Gaming Laptops Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Processor Type (Intel, AMD, Others), By GPU Type (NVIDIA, AMD Radeon, Intel Arc, Others), By Display Size (Below 15 Inches, 15–17 Inches, Above 17 Inches), By End User (Professional Gamers, Casual Gamers, Game Developers, eSports Organizations), By Distribution Channel (Online, Offline) And Geography

2025-11-27

Consumer Products

Jaya Bundele (Research Analyst)

Description

Gaming Laptops Market

Overview

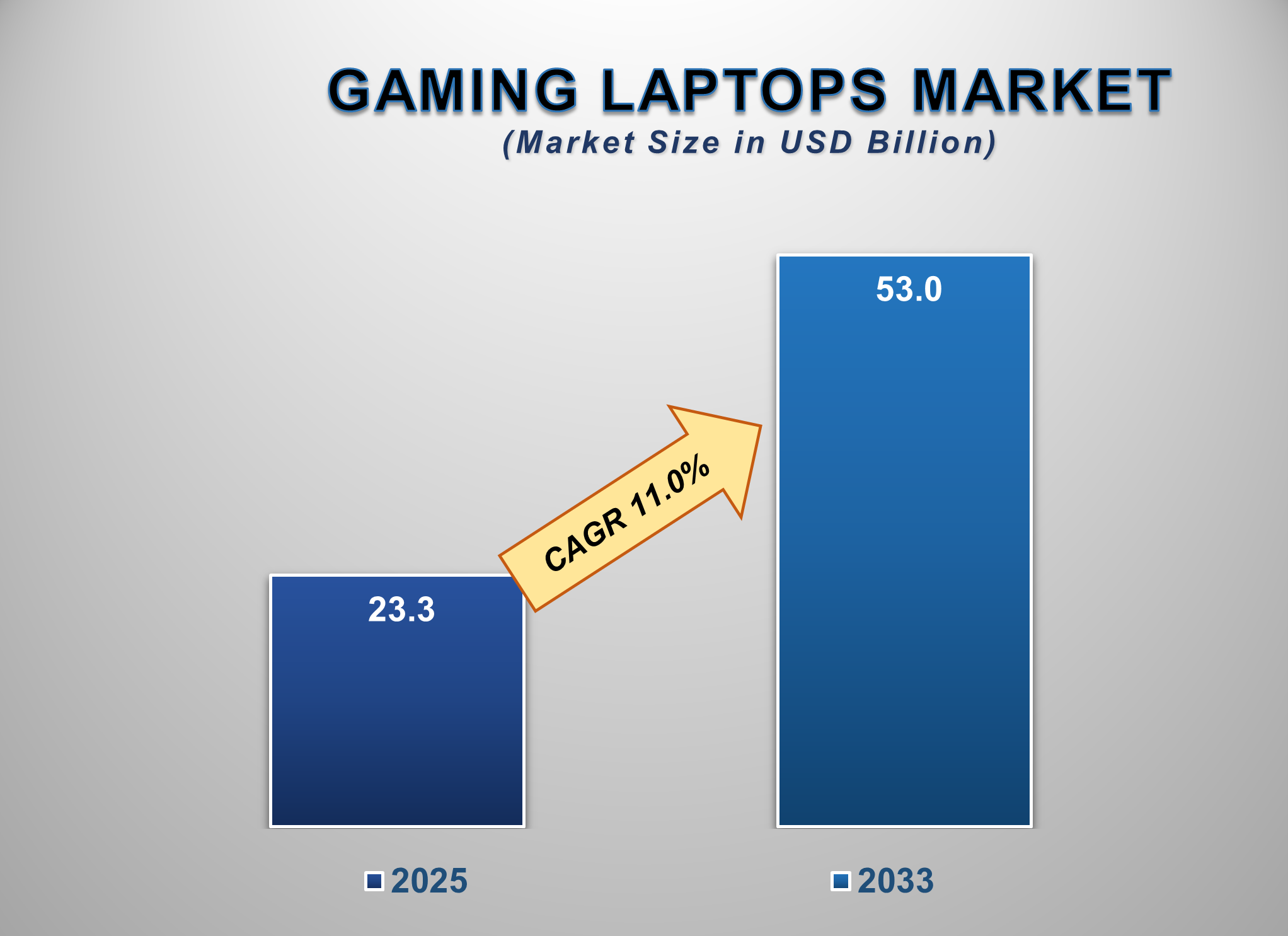

The Gaming Laptops Market is poised for a period of dynamic expansion from 2025 to 2033, fueled by relentless hardware innovation, the global ascent of esports, and the increasing demand for portable, high-performance computing. The market is projected to be valued at approximately USD 23.3 billion in 2025 and is forecasted to surge to nearly USD 53.0 billion by 2033, exhibiting a robust compound annual growth rate (CAGR) of 11.0% during this period.

Gaming laptops are specialized portable

computers engineered with high-performance components, including dedicated

graphics processing units (GPUs), advanced cooling systems, and

high-refresh-rate displays to deliver a seamless and immersive gaming experience.

Market growth is primarily driven by the continuous competition and innovation

between CPU and GPU manufacturers, the rising popularity of competitive gaming

and live streaming, and the convergence of gaming and content creation

workflows.

The increasing disposable income in emerging

economies, coupled with the growing cultural mainstreaming of video games, is

creating sustained global demand. Technological advancements such as AI-powered

performance optimization (e.g., NVIDIA DLSS, AMD FSR), the adoption of mini-LED

and OLED display technologies, and more efficient thermal management solutions

are key market enablers. The Asia-Pacific region currently leads the market due

to its massive gamer demographic and strong manufacturing base, while North

America remains a critical market for premium and high-performance models. With

the ongoing evolution of game graphics and the need for versatile, powerful

mobile workstations, the Gaming Laptops Market is set for significant growth

over the next decade.

Gaming Laptops Market Drivers and

Opportunities

The Intense Competition and Innovation in the

CPU and GPU Sectors are the Core drivers for the Gaming Laptops Market

The fierce rivalry between Intel and AMD in the

CPU space and between NVIDIA, AMD, and Intel

in the GPU arena directly fuels market growth. Each new generation of

processors and graphics cards delivers substantial performance improvements,

real-time ray tracing capabilities, and AI-enhanced features. This creates a

persistent upgrade cycle, enticing enthusiasts and professionals to seek the

latest technology for a competitive edge and superior visual fidelity. The

ability of modern gaming laptops to deliver desktop-class performance in a

portable form factor is a key value proposition, driving both new customer

acquisition and repeat purchases.

The Professionalization of Esports and the

Content Creation Boom is Catalyzing Massive Market Growth

The global esports industry's transformation

into a professional sport has created a non-negotiable demand for reliable,

high-performance, and portable gaming systems for training, competition, and

broadcasting. Simultaneously, the explosion of content creation on platforms

like Twitch, YouTube, and TikTok requires a single machine capable of playing

demanding games at maximum settings while simultaneously handling

resource-intensive video encoding and streaming. This dual-application demand

elevates the gaming laptop from a recreational device to an essential

professional tool, expanding the market's scope and driving sales of high-end

models.

Technological Convergence and Supply Chain

Diversification are Unlocking New Opportunities

The blending of gaming, streaming, and

professional creative work presents significant opportunities for market

differentiation. Key areas of development include advanced vapor chamber

cooling solutions to sustain higher clock speeds, the integration of next-generation

connectivity like Wi-Fi 7, and the use of premium, lightweight materials.

Furthermore, the entry of new processor architectures, such as Apple's M-series

and other ARM-based chips, presents a new frontier for performance-per-watt and

battery life. The growing trend of OEMs and ODMs (Original Design

Manufacturers) like Clevo and TongFang partnering with regional brands (e.g.,

Eluktronics, XPG) allows for greater product diversification and caters to

niche market segments, increasing overall market penetration.

Gaming Laptops Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 23.3 Billion |

|

Market Forecast in 2033 |

USD 53.0 Billion |

|

CAGR % 2025-2033 |

11.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Technological Analysis, Company Market Share,

Company Heatmap, Pricing Analysis, Growth Factors and more |

|

Segments Covered |

●

By Type ●

By Disease ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Gaming Laptops Market Report Segmentation Analysis

The global Gaming Laptops Market

industry analysis is segmented by Type, by Processor Type, by GPU Type, by

Display Size, by End-user, by Distribution Channel, and by region.

The Intel processor type segment is anticipated to command

the largest market share in 2025.

The market is divided by Processor Type into

Intel, AMD, and Others (e.g., Apple M-series, ARM-based). Intel continues to

hold a dominant share, driven by its long-established brand presence, extensive

partnerships with laptop OEMs, and strong single-core performance that is

highly valued in gaming. However, AMD has been gaining significant traction

with its Ryzen series, which offers competitive multi-core performance and

power efficiency.

The NVIDIA GPU Type segment dominated the market in 2025 and

is projected to grow at a significant CAGR.

Based on GPU Type, the market is segmented into

NVIDIA, AMD Radeon, Intel Arc, and Others. NVIDIA holds an overwhelming market

share. This dominance is attributed to its technological leadership in ray

tracing and AI-powered upscaling (DLSS), a robust software ecosystem (GeForce

Experience), and its strong brand association with high-performance gaming,

making it the preferred choice for most gamers and manufacturers.

The dominance of the NVIDIA segment is intrinsically linked to its continuous innovation in graphics technology and the software ecosystem. Features like real-time ray tracing and Deep Learning Super Sampling (DLSS) have become industry benchmarks, providing a tangible visual and performance advantage that is heavily marketed by both NVIDIA and its partners. The widespread adoption of the "GeForce RTX" branding across a vast range of laptops, from budget to flagship, creates a unified and powerful marketing message that resonates with consumers. As game developers continue to prioritize these technologies, the demand for NVIDIA GPUs is reinforced, ensuring the segment's continued leadership.

The 15–17-inch display size segment is expected to hold a

significant market share in 2025.

By Display Size, the market is categorized into below 15 inches, 15–17 inches, and above 17 inches. The 15–17 inch segment is the industry standard and largest contributor.

This size offers the ideal balance between screen immersion for gaming, a

comfortable form factor for portability, and sufficient space for a full-sized

keyboard, making it the most popular and widely available category.

The Casual Gamers end-user segment dominated the global

gaming laptops market in 2025.

Based on End User, the market is segmented into

Professional Gamers, Casual Gamers, Game Developers, and eSports Organizations.

The Casual Gamers segment holds the largest share by a wide margin. This vast

group encompasses the broad base of consumers who purchase gaming laptops for

entertainment and hobbyism, driving volume sales in the mid-range and budget

segments.

The Online distribution channel segment is projected to be

the fastest-growing channel during the forecast period.

The market is divided by Distribution Channel

into Online (E-commerce, Brand Websites) and Offline (Retail Stores, Specialty

Stores). While offline channels remain crucial for hands-on experience, the

Online segment is growing rapidly due to the convenience of direct-to-consumer

sales, frequent online discounts, wider product selection, and detailed

customer reviews available on e-commerce platforms.

The following segments

are part of an in-depth analysis of the global gaming laptops market:

|

Market Segments |

|

|

By Processor Type |

●

Intel ●

AMD ●

Others (e.g., Apple

M-series, ARM-based) |

|

By GPU Type |

●

NVIDIA ●

AMD Radeon ●

Intel Arc ●

Others |

|

By Display Size |

●

Below 15 Inches ●

15–17 Inches ●

Above 17 Inches |

|

By End-user |

●

Professional Gamers ●

Casual Gamers ●

Game Developers ●

eSports

Organizations |

|

By Distribution Channel |

●

Online Store ●

Offline Store |

Gaming Laptops Market Share Analysis by Region

The North America region is anticipated to hold the largest

portion of the Gaming Laptops Market globally throughout the forecast period.

The dominance of North America can be attributed

to its strong gaming culture, high disposable income, and early adoption of

advanced gaming technologies. The region hosts some of the world’s leading

gaming laptop manufacturers and component suppliers, such as Dell (Alienware),

HP (OMEN), and Razer, which continuously invest in product innovation and

performance enhancements.

Moreover, the widespread availability of

high-speed internet infrastructure and the growing popularity of eSports

tournaments and online multiplayer games have fueled demand for

high-performance laptops. The United States remains the largest contributor within

the region due to its extensive gaming community, strong presence of

professional gaming leagues, and high concentration of tech-savvy

consumers. Additionally, the integration of AI-driven graphics, advanced

cooling systems, and VR-ready features further strengthens the market’s growth

in North America, positioning it as the leading region in terms of both revenue

and adoption rate for gaming laptops.

Gaming Laptops Market Competition Landscape Analysis

The global gaming laptops market

is severely competitive and fragmented, characterized by the presence of major

multinational brands, dedicated gaming-focused companies, and agile boutique

builders. Competition is centered on technological leadership (first-to-market

with new GPUs/CPUs), brand identity, design aesthetics, and

performance-per-dollar. Key strategies include high-profile sponsorships of

esports teams and influencers, continuous R&D into cooling and form

factors, and strategic partnerships with key component suppliers. The market

also features a significant segment of companies that utilize chassis from ODMs

like Clevo to offer customizable, high-performance models directly to

consumers.

Global Gaming Laptops Market Recent Developments News:

- In February 2025, ASUS ROG unveiled its new

Zephyrus line featuring the latest NVIDIA GeForce RTX 50 series laptops,

emphasizing a new dual-chamber cooling system for maximized performance in

an ultra-thin design.

- In January 2025, Lenovo Legion announced a

multi-year partnership with a leading global esports league, becoming the

official gaming laptop partner and solidifying its brand in the

professional gaming scene.

- In November 2024, MSI launched its new

"Titan" series, touted as the world's first laptop to feature a

factory-overclocked GPU and a 4K 144 Hz

mini-LED display, targeting the extreme high-end enthusiast segment.

- In October 2024, Eluktronics introduced a new water-cooling accessory

for its flagship laptops, demonstrating the trend of boutique

manufacturers pushing performance boundaries beyond standard air cooling.

The Global Gaming Laptops

Market Is Dominated by a Few Large Companies, such as

●

ASUSTeK Computer Inc.

(ASUS)

●

Acer Inc.

●

Dell Technologies Inc.

●

HP Inc.

●

Lenovo Group Limited

●

MSI (Micro-Star

International Co., Ltd.)

●

Razer Inc.

●

Gigabyte Technology

Co., Ltd.

●

Samsung Electronics

Co., Ltd.

●

Origin PC Corporation

●

Eluktronics, Inc.

●

Clevo (Hasee Computer

Co., Ltd.)

●

EVGA Corporation

●

CyberPowerPC

●

XPG (ADATA Technology

Co., Ltd.)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Gaming Laptops

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Gaming Laptops Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Gaming Laptops

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Processor Type of Global Gaming

Laptops Market

1.3.2.GPU Type of Global Gaming

Laptops Market

1.3.3.Display Size of Global Gaming

Laptops Market

1.3.4.End-user of Global Gaming

Laptops Market

1.3.5.Distribution Channel of

Global Gaming Laptops Market

1.3.6.Region of Global Gaming

Laptops Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Technological

Advancements

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Gaming Laptops Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by Processor Type

4.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by Processor

Type, 2020 - 2033

4.1.1.Intel

4.1.2.AMD

4.1.3.Others (e.g., Apple

M-series, ARM-based)

5. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by GPU Type

5.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by GPU Type, 2020

- 2033

5.1.1.NVIDIA

5.1.2.AMD Radeon

5.1.3.Intel Arc

5.1.4.Others

6. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by Display Size

6.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by Display Size,

2020 - 2033

6.1.1.Below 15 Inches

6.1.2.15–17 Inches

6.1.3.Above 17 Inches

7. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by End-user

7.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

7.1.1.Professional Gamers

7.1.2.Casual Gamers

7.1.3.Game Developers

7.1.4.eSports Organizations

8. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by Distribution Channel

8.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

8.1.1.Online Store

8.1.2.Offline Store

9. Global

Gaming Laptops Market Estimates

& Forecast Trend Analysis, by region

9.1.

Global

Gaming Laptops Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

9.1.1.North America

9.1.2.Europe

9.1.3.Asia Pacific

9.1.4.Middle East & Africa

9.1.5.Latin America

10. North America Gaming

Laptops Market: Estimates &

Forecast Trend Analysis

10.1. North America Gaming

Laptops Market Assessments & Key Findings

10.1.1.

North

America Gaming Laptops Market Introduction

10.1.2.

North

America Gaming Laptops Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

10.1.2.1.

By Processor Type

10.1.2.2.

By GPU Type

10.1.2.3.

By Display Size

10.1.2.4.

By End-user

10.1.2.5.

By Distribution Channel

10.1.2.6. By Country

10.1.2.6.1. The U.S.

10.1.2.6.2. Canada

11. Europe Gaming

Laptops Market: Estimates &

Forecast Trend Analysis

11.1. Europe Gaming Laptops

Market Assessments & Key Findings

11.1.1. Europe Gaming Laptops

Market Introduction

11.1.2. Europe Gaming Laptops

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Processor Type

11.1.2.2.

By GPU Type

11.1.2.3.

By Display Size

11.1.2.4.

By End-user

11.1.2.5.

By Distribution Channel

11.1.2.6. By Country

11.1.2.6.1.

Germany

11.1.2.6.2.

Italy

11.1.2.6.3.

U.K.

11.1.2.6.4.

France

11.1.2.6.5.

Spain

11.1.2.6.6.

Switzerland

11.1.2.6.7. Rest

of Europe

12. Asia Pacific Gaming

Laptops Market: Estimates &

Forecast Trend Analysis

12.1. Asia Pacific Market

Assessments & Key Findings

12.1.1.

Asia

Pacific Gaming Laptops Market Introduction

12.1.2.

Asia

Pacific Gaming Laptops Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

12.1.2.1.

By Processor Type

12.1.2.2.

By GPU Type

12.1.2.3.

By Display Size

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. China

12.1.2.5.2. Japan

12.1.2.5.3. India

12.1.2.5.4. Australia

12.1.2.5.5. South Korea

12.1.2.5.6. Rest of Asia Pacific

13. Middle East & Africa Gaming

Laptops Market: Estimates &

Forecast Trend Analysis

13.1. Middle East & Africa

Market Assessments & Key Findings

13.1.1. Middle

East & Africa

Gaming Laptops Market Introduction

13.1.2. Middle

East & Africa

Gaming Laptops Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Processor Type

13.1.2.2.

By GPU Type

13.1.2.3.

By Display Size

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. UAE

13.1.2.5.2. Saudi

Arabia

13.1.2.5.3. South

Africa

13.1.2.5.4. Rest

of MEA

14. Latin America

Gaming Laptops Market: Estimates &

Forecast Trend Analysis

14.1. Latin America Market

Assessments & Key Findings

14.1.1. Latin America Gaming

Laptops Market Introduction

14.1.2. Latin America Gaming

Laptops Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

14.1.2.1.

By Processor Type

14.1.2.2.

By GPU Type

14.1.2.3.

By Display Size

14.1.2.4.

By End-user

14.1.2.5. By Country

14.1.2.5.1. Brazil

14.1.2.5.2. Argentina

14.1.2.5.3. Mexico

14.1.2.5.4. Rest

of LATAM

15.

Country

Wise Market: Introduction

16.

Competition

Landscape

16.1. Global Gaming Laptops

Market Product Mapping

16.2. Global Gaming Laptops

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

16.3. Global Gaming Laptops

Market Tier Structure Analysis

16.4. Global Gaming Laptops

Market Concentration & Company Market Shares (%) Analysis, 2024

17.

Company

Profiles

17.1.

ASUSTeK Computer Inc. (ASUS)

17.1.1.

Company

Overview & Key Stats

17.1.2.

Financial

Performance & KPIs

17.1.3.

Product

Portfolio

17.1.4.

SWOT

Analysis

17.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

17.2.

Acer Inc.

17.3.

Dell Technologies Inc.

17.4.

HP Inc.

17.5.

Lenovo Group Limited

17.6.

MSI (Micro-Star International Co., Ltd.)

17.7.

Razer Inc.

17.8.

Gigabyte Technology Co., Ltd.

17.9.

Samsung Electronics Co., Ltd.

17.10.

Origin PC Corporation

17.11.

Eluktronics, Inc.

17.12.

Clevo (Hasee Computer Co., Ltd.)

17.13.

EVGA Corporation

17.14.

CyberPowerPC

17.15.

XPG (ADATA Technology Co., Ltd.)

17.16.

Other Prominent Players

18. Research

Methodology

18.1. External Transportations /

Databases

18.2. Internal Proprietary

Database

18.3. Primary Research

18.4. Secondary Research

18.5. Assumptions

18.6. Limitations

18.7. Report FAQs

19. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables