Floor Cleaner Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Multisurface Floor Cleaners, Ceramic & Tile Cleaners, Marble Cleaners, Others), By Application (Commercial, Residential), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores, Online), and Geography.

2025-09-10

Consumer Products

Jaya Bundele (Research Analyst)

Description

Floor Cleaner Market Overview

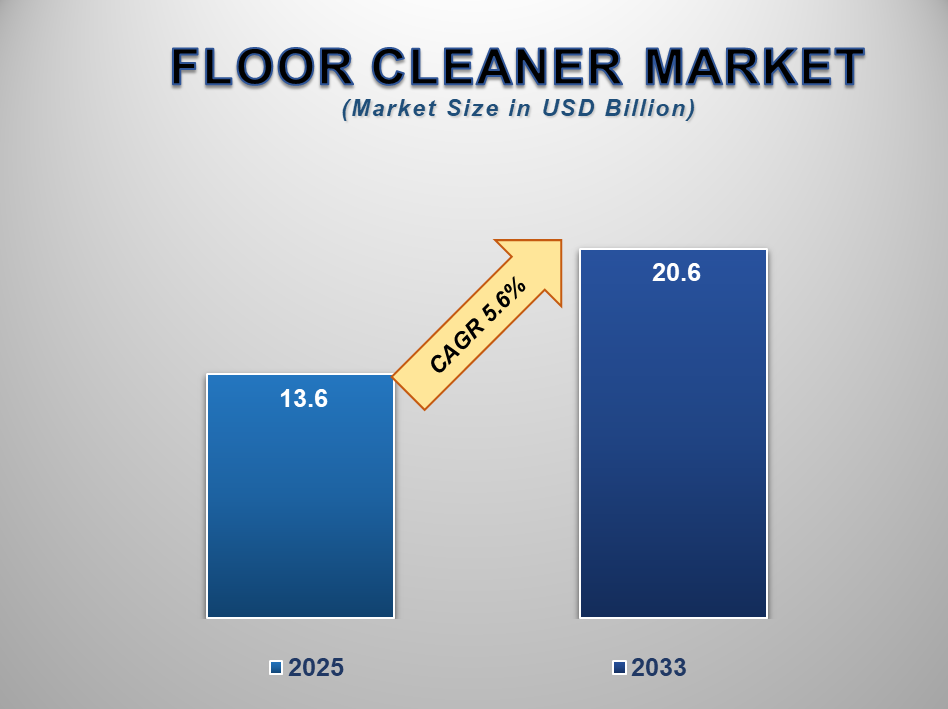

The Global Floor Cleaner Market is experiencing robust growth, driven by rising urbanization, increasing hygiene awareness, and the expansion of modern retail channels. Valued at USD 13.6 billion in 2025, the market is projected to reach USD 20.6 billion by 2033, growing at a CAGR of 5.6% over the forecast period. Floor cleaners are essential household and commercial cleaning agents designed to maintain hygiene, improve indoor air quality, and extend the durability of flooring materials. With consumer lifestyles becoming more fast-paced, demand for easy-to-use and multipurpose cleaners has surged. In addition, the COVID-19 pandemic accelerated hygiene consciousness, boosting the adoption of disinfectant-based cleaning solutions.

The market includes a wide

variety of products such as multi-surface cleaners, ceramic & tile

cleaners, and marble cleaners, catering to both residential and commercial

applications. Supermarkets, hypermarkets, and e-commerce channels have played a

pivotal role in making these products easily accessible to global consumers.

Technological advancements in formulations, including eco-friendly and

biodegradable cleaners, are further driving adoption. As consumer focus shifts

toward sustainability and healthier living, floor cleaner brands are innovating

with plant-based and non-toxic formulas. This changing preference, along with

expanding urban middle-class populations, ensures continued strong demand for

floor cleaners globally.

Floor Cleaner Market

Drivers and Opportunities

Rising consumer awareness of hygiene and infection control is

boosting the floor cleaner market

Heightened hygiene consciousness

is one of the strongest drivers propelling the floor cleaner market worldwide.

The global population has become increasingly aware of the risks associated

with poor cleanliness, especially after the COVID-19 pandemic highlighted the

role of surfaces in disease transmission. Consumers are seeking cleaning

products that not only maintain surface shine but also provide antibacterial

and disinfectant properties. Schools, offices, healthcare facilities, and

households alike are investing more in cleaning products to ensure safe and

sanitized environments. The demand for floor cleaners with multi-functional capabilities,

such as removing stains, eliminating germs, and leaving fresh fragrances, has

grown rapidly. This trend is supported by aggressive marketing campaigns from

leading brands emphasizing health and safety. In developing countries, rapid

urbanization and improved access to modern retail formats like supermarkets and

online platforms are introducing branded floor cleaners to households

previously reliant on traditional cleaning methods. As a result, growing

hygiene awareness across all income groups is significantly boosting market

revenues and ensuring long-term demand for floor cleaners.

Expansion of retail and e-commerce channels is accelerating

market growth

The rise of organized retail and

digital commerce has transformed how consumers access and purchase floor

cleaning products. Supermarkets, hypermarkets, and specialty stores provide

visibility and convenience, allowing consumers to choose from a wide range of

branded cleaners. Promotions, discounts, and product bundling in these stores

further stimulate sales. Meanwhile, the growth of e-commerce has created new

opportunities, particularly in emerging economies where online platforms are

rapidly gaining trust. Consumers increasingly prefer ordering cleaning products

online for doorstep delivery, often subscribing to recurring purchases. Leading

companies are leveraging this shift by enhancing their digital presence,

offering product demonstrations, and introducing direct-to-consumer sales

models. In addition, smaller, eco-friendly, and niche brands are using

e-commerce platforms to compete effectively with global giants. The dual push

from offline and online retail expansion is ensuring greater product penetration

across rural and urban markets alike, making distribution efficiency a critical

growth driver for the floor cleaner industry.

Opportunity for the Floor Cleaner Market

Eco-friendly and sustainable cleaning products present

significant market opportunities

Sustainability is becoming a defining factor in consumer purchasing decisions, creating a major opportunity for floor cleaner manufacturers. Growing concerns about chemical residues, indoor air pollution, and environmental damage are fueling demand for green and biodegradable cleaning products. Eco-conscious consumers, especially in developed markets such as Europe and North America, are actively seeking plant-based, non-toxic formulations free from harsh chemicals like ammonia and bleach. Manufacturers are responding with innovations in bio-enzymatic cleaners, natural fragrances, and recyclable packaging to cater to this demand. Moreover, government regulations promoting eco-friendly cleaning solutions are accelerating the adoption of sustainable practices in the cleaning industry. For instance, several regions are mandating reduced use of volatile organic compounds (VOCs) in household products. This shift is not limited to premium buyers; affordable eco-friendly cleaners are also emerging in price-sensitive markets, further expanding the addressable consumer base. As sustainability transitions from niche preference to mainstream expectation, eco-friendly floor cleaners are poised to capture a growing share of the global market.

Floor Cleaner Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 13.6 Billion |

|

Market Forecast in 2033 |

USD 20.6 Billion |

|

CAGR % 2025-2033 |

5.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Product ●

By Application ●

By Distribution Channel |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Floor Cleaner Market Report Segmentation Analysis

The global Floor Cleaner Market

industry analysis is segmented by product, by application, by distribution

channel, and by region.

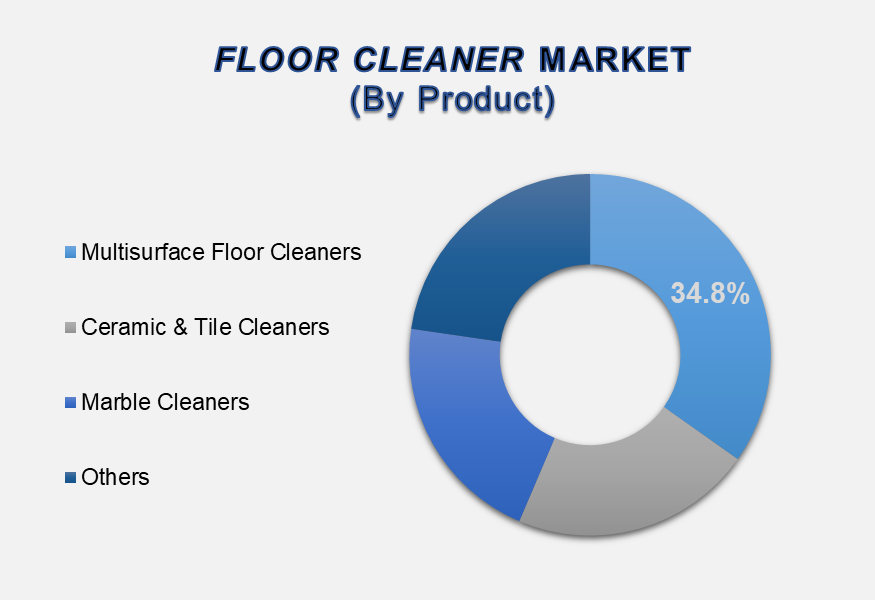

The Multisurface Floor Cleaners segment accounted for the

largest share in the global floor cleaner market.

By product, the market is divided into Multisurface Floor Cleaners, Ceramic & Tile Cleaners, Marble Cleaners, and Others. The multisurface floor cleaners segment held over 35% of the market share in 2024 due to their versatility and convenience. These products are designed to work effectively on a wide range of surfaces, including wood, tile, laminate, and vinyl, making them the preferred choice for households and commercial establishments alike. Consumers increasingly value time-saving solutions, and multisurface cleaners eliminate the need to purchase multiple specialized products. In addition, innovations in formulations that combine stain removal, fragrance, and antibacterial properties are boosting adoption. Ceramic & tile cleaners and marble cleaners remain important niche categories, primarily used in regions with a high prevalence of tiled or marble flooring. However, the growing trend of multi-functional solutions ensures multisurface cleaners maintain their leadership in the market.

The residential segment accounted for the largest share in

the global floor cleaner market.

By application, the market

divides into Commercial and Residential. The residential segment held the

leading position in 2024, driven by rising consumer focus on household hygiene

and the increasing frequency of cleaning routines. Urban households are

particularly inclined toward branded and specialized cleaners due to higher

disposable incomes and exposure to modern retail. Additionally, the increasing

number of dual-income families has led to demand for fast, effective, and

easy-to-use cleaning solutions. The commercial segment, encompassing offices,

malls, schools, and hospitals, is also experiencing steady growth, driven by

stricter hygiene regulations and higher foot traffic in public spaces. However,

with the growing middle-class population and expanding urbanization,

residential applications continue to dominate overall demand for floor cleaners

globally.

The Supermarkets & Hypermarkets segment accounted for the

largest share in the global floor cleaner market.

By distribution channel, the

market divides into Supermarkets & Hypermarkets, Convenience Stores,

Specialty Stores, and Online. Supermarkets and hypermarkets dominate the

distribution landscape, owing to their ability to offer consumers a wide

variety of brands and product types in one location. The availability of

promotional offers, discounts, and bulk purchasing options further drives sales

through this channel. Convenience stores and specialty stores also play a

significant role, especially in emerging economies, where smaller retail

outlets remain prevalent. The online channel is growing rapidly as consumers

increasingly value the convenience of home delivery and subscription-based

purchasing. While e-commerce penetration is highest in developed regions, it is

expanding quickly across Asia Pacific and Latin America. Despite this growth,

supermarkets and hypermarkets remain the most widely used distribution channels

due to their established trust, physical product visibility, and direct

consumer engagement.

The following segments are part

of an in-depth analysis of the global floor cleaner market:

|

Market Segments |

|

|

By Product |

●

Multisurface Floor

Cleaners ●

Ceramic & Tile

Cleaners ●

Marble Cleaners ●

Others |

|

By Application |

●

Commercial ●

Residential |

|

By Distribution Channel |

●

Supermarkets &

Hypermarkets ●

Convenience Stores ●

Specialty Stores ●

Online |

Floor Cleaner Market

Share Analysis by Region

The North America region is projected to hold the largest

share of the global Floor Cleaner market over the forecast period.

North America accounted for 38.1%

of the market in 2025, making it the dominant region in floor cleaner adoption.

The U.S. leads the market with high demand for premium and eco-friendly

cleaning solutions, supported by advanced retail infrastructure and strong

brand presence. Consumer preference for convenient, multi-surface, and

fragrance-rich cleaning products is particularly strong. Additionally, the

shift away from traditional cleaning methods to branded, ready-to-use products

continues to reinforce North America’s leadership. Strong marketing strategies,

widespread availability, and high household penetration of floor cleaners

underpin the region’s market dominance.

Rapid urbanization, rising

disposable incomes, and changing lifestyle preferences are key factors driving

growth in Asia Pacific. Countries such as China, India, and Indonesia are

witnessing surging demand for household hygiene products due to expanding middle-class

populations and increasing awareness of cleanliness. Moreover, the rise of

modern retail channels and e-commerce is making branded cleaners more

accessible to consumers in rural and urban areas alike. With growing concerns

about infectious diseases and government initiatives promoting sanitation,

demand for both residential and commercial cleaning solutions is accelerating.

Asia Pacific is expected to emerge as the fastest-growing hub for floor

cleaners, driven by demographic growth and evolving consumer habits.

Floor Cleaner Market Competition Landscape Analysis

The global

floor cleaner market is highly competitive, with multinational corporations and

regional players actively competing for market share. Leading companies such as

Reckitt Benckiser, Procter & Gamble, Henkel, Unilever, and Kao Corporation

dominate the market through their extensive product portfolios, strong brand

recognition, and widespread distribution networks. These players are

increasingly focusing on eco-friendly and bio-based product innovations to

cater to shifting consumer preferences.

Global Floor Cleaner

Market Recent Developments News:

- In April 2022 – Alfred Kärcher expanded its autonomous cleaning

solutions with the launch of a professional robotic scrubber, enhancing

its portfolio of automated products for industrial and commercial

applications.

- In

January 2022 – Bortek Industries, Inc. (Bortek) acquired the operating

assets of Carolina Industrial Equipment, Inc. (CIE), a renowned

distributor of industrial cleaning and environmental equipment. This

strategic acquisition strengthens Bortek’s market presence and service

capabilities in the industrial sector.

The Global Floor Cleaner

Market is dominated by a few large companies, such as

●

Procter & Gamble

●

Unilever

●

Reckitt Benckiser

●

Henkel

●

The Clorox Company

●

SC Johnson

●

Kao Corporation

●

Colgate-Palmolive

●

Diversey Holdings

●

Church & Dwight

●

GOJO Industries

●

Zep Inc.

●

Nice Group

●

Phoenix Brands

●

Liby Group

●

Amorepacific

Corporation

●

Bona

●

Hillyard

●

Betco

●

Rochester Midland

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables