Frozen Pet Food Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Raw Diets, Freeze-Dried & Dehydrated, Frozen Treats, Prepared Frozen Meals), By Pet Type (Dogs, Cats, Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Pet Stores, Online Retail, Veterinary Clinics), and Geography

2025-12-19

Consumer Products

Jaya Bundele (Research Analyst)

Description

Frozen Pet

Food Market Overview

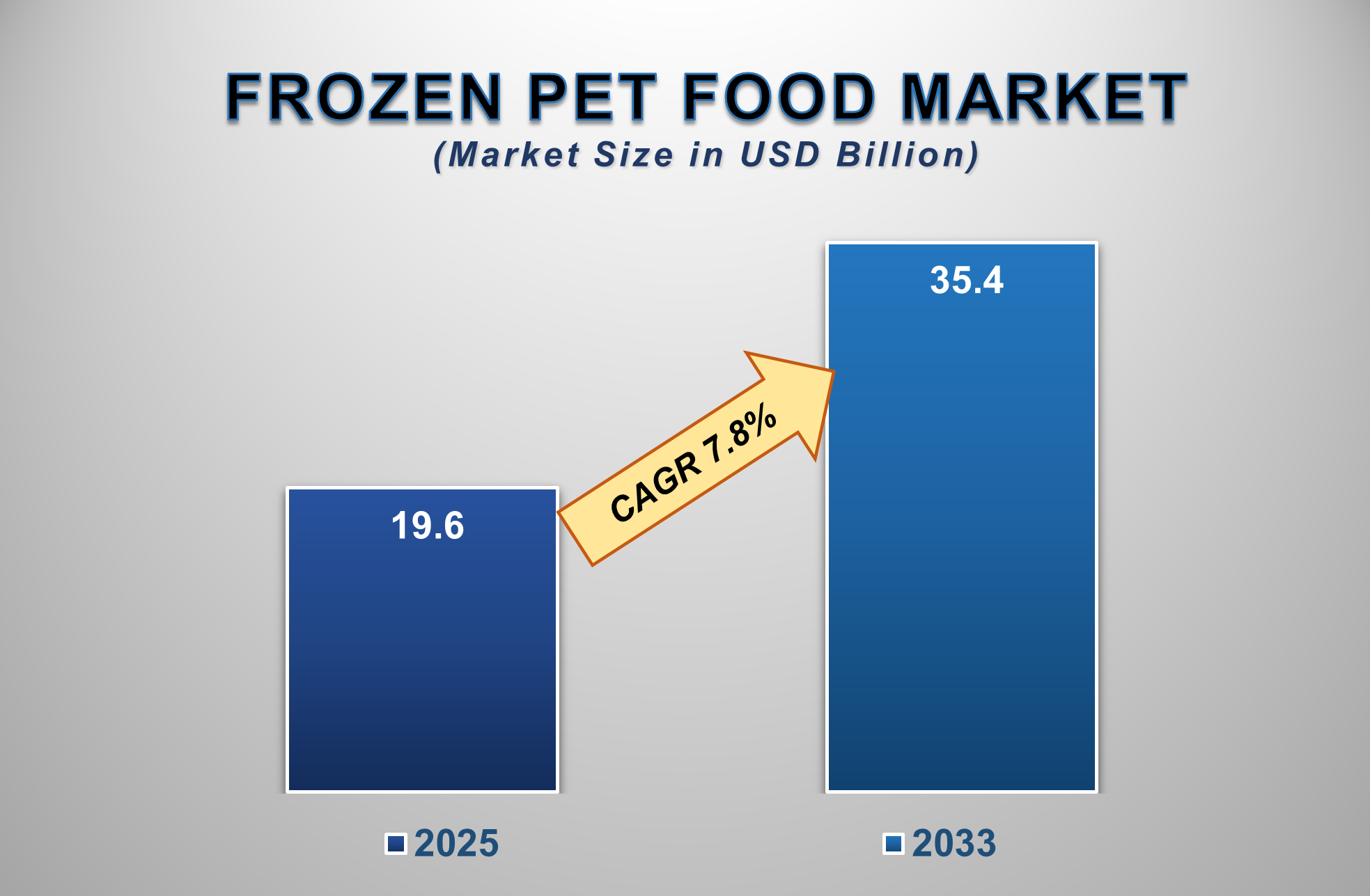

The Frozen Pet Food Market is set for significant expansion from 2025 to 2033, driven by the humanization of pets, rising awareness of pet nutrition, and growing demand for fresh, minimally processed food options. The market is expected to be valued at USD 19.6 billion in 2025 and is projected to reach USD 35.4 billion by 2033, registering a CAGR of 7.8% during the forecast period.

Frozen pet food encompasses a range of products, including raw (BARF—Biologically Appropriate Raw Food), gently cooked frozen meals,

freeze-dried raw, and frozen treats. These products are perceived as healthier,

more natural alternatives to traditional kibble and canned food, offering

higher moisture content, preserved nutrients, and limited artificial additives.

The market growth is fueled by pet owners' increasing focus on ingredient

transparency, functional benefits (e.g., improved coat health, digestion,

and energy), and the prevention of pet obesity and

allergies. North America leads the market due to high pet ownership and

premiumization trends, while Asia-Pacific is witnessing the fastest growth,

spurred by urbanization, rising disposable income, and changing attitudes

toward pet care.

Frozen Pet Food Market Drivers and Opportunities

Increasing Pet Humanization and Demand for

Premium, Natural Nutrition Is the Primary Market Driver

The trend of treating pets as family members is the most

influential driver. Pet owners are increasingly seeking human-grade,

high-quality food options that mirror their own dietary preferences for fresh,

clean-label, and nutrient-dense ingredients. Concerns over recalls and the

perceived limitations of ultra-processed dry food have led many to explore

frozen raw or gently cooked diets. The growing awareness of the link between

diet and pet health issues (allergies, dental problems, obesity) is pushing owners

toward specialized frozen formulations. Social media, pet influencers, and

endorsements from veterinarians and breeders further educate and motivate

consumers, normalizing the transition to premium frozen diets. The number of

pet owners in the United States has demonstrated a robust and sustained

increase over recent years, solidifying the nation's status as a pet-loving

society. This growth is propelled by several key demographic and societal

trends.

The primary driver has been a significant rise in

millennial and Gen Z pet ownership. These generations are delaying major life

milestones like marriage and children, often opting for pets as companions and

"starter families." Furthermore, the widespread shift to remote and

hybrid work models, accelerated by the pandemic, has created more flexible

lifestyles conducive to pet care. This has reduced a major historical barrier

to ownership.

Pet adoption has also been amplified by changing household

structures, including a growing number of single-person households and couples

without children, where pets fulfill crucial

companionship roles. Increased awareness of animal welfare and the promotion of

adoption through shelters and social media have made acquiring a pet more

accessible and socially encouraged than ever before. As a result, national

surveys consistently show that approximately 66% to 70% of U.S. households now

own a pet, translating to nearly 90 million homes.

Growth of E-commerce and Direct-to-Consumer (DTC)

Subscription Models Are Accelerating Market Adoption

The convenience of online shopping and subscription

services has made purchasing bulky frozen goods seamless. Specialty online pet

retailers and brand-owned DTC channels offer home delivery of insulated

packages, simplifying the logistics of frozen food. Subscription models ensure

customer loyalty and predictable revenue streams for manufacturers while

providing convenience for owners. This channel also serves as a key platform

for education, allowing brands to communicate the benefits of frozen nutrition

directly to consumers. The expansion of cold chain logistics capabilities

globally is making frozen pet food more accessible beyond traditional

brick-and-mortar stores.

Innovation in Product Formats, Functional Ingredients, and Sustainability

Present Significant Opportunities.

Continuous innovation is creating new market segments.

Blended formats (e.g., kibble mixed with freeze-dried raw bits), single-protein

recipes for sensitive pets, and life-stage-specific frozen meals are gaining

popularity. The integration of functional ingredients like probiotics, omega

fatty acids, and superfoods (e.g., blueberries, kale) adds a health and wellness angle. Sustainability is a major

opportunity area, with brands exploring eco-friendly packaging (recyclable,

compostable), ethically sourced ingredients, and carbon-neutral supply chains

to appeal to environmentally conscious consumers. Furthermore, personalization

through DNA-based or health-condition-specific frozen meal plans, facilitated

by emerging tech and data analytics, represents a high-growth frontier for

premium offerings.

Frozen Pet Food Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 19.6 Billion |

|

Market Forecast in 2033 |

USD 35.4 Billion |

|

CAGR % 2025-2033 |

7.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Service Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Pet Type ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Frozen Pet Food Market Report Segmentation

Analysis

The

global Medica Spa Market is segmented by Product Type, Pet Type, Distribution

Channel, and Region.

Raw Diets Are Anticipated to Command the Largest

Market Share in 2025

Raw frozen diets (including patties, nuggets, and chubs) dominate the Product Type segment, driven by a strong belief among pet owners in the benefits of a species-appropriate, uncooked diet. This category's leadership is anchored in its perception as the most "natural" option, believed to improve dental health, digestion, skin, coat, and energy levels. Despite concerns over bacterial safety, advances in High-Pressure Processing (HPP) to eliminate pathogens without cooking have alleviated some fears and boosted adoption. The passionate advocacy from a core consumer base and the proliferation of specialty brands dedicated to raw nutrition ensure this segment's continued revenue leadership.

The Dog Segment Holds the Largest Share by Pet

Type

Dogs

represent the primary pet type segment, accounting for the majority of frozen

food sales. This dominance stems from larger portion sizes, higher pet

consumption, and a longer history of dietary diversification for dogs compared

to other pets. Dog owners are highly engaged in trends like raw feeding and

functional nutrition. The cat segment is, however, growing at an accelerated

rate as owners become more aware of the high-protein, moisture-rich needs of

felines, which align perfectly with frozen and freeze-dried product benefits.

Online Retail Channels Are the Fastest-Growing

Distribution Channel

While

Specialty Pet Stores currently lead in offering expert advice and a curated

selection, Online Retail is the fastest-growing distribution channel. The

convenience of home delivery for heavy, frozen products, coupled with the

ability to easily compare brands, read reviews, and enroll in subscriptions,

makes online platforms highly attractive. The DTC model, in particular, allows

brands to build direct relationships with consumers, offer personalized

recommendations, and control the cold chain from factory to doorstep, ensuring

product integrity.

The following segments are

part of an in-depth analysis of the global Frozen Pet Food Market:

|

Market

Segments |

|

|

By Product

Type |

●

Raw Diets ●

Freeze-Dried &

Dehydrated ●

Frozen Treats ●

Prepared Frozen

Meals |

|

By Pet Type |

●

Dogs ●

Cats ●

Others (Birds,

Reptiles, etc.) |

|

By Distribution Channel |

●

Supermarkets/Hypermarkets ●

Specialty Pet Stores ●

Online Retail ●

Veterinary Clinics |

Frozen Pet Food Market Share Analysis by Region

North America is anticipated to hold the largest

portion of the frozen pet food market globally throughout the forecast period.

North

America's leadership is attributed to its mature pet care market, high pet

ownership rates, high disposable income, and

early adoption of premiumization trends. The United States is the leader, with a high concentration of pioneering brands, robust

cold chain infrastructure, and widespread consumer awareness. Europe follows

closely, with strong demand in Western Europe driven by stringent pet food

quality standards and a natural/organic food culture. The Asia-Pacific region

is expected to be the fastest-growing, fueled by rapid urbanization, a growing

middle class, increasing pet adoption, and the gradual shift from basic feed to

premium nutrition in countries like China, Japan, and Australia.

Frozen Pet Food Market Competition Landscape

Analysis

The global market is

moderately consolidated, with a mix of large, diversified pet food corporations

and agile, niche-focused specialist brands. Competition revolves around

ingredient quality, sourcing transparency, nutritional science, safety

standards (e.g., HPP), brand trust, and supply chain reliability. Leading

players are investing heavily in R&D for novel formulations and acquiring

successful niche brands to gain market share. Marketing focuses heavily on

educational content about pet health, sustainability claims, and leveraging

social media pet influencers. Strategic partnerships with veterinary networks

and pet retailers are crucial for credibility and shelf space.

Global Frozen Pet Food Market Recent Developments

News:

- In January 2025, Nestlé Purina PetCare launched a new line of

veterinary-exclusive frozen therapeutic diets for pets with specific

health conditions.

- In November 2024, Champion Petfoods (Orijen)

expanded its freeze-dried raw product range with a new

"WholePrey" line, targeting the premium dog food segment in

North America and Europe.

- In September 2024, The Farmer's Dog announced a major facility

expansion to increase production capacity for its fresh, pre-portioned

cooked meals, signalling increased competition in the prepared frozen

segment.

- In July 2024, General Mills (Blue Buffalo) acquired a leading

independent raw frozen pet food company to strengthen its position in the

high-growth natural pet food category.

The Global Frozen Pet Food Market Is Dominated by

a Few Large Companies, such as

●

Nestlé Purina PetCare

●

Mars, Incorporated

●

General Mills, Inc.

●

The J.M. Smucker

Company

●

Champion Petfoods LP

●

The Farmer's Dog

●

Stella & Chewy's

LLC

●

Primal Pet Foods, Inc.

●

Tyson Foods, Inc.

(True Chews)

●

Freshpet, Inc.

●

Ainsworth Pet

Nutrition

●

Simmons Pet Food, Inc.

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Frozen Pet Food

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Frozen Pet Food Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Frozen Pet Food

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Frozen

Pet Food Market

1.3.2.Pet Type of Global Frozen

Pet Food Market

1.3.3.Distribution Channel of Global

Frozen Pet Food Market

1.3.4.Region of Global Frozen

Pet Food Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Frozen Pet Food Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Frozen Pet Food Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Frozen Pet Food Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Raw Diets

4.1.2.Freeze-Dried &

Dehydrated

4.1.3.Frozen Treats

4.1.4.Prepared Frozen Meals

5. Global

Frozen Pet Food Market Estimates

& Forecast Trend Analysis, by Pet Type

5.1.

Global

Frozen Pet Food Market Revenue (US$ Bn) Estimates and Forecasts, by Pet Type, 2020

- 2033

5.1.1.Dogs

5.1.2.Cats

5.1.3.Others (Birds, Reptiles,

etc.)

6. Global

Frozen Pet Food Market Estimates

& Forecast Trend Analysis, by Distribution Channel

6.1.

Global

Frozen Pet Food Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

6.1.1.Supermarkets/Hypermarkets

6.1.2.Specialty Pet Stores

6.1.3.Online Retail

6.1.4.Veterinary Clinics

7. Global

Frozen Pet Food Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Frozen Pet Food Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Frozen

Pet Food Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Frozen Pet Food Market Assessments & Key Findings

8.1.1.North America Frozen Pet

Food Market Introduction

8.1.2.North America Frozen Pet

Food Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Pet Type

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Frozen

Pet Food Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Frozen Pet Food Market Assessments & Key Findings

9.1.1.Europe Frozen Pet Food

Market Introduction

9.1.2.Europe Frozen Pet Food

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Pet Type

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Frozen

Pet Food Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Frozen Pet Food Market Introduction

10.1.2.

Asia

Pacific Frozen Pet Food Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Pet Type

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Frozen

Pet Food Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Frozen Pet Food Market Introduction

11.1.2.

Middle East & Africa Frozen Pet Food Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Pet Type

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Frozen Pet Food Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Frozen Pet Food Market Introduction

12.1.2.

Latin

America Frozen Pet Food Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Pet Type

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Frozen Pet Food Market Product Mapping

14.2.

Global

Frozen Pet Food Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

14.3.

Global

Frozen Pet Food Market Tier Structure Analysis

14.4.

Global

Frozen Pet Food Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Nestlé Purina PetCare

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Mars,

Incorporated

15.3. General

Mills, Inc.

15.4. The J.M.

Smucker Company

15.5. Champion

Petfoods LP

15.6. The Farmer's

Dog

15.7. Stella &

Chewy's LLC

15.8. Primal Pet

Foods, Inc.

15.9. Tyson Foods,

Inc. (True Chews)

15.10. Freshpet,

Inc.

15.11. Ainsworth Pet

Nutrition

15.12. Simmons Pet

Food, Inc.

15.13. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables