Food Flavors Market Size and Forecast (2025 – 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type (Natural, Synthetic); By Form (Liquid & Gel, Dry); By Flavor (Chocolate, Fruit & Nut, Vanilla, Spices & Savory, Others); By Application (Food, Beverages, Others); and Geography

2025-08-13

Consumer Products

Jaya Bundele (Research Analyst)

Description

Food Flavors Market Overview

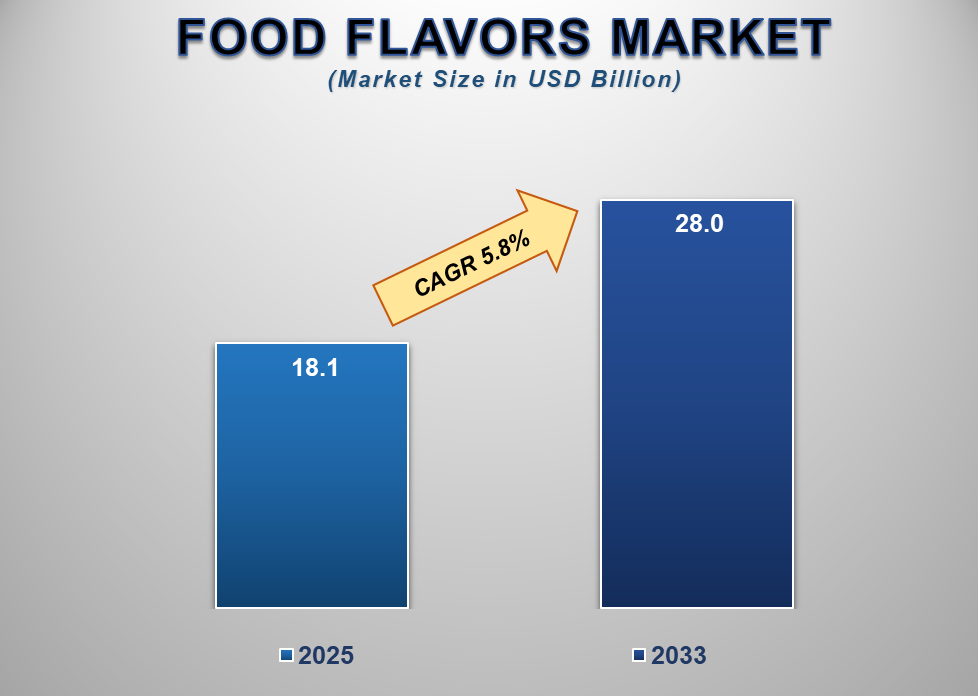

The Global Food Flavors Market size is witnessing steady growth, driven by evolving consumer preferences, increasing demand for natural and clean-label products, and continuous innovation in flavor technologies. According to market analysis, the Food Flavors Market is projected to grow from USD 18.1 billion in 2025 to USD 28.0 billion by 2033, registering a compound annual growth rate (CAGR) of 5.8% during the forecast period.

Food flavors play a crucial role in enhancing the sensory experience of food products, contributing significantly to their market appeal and consumer acceptance. The market is primarily driven by rising global demand for processed and packaged foods, particularly in urban areas. Rapidly changing dietary patterns, increased consumption of convenience foods, and the expansion of the food and beverage industry have amplified the need for innovative and diverse flavor solutions. Natural flavors are gaining particular traction due to growing health consciousness and consumer preference for plant-based, organic, and sustainable products. Furthermore, increasing investments in R&D and advanced flavor encapsulation technologies contribute to market expansion. Trends such as sugar reduction, plant-based foods, and functional beverages continue to shape demand for new flavor profiles. Major players are focusing on expanding their portfolios to cater to diverse regional tastes and regulatory standards.

Food Flavors Market Drivers and Opportunities

Rising demand for natural food flavours and clean-label food

products is anticipated to lift the Food Flavors market during the forecast

period.

One of the primary growth drivers

for the global Food Flavors Market is the rising consumer preference for

natural, organic, and clean-label products. Modern consumers are increasingly

mindful of ingredient transparency and are shifting away from synthetic

additives due to health concerns related to artificial substances. This trend

is especially prevalent in developed regions such as North America and Europe,

where regulatory frameworks like the FDA and EFSA emphasize clean-label

standards. Natural food flavors derived from plant, fruit, and spice extracts

are seeing heightened demand across categories such as beverages, dairy,

bakery, and snacks. Major food manufacturers are reformulating existing

products and developing new lines using natural flavors to meet consumer

expectations and comply with evolving regulations. The growing popularity of

plant-based diets further reinforces the importance of the natural food colors

& flavors market, as companies seek to replicate traditional taste profiles

in meat alternatives, dairy substitutes, and functional beverages. In response

to this trend, industry leaders are investing heavily in R&D, sustainable

sourcing practices, and advanced flavor extraction techniques such as CO2

extraction and cold-press methods, ensuring both product quality and regulatory

compliance. This increasing preference for natural and clean-label products is

expected to drive substantial growth in the Food Flavors market throughout the

forecast period.

Rising demand for exotic

and regional flavor profiles is anticipated to lift the Food Flavors market

during the forecast period.

The Food Flavors Market is significantly influenced by consumers' growing interest in exotic and regionally inspired flavor profiles. Globalization, increased international travel, and the rise of multicultural culinary trends have led to heightened consumer curiosity about new and unique flavors. Food and beverage companies are responding by introducing products featuring flavors from diverse regions, including Asian spices, Latin American fruits, Middle Eastern herbs, and African-inspired seasonings. This trend is particularly visible in the snacks, beverages, and ready-to-eat meals segments, where flavor innovation directly impacts product differentiation and brand competitiveness. Moreover, millennial and Gen Z consumers, who are more open to experimenting with food and beverage choices, are driving demand for bold, authentic, and fusion flavors. To capitalize on this opportunity, flavor manufacturers are developing customized solutions that cater to local taste preferences while maintaining global appeal. Advanced technologies such as flavor modulation and flavor masking allow for the creation of complex, layered flavor profiles without compromising nutritional or clean-label attributes. Companies are also leveraging data analytics and AI-driven insights to predict emerging flavor trends and optimize their product development pipelines. The increasing popularity of exotic and regional flavor profiles represents a strong growth avenue for the Food Flavors Market in the coming years.

Opportunity for the Food Flavors Market

Expanding applications of

flavors in functional and health-focused products are create significate

opportunities for the Food Flavors market.

A key opportunity driving the growth of the global Food Flavors Market is the expanding application of flavors in functional and health-focused food and beverage products. As consumers become more health-conscious, there is a growing demand for products that offer both nutritional benefits and appealing taste profiles. Functional foods and beverages fortified with vitamins, minerals, probiotics, and plant-based proteins often face challenges in taste masking, making flavor solutions crucial to their market success. This trend spans across diverse product categories, including sports nutrition drinks, meal replacement products, fortified dairy products, plant-based alternatives, and dietary supplements. Flavor manufacturers are increasingly collaborating with health and wellness brands to develop specialized flavor systems that enhance palatability while supporting the functional integrity of the products. Innovations such as encapsulated flavors, natural sweeteners, and botanical extracts are being utilized to create balanced and enjoyable sensory experiences. Additionally, regulatory approvals for health claims and clean-label positioning further encourage the integration of sophisticated flavor technologies in this segment. As consumers prioritize both taste and health benefits, the role of flavors in functional and health-focused products is expected to expand significantly, offering robust opportunities for growth in the Food Flavors Market over the forecast period.

Food Flavors Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 18.1 Billion |

|

Market Forecast in 2033 |

USD 28.0 Billion |

|

CAGR % 2025-2033 |

5.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Type ●

By Form ●

By Flavor ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Food Flavors Market Report Segmentation Analysis

The global Food Flavors Market

industry analysis is segmented by type, by form, by flavor, by application, and

by region

The Natural segment accounted for the largest market share in

the global Food Flavors market.

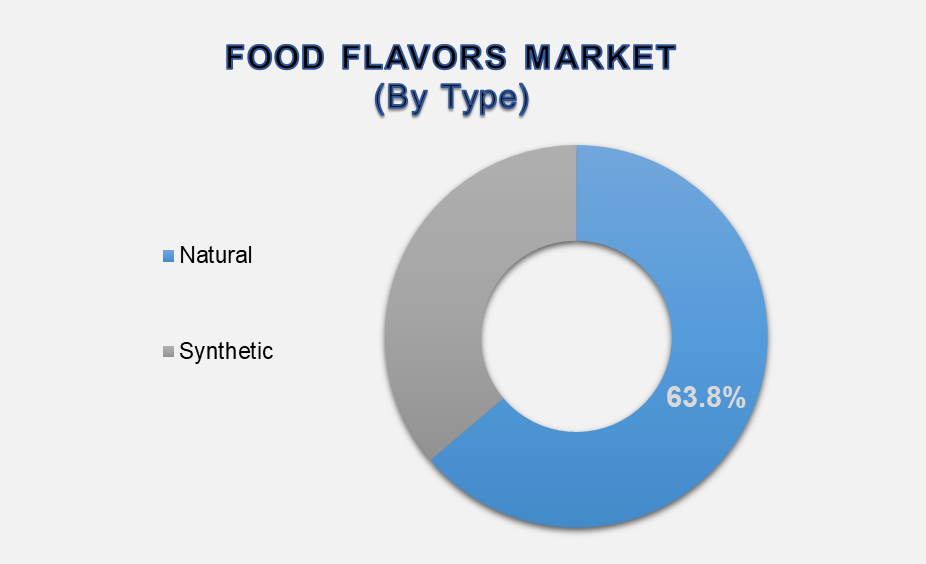

By Type, the market is segmented into Natural and Synthetic flavors. The Natural segment accounted for the largest market share at 63.8% in the global Food Flavors market. This dominant position is driven by growing consumer preference for plant-based, organic, and clean-label ingredients across the food and beverage industry. Increasing regulatory support and awareness regarding the health benefits of natural products have further strengthened this segment. Major food manufacturers are actively expanding their natural flavor portfolios through acquisitions and partnerships with natural ingredient suppliers.

The Chocolate segment accounted for the largest market share

in the global Food Flavors market.

By Flavor, the market is

segmented into Chocolate, Fruit & Nut, Vanilla, Spices & Savory, and

Others. The Chocolate segment holds the largest share in the global Food

Flavors market due to its widespread use across multiple product categories, including

bakery, confectionery, dairy products, and beverages. Chocolate remains a

highly preferred flavor among all age groups and is considered a staple in

numerous regional cuisines. The consistent demand for chocolate-flavored

products is supported by innovation in cocoa sourcing, flavor blends, and

premium product offerings. Growing consumption of chocolate-based products in

emerging markets and increasing trends towards dark and functional chocolate

varieties further enhance this segment's dominant position.

The Food segment holds the largest share in the global Food

Flavors market.

By Application, the market is

segmented into Food, Beverages, and Others. The Food segment holds the largest

share owing to the extensive use of flavors in everyday cooking, packaged

foods, ready-to-eat meals, and frozen foods. Increasing global demand for

flavorful and convenient food options drives the continued dominance of this

segment. The rise in processed food consumption, particularly in urban centers,

and the demand for ethnic and fusion cuisine flavors support strong growth in

the food application category. Additionally, ongoing flavor innovation tailored

to specific cuisines and health-conscious preferences further solidifies the

segment's leadership.

The following segments are part

of an in-depth analysis of the global Food Flavors Market:

|

Market Segments |

|

|

By Type |

●

Natural ●

Synthetic |

|

By Form |

●

Liquid & Gel ●

Dry |

|

By Flavor |

●

Chocolate ●

Fruit & Nut ●

Vanilla ●

Spices & Savory ●

Others |

|

By Application |

●

Food o Dairy Products o Bakery & Confectionery o Supplements & Nutrition Products o Meat & Seafood Products o Snacks o Pet Foods o Sauces, Dressings & Condiments o Others ●

Beverages o Juices & Juice Concentrates o Functional Beverages o Alcoholic Beverages o Carbonated Soft Drinks o Others ●

Others |

Food Flavors Market Share Analysis by Region

The North America region is projected to hold the largest share of the global Food Flavors market over the forecast period.

North America holds the dominant

position in the global Food Flavors market, accounting for approximately 35.5%

of the total market share. This leadership is primarily driven by the region’s

well-established food and beverage industry, coupled with high consumer demand

for innovative and clean-label products. The presence of leading flavor

manufacturers such as International Flavors & Fragrances (IFF), McCormick

& Company, and Sensient Technologies further strengthens North America’s

position. Advanced R&D facilities, strong regulatory frameworks, and

consumer trends favoring organic and functional foods contribute to the

continuous demand for new and natural flavor solutions. Major companies are

actively investing in flavor innovation, plant-based products, and

sugar-reduction technologies to cater to evolving consumer preferences.

Additionally, the region benefits from a mature retail sector and robust

foodservice channels that support sustained growth in the food flavors market.

In contrast, the Asia Pacific is forecasted to witness the highest CAGR in the Food Flavors market during the forecast period. Rapid urbanization, expanding middle-class populations, and growing demand for packaged and convenience foods in countries like China, India, and Japan are key factors fueling this accelerated growth. The region is experiencing a surge in domestic food production, supported by government initiatives to boost the food processing sector. Local flavor preferences and rising adoption of Western culinary trends are driving flavor diversification. Moreover, increasing awareness of health and wellness products is contributing to the rising demand for natural and functional flavor ingredients. As a result, the Asia Pacific is expected to emerge as a major growth hub for the global Food Flavors market during the forecast period

Food Flavors Market Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of products. Some of the key players are Givaudan, International Flavors &

Fragrances (IFF), Firmenich, Symrise, Kerry Group, Sensient Technologies,

Takasago, Mane.

Global Food Flavors

Market Recent Developments News:

- In October

2024 – Synergy Flavors unveiled its innovative ‘Heat & Fire’ flavor

portfolio, responding to growing consumer demand for bold, spicy taste

experiences. The collection features natural flavors and concentrated

pastes tailored for food manufacturers, enabling them to infuse

customizable heat levels into diverse products like ready meals,

plant-based proteins, and baked goods. This versatile flavor system

empowers brands to create differentiated, trend-forward products aligned

with evolving consumer preferences.

- In October 2024 – Givaudan Taste & Wellbeing commenced

construction on its USD 58.31 million production hub in Cikarang,

Indonesia, marking a strategic investment in Southeast Asian market

growth. The 24,000 sqm facility (on a 50,000 sqm land parcel) will

manufacture savory ingredients, sweet flavors, snack powders, and infant

nutrition solutions, with infrastructure designed for future capacity

expansion. This development strengthens Givaudan’s regional supply chain

capabilities while supporting local food innovation.

The Global Food Flavors Market is dominated by a few large

companies, such as

●

Givaudan

●

International Flavors

& Fragrances (IFF)

●

Firmenich

●

Symrise

●

Kerry Group

●

Sensient Technologies

●

Takasago

●

Mane

●

T. Hasegawa

●

Robertet

●

Archer Daniels Midland

(ADM)

●

McCormick &

Company

●

Bell Flavors &

Fragrances

●

Frutarom

●

Döhler

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Food Flavors Market Introduction and Market Overview

- Objectives of the Study

- Global Food Flavors Market Scope and Market Estimation

- Global Food Flavors Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Food Flavors Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Type of Global Food Flavors Market

- Form of Global Food Flavors Market

- Flavor of Global Food Flavors Market

- Application of Global Food Flavors Market

- Region of Global Food Flavors Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Food Flavors Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Food Flavors Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Food Flavors Market Estimates & Forecast Trend Analysis, by Type

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2021 - 2033

- Natural

- Synthetic

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2021 - 2033

- Global Food Flavors Market Estimates & Forecast Trend Analysis, by Form

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Form, 2021 - 2033

- Liquid & Gel

- Dry

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Form, 2021 - 2033

- Global Food Flavors Market Estimates & Forecast Trend Analysis, by Flavor

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Flavor, 2021 - 2033

- Chocolate

- Fruit & Nut

- Vanilla

- Spices & Savory

- Others

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Flavor, 2021 - 2033

- Global Food Flavors Market Estimates & Forecast Trend Analysis, by Application

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Food

- Dairy Products

- Bakery & Confectionery

- Supplements & Nutrition Products

- Meat & Seafood Products

- Snacks

- Pet Foods

- Sauces, Dressings & Condiments

- Others

- Beverages

- Juices & Juice Concentrates

- Functional Beverages

- Alcoholic Beverages

- Carbonated Soft Drinks

- Others

- Others

- Food

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Food Flavors Market Estimates & Forecast Trend Analysis, by region

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Food Flavors Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Food Flavors Market: Estimates & Forecast Trend Analysis

- North America Food Flavors Market Assessments & Key Findings

- North America Food Flavors Market Introduction

- North America Food Flavors Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type

- By Form

- By Flavor

- By Application

- By Country

- The U.S.

- Canada

- North America Food Flavors Market Assessments & Key Findings

- Europe Food Flavors Market: Estimates & Forecast Trend Analysis

- Europe Food Flavors Market Assessments & Key Findings

- Europe Food Flavors Market Introduction

- Europe Food Flavors Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type

- By Form

- By Flavor

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Food Flavors Market Assessments & Key Findings

- Asia Pacific Food Flavors Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Food Flavors Market Introduction

- Asia Pacific Food Flavors Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type

- By Form

- By Flavor

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Food Flavors Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Food Flavors Market Introduction

- Middle East & Africa Food Flavors Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type

- By Form

- By Flavor

- By Application

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Food Flavors Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Food Flavors Market Introduction

- Latin America Food Flavors Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type

- By Form

- By Flavor

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Food Flavors Market Product Mapping

- Global Food Flavors Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Food Flavors Market Tier Structure Analysis

- Global Food Flavors Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Givaudan

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Givaudan

* Similar details would be provided for all the players mentioned below

- International Flavors & Fragrances (IFF)

- Firmenich

- Symrise

- Kerry Group

- Sensient Technologies

- Takasago

- Mane

- Hasegawa

- Robertet

- Archer Daniels Midland (ADM)

- McCormick & Company

- Bell Flavors & Fragrances

- Frutarom

- Döhler

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables