Gene Vector Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Type (Viral Vectors, Non-Viral Vectors), By Application (Gene Therapy, Vaccinology, Research & Development), By Disease (Oncological Disorders, Rare Diseases, Neurological Disorders, Infectious Diseases, Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, CROs & CDMOs) And Geography

2025-11-14

Healthcare

Swetal (Research Analyst)

Description

Gene Vector Market

Overview

The Gene Vector Market is positioned for a

period of transformative growth from 2025 to 2033, underpinned by the

revolutionary advances in gene and cell therapies. The market is projected to

be valued at approximately USD 2.6 billion in 2025 and is forecasted to surge

to nearly USD 7.6 billion by 2033, exhibiting an exceptional compound annual

growth rate (CAGR) of 14.9% during this period.

Gene vectors are vehicles, typically viral or

non-viral, used to deliver genetic material into a patient's cells for

therapeutic or prophylactic purposes. They are the fundamental engine driving

modern gene therapy and vaccinology. The market growth is primarily fuelled by

the escalating number of approved gene therapies, the tremendous success and

widespread application of viral vectors in vaccine development (exemplified by

COVID-19 vaccines), and increasing investment

in genomic medicine.

The growing prevalence of genetic disorders,

cancers, and infectious diseases, coupled with a strong pipeline of over a

thousand gene therapy clinical trials globally, is creating an unprecedented

demand for vector manufacturing and development. Technological advancements in

vector design for improved safety and efficacy, scalability of production

processes, and the exploration of novel non-viral delivery systems are key

market enablers. North America currently leads the market due to a favorable

regulatory landscape and high R&D expenditure, while the Asia-Pacific

region is emerging as a pivotal hub for manufacturing and clinical research.

With the continuous expansion of therapeutic applications and the push for more

accessible treatments, the Gene Vector Market is set to experience robust

expansion over the next decade.

Gene Vector Market Drivers and

Opportunities

The Unprecedented Expansion of Gene and

Cell Therapies is the Core Driver for the Gene Vector Market

The global regulatory approval of multiple

high-profile gene therapies for conditions like spinal muscular atrophy,

beta-thalassemia, and various cancers has validated the therapeutic potential

of gene vectors, particularly viral vectors like AAV and lentivirus. These approvals have catalyzed massive investment from

both biopharma companies and venture capital, fueling a vast and growing

clinical pipeline. Vectors are the indispensable workhorses in these therapies,

responsible for the precise delivery of corrective genes. The demand for

high-quality, clinically-grade vectors for late-stage trials and commercial

supply is immense and forms the primary growth engine for the market. The shift

from research-scale to large-scale GMP manufacturing to meet this demand is a

critical and defining trend.

Gene therapy in oncology represents a diverse

and rapidly advancing field, employing multiple strategic approaches to combat

cancer. One key strategy is oncolytic virotherapy, which utilizes genetically

engineered viruses that selectively infect and lyse cancer cells while

stimulating immune responses, as demonstrated by talimogene laherparepvec

(Imlygic) for melanoma. Another approach involves sophisticated gene editing

technologies like CRISPR-Cas9, which can directly disrupt oncogenic pathways in

tumor cells or enhance the anti-tumor capabilities of engineered immune cells.

Additionally, in vivo gene therapy focuses on delivering therapeutic genes

directly into patients' cells, such as reintroducing functional tumor

suppressor genes like p53 or activating suicide genes that trigger targeted

cell death. Furthermore, cancer vaccines leverage viral vectors to deliver

tumor-specific antigens, priming the host's immune system to recognize and

eliminate malignant cells. These complementary strategies highlight the

multifaceted nature of oncologic gene therapy, collectively contributing to its

growing prevalence in cancer treatment by addressing different aspects of tumor

biology and harnessing both direct cytotoxic mechanisms and enhanced

immunotherapeutic responses.

The Proliferation of Viral Vectors in

Modern Vaccinology is Catalyzing Massive Market Growth

The global response to the COVID-19 pandemic

demonstrated the power and scalability of viral vector-based vaccine platforms.

This success has established viral vectors as a versatile and rapid-response

technology for infectious disease prevention. Research and development into

vector-based vaccines for other diseases such as HIV, Zika, and malaria have

been significantly accelerated. This application represents a massive,

high-volume segment for the gene vector market, distinct from one-time gene

therapies. The proven manufacturability and immunogenicity of these platforms

ensure their continued use in future epidemic and pandemic preparedness,

creating a sustained and high-growth driver for the market.

Technological Innovations in Vector

Engineering and Manufacturing are Unlocking New Opportunities

The need for safer, more efficient, and

higher-capacity vectors is driving a wave of innovation, presenting significant

opportunities. Key areas of development include the engineering of novel

capsids for improved tissue targeting and reduced immunogenicity, and the creation of "tunable" non-viral vectors for

more controlled gene expression. Furthermore, the high cost and complexity of

viral vector manufacturing have created a substantial opportunity for

technological advancements in production systems. The adoption of suspension

cell culture systems, continuous manufacturing processes, and advanced

analytics for process control is critical to

reducing costs and increasing scale. The emergence of plasmid DNA and RNA

technologies as viable non-viral alternatives is also expanding the market's

scope, offering potential advantages in safety and manufacturing simplicity for

certain applications.

Gene Vector Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.6 Billion |

|

Market Forecast in 2033 |

USD 7.6 Billion |

|

CAGR % 2025-2033 |

14.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio, Application Analysis, Company Market Share,

Company Heatmap, Regulatory Landscape, Growth Factors and more |

|

Segments Covered |

●

By Type ●

By Disease ●

By Application ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Gene Vector Market Report Segmentation Analysis

The global gene vector market

industry analysis is segmented by Type, by Application, by Disease, by

End-User, and by Region.

The Viral Vectors segment is anticipated to command the

largest share in the global Gene Vector Market during the forecast period.

Based on type, the market is divided into Viral Vectors (Adenovirus, Adeno-associated Virus (AAV), Lentivirus, Retrovirus, Others) and Non-Viral Vectors (Naked DNA, Electroporation, Lipofection, Others). The Viral Vectors segment is dominant, accounting for the overwhelming market share. This is attributed to their high transduction efficiency, proven clinical success in approved therapies and vaccines, and well-established, though complex, manufacturing protocols. AAV and Lentivirus are the leading sub-segments due to their favorable safety profiles and use in permanent gene correction.

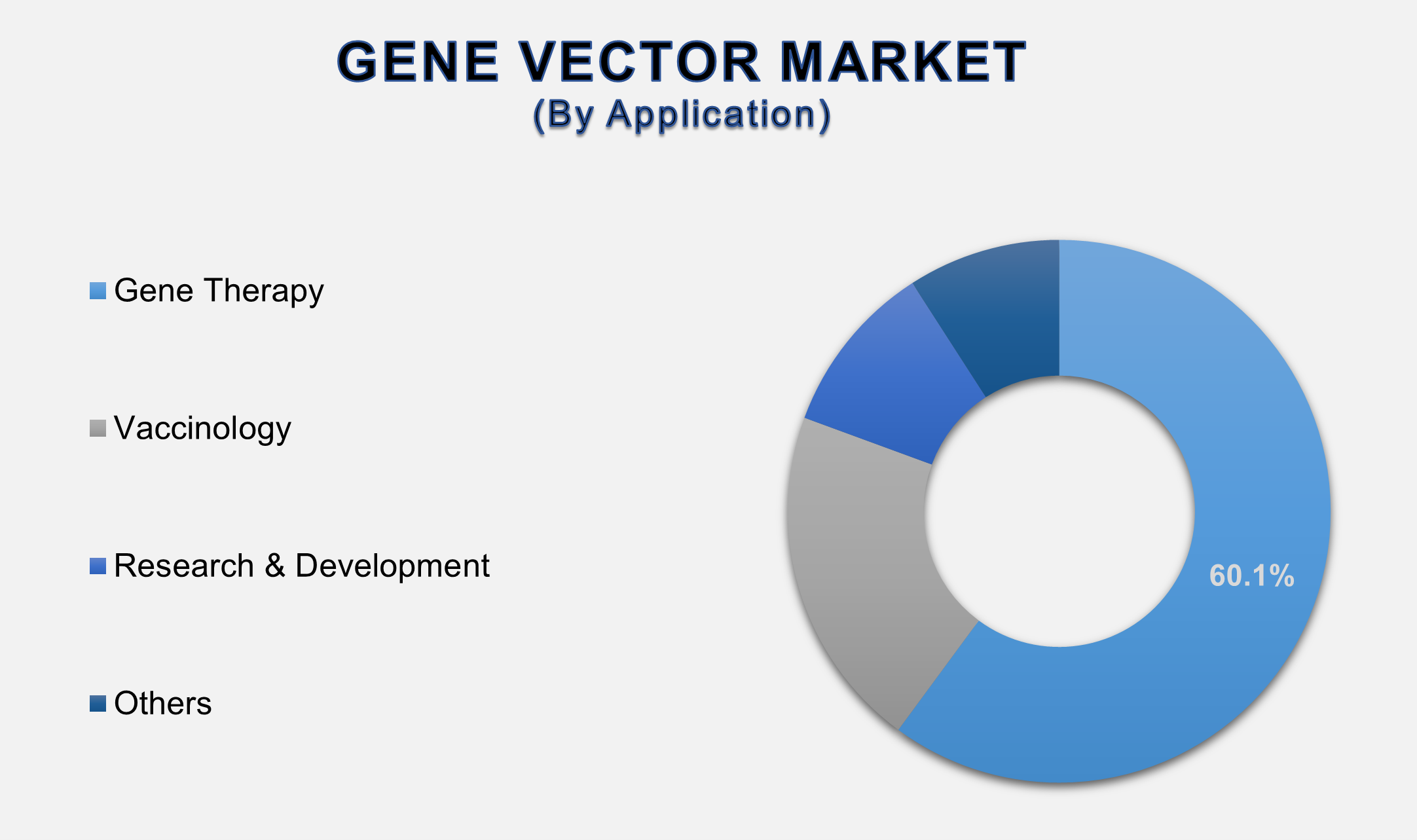

The Gene Therapy segment dominated the market in 2025 and is

projected to grow at a significant CAGR during the forecast period.

Based on application, the market is segmented

into Gene Therapy, Vaccinology, and Research & Development. The Gene

Therapy segment holds the largest share. This dominance is driven by the high

value and curative potential of gene therapies, which command premium pricing

and represent the most direct and transformative application of gene vectors.

The intense R&D activity and growing commercial footprint for both rare and

common diseases solidify this segment's leadership position.

The dominance of the Gene Therapy segment is

intrinsically linked to the paradigm shift towards one-time, potentially

curative treatments for genetic diseases. The ability of viral vectors,

especially AAV and Lentivirus, to deliver therapeutic genes with high

efficiency and long-lasting expression has made them the cornerstone of this

new therapeutic modality. The high cost of goods and the significant technical

and regulatory hurdles in vector manufacturing are reflected in the premium

pricing of these therapies, which in turn drives the high revenue of this

segment. As the pipeline of gene therapies matures, with targets expanding from

ultra-rare monogenic diseases to more prevalent conditions like hemophilia and

oncology, the demand for clinical and commercial-grade vectors is set to

increase exponentially, ensuring the continued dominance of this application.

The Oncological Disorders segment is expected to hold a

significant market share in 2025.

By disease, the market is divided into

Oncological Disorders, Rare Diseases, Neurological Disorders, Infectious

Diseases, and Others. The Oncological Disorders segment is a major contributor,

largely due to the widespread use of lentiviral and retroviral vectors in CAR-T

cell therapies for various cancers. The high incidence of cancer and the rapid

adoption of these immunotherapies fuel this segment's substantial market share.

While monogenic rare diseases often represent the

ideal genetic targets, oncology accounts for an overwhelming majority, approximately 60-70%, of

all active gene therapy clinical trials globally. This prevalence is driven by

a powerful convergence of scientific opportunity, clinical need, and commercial

viability.

The following segments

are part of an in-depth analysis of the global Gene Vector Market:

|

Market Segments |

|

|

By Type |

●

Viral Vectors o

Adenovirus o

AAV

(adeno-associated virus) o

Lentivirus o

Retrovirus o

Others ●

Non-Viral Vectors |

|

By Disease |

●

Oncological

Disorders ●

Rare Diseases ●

Neurological

Disorders ●

Infectious Diseases ●

Others |

|

By Application |

●

Gene Therapy ●

Vaccinology ●

Research &

Development ●

Others |

|

By End-user |

●

Pharmaceutical &

Biotechnology Companies ●

Academic &

Research Institutes ●

Contract Research

& Manufacturing Organizations (CROs & CDMOs) ●

Others |

Gene Vector Market Share Analysis by Region

The North America region is anticipated to hold the largest

portion of the Gene Vector Market globally throughout the forecast period.

North America is the leading segment, holding a

dominant share of over 50%. This is a direct result of the region's

concentration of pioneering gene therapy companies, a robust regulatory

framework from the FDA that has approved several gene therapies, the presence

of world-leading academic research institutions, and favorable

reimbursement landscapes. High healthcare expenditure and strong venture

capital funding further consolidate its leadership.

North America in the gene vector market is a

testament to its integrated ecosystem for advanced therapeutic innovation. The

United States is the epicenter of gene therapy development, hosting the

majority of clinical trials and being the first to market for several landmark

treatments. The FDA's proactive approach in creating expedited pathways for

regenerative medicine products has provided a clear regulatory route for

companies. Furthermore, the presence of world-class research universities and

medical centers drives foundational vector research, while a mature venture

capital and public financing market provides the necessary capital for the

high-cost development of these therapies. The convergence of these factors—cutting-edge R&D, a supportive regulatory environment, ample

funding, and a strong commercial biopharma sector—creates a virtuous cycle that

ensures North America's continued dominance in the global gene vector

landscape.

Gene Vector Market Competition Landscape Analysis

The global gene vector market is

highly competitive and characterized by the presence of established CDMOs

(Contract Development and Manufacturing Organizations), large biopharmaceutical

companies, and specialized technology firms. The market is witnessing intense

competition for manufacturing capacity and technological superiority. Key

strategies include significant capital investment in expanding GMP

manufacturing facilities, strategic partnerships and long-term supply

agreements with therapy developers, and a strong focus on R&D to develop

next-generation vectors with improved properties. Vertical integration, where

therapy developers bring vector manufacturing in-house, is another notable

trend.

Global Gene Vector Market Recent Developments News:

- In February 2025, Catalent, Inc. announced a major

expansion of its viral vector manufacturing facility in Maryland, USA, to

meet the growing demand from late-stage gene therapy clients.

- In December 2024, Pfizer Inc. entered a long-term

strategic partnership with a leading AAV vector technology company to gain

access to novel capsids for its next-generation gene therapy pipeline.

- In October 2024, Lonza Group AG launched a new

platform for scalable plasmid DNA production, addressing a critical

bottleneck in both viral and non-viral gene therapy manufacturing.

- In August 2024, Sarepta Therapeutics, Inc. received FDA approval for

its second AAV-based gene therapy, further validating the platform and

stimulating market growth.

The Global Gene Vector

Market Is Dominated by a Few Large Companies, such as

●

Thermo Fisher

Scientific Inc.

●

Merck KGaA

●

Danaher Corporation

(Cytiva)

●

Lonza Group AG

●

Fujifilm Holdings

Corporation

●

Catalent, Inc.

●

Charles River

Laboratories International, Inc.

●

Sartorius AG

●

Takara Bio Inc.

●

Spark Therapeutics,

Inc.

●

Novartis AG

●

BioNTech SE

●

REGENXBIO Inc.

●

Oxford Biomedica plc

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Gene Vector Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Gene Vector Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Gene Vector Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Type of Global Gene Vector

Market

1.3.2.Disease of Global Gene

Vector Market

1.3.3.Application of Global Gene

Vector Market

1.3.4.End-user of Global Gene

Vector Market

1.3.5.Region of Global Gene

Vector Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5. Overview of Biosensors

for stem cell-based applications

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Gene Vector Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Gene Vector Market Estimates

& Forecast Trend Analysis, by Type

4.1.

Global

Gene Vector Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020 -

2033

4.1.1.Viral Vectors

4.1.1.1.

Adenovirus

4.1.1.2.

AAV

(adeno-associated virus)

4.1.1.3.

Lentivirus

4.1.1.4.

Retrovirus

4.1.1.5.

Others

4.1.2.Non-Viral Vectors

5. Global

Gene Vector Market Estimates

& Forecast Trend Analysis, by Disease

5.1.

Global

Gene Vector Market Revenue (US$ Bn) Estimates and Forecasts, by Disease, 2020 -

2033

5.1.1.Oncological Disorders

5.1.2.Rare Diseases

5.1.3.Neurological Disorders

5.1.4.Infectious Diseases

5.1.5.Others

6. Global

Gene Vector Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Gene Vector Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Gene Therapy

6.1.2.Vaccinology

6.1.3.Research & Development

6.1.4.Others

7. Global

Gene Vector Market Estimates

& Forecast Trend Analysis, by End-user

7.1.

Global

Gene Vector Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020

- 2033

7.1.1.Pharmaceutical &

Biotechnology Companies

7.1.2.Academic & Research

Institutes

7.1.3.Contract Research &

Manufacturing Organizations (CROs & CDMOs)

7.1.4.Others

8. Global

Gene Vector Market Estimates

& Forecast Trend Analysis, by Region

8.1.

Global

Gene Vector Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Gene

Vector Market: Estimates & Forecast

Trend Analysis

9.1. North America Gene Vector

Market Assessments & Key Findings

9.1.1.North America Gene Vector

Market Introduction

9.1.2.North America Gene Vector

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Type

9.1.2.2.

By Disease

9.1.2.3.

By Application

9.1.2.4.

By End-user

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Gene

Vector Market: Estimates & Forecast

Trend Analysis

10.1. Europe Gene Vector Market

Assessments & Key Findings

10.1.1. Europe Gene Vector Market

Introduction

10.1.2. Europe Gene Vector Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Type

10.1.2.2.

By Disease

10.1.2.3.

By Application

10.1.2.4.

By End-user

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Gene

Vector Market: Estimates & Forecast

Trend Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Gene Vector Market Introduction

11.1.2.

Asia

Pacific Gene Vector Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Type

11.1.2.2.

By Disease

11.1.2.3.

By Application

11.1.2.4.

By End-user

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Gene

Vector Market: Estimates & Forecast

Trend Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Gene Vector Market Introduction

12.1.2. Middle

East & Africa

Gene Vector Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Type

12.1.2.2.

By Disease

12.1.2.3.

By Application

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Gene Vector Market: Estimates &

Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Gene Vector

Market Introduction

13.1.2. Latin America Gene Vector

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Type

13.1.2.2.

By Disease

13.1.2.3.

By Application

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Gene Vector Market Product

Mapping

15.2. Global Gene Vector Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

15.3. Global Gene Vector Market Tier

Structure Analysis

15.4. Global Gene Vector Market

Concentration & Company Market Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

Thermo Fisher Scientific Inc.

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2.

Merck KGaA

16.3.

Danaher Corporation (Cytiva)

16.4.

Lonza Group AG

16.5.

Fujifilm Holdings Corporation

16.6.

Catalent, Inc.

16.7.

Charles River Laboratories International, Inc.

16.8.

Sartorius AG

16.9.

Takara Bio Inc.

16.10.

Spark Therapeutics, Inc.

16.11.

Novartis AG

16.12.

BioNTech SE

16.13.

REGENXBIO Inc.

16.14.

Oxford Biomedica plc

16.15.

Other Prominent Players

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables