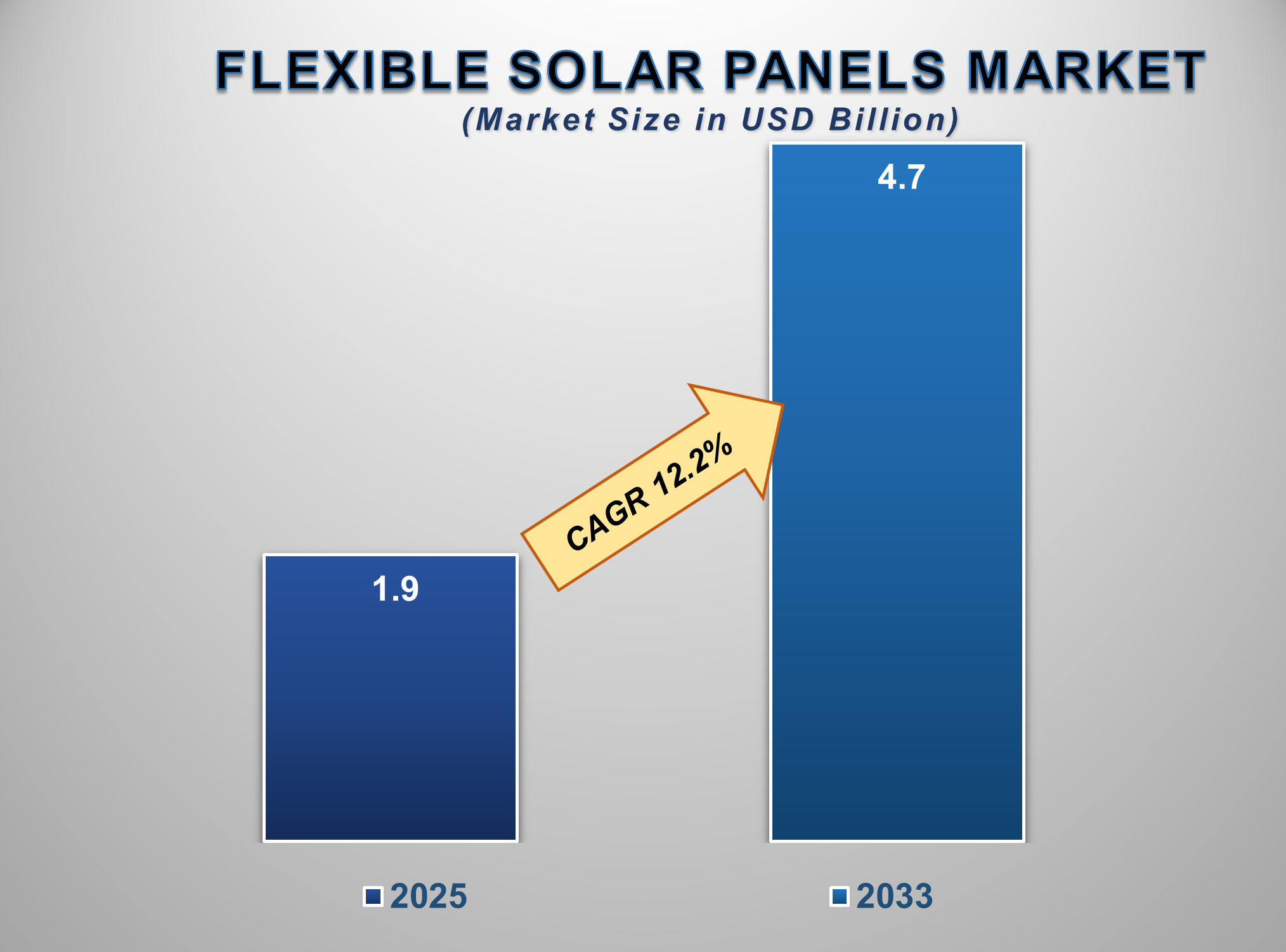

The Flexible Solar Panels Market is poised for a period of dynamic and rapid growth from 2025 to 2033, fueled by the escalating global demand for renewable energy, the unique advantages of lightweight and portable power generation, and the expansion of applications beyond traditional solar farms. The market is projected to be valued at approximately USD 1.9 billion in 2025 and is forecasted to reach nearly USD 4.7 billion by 2033, exhibiting a robust compound annual growth rate (CAGR) of 12.2% during this period.

Flexible solar panels are characterized by their

lightweight, thin-film construction, which allows them to be bent and conform

to curved surfaces. This distinguishes them from rigid, glass-based solar

panels and opens up a wide array of new applications. The market's significant

expansion is primarily driven by the global transition towards clean energy,

supported by government incentives and declining costs of photovoltaic

technology.

Furthermore, the versatility of flexible panels

enables their integration into vehicles, portable electronics, and

building-integrated photovoltaics (BIPV), creating novel use cases. The growing

demand for off-grid power solutions for recreational, military, and emergency

response applications is also a key contributor to market growth. North America

and Europe are significant markets due to high consumer awareness and

supportive policies, while the Asia-Pacific region is expected to witness the

fastest growth, driven by its massive investments in renewable energy and

strong manufacturing base for electronics.

Flexible Solar

Panels Market Drivers and Opportunities

The Global Push for Renewable Energy and

Unique Application Versatility is the Primary Market Driver

The relentless global shift towards renewable

energy sources is the most powerful force propelling the flexible solar panels

market. Governments worldwide are implementing ambitious carbon reduction

targets and offering subsidies, tax credits, and feed-in tariffs to encourage

solar adoption. While traditional panels dominate utility-scale projects,

flexible panels carve out a critical niche due to their unique physical

properties. Their lightweight and bendable nature allows for installation on

surfaces that cannot support heavy, rigid arrays, such as the curved roofs of

vehicles (RVs, boats, cars), tents, and certain architectural structures. This

versatility unlocks new markets and applications, making solar power accessible

in mobile and space-constrained environments. The demand for portable power for

outdoor recreation, remote work, and disaster relief further amplifies this

driver, establishing flexible solar panels as an essential tool for modern,

decentralized energy needs.

The global renewable energy market continues its

robust growth, with solar power leading the charge. In 2024, global solar

photovoltaic (PV) capacity additions are estimated to have reached over 350 GW,

accounting for more than half of all new renewable energy capacity. Total

installed solar PV capacity is projected to surpass 5,500 GW by 2030. This

growth is underpinned by falling technology costs, energy security concerns,

and strong policy support in major economies like the United States, China, and

the European Union. This data underscores the immense scale of the solar energy

transition and highlights the specific opportunity for flexible panels to

capture a growing segment of this market by addressing applications where

conventional panels are impractical or impossible to deploy.

The Rise of Building-Integrated Photovoltaics

(BIPV) and Electric Vehicle Integration is Driving Strategic Adoption

The convergence of solar technology with

construction and transportation is a powerful catalyst for the flexible solar

panels market. The building-integrated

Photovoltaics (BIPV) sector represents a major growth frontier, where solar

elements are incorporated directly into building materials like roofing

membranes, facades, and skylights. Flexible panels are ideally suited for this

application due to their low weight and adaptability, turning buildings into

distributed power generators without compromising aesthetics. Simultaneously,

the electric vehicle (EV) revolution is creating a new avenue for market

expansion. Flexible solar panels are being integrated into the roofs, hoods,

and trailers of EVs, trucks, and buses to extend driving range, power auxiliary

systems, and reduce reliance on charging infrastructure. This integration

transforms vehicles from mere energy consumers into mobile power harvesters,

enhancing their sustainability and functionality.

Technological Advancements and Material

Science Innovations Present Significant Opportunities

Breakthroughs in photovoltaic materials and

manufacturing processes are creating significant growth frontiers for the

flexible solar panel market. Key opportunities

lie in the development of more efficient and durable thin-film technologies,

such as CIGS (Copper Indium Gallium Selenide) and Perovskite solar cells.

Perovskite technology, in particular, holds promise for higher efficiency rates

and lower production costs in the future. Furthermore, advancements in

encapsulation materials are improving the longevity and weather resistance of

flexible panels, addressing a key concern for potential adopters. For

manufacturers, investing in R&D to boost conversion efficiency, reduce

degradation rates, and develop scalable, low-cost production methods is

a key strategy to

capture untapped market potential and make flexible solar panels a more

mainstream energy solution.

Flexible Solar Panels

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 1.9 Billion |

|

Market Forecast in 2033 |

USD 4.7 Billion |

|

CAGR % 2025-2033 |

12.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Return Type ●

By Service ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Flexible Solar Panels

Market Report Segmentation Analysis

The global Flexible Solar Panels

Market industry analysis is segmented by Type, by Application, by End-User, and

by Region.

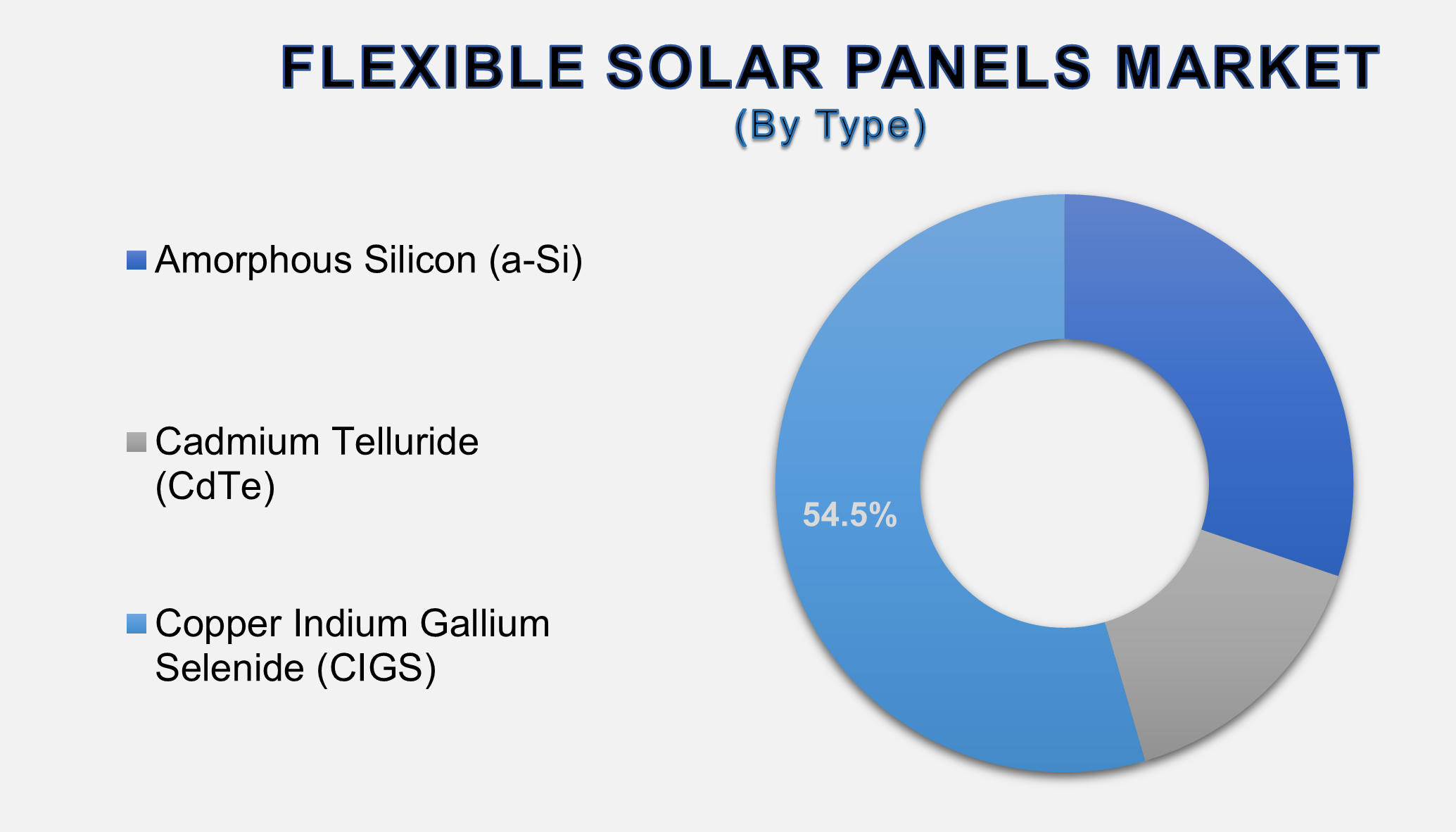

The CIGS Type segment is anticipated to command a

significant market share in 2025

The Type segment is categorized

into Amorphous Silicon (a-Si), Cadmium Telluride (CdTe), and Copper Indium

Gallium Selenide (CIGS). The CIGS segment holds a substantial and leading share

due to its superior efficiency and performance characteristics compared to

other thin-film options. CIGS panels offer the highest conversion efficiency

rates among mainstream flexible technologies, often approaching those of

polycrystalline silicon panels. They also perform better in real-world

conditions with partial shading and high temperatures. While historically more

expensive, advancements in manufacturing have been steadily reducing costs.

Their excellent flexibility, lightweight properties, and relatively high

efficiency make CIGS the preferred choice for high-performance applications in

aerospace, defense, and premium consumer products, securing its prominent

position in the market.

The Portable Application segment is projected to

grow at a significant CAGR.

The Application segment includes Residential,

Commercial, Automotive, and Portable. The portable application segment's

projected significant growth is directly linked to the increasing demand for

mobile and off-grid power solutions. This encompasses a wide range of products,

from foldable solar chargers for smartphones and laptops to larger, rollable

panels for camping, hiking, and military operations. The growth of the

"digital nomad" lifestyle, the popularity of outdoor recreational

activities, and the need for reliable power in remote locations and emergencies

are key drivers. The convenience, declining cost, and improving power output of

portable flexible panels make them an indispensable accessory for a growing

number of consumers and professionals, fueling rapid adoption and making this

the fastest-growing application segment.

The Automotive End-user segment is projected to

witness the highest growth rate.

The End-User segment is divided into Residential,

Commercial, Industrial, Automotive, and Aerospace & Defence. The Automotive

segment's position as the fastest-growing channel is a direct consequence of

the industry's electrification and the pursuit of sustainability. Automotive

manufacturers are increasingly integrating flexible solar panels into sunroofs

and body panels of electric and hybrid vehicles to provide auxiliary power, run

ventilation systems, and marginally extend the vehicle's range. This application

reduces the load on the main battery and improves overall energy efficiency.

The burgeoning markets for electric recreational vehicles (RVs) and commercial

trucks, where energy needs are high, present a particularly strong opportunity.

The continuous innovation in vehicle-integrated solar technology and

partnerships between solar companies and automakers are powerful forces

propelling the explosive growth of flexible panels within the automotive

industry.

The following segments are part of an in-depth analysis of

the global Flexible Solar Panels Market:

|

Market

Segments |

|

|

By Type |

●

Amorphous Silicon

(a-Si) ●

Cadmium Telluride

(CdTe) ●

Copper Indium

Gallium Selenide (CIGS) |

|

By Application

|

●

Residential ●

Commercial ●

Automotive ●

Portable |

|

By End-user |

●

Residential ●

Commercial ●

Industrial ●

Automotive ●

Aerospace &

Defense ●

Others |

Flexible Solar Panels

Market Share Analysis by Region

The Asia-Pacific region

is anticipated to hold the largest portion of the Flexible Solar Panels Market

globally throughout the forecast period.

Asia-Pacific's dominance is attributed to its

massive manufacturing capacity for solar PV components, strong government

support for renewable energy, and a rapidly growing consumer electronics and

automotive sector. China, in particular, is the world's largest producer and

consumer of solar panels, providing a robust foundation for the flexible

segment. Furthermore, countries like Japan, South Korea, and India are making

significant investments in solar energy and technological innovation. The

presence of a vast electronics manufacturing ecosystem allows for seamless

integration of flexible panels into a wide range of products, from portable

chargers to vehicles, solidifying the region's leading position.

China, in particular, is a critical hub for the

flexible solar panel market. The country's industrial policy, strong R&D

focus, and control over the solar supply chain from raw materials to finished

products give it a decisive competitive advantage. Chinese companies are

leaders in the production of thin-film solar technologies and are at the

forefront of developing next-generation solutions like perovskite. The large

domestic market for EVs and consumer electronics also provides a ready testing

ground and demand driver for innovative flexible solar applications, ensuring

its central role in the global market.

Flexible Solar Panels

Market Competition Landscape Analysis

The global flexible solar

panel market is fragmented and highly competitive, featuring a mix of

established solar giants, specialized thin-film manufacturers, and a growing

number of innovative startups. Competition is intensifying and centers on

product efficiency, durability, flexibility, price, and application-specific

expertise. Key strategies include heavy investment in R&D to advance

thin-film technologies, strategic partnerships with automotive and construction

companies for integrated solutions, and expansion of distribution channels for

consumer-facing portable products. The market also sees competition from

companies developing complementary technologies, such as energy storage, to

offer integrated power solutions.

Global Flexible Solar

Panels Market Recent Developments News:

- In February 2025, a European automotive

manufacturer announced a partnership with a leading CIGS producer to

integrate flexible solar roofs into its next-generation electric vehicles,

aiming to add up to 20 km of range per day.

- In December 2024, Hanergy Mobile Energy launched a

new line of ultra-lightweight, rollable perovskite solar panels for the

consumer market, boasting a record-breaking power-to-weight ratio for

portable applications.

- In August 2024, Ascent Solar Technologies, Inc.

secured a new contract to supply its flexible CIGS panels for a U.S.

Department of Defense program focused on lightweight, mobile power for

field operations.

- In October 2024, SunPower Corporation announced a strategic shift to

enter the BIPV market with a new line of flexible solar shingles designed

for residential rooftops with low weight-bearing capacity.

The Global Flexible Solar Panels Market Is Dominated by a Few

Large Companies, such as

●

Hanergy Thin Film

Power Group Ltd.

●

Ascent Solar

Technologies, Inc.

●

SunPower Corporation

●

Flisom AG

●

Global Solar Energy,

Inc. (Hanergy)

●

PowerFilm Solar Inc.

●

SoloPower Systems

●

Miasolé Hi-Tech Corp.

(Hanergy)

●

Jinko Solar Co., Ltd.

●

Canadian Solar Inc.

●

Trina Solar Co., Ltd.

●

LG Electronics Inc.

●

Sharp Corporation

●

Panasonic Corporation

●

Ricoh Company, Ltd.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Flexible Solar

Panels Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Flexible Solar Panels Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Flexible Solar

Panels Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Flexible

Solar Panels Market

1.3.2.Application of Global Flexible

Solar Panels Market

1.3.3.End-user of Global Flexible

Solar Panels Market

1.3.4.Region of Global Flexible

Solar Panels Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

Flexible Solar Panels Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Flexible Solar Panels Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Flexible Solar Panels Market Revenue (US$ Bn) Estimates and Forecasts, by Type,

2020 - 2033

4.1.1.Amorphous Silicon (a-Si)

4.1.2.Cadmium Telluride (CdTe)

4.1.3.Copper Indium Gallium

Selenide (CIGS)

5. Global

Flexible Solar Panels Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Flexible Solar Panels Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Residential

5.1.2.Commercial

5.1.3.Automotive

5.1.4.Portable

6. Global

Flexible Solar Panels Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Flexible Solar Panels Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

2020 - 2033

6.1.1.Residential

6.1.2.Commercial

6.1.3.Industrial

6.1.4.Automotive

6.1.5.Aerospace & Defense

6.1.6.Others

7. Global

Flexible Solar Panels Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Flexible Solar Panels Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Flexible

Solar Panels Market: Estimates &

Forecast Trend Analysis

8.1. North America Flexible

Solar Panels Market Assessments & Key Findings

8.1.1.North America Flexible

Solar Panels Market Introduction

8.1.2.North America Flexible

Solar Panels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Type

8.1.2.2.

By Application

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Flexible

Solar Panels Market: Estimates &

Forecast Trend Analysis

9.1. Europe Flexible Solar

Panels Market Assessments & Key Findings

9.1.1.Europe Flexible Solar

Panels Market Introduction

9.1.2.Europe Flexible Solar

Panels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Application

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Flexible

Solar Panels Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Flexible Solar Panels Market Introduction

10.1.2.

Asia

Pacific Flexible Solar Panels Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Application

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Flexible

Solar Panels Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Flexible Solar Panels Market Introduction

11.1.2. Middle

East & Africa

Flexible Solar Panels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Application

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Flexible Solar Panels Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Flexible

Solar Panels Market Introduction

12.1.2. Latin America Flexible

Solar Panels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Application

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Flexible Solar

Panels Market Product Mapping

14.2. Global Flexible Solar

Panels Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Flexible Solar

Panels Market Tier Structure Analysis

14.4. Global Flexible Solar

Panels Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Hanergy Thin Film Power Group Ltd.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Ascent Solar Technologies, Inc.

15.3.

SunPower Corporation

15.4.

Flisom AG

15.5.

Global Solar Energy, Inc. (Hanergy)

15.6.

PowerFilm Solar Inc.

15.7.

SoloPower Systems

15.8.

Miasolé Hi-Tech Corp. (Hanergy)

15.9.

Jinko Solar Co., Ltd.

15.10.

Canadian Solar Inc.

15.11.

Trina Solar Co., Ltd.

15.12.

LG Electronics Inc.

15.13.

Sharp Corporation

15.14.

Panasonic Corporation

15.15.

Ricoh Company, Ltd.

15.16.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables