Food Enzymes Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Carbohydrases, Proteases, Lipases), By Source (Microorganisms, Plants, Animals), By Application (Bakery, Dairy, Beverages, Nutraceuticals), And Geography

2025-12-03

Consumer Products

Jaya Bundele (Research Analyst)

Description

Food Enzymes Market Overview

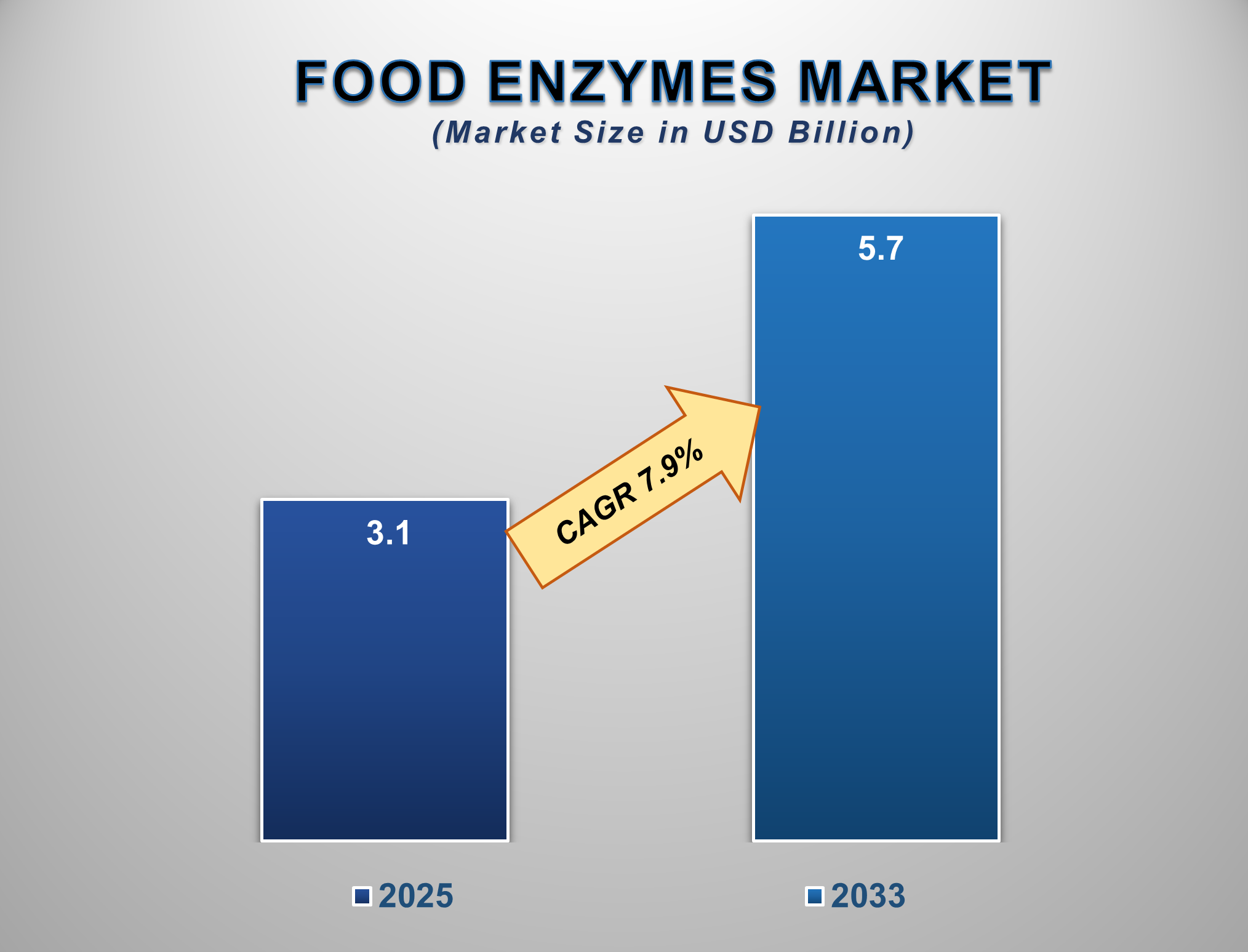

The Food Enzymes Market is poised for strong and sustained growth from 2025 to 2033, driven by the rising demand for processed foods, the shift towards clean-label and natural ingredients, and the increasing utilization of enzymes to improve food quality and production efficiency. The market is projected to be valued at approximately USD 3.1 billion in 2025 and is forecasted to reach nearly USD 5.7 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 7.9% during this period.

Food enzymes are specialized proteins that

catalyze specific biochemical reactions in food processing, serving as natural

alternatives to chemical additives. The market's robust expansion is primarily

fueled by the growing consumer preference for products with clean labels, free

from synthetic preservatives and additives. Enzymes enable manufacturers to

improve texture, enhance flavor, extend shelf

life, and increase yield sustainably and cost-effectively.

Furthermore, the advancement of enzyme

technologies, including microbial fermentation and genetic engineering, is

leading to the development of more efficient and specialized enzyme solutions.

The burgeoning functional food and beverage sector, where enzymes are key in

producing lactose-free, gluten-free, and prebiotic-enriched products, is a

significant growth driver. North America and Europe currently lead the market

due to stringent food regulations and high consumer awareness, while the

Asia-Pacific region is expected to witness the fastest growth, propelled by its

rapidly expanding food and beverage industry.

Food Enzymes

Market Drivers and Opportunities

The Surging Demand for Clean-Label and

Natural Ingredients is the Primary Market Driver

The most powerful force propelling the food

enzymes market is the global consumer shift towards clean-label and natural

products. Modern consumers are increasingly scrutinizing product ingredient

lists, preferring items with recognizable, naturally derived components over chemical-sounding additives. Food enzymes,

being biological catalysts, perfectly align with this trend, as they are considered processing aids and often do not

need to be declared on the final label in many regions or are listed as natural ingredients. They allow

manufacturers to replace synthetic emulsifiers, texture modifiers, and

preservatives while achieving superior results in terms of product softness,

volume, and shelf stability. This consumer-driven demand for transparency and

naturality is compelling food producers to reformulate their products, creating

a massive and sustained demand for enzyme solutions across all food and

beverage categories.

The Need for Process Optimization and Cost

Efficiency in Food Manufacturing is Driving Adoption

The food enzymes market is significantly driven

by the economic and operational benefits they offer to manufacturers. Enzymes

act as highly efficient biocatalysts that speed up processes, reduce energy

consumption, and improve raw material utilization, leading to substantial cost

savings. In baking, enzymes enhance dough stability and volume, reducing waste.

In dairy, they accelerate cheese ripening and increase yield. In starch

processing, they enable the efficient conversion of corn into high-fructose corn

syrup and other sweeteners. This drive for operational excellence, higher

throughput, and reduced production costs is a critical factor for large-scale

food producers operating on thin margins. The ability of enzymes to deliver

consistent and high-quality results makes them an indispensable tool for

modern, efficient food manufacturing.

The Expansion in Health & Wellness and

Specialty Diets Presents Significant Opportunities

The convergence of food science and nutrition is

unlocking significant growth frontiers for the food enzymes market. A major

opportunity lies in the burgeoning health and wellness sector, particularly in

the development of functional foods and products for specialized diets. Enzymes

are crucial in creating lactose-free dairy products (using lactase),

gluten-free baked goods (using proteases to break down gluten), and prebiotic

ingredients (using enzymes to produce fructo-oligosaccharides from sucrose). Furthermore,

the rising demand for plant-based protein alternatives presents a massive

opportunity for protease enzymes to improve the texture, flavor, and

nutritional profile of products like meat analogues. For enzyme manufacturers,

investing in R&D to develop novel, targeted enzyme blends for these

high-growth niches and leveraging biotechnological advancements to create more

robust and specific enzymes are key strategies to capture premium market value

and drive future growth.

Food Enzymes Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 3.1 Billion |

|

Market Forecast in 2033 |

USD 5.7 Billion |

|

CAGR % 2025-2033 |

7.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Type ●

By Source ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Food Enzymes Market

Report Segmentation Analysis

The global Food Enzymes Market

industry analysis is segmented by Type, by Source, by Application, and by

region.

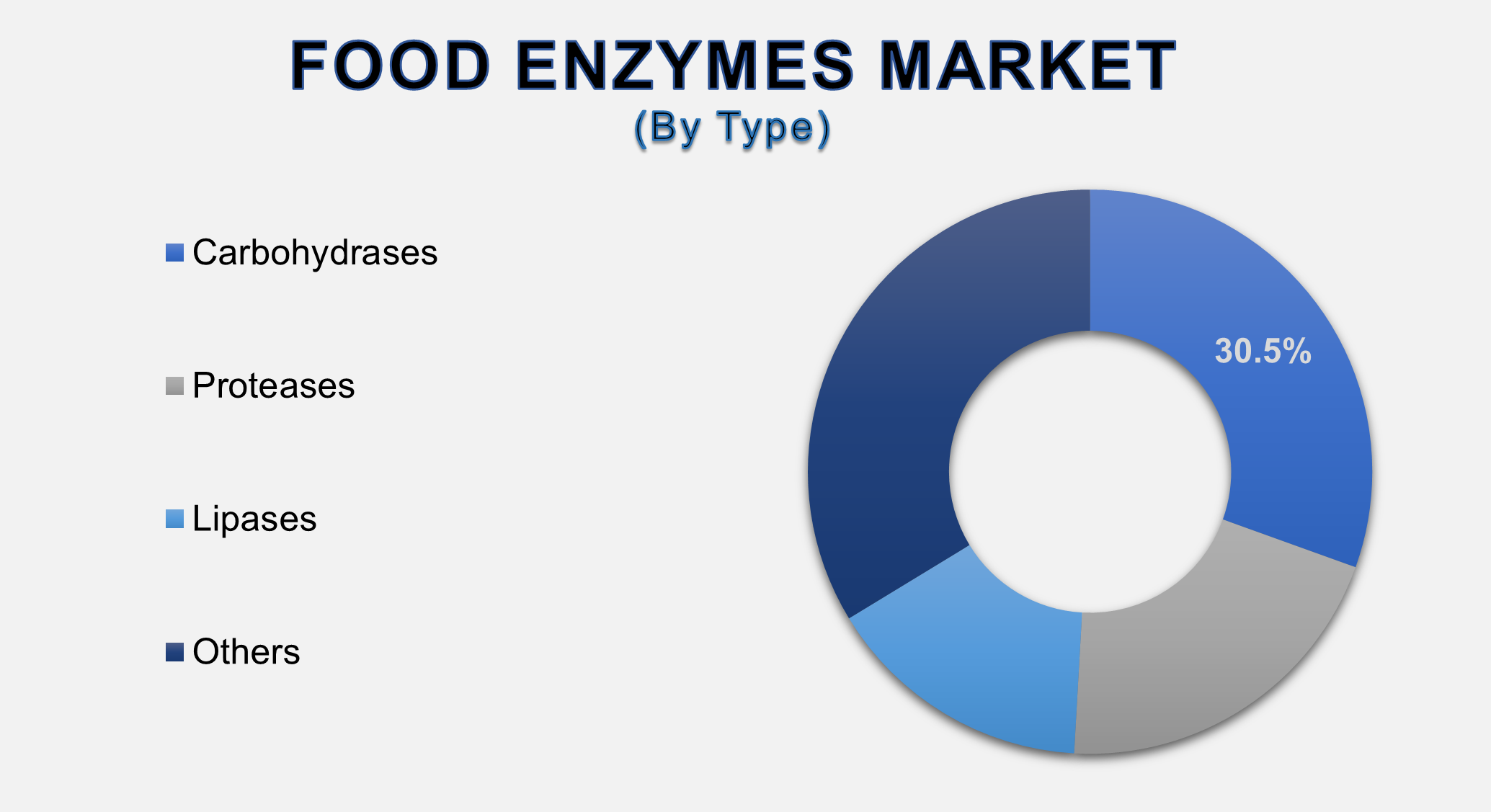

The Carbohydrases type

segment is anticipated to command the largest market share in 2025

The Type segment is categorised into

Carbohydrases, Proteases, and Lipases. The dominance of the carbohydrases

segment is attributed to their extensive and versatile applications across the

food and beverage industry. This category includes enzymes like amylases (for

starch conversion in baking and sweetener production), cellulases, pectinases

(for juice clarification and extraction), and lactase (for lactose-free dairy

products). The massive scale of the bakery, beverage, and starch processing

industries, which rely heavily on these enzymes for texture modification,

sweetness control, and yield improvement, solidifies carbohydrases' position as

the segment with the largest market share. Their critical role in producing

biofuels from starch also contributes to their demand.

The Microorganisms source segment is projected to

grow at a significant CAGR.

The Source segment includes Microorganisms,

Plants, and Animals. The microorganisms segment's projected significant growth

is driven by its advantages in production scalability, consistency, and

cost-effectiveness. Microbial fermentation allows for the controlled and

large-scale production of a wide variety of highly specific and pure enzymes.

It is not subject to seasonal variations or geographical limitations associated

with plant and animal sources. Furthermore, advancements in genetic engineering

and strain selection have enabled the development of robust microbial strains

that produce enzymes with desired characteristics, such as thermostability and

specific pH activity, tailored for modern industrial processes. This

reliability and flexibility make microbial-derived enzymes the preferred choice

for most industrial applications.

The Beverages application segment is projected to

witness the highest growth rate.

The Application segment is divided into Bakery,

Dairy, Beverages, and Nutraceuticals. The Beverages segment's position as the

fastest-growing channel is a result of the escalating global demand for

processed, clear, and stable beverages. Enzymes are indispensable in juice and

wine production for extraction, clarification, and debittering; in brewing for

efficient mashing and filtration; and in the production of functional and

reduced-sugar drinks. The growing popularity of fresh-tasting, natural, and clear

juices, coupled with the need for production efficiency in large-scale

breweries and soft drink manufacturing, is fueling the rapid adoption of

enzyme solutions. The ability of enzymes to create value-added products, such

as prebiotic beverages, further accelerates this segment's growth.

The following segments are part of an in-depth analysis of

the global Food Enzymes Market:

|

Market

Segments |

|

|

By Type |

●

Carbohydrases ●

Proteases ●

Lipases ●

Others |

|

By Source |

●

Microorganisms ●

Plants ●

Animals |

|

By Application |

●

Food Industry ●

Food Service ●

Retail/Household |

Food Enzymes Market Share

Analysis by Region

The North America region

is anticipated to hold a significant portion of the Food Enzymes Market

globally throughout the forecast period.

North America's dominance is attributed to its

highly developed and innovative food and beverage industry, stringent food

safety regulations that favor enzyme-based solutions over chemical

alternatives, and high consumer awareness regarding health and clean-label

products. The region is home to several leading global enzyme manufacturers and

has a strong R&D infrastructure. The well-established markets for

lactose-free dairy, gluten-free products, and craft brewing, all of which are

heavy users of specialized enzymes, further drive demand. The presence of major

food conglomerates that continuously seek process optimization and product

innovation ensures a steady and high-value market for food enzymes in the

region.

The United States alone is a powerhouse for

enzyme consumption and innovation. The country's Food and Drug Administration

(FDA) has a well-defined regulatory pathway for food enzymes (Generally

Recognized as Safe—GRAS), which facilitates market entry for new products. The high

per capita consumption of processed foods, dairy products, and beverages,

combined with strong trends in health and wellness, creates a robust domestic demand. The concentration of leading

biotechnology and food science companies in the U.S. fosters a competitive

environment focused on developing next-generation enzyme technologies,

reinforcing the region's market leadership.

Food Enzymes Market

Competition Landscape Analysis

The global food enzymes market

is moderately consolidated and characterized by intense competition among a few

major international players and several smaller regional ones. Competition is

based on technological innovation, product portfolio diversity, price, and the

ability to provide tailored solutions to large food and beverage clients. Key

strategies include significant investment in R&D to develop novel and more

efficient enzymes, strategic mergers and acquisitions to expand technological

capabilities and geographic reach, and forming long-term partnerships with key

industrial customers. Intellectual property, particularly in recombinant enzyme

technology, is a critical competitive barrier.

Global Food Enzymes

Market Recent Developments News:

- In March 2025, Novozymes A/S launched a new suite

of baking enzymes designed to reduce acrylamide formation and extend the

softness of whole-grain bread, targeting the health-conscious consumer

segment.

- In January 2025, International Flavors &

Fragrances Inc. (IFF) announced a strategic expansion of its microbial

fermentation capacity in Europe, focusing on producing non-GMO enzymes for

the clean-label market.

- In November 2024, DSM-Firmenich (now DSM-Firmenich) received regulatory

approval in China for its novel protease used in plant-based meat

alternatives, aiming to capture share in the rapidly growing Asia-Pacific

market.

- In September 2024, Chr. Hansen Holding A/S introduced a new lactase

enzyme with enhanced thermostability, allowing dairy producers to create

lactose-free products with a cleaner flavor profile and more efficient

processing.

The Global Food Enzymes

Market Is Dominated by a Few Large Companies, such as

●

Novozymes A/S

●

International Flavors

& Fragrances Inc. (IFF)

●

dsm-firmenich

●

Chr. Hansen Holding

A/S

●

DuPont de Nemours,

Inc.

●

Kerry Group plc

●

AB Enzymes

●

Amano Enzyme Inc.

●

Advanced Enzyme

Technologies

●

Aum Enzymes

●

Biocatalysts Ltd.

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Food Enzymes Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Food Enzymes Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Food Enzymes Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Food

Enzymes Market

1.3.2.Source of Global Food

Enzymes Market

1.3.3.Application of Global Food

Enzymes Market

1.3.4.Region of Global Food

Enzymes Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Food Enzymes Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Food Enzymes Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Food Enzymes Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 -

2033

4.1.1.Carbohydrases

4.1.2.Proteases

4.1.3.Lipases

4.1.4.Others

5. Global

Food Enzymes Market Estimates

& Forecast Trend Analysis, by Source

5.1.

Global

Food Enzymes Market Revenue (US$ Bn) Estimates and Forecasts, by Source, 2020 -

2033

5.1.1.Microorganisms

5.1.2.Plants

5.1.3.Animals

6. Global

Food Enzymes Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Food Enzymes Market Revenue (US$ Bn) Estimates and Forecasts, by Application

2020 - 2033

6.1.1.Bakery

6.1.2.Dairy

6.1.3.Beverages

6.1.4.Nutraceuticals

6.1.5.Others

7. Global

Food Enzymes Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Food Enzymes Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 -

2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Food

Enzymes Market: Estimates &

Forecast Trend Analysis

8.1. North America Food Enzymes

Market Assessments & Key Findings

8.1.1.North America Food Enzymes

Market Introduction

8.1.2.North America Food Enzymes

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Type

8.1.2.2.

By Source

8.1.2.3.

By Application

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Food

Enzymes Market: Estimates &

Forecast Trend Analysis

9.1. Europe Food Enzymes Market

Assessments & Key Findings

9.1.1.Europe Food Enzymes Market

Introduction

9.1.2.Europe Food Enzymes Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Source

9.1.2.3.

By Application

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Food

Enzymes Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Food Enzymes Market Introduction

10.1.2.

Asia

Pacific Food Enzymes Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Source

10.1.2.3.

By Application

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Food

Enzymes Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Food Enzymes Market Introduction

11.1.2. Middle

East & Africa

Food Enzymes Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Source

11.1.2.3.

By Application

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Food Enzymes Market: Estimates &

Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Food Enzymes

Market Introduction

12.1.2. Latin America Food Enzymes

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Source

12.1.2.3.

By Application

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Food Enzymes Market

Product Mapping

14.2. Global Food Enzymes Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

14.3. Global Food Enzymes Market

Tier Structure Analysis

14.4. Global Food Enzymes Market

Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Novozymes A/S

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

International Flavors & Fragrances Inc. (IFF)

15.3.

dsm-firmenich

15.4.

Chr. Hansen Holding A/S

15.5.

DuPont de Nemours, Inc.

15.6.

Kerry Group plc

15.7.

AB Enzymes

15.8.

Amano Enzyme Inc.

15.9.

Advanced Enzyme Technologies

15.10.

Aum Enzymes

15.11.

Biocatalysts Ltd.

15.12.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables