Food Authenticity Testing Services Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Target (Meat, Fish & Seafood, Dairy, Honey, Oil, Grain & Cereal, Processed Foods, Others), By Technology (PCR, LC-MS/GC-MS, Isotope Analysis, Immunoassay, NIR Spectroscopy, Others), By End-user (Government & Regulatory Bodies, Food Manufacturers, Retailers & Distributors, Third-Party Testing Labs), and Geography

2025-12-19

Consumer Products

Jaya Bundele (Research Analyst)

Description

Food

Authenticity Testing Services Market Overview

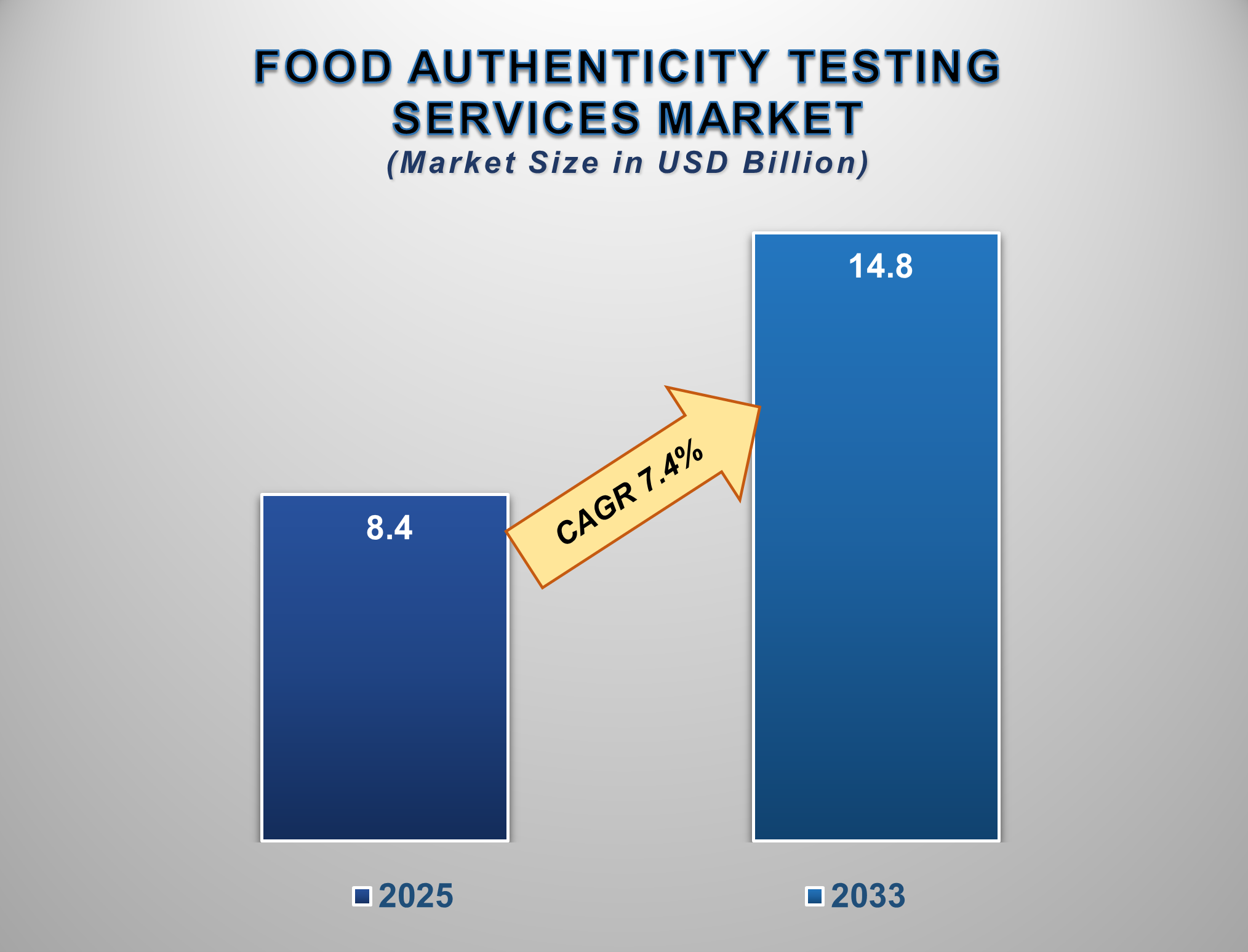

The Food Authenticity Testing Services Market is poised for robust growth from 2025 to 2033, driven by rising global food fraud incidents, stringent regulatory frameworks, and increasing consumer demand for food safety and transparency. The market is expected to be valued at USD 8.4 billion in 2025 and is projected to reach USD 14.8 billion by 2033, registering a CAGR of 7.4% during the forecast period.

Food authenticity testing services involve analytical

procedures to detect adulteration, mislabeling, and counterfeiting in food

products. These services ensure products comply with labeling laws, verify

origin and species, and protect consumers from health risks and economic

deception. High-profile food fraud scandals involving olive oil, honey, spices,

meat, and seafood have heightened regulatory scrutiny worldwide. Mandatory

labeling laws (e.g., the EU's Food Information

to Consumers Regulation and the US FSMA) and

global supply chain complexity are major growth drivers. Technological

advancements, such as rapid DNA-based testing and portable spectrometry, have

improved detection accuracy and speed. Europe and North America lead the market

due to mature regulatory environments, while the Asia-Pacific region is

experiencing the fastest growth due to expanding food trade and rising domestic

safety standards.

Food Authenticity Testing Services Market Drivers

and Opportunities

Rising Incidents of Food Fraud and Stringent Global

Regulations Are the Primary Market Drivers

Economic adulteration for unfair profit is a pervasive

issue, impacting nearly all food categories. Incidents such as horsemeat in

beef, dilution of olive oil, and mislabeling of fish species have eroded

consumer trust and prompted governments to enforce stricter testing and

traceability mandates. Regulatory bodies like the FDA (USA), EFSA (Europe), and

FSSAI (India) are increasingly mandating authenticity verification, compelling

food manufacturers and retailers to invest in routine testing. Furthermore, the

globalization of supply chains makes tracking ingredient origins more

challenging, necessitating robust testing protocols at multiple checkpoints.

This combination of economic, safety, and regulatory pressures is making

authenticity testing an integral, non-negotiable component of the modern food

industry.

Growing Consumer Awareness and Demand for Premium, Traceable

Products Are Accelerating Market Adoption

Today's consumers are more informed and concerned about

what they eat, demanding transparency regarding origin, organic status, non-GMO

claims, and ethical sourcing. This shift in consumer behavior is pushing brands

to adopt "farm-to-fork" traceability and verify premium claims

through scientific testing. Technologies like blockchain for supply chain

transparency are often integrated with physical testing results to provide

digital proof of authenticity. Retailers and foodservice providers are also

leveraging authenticity as a brand differentiator and a tool for risk

management. This consumer-led demand for integrity and quality is transforming

authenticity testing from a regulatory compliance cost into a strategic

value-add for brands.

Technological

Advancements and Untapped Potential in Emerging Markets Present Significant

Opportunities

Rapid innovation in testing technologies, such as

next-generation sequencing (NGS), hyperspectral imaging, and AI-powered data

analysis, is creating faster, cheaper, and more accurate testing solutions.

These advancements are making testing accessible to smaller producers for

high-frequency screening. Emerging markets in Asia-Pacific, Latin America, and

the Middle East present immense growth potential due to rising disposable

incomes, growing imported food consumption, and developing food safety regulations.

Strategic opportunities exist for testing service providers in establishing

localized labs, forming partnerships with agri-food exporters, and offering

cost-effective, targeted testing panels for prevalent local frauds (e.g.,

adulterated spices, milk, or saffron).

Food Authenticity Testing Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 8.4 Billion |

|

Market Forecast in 2033 |

USD 14.8 Billion |

|

CAGR % 2025-2033 |

7.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Target ●

By Technology ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Food Authenticity Testing Services Market Report

Segmentation Analysis

The global Food Authenticity

Testing Services Market is segmented by Target, Technology, End-user, and

Region.

Meat & Meat Products

Are Anticipated to Command the Largest Market Share in 2025

The

meat segment dominates due to its high economic value and frequent history of

adulteration, including species substitution (e.g., horsemeat), undeclared

protein extension, and false origin claims. Strict Halal and Kosher

certification requirements also necessitate rigorous species and process

verification. PCR-based testing is the gold standard in this category for its

ability to identify even trace amounts of adulterant DNA. Growing global meat

consumption, coupled with complex multi-country processing chains, ensures that

meat authenticity testing remains the largest and most critical segment for

ensuring consumer safety and regulatory compliance.

The PCR Technology

Segment Holds the Largest Share by Technology

Polymerase

Chain Reaction (PCR) technology is the leading segment due to its high

specificity, sensitivity, and ability to detect genetic material from even

highly processed foods. It is the preferred method for species identification

in meat, fish, and dairy products, as well as for detecting GMOs and allergens.

Its dominance is reinforced by standardization in international methods (e.g.,

ISO), relatively lower cost per test compared to some advanced techniques, and

its widespread adoption in commercial and regulatory labs. Continuous

advancements, like digital PCR and real-time PCR, are further solidifying its

position as the workhorse technology for food authenticity testing.

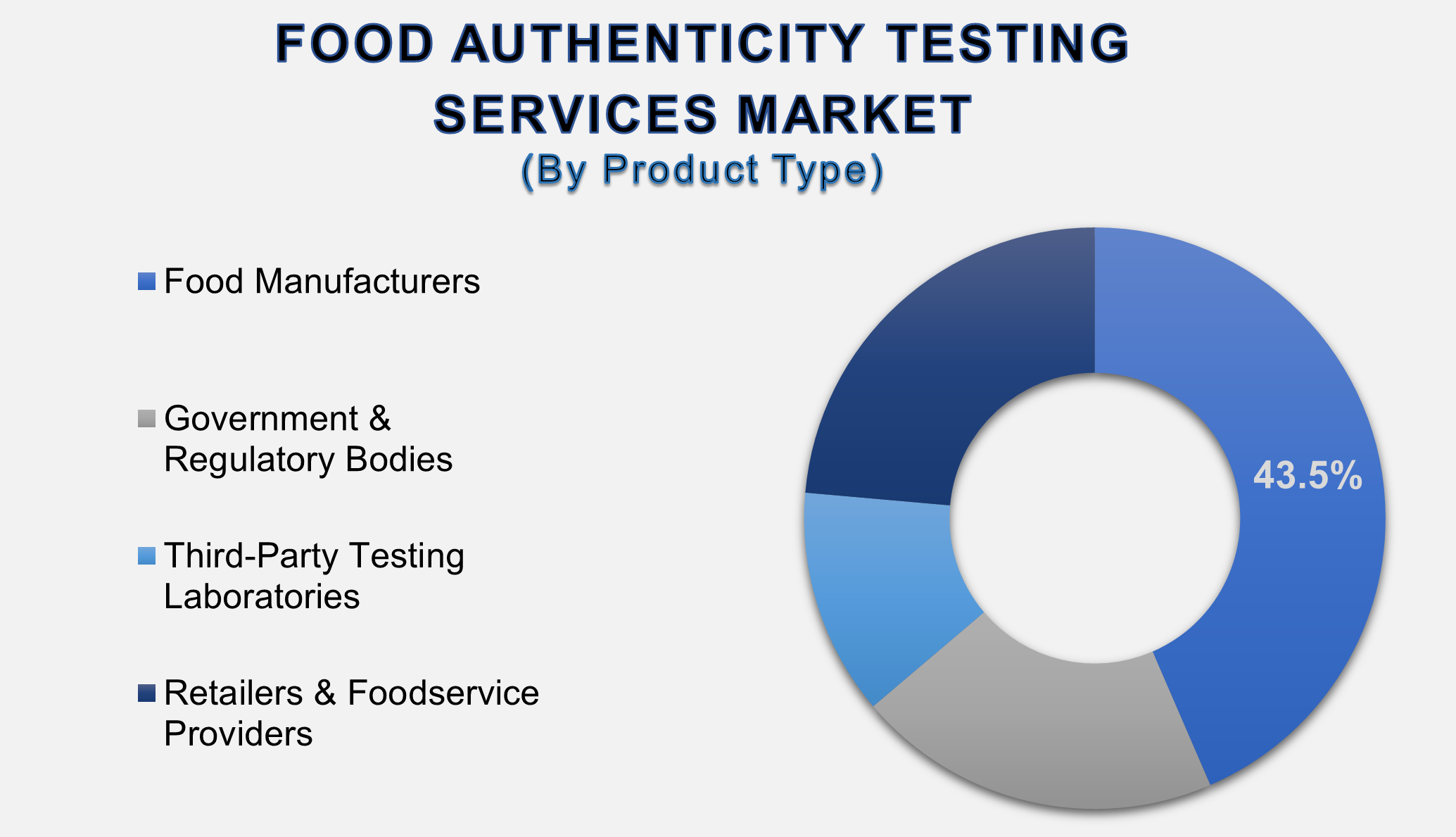

Food Manufacturers Lead

the End-user Segment

Food manufacturers are the largest end-user segment, as they bear the primary responsibility for the safety and authenticity of their products. Proactive testing is integral to their quality control (QC) and quality assurance (QA) programs to mitigate recall risks, protect brand reputation, and comply with both internal specifications and external regulations. This includes testing incoming raw materials, in-process samples, and final products. The scale of their operations generates consistent, high-volume demand for testing services, making this segment the cornerstone of the market.

The following segments are

part of an in-depth analysis of the global Food Authenticity Testing Services

Market:

|

Market

Segments |

|

|

By Target |

●

Meat & Meat

Products ●

Fish & Seafood ●

Dairy & Dairy

Products ●

Honey ●

Olive Oil &

Edible Oils ●

Grain & Cereal ●

Spices & Herbs ●

Processed Foods ●

Others |

|

By Technology |

●

PCR-based ●

Mass Spectrometry

(LC-MS/GC-MS) ●

Isotope Analysis

(IRMS) ●

Immunoassay ●

NIR &

Spectroscopy ●

Others |

|

By End-user |

●

Food Manufacturers ●

Government &

Regulatory Bodies ●

Third-Party Testing

Laboratories ●

Retailers &

Foodservice Providers |

Food

Authenticity Testing Services Market Share Analysis by Region

The Europe region is

anticipated to hold the largest portion of the Food Authenticity Testing

Services Market globally throughout the forecast period

Europe's

leadership stems from the world's most stringent food safety and labeling

regulations, a high level of consumer awareness, and a history of major food

fraud incidents that triggered regulatory overhauls. The European Commission's

coordinated control plans and the EU's robust geographical indication (GI)

system for protecting regional foods (like Parma ham and Champagne) create massive, mandated demand for origin and

authenticity testing. The strong presence of

major testing service providers and advanced food research institutes further

consolidates Europe's dominant market position.

Food Authenticity Testing Services Market

Competition Landscape Analysis

The global market is

semi-consolidated, featuring a mix of large multinational analytical

corporations, specialized food testing firms, and regional players. Competition

is based on technological expertise, accreditation scope (ISO, UKAS),

turnaround time, global laboratory network, and service portfolio. Key

strategies include mergers and acquisitions to expand geographical and

technical capabilities, development of multi-parameter testing kits, and

investments in rapid, on-site testing solutions to serve the farm and factory

gate.

Global Food Authenticity Testing Services Market Recent

Developments News:

- In February 2025, Eurofins Scientific launched a new

blockchain-integrated platform that pairs authenticity test results with

immutable digital supply chain records.

- In December 2024, SGS SA expanded its meat speciation testing

capacity in Brazil to support the growing meat export industry.

- In October 2024, Intertek Group plc introduced a rapid, portable NIR

device for on-site screening of olive oil adulteration.

- In August 2024, Bureau Veritas formed a strategic partnership with a

leading Asian retail conglomerate to provide end-to-end supply chain

auditing and testing services.

The Global Food Authenticity Testing Services

Market Is Dominated by a Few Large Companies, such as

●

Eurofins Scientific

●

SGS SA

●

Intertek Group plc

●

Bureau Veritas

●

Mérieux NutriSciences

●

ALS Limited

●

TÜV SÜD

●

Microbac Laboratories

●

ROMER Labs Division

Holding GmbH

●

Neogen Corporation

●

Thermo Fisher

Scientific Inc.

●

Waters Corporation

●

Shimadzu Corporation

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Food Authenticity

Testing Services Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Food Authenticity Testing Services Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Food Authenticity

Testing Services Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Target of Global Food

Authenticity Testing Services Market

1.3.2.Technology of Global Food

Authenticity Testing Services Market

1.3.3.End-user of Global Food

Authenticity Testing Services Market

1.3.4.Region of Global Food

Authenticity Testing Services Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Food Authenticity Testing Services Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Food Authenticity Testing Services Market

Estimates & Forecast Trend Analysis, by Target

4.1.

Global

Food Authenticity Testing Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Target, 2020 - 2033

4.1.1.Meat & Meat Products

4.1.2.Fish & Seafood

4.1.3.Dairy & Dairy Products

4.1.4.Honey

4.1.5.Olive Oil & Edible

Oils

4.1.6.Grain & Cereal

4.1.7.Spices & Herbs

4.1.8.Processed Foods

4.1.9.Others

5. Global

Food Authenticity Testing Services Market

Estimates & Forecast Trend Analysis, by Technology

5.1.

Global

Food Authenticity Testing Services Market Revenue (US$ Bn) Estimates and

Forecasts, by Technology, 2020 - 2033

5.1.1.PCR-based

5.1.2.Mass Spectrometry

(LC-MS/GC-MS)

5.1.3.Isotope Analysis (IRMS)

5.1.4.Immunoassay

5.1.5.NIR & Spectroscopy

5.1.6.Others

6. Global

Food Authenticity Testing Services Market

Estimates & Forecast Trend Analysis, by End-user

6.1.

Global

Food Authenticity Testing Services Market Revenue (US$ Bn) Estimates and

Forecasts, by End-user 2020 - 2033

6.1.1.Food Manufacturers

6.1.2.Government &

Regulatory Bodies

6.1.3.Third-Party Testing

Laboratories

6.1.4.Retailers &

Foodservice Providers

7. Global

Food Authenticity Testing Services Market

Estimates & Forecast Trend Analysis, by region

7.1.

Global

Food Authenticity Testing Services Market Revenue (US$ Bn) Estimates and

Forecasts, by region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Food

Authenticity Testing Services Market:

Estimates & Forecast Trend Analysis

8.1.

North

America Food Authenticity Testing Services Market Assessments & Key

Findings

8.1.1.North America Food

Authenticity Testing Services Market Introduction

8.1.2.North America Food

Authenticity Testing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

8.1.2.1. By Target

8.1.2.2. By Technology

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Food

Authenticity Testing Services Market:

Estimates & Forecast Trend Analysis

9.1.

Europe

Food Authenticity Testing Services Market Assessments & Key Findings

9.1.1.Europe Food Authenticity

Testing Services Market Introduction

9.1.2.Europe Food Authenticity

Testing Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Target

9.1.2.2. By Technology

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Food

Authenticity Testing Services Market:

Estimates & Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Food Authenticity Testing Services Market Introduction

10.1.2.

Asia

Pacific Food Authenticity Testing Services Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

10.1.2.1. By Target

10.1.2.2. By Technology

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Food

Authenticity Testing Services Market:

Estimates & Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Food Authenticity Testing Services

Market Introduction

11.1.2.

Middle East & Africa Food Authenticity Testing Services

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Target

11.1.2.2. By Technology

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Food Authenticity Testing Services Market: Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Food Authenticity Testing Services Market Introduction

12.1.2.

Latin

America Food Authenticity Testing Services Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

12.1.2.1. By Target

12.1.2.2. By Technology

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Food Authenticity Testing Services Market Product Mapping

14.2.

Global

Food Authenticity Testing Services Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

14.3.

Global

Food Authenticity Testing Services Market Tier Structure Analysis

14.4.

Global

Food Authenticity Testing Services Market Concentration & Company Market

Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Eurofins Scientific

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. SGS SA

15.3. Intertek

Group plc

15.4. Bureau

Veritas

15.5. Mérieux

NutriSciences

15.6. ALS Limited

15.7. TÜV SÜD

15.8. Microbac

Laboratories

15.9. ROMER Labs

Division Holding GmbH

15.10. Neogen

Corporation

15.11. Thermo Fisher

Scientific Inc.

15.12. Waters

Corporation

15.13. Shimadzu

Corporation

15.14. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables