Gaming Console Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Home Console, Handheld Console), By End-use (Residential, Commercial), By Application (Gaming, Non-Gaming), and Geography

2026-02-17

Media & Entertainment

Jaya Bundele (Research Analyst)

Description

Gaming Console Market

Overview

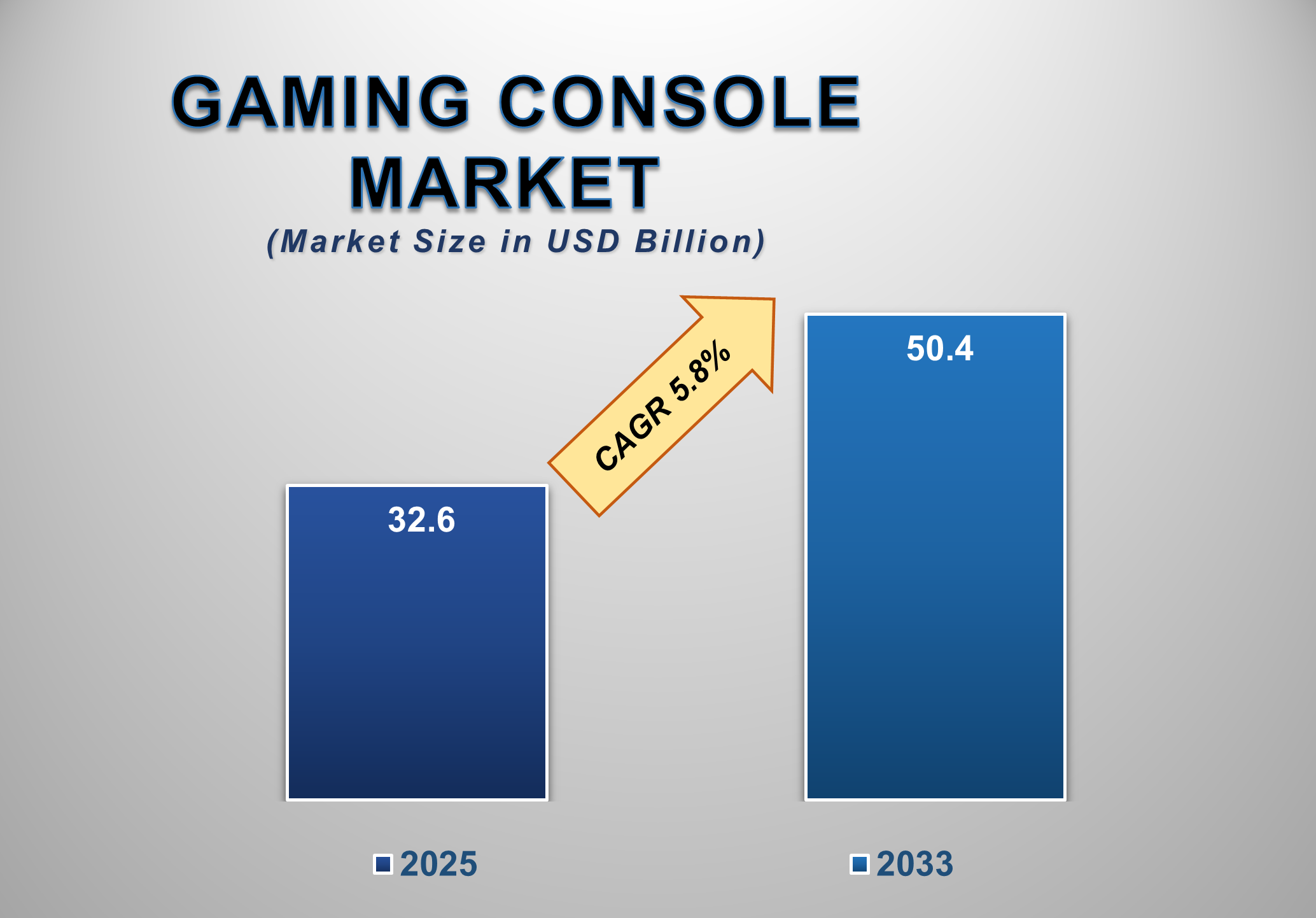

The global Gaming Console Market represents a core segment of the interactive entertainment industry, driven by rapid advancements in gaming technology, growing consumer demand for immersive experiences, and the expanding global gamer population. Gaming consoles serve as dedicated hardware platforms for video gaming, entertainment streaming, and increasingly, social interaction. In 2025, the global gaming console market is valued at USD 32.6 billion and is projected to reach USD 50.4 billion by 2033, growing at a CAGR of 5.8% during the forecast period.

Market expansion is fueled by

continuous innovation in console hardware, including enhanced graphics

processing units (GPUs), faster solid-state drives (SSDs), cloud connectivity,

and support for high-resolution gaming formats such as 4K and 8K. Leading console

manufacturers are also focusing on ecosystem development, integrating

subscription-based gaming services, digital storefronts, and cross-platform

compatibility to enhance user engagement and lifetime value.

Gaming Console Market Drivers and Opportunities

Rising Demand for Immersive and High-Performance Gaming

Experiences Is Driving Market Growth

The growing demand for immersive,

high-performance gaming experiences is a primary driver of the global gaming

console market. Modern gamers increasingly seek realistic visuals, advanced

physics engines, fast load times, and seamless multiplayer experiences. Gaming

consoles are specifically designed to deliver optimized performance for these

requirements, making them a preferred choice over general-purpose computing

devices for many users.

Next-generation consoles incorporate

cutting-edge hardware components, including custom-designed CPUs and GPUs, ray

tracing technology, and ultra-fast SSD storage. These advancements

significantly enhance gameplay realism, reduce latency, and enable expansive

open-world gaming environments. As a result, gamers are increasingly upgrading

from older console generations to access improved performance and exclusive

game titles. In addition, the integration of virtual reality (VR), augmented

reality (AR), and haptic feedback technologies is elevating the gaming

experience further. Console manufacturers are investing in proprietary

controllers, accessories, and peripherals to deepen immersion and differentiate

their platforms. As consumer expectations continue to rise, demand for advanced

gaming consoles is expected to remain strong, supporting sustained market

growth.

Expansion of Digital

Gaming Ecosystems and Subscription Services Is Accelerating Adoption

The rapid expansion of digital gaming

ecosystems and subscription-based services is another major driver propelling

the gaming console market. Console manufacturers are increasingly shifting

toward service-oriented business models that extend beyond hardware sales.

Subscription offerings such as game libraries, cloud gaming access, and online

multiplayer services provide recurring revenue streams and strengthen customer

loyalty. Digital distribution has transformed how games are purchased and

consumed. Gamers can instantly download titles, access downloadable content

(DLC), and receive regular updates without relying on physical media. This

convenience, combined with frequent promotional offers and bundled

subscriptions, enhances the overall value proposition of console ownership.

Furthermore, cloud gaming integration

allows users to stream games directly to consoles, reducing dependency on local

hardware performance and expanding access to a broader range of titles. These

ecosystem-driven strategies are not only increasing console adoption but also

extending product lifecycles, making digital services a critical growth driver

for the market.

Growth of Gaming in

Emerging Markets and Cross-Platform Integration Is Creating New Opportunities

The expanding gaming population in

emerging markets presents a significant opportunity for the global gaming

console market. Rapid urbanization, increasing internet penetration, and rising

disposable incomes are transforming gaming from a niche hobby into a mainstream

entertainment activity across Asia Pacific, Latin America, and parts of the

Middle East.

Asia Pacific is expected to witness the

highest CAGR during the forecast period, driven by a young demographic,

expanding esports culture, and growing acceptance of console gaming.

Manufacturers are increasingly tailoring pricing strategies, content localization,

and distribution models to capture demand in these markets. Additionally,

cross-platform gaming and interoperability between consoles, PCs, and mobile

devices are opening new growth avenues. Gamers now expect seamless gameplay

across devices, shared progress, and unified multiplayer experiences. Console

makers that successfully integrate cross-platform functionality and cloud-based

gaming solutions are well-positioned to capitalize on this evolving landscape.

Gaming Console Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 32.6 Billion |

|

Market Forecast in 2035 |

USD 50.4 Billion |

|

CAGR % 2025-2035 |

5.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

Type, End-use, Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Gaming Console Market Report Segmentation Analysis

The Global Gaming Console Market

Industry Analysis Is Segmented By Type, End-use, Application, and by Region.

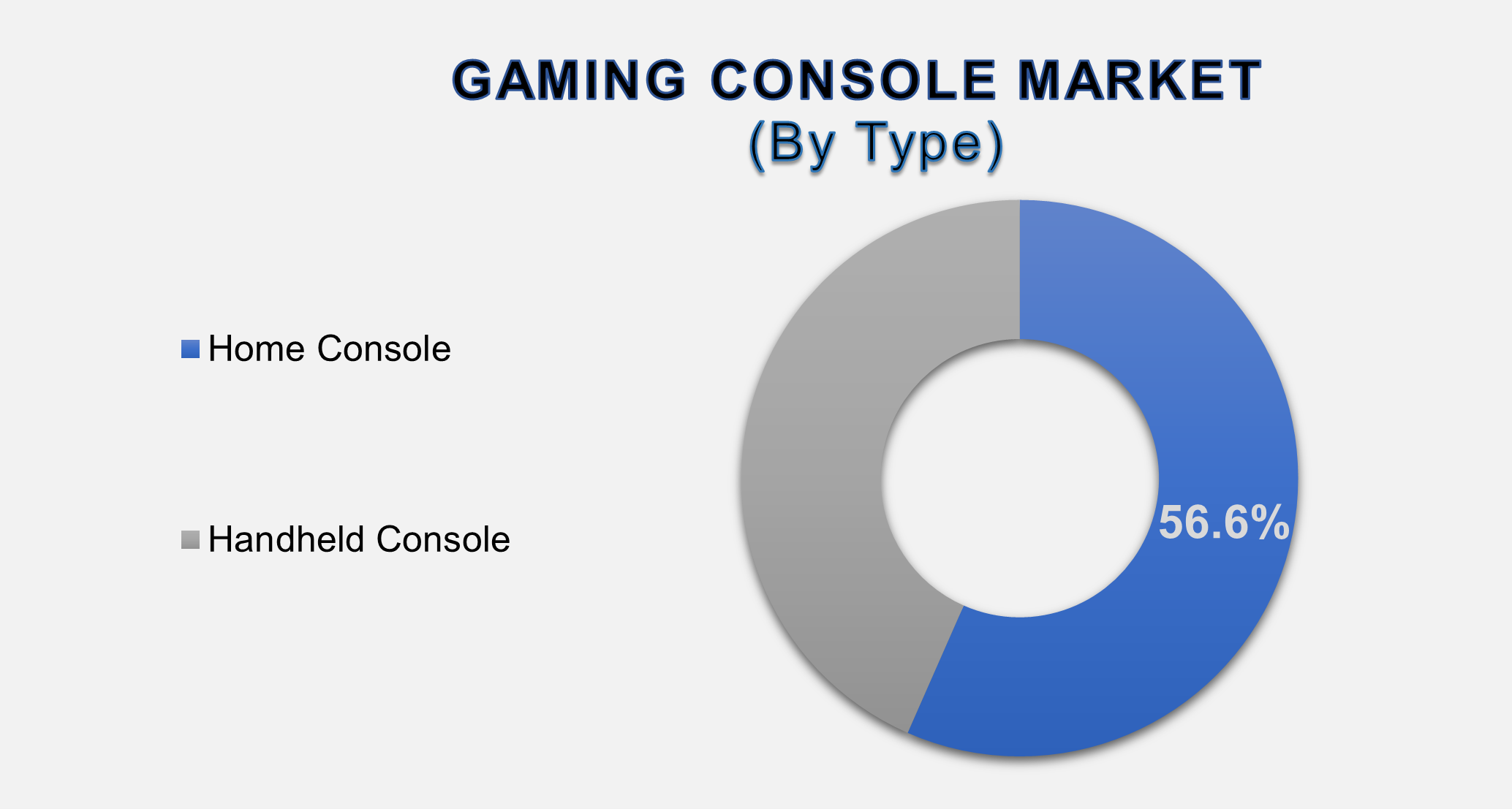

Home Console

Segment Accounted for the Largest Market Share in the Global Gaming Console

Market

The home console segment accounted for the largest share of the global gaming console market, contributing 56.6% of total revenue. Home consoles are designed to deliver high-end gaming experiences with advanced graphics, powerful processors, and support for large-screen displays. These systems are particularly popular among core gamers and households seeking premium entertainment experiences. Home consoles benefit from exclusive game titles, strong developer support, and robust online ecosystems. Their ability to function as all-in-one entertainment hubs—supporting gaming, streaming, and multimedia applications—further enhances their appeal. As next-generation home consoles continue to evolve, this segment is expected to maintain its dominant position throughout the forecast period.

Residential End-use Segment Dominated the

Global Market

The residential segment dominates the gaming console

market by end-use, driven by widespread household adoption and increasing

leisure spending on home entertainment. Gaming consoles have become central to

family entertainment setups, offering multiplayer gaming, streaming services,

and social connectivity. The rise of stay-at-home entertainment trends and

digital content consumption has further strengthened residential demand.

Console manufacturers are increasingly targeting households with bundled offerings,

parental controls, and family-friendly content, reinforcing the dominance of

this segment.

Gaming Application Segment Held a Significant

Market Share

The gaming application segment holds a significant

share of the market, as consoles are primarily designed for interactive gaming

experiences. High-quality game libraries, exclusive franchises, and online

multiplayer features drive sustained engagement within this segment. While

non-gaming applications such as streaming and media playback contribute

additional value, gaming remains the core function and revenue driver for

console platforms. Continued innovation in game design and interactive

technologies is expected to sustain strong demand for gaming-focused consoles.

The following segments are part of an in-depth analysis of the global Gaming

Console market:

|

Market Segments |

|

|

By Type |

●

Home Console ●

Handheld Console o

Portable o

Non-Portable |

|

By End User |

●

Residential ●

Commercial |

|

By Application |

●

Gaming ●

Non-Gaming |

Gaming Console Market Share Analysis by Region

North America is anticipated to hold the biggest portion of

the Gaming Console Market globally throughout the forecast period.

North America accounted for 43.1%

of the global gaming console market, making it the largest regional market. The

region benefits from high consumer spending power, early adoption of

next-generation consoles, and a well-established gaming culture. The United

States leads regional demand, supported by strong presence of major console

manufacturers, robust esports ecosystems, and widespread broadband

connectivity.

Asia Pacific is expected to

register the highest CAGR during the forecast period, driven by rapid growth in

the gaming population, rising disposable incomes, and increasing acceptance of

console gaming. Countries such as Japan, China, South Korea, and India are

witnessing expanding demand for gaming consoles, supported by localized

content, esports popularity, and improving digital infrastructure. As console

gaming gains traction alongside mobile gaming, Asia Pacific is poised to become

a key growth engine for the global market.

Gaming Console Market Competition Landscape Analysis

The global gaming console market

is highly competitive and dominated by a mix of established multinational

corporations and emerging hardware innovators. Market competition is centered

on hardware performance, exclusive content, ecosystem strength, and service

offerings. Strategic partnerships with game developers and content creators

play a critical role in shaping competitive positioning.

Global Gaming Console Market Recent Developments News:

- In June

2025 – Microsoft announced a multi-year partnership with AMD to

co-engineer custom silicon for its next-generation Xbox consoles. The

platform is designed to deliver a unified, device-agnostic gaming

experience across living room consoles, handheld devices, and the cloud.

Microsoft is also collaborating with its Windows team to position Windows

as the leading gaming platform, reinforcing its commitment to cross-device

accessibility.

- In June

2025 – Microsoft and ASUS announced the upcoming launch of the ROG Xbox

Ally and ROG Xbox Ally X handheld gaming consoles. Developed in

collaboration, these devices support Xbox Play Anywhere, Game Pass, Xbox

Cloud Gaming (Beta), and Remote Play, enabling console-quality gaming on

the go. They are scheduled for a holiday season release in select markets.

- In June

2025 – Nintendo launched the Nintendo Switch 2, featuring enhanced

hardware performance and an expanded content library. Alongside the

release, a firmware update was rolled out, bringing system stability

improvements and expanding the Nintendo Classics catalog with legacy

GameCube titles, emphasizing innovation and backward compatibility.

The Global Gaming Console Market

Is Dominated by a Few Large Companies, such as

●

Sony Interactive

Entertainment

●

Microsoft

●

Nintendo

●

Atari

●

Sega

●

Valve Corporation

●

Nvidia

●

Razer

●

Mad Catz

●

Hyperkin

●

Analogue

●

SNK

●

Arcade1Up

●

Polymega

●

Evercade

●

Anbernic

●

Retroid

●

AYANEO

●

GPD

●

One-Netbook

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Gaming Console

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Gaming Console Market Scope and Market Estimation

1.2.1.Global Gaming Console Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Gaming Console

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Gaming

Console Market

1.3.2.End User of Global Gaming

Console Market

1.3.3.Application of Global Gaming

Console Market

1.3.4.Region of Global Gaming

Console Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Gaming Console Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Gaming Console Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Gaming Console Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 -

2033

4.1.1.Home Console

4.1.2.Handheld Console

4.1.2.1.

Portable

4.1.2.2.

Non-Portable

5. Global

Gaming Console Market Estimates

& Forecast Trend Analysis, by End User

5.1.

Global

Gaming Console Market Revenue (US$ Bn) Estimates and Forecasts, by End User,

2020 - 2033

5.1.1.Residential

5.1.2.Commercial

6. Global

Gaming Console Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Gaming Console Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Gaming

6.1.2.Non-Gaming

7. Global

Gaming Console Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Gaming Console Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Gaming

Console Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Gaming Console Market Assessments & Key Findings

8.1.1.North America Gaming

Console Market Introduction

8.1.2.North America Gaming

Console Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Type

8.1.2.2. By End User

8.1.2.3. By Application

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Gaming

Console Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Gaming Console Market Assessments & Key Findings

9.1.1.Europe Gaming Console

Market Introduction

9.1.2.Europe Gaming Console

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Type

9.1.2.2. By End User

9.1.2.3. By Application

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Gaming

Console Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Gaming Console Market Introduction

10.1.2.

Asia

Pacific Gaming Console Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

10.1.2.1. By Type

10.1.2.2. By End User

10.1.2.3. By Application

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Gaming

Console Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Gaming Console Market Introduction

11.1.2.

Middle East & Africa Gaming Console Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Type

11.1.2.2. By End User

11.1.2.3. By Application

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Gaming Console Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Gaming Console Market Introduction

12.1.2.

Latin

America Gaming Console Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

12.1.2.1. By Type

12.1.2.2. By End User

12.1.2.3. By Application

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Gaming Console Market Product Mapping

14.2.

Global

Gaming Console Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3.

Global

Gaming Console Market Tier Structure Analysis

14.4.

Global

Gaming Console Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

Sony Interactive Entertainment

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Microsoft

15.3. Nintendo

15.4. Atari

15.5. Sega

15.6. Valve

Corporation

15.7. Nvidia

15.8. Razer

15.9. Mad Catz

15.10. Hyperkin

15.11. Analogue

15.12. SNK

15.13. Arcade1Up

15.14. Polymega

15.15. Evercade

15.16. Anbernic

15.17. Retroid

15.18. AYANEO

15.19. GPD

15.20. One-Netbook

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables