Geothermal Power Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Power Station Type (Dry Steam Power Stations, Flash Steam Power Stations, and Binary Cycle Power Stations), End Use (Residential, Commercial, Industrial, and Others), and Geography

2026-02-04

Energy & Power

Ekta Chaurasia (Team Lead)

Description

Geothermal

Power Market Overview

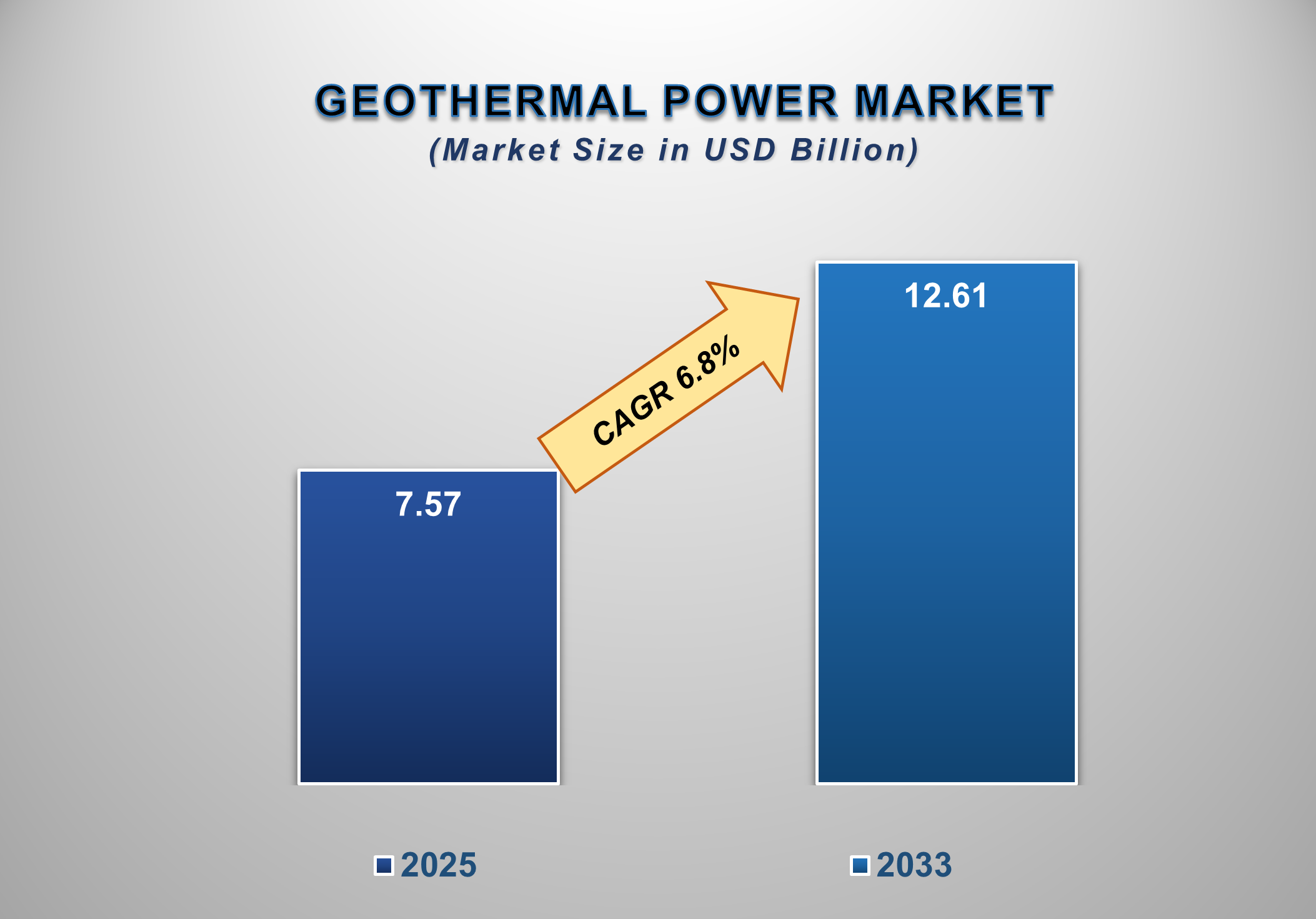

The global geothermal power market is experiencing strong growth, driven by the growing demand for clean, reliable, and low-carbon energy. Valued at USD 7.57 billion in 2025, the market is projected to reach USD 12.61 billion by 2033, growing at a CAGR of 6.8% during the forecast period.

The geothermal power market, which provides a dependable,

low-carbon, baseload source of electricity, is an important part of the world's

renewable energy landscape. Since geothermal energy is not weather-dependent

like solar and wind power, it is essential for grid stability and long-term

energy security. Dry steam, flash steam, and binary cycle power plants are some

of the technologies that use heat from the Earth's interior to create

electricity.

Growing demand for renewable energy, favorable government

regulations, and plans to reduce greenhouse gas emissions are driving the

industry globally. The majority of installed geothermal capacity is found in

countries along tectonic plate boundaries or volcanic regions, such as the

United States, Indonesia, the Philippines, Kenya, Iceland, and New Zealand,

because of the availability of suitable resources. Flash steam power plants

currently account for the majority of plant technologies, followed by binary

cycle plants, which are becoming more popular due to their ability to utilize

low-temperature geothermal resources and their low environmental impact.

Technological developments are essential to the growth of

the market. Organic Rankine Cycle (ORC) systems, reservoir management, and

drilling techniques have all enhanced efficiency and decreased costs.

Furthermore, Enhanced Geothermal Systems (EGS) are showing promise as a way to

enable geothermal development in areas without hydrothermal resources.

The geothermal power market has drawbacks despite its

benefits, such as high initial capital costs, hazards associated with

exploration, lengthy project development schedules, and site-specific

constraints. Careful management is also necessary for environmental issues,

including land use and induced seismicity. Long plant lifespans, low operating

costs, and steady power generation, however, frequently overcome these

obstacles over time.

The market for geothermal power is anticipated to increase

steadily in the future as nations promote energy resilience and diversify their

energy mix. The implementation of geothermal energy is expected to be

accelerated by increased investment, international cooperation, and favorable

regulatory frameworks, placing it as a major player in the global shift toward

dependable and sustainable power generation.

Geothermal

Power Market Drivers and Opportunities

Growing Demand for Clean

and Reliable Energy

The growing need for clean, dependable, low-carbon

electricity around the world is one of the main factors propelling the

geothermal power market. Geothermal energy offers a special benefit as a

baseload renewable resource that operates constantly regardless of weather

conditions as nations strive to meet climate targets and reduce reliance on

fossil fuels. As an example of how geothermal power can serve national

decarbonization goals while maintaining energy security, Iceland produces a

significant amount of its electricity and heating from geothermal energy.

Government Policies and Regulatory Support

The growth of the geothermal market is being accelerated by

favorable government regulations and incentives. These consist of

risk-mitigation funds, tax credits, feed-in tariffs, and concessional finance

for drilling and exploration. Federal tax incentives and Department of Energy

research and development funds are available for geothermal projects in the

United States. In a similar vein, Indonesia and Kenya have implemented

legislative frameworks that encourage private participation in geothermal exploration,

lowering project risks in the early stages and enhancing bankability.

Technological Advancements in Geothermal Systems

Geothermal technology advancements are greatly enhancing

project viability and cost-effectiveness. Power generation from low-temperature

resources that were previously thought to be unprofitable has been made

possible by advancements in drilling methods, reservoir modeling, and binary

cycle power plants. For example, binary cycle plants are frequently employed in

Nevada, USA, where geothermal resources with moderate temperatures are

abundant. Additionally, by enabling geothermal development in non-volcanic areas

through engineered reservoirs, Enhanced Geothermal Systems (EGS) offer a

significant opportunity.

Increasing Energy Security and Grid Stability Needs

By lowering dependency on imported fuels and offering

steady, long-term electricity output, geothermal power promotes energy

security. This is especially crucial for developing economies and island

states. One of the biggest geothermal producers in the world, the Philippines,

uses geothermal energy to stabilize electricity rates and reduce reliance on

fuel imports. By guaranteeing a steady supply, geothermal power performs a

complementary function as grids include larger percentages of intermittent renewable

energy sources like solar and wind.

Expanding Applications Beyond Power Generation

Geothermal energy offers prospects in direct-use

applications, industrial operations, and district heating in addition to power

generation. In an effort to decarbonize urban heat supply, European nations

like France and Germany are increasing the use of geothermal district heating

systems. Co-generation of power and heat increases market potential and

enhances project economics, particularly in colder climates.

Emerging Markets and Private Sector Participation

There is significant untapped geothermal potential in

emerging countries in Latin America, Africa, and Southeast Asia. New

opportunities are being made possible by the increased involvement of private

developers, which is being supported by international organizations like the

World Bank. The Olkaria geothermal complex in Kenya, for instance, serves as an

example of how public-private cooperation may expand geothermal capacity while

fostering economic growth.

Geothermal Power Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 7.57 Billion |

|

Market Forecast in 2033 |

USD 12.61 Billion |

|

CAGR % 2025-2033 |

6.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Comprehensive global

geothermal power market size and forecast analysis, product type and

technology assessment, distribution channel evaluation, end-user consumption

trends, power generation capacity and installation performance evaluation,

regional and country-level market insights, competitive landscape and market

share analysis, technological advancements in geothermal systems and drilling

technologies, digital transformation and data analytics impact, growth

drivers, challenges, opportunities, and strategic insights for geothermal

developers, equipment suppliers, utilities, and investors. |

|

Segments Covered |

●

By Power Station

Type ●

By End Use |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Switzerland 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

South Africa |

Geothermal Power Market

Report Segmentation Analysis

The global geothermal power

market analysis is segmented by Power Station Type, End Use, and Region.

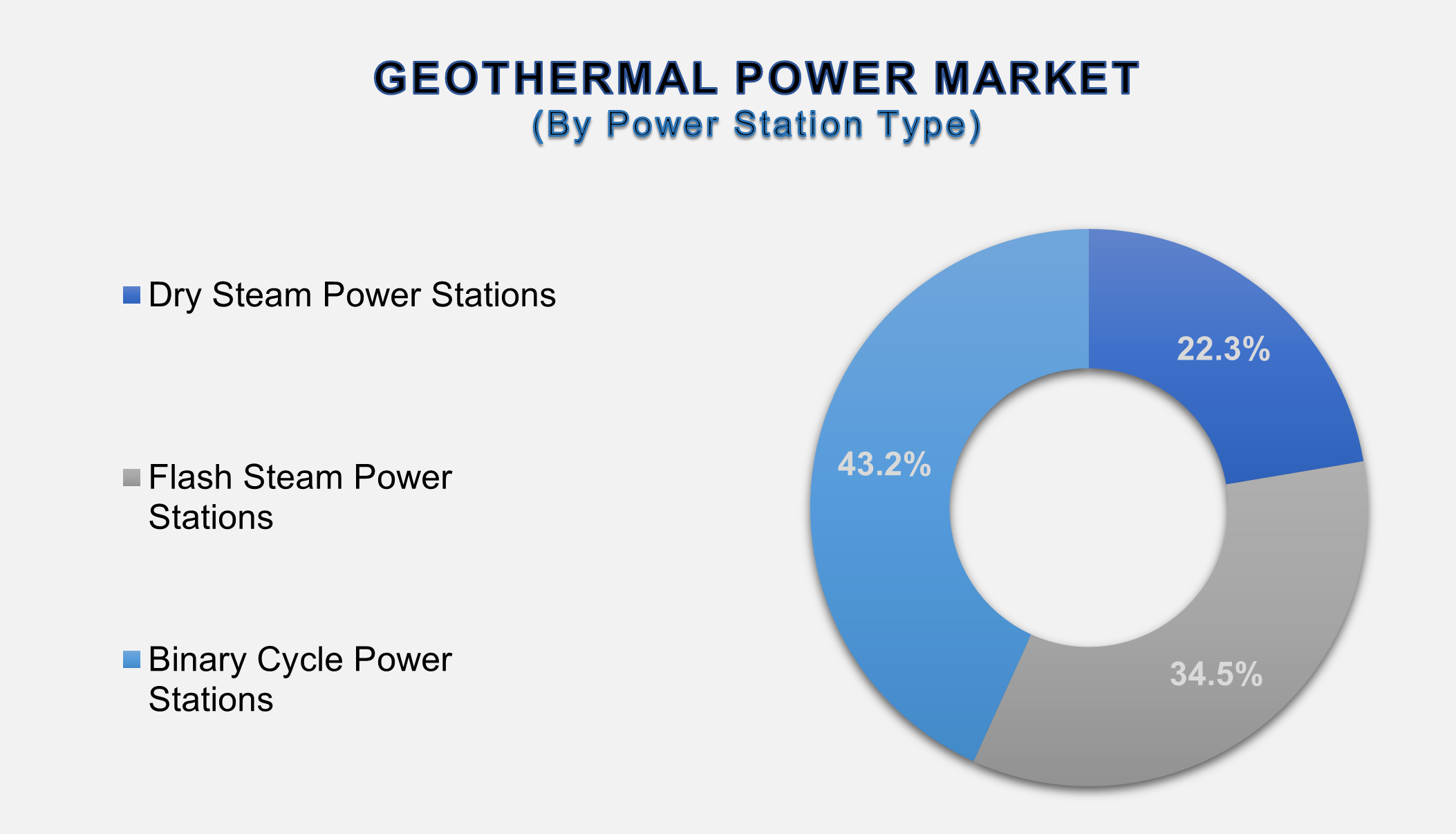

The Binary Power Cycle

Stations segment dominated the market in 2025 and is projected to grow at the

highest CAGR during the forecast period.

By Product Type, the geothermal

power market is segmented into dry steam power stations, flash steam power

stations, and binary cycle power stations. The binary power cycle stations

segment accounts for the largest share of the global geothermal power market. A

crucial technology in the geothermal power industry, binary power cycle

stations are especially well-suited for geothermal resources with low to medium

temperatures. Binary cycle stations, in contrast to flash or dry steam plants,

employ geothermal fluid to heat a secondary working fluid with a lower boiling

point, like pentane or isobutane. The geothermal fluid is reinjected into the

reservoir while this secondary fluid evaporates and powers a turbine. In

addition to this, binary plants function as closed-loop systems with almost no

emissions and little effect on the environment. These stations increase market

potential by enabling geothermal development in areas that were previously

thought to be unprofitable. Binary cycle stations are becoming more and more

significant in contemporary geothermal power generation due to their high

efficiency, modular design, and compatibility with Enhanced Geothermal Systems

(EGS).

The Industrial segment

holds the highest share of the End Use Segment over the forecast period

Based

on end use, the market is bifurcated into residential, commercial, industrial,

and others. The industrial segment accounts for the largest share of the

market. Geothermal energy is being utilized more and more in the industrial

sector to support combined heat and power (CHP), electricity generation, and

process heat. Since geothermal energy can produce steady, continuous heat at a

range of temperatures, it is advantageous to industries including food and

beverage processing, pulp and paper, chemical manufacturing, mining, and

textiles. Geothermal heat, for instance, is utilized for washing, drying,

pasteurization, and steam production, which lessens reliance on fossil fuels

and lowers operational expenses. In order to increase energy efficiency and dependability,

industrial enterprises close to geothermal resources can incorporate on-site

geothermal power plants. Geothermal energy offers an affordable, low-emission

option for long-term industrial energy needs as businesses look to satisfy

sustainability goals and decarbonize operations.

The following segments are

part of an in-depth analysis of the global Geothermal Power Market:

|

Market

Segments |

|

|

By Power

Station Type |

●

Dry Steam Power

Stations ●

Flash Steam Power

Stations ●

Binary Cycle Power

Stations |

|

By End Use |

●

Residential ●

Commercial ●

Industrial ●

Others |

Geothermal Power Market Share Analysis by Region

The Asia-Pacific region

is projected to hold the largest share of the global geothermal power market

over the forecast period.

The

Asia-Pacific region is projected to hold the largest share of the global

geothermal power market over the forecast period and is also expected to be the

fastest-growing region. The market for geothermal power in Asia-Pacific is

expected to increase significantly due to the region's extensive geothermal

resources, growing energy demand, and robust government backing for clean

energy. Leading nations include Japan, New Zealand, Indonesia, and the

Philippines, which are among the top producers of geothermal electricity

worldwide. Particularly in Indonesia's Java and Sumatra regions, exploration

and plant development are being made easier by strategic policies, advantageous

feed-in tariffs, and public-private partnerships. Enhanced Geothermal Systems

(EGS) and binary cycle plants are seeing an increase in investment due to

technological advancements and risk-mitigation funding. The region's growing

industrial base and emphasis on energy security encourage the use of geothermal

energy. Asia-Pacific continues to be a vital and dynamic market for geothermal

expansion as countries prioritize decarbonization and affordable electricity.

Global

Geothermal Power Market Recent Developments News:

●

In October 2023, Ormat

Technologies Inc. expanded its renewable energy asset base and portfolio by

purchasing a 150 MW portfolio of solar and geothermal assets from Enel Green

Power North America for about $271 million.

●

In June 2025, Calpine

Corporation increased its geothermal capacity at The Geysers by 7 MW in

partnership with MCE, and the new output is began supplying sustainable energy

to nearby towns.

●

In November 2025, the

Ulubelu Green Hydrogen Pilot Project, which combines geothermal energy with

green hydrogen technology, was started by PT Pertamina Geothermal Energy (PGE)

as an example of cross-sector decarbonization efforts.

The Global

Geothermal Power Market is dominated by a few large companies, such as

●

Ormat Technologies,

Inc.

●

Calpine Corporation

●

Enel Green Power

S.p.A.

●

Pertamina Geothermal

Energy

●

Kenya Electricity

Generating Company (KenGen)

●

Energy Development

Corporation (EDC)

●

Chevron Corporation

●

Contact Energy Limited

●

Mitsubishi Power

●

Toshiba Energy Systems

& Solutions

●

General Electric (GE)

●

Turboden S.p.A.

●

Ansaldo Energia S.p.A.

●

Atlas Copco Group

●

Exergy International

S.r.l.

●

Innergex Renewable

Energy Inc.

●

TAS Energy Inc.

●

Climeon AB

●

Iceland Drilling

Company Ltd.

● Reykjavik Geothermal Ltd.

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global Geothermal Power Market Introduction and Market Overview

1.1.

Objectives of the Study

1.2.

Global Geothermal Power Market Scope and Market Estimation

1.2.1.Global Geothermal

Power Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Geothermal

Power Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Power Station

Type of Global Geothermal Power Market

1.3.2.End Use of

Global Geothermal Power Market

1.3.3.Region of

Global Geothermal Power Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Geothermal Power Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Geothermal Power Market Estimates & Forecast Trend Analysis, by Power Station Type

4.1.

Global Geothermal Power Market Revenue (US$ Bn) Estimates and

Forecasts, by Power Station Type, 2020 - 2033

4.1.1.Dry Steam

Power Stations

4.1.2.Flash Steam

Power Stations

4.1.3.Binary Cycle

Power Stations

5. Global Geothermal Power Market Estimates & Forecast Trend Analysis, by End Use

5.1.

Global Geothermal Power Market Revenue (US$ Bn) Estimates and

Forecasts, by End Use, 2020 - 2033

5.1.1.Residential

5.1.2.Commercial

5.1.3.Industrial

5.1.4.Others

6.

Global

Geothermal Power Market Estimates & Forecast Trend Analysis, by Region

6.1.

Global Geothermal Power Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East

& Africa

6.1.5.Latin America

7.

North America Geothermal

Power Market: Estimates & Forecast

Trend Analysis

7.1.

North America Geothermal Power Market Assessments & Key

Findings

7.1.1.North America

Geothermal Power Market Introduction

7.1.2.North America

Geothermal Power Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Power Station Type

7.1.2.2. By End Use

7.1.2.3.

By Country

7.1.2.3.1.

The U.S.

7.1.2.3.2.

Canada

8.

Europe Geothermal

Power Market: Estimates & Forecast

Trend Analysis

8.1.

Europe Geothermal Power Market Assessments & Key Findings

8.1.1.Europe Geothermal

Power Market Introduction

8.1.2.Europe Geothermal

Power Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Power Station Type

8.1.2.2. By End Use

8.1.2.3. By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Russia

8.1.2.3.7.

Rest

of Europe

9.

Asia Pacific Geothermal

Power Market: Estimates & Forecast

Trend Analysis

9.1.

Asia Pacific Geothermal Power Market Assessments & Key

Findings

9.1.1.Asia Pacific Geothermal

Power Market Introduction

9.1.2.Asia Pacific Geothermal

Power Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Power Station Type

9.1.2.2. By End Use

9.1.2.3.

By Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South Korea

9.1.2.3.6.

Rest of Asia Pacific

10.

Middle East & Africa Geothermal Power Market:

Estimates & Forecast Trend Analysis

10.1. Middle

East & Africa Geothermal Power Market Assessments & Key Findings

10.1.1.

Middle East & Africa Geothermal

Power Market Introduction

10.1.2.

Middle East & Africa Geothermal

Power Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Power Station Type

10.1.2.2. By End Use

10.1.2.3.

By Country

10.1.2.3.1.

UAE

10.1.2.3.2.

Saudi Arabia

10.1.2.3.3.

South Africa

10.1.2.3.4. Rest of MEA

11.

Latin America Geothermal

Power Market: Estimates & Forecast

Trend Analysis

11.1. Latin

America Event Industry Assessments & Key Findings

11.1.1.

Latin America Geothermal Power Market Introduction

11.1.2.

Latin America Geothermal Power Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

11.1.2.1. By Power Station Type

11.1.2.2. By End Use

11.1.2.3.

By Country

11.1.2.3.1.

Brazil

11.1.2.3.2.

Mexico

11.1.2.3.3.

Argentina

11.1.2.3.4. Rest of LATAM

12.

Country Wise Market: Introduction

13. Competition

Landscape

13.1. Global

Geothermal Power Market Product Mapping

13.2. Global

Geothermal Power Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

13.3. Global

Geothermal Power Market Tier Structure Analysis

13.4. Global

Geothermal Power Market Concentration & Company Market Shares (%) Analysis,

2024

14. Company

Profiles

14.1.

Ormat Technologies, Inc.

14.1.1.

Company Overview & Key Stats

14.1.2.

Financial Performance & KPIs

14.1.3.

Product Portfolio

14.1.4.

SWOT Analysis

14.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

14.2.

Calpine Corporation

14.3.

Enel Green Power S.p.A.

14.4.

Pertamina Geothermal Energy

14.5.

Kenya Electricity Generating Company (KenGen)

14.6.

Energy Development Corporation (EDC)

14.7.

Chevron Corporation

14.8.

Contact Energy Limited

14.9.

Mitsubishi Power

14.10.

Toshiba Energy Systems & Solutions

14.11.

General Electric (GE)

14.12.

Turboden S.p.A.

14.13.

Ansaldo Energia S.p.A.

14.14.

Atlas Copco Group

14.15.

Exergy International S.r.l.

14.16.

Innergex Renewable Energy Inc.

14.17.

TAS Energy Inc.

14.18.

Climeon AB

14.19.

Iceland Drilling Company Ltd.

14.20.

Other Prominent Players

15.

Research

Methodology

15.1. External

Transportations / Databases

15.2. Internal

Proprietary Database

15.3. Primary

Research

15.4. Secondary

Research

15.5. Assumptions

15.6. Limitations

15.7. Report

FAQs

16.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables