Healthcare BPO Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Payer Service (Human Resource Management Claims Management, Customer Relationship Management (CRM), Operational/Administrative Management, Care Management, Provider Management, Other) By Provider Service (Patient Enrolment And Strategic Planning, Patient Care Service, Revenue Cycle Management) By Pharmaceutical Service (Research And Development, Manufacturing, Non-Clinical Services, Supply Chain Management And Logistics, Sales And Marketing Services, Other Non-Clinical Services) And Geography

2025-10-31

Healthcare

Swetal (Research Analyst)

Description

Healthcare BPO Market Overview

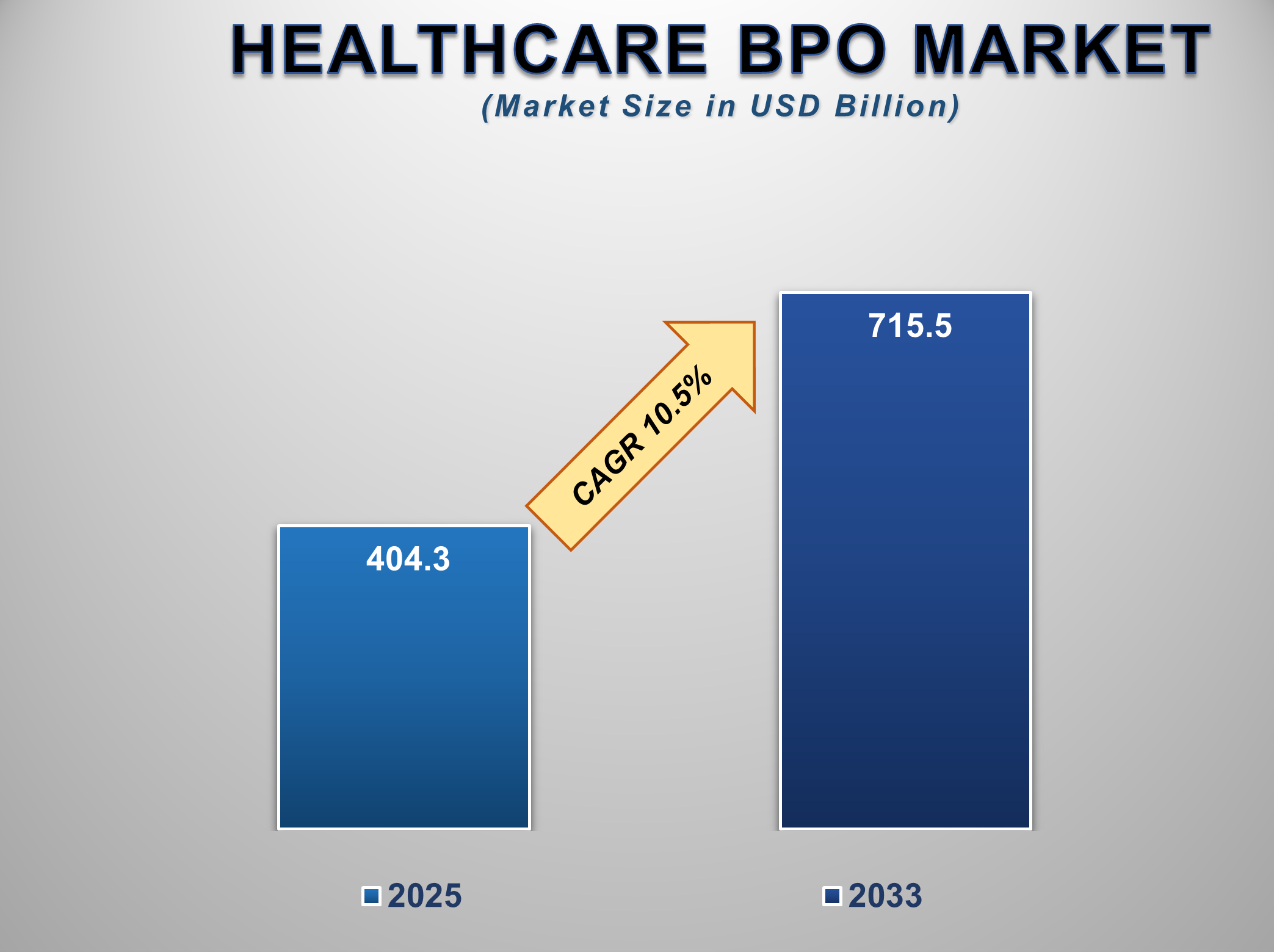

The Global Healthcare BPO Market is projected to grow from US$ 404.3 billion in 2025 to approximately US$ 715.5 billion by 2033, reflecting a CAGR of 7.8% during the forecast period. This growth is primarily fueled by the rising need for cost-efficient, scalable, and effective healthcare services amid increasing operational and administrative complexities across the healthcare ecosystem.

Healthcare Business Process

Outsourcing (BPO) involves delegating non-core but essential functions such as

medical billing, claims processing, coding, data entry, and customer support to

third-party service providers. The market’s expansion is being driven by

mounting administrative burdens on healthcare organizations, growing patient

care demands, and the pressure on providers, payers, and hospitals to

streamline operations. A key driver is the rising focus on reducing operational

costs so that healthcare organizations can prioritize clinical excellence and

patient satisfaction.

Healthcare BPO Market Drivers and Opportunities

The rising need for cost reduction in healthcare operations

is anticipated to lift the healthcare BPO market during the forecast period

The growing pressure on healthcare service

providers to control operational costs is the key driver of the worldwide

healthcare BPO market. With healthcare costs escalating due to the growing

number of patients, complex treatments, and compliance costs, the outsourcing

of non-core processes becomes increasingly desirable. Activities like medical

billing, processing of claims, transcription, and coding take too long and

entail high costs when done in-house. With the help of specialized third-party

service firms, healthcare organizations achieve streamlined processes, lower

administrative overhead, and dedicate more time to patients. This saving in

costs not only increases profitability but also aids in scalability, primarily

for mid-sized hospitals and clinics. Also, the worldwide healthcare BPO market

will see high growth as value-based models of healthcare grow, and there will

be increasing demand for transparency and efficiency. With mounting competition

and fund constraints, healthcare service providers are forced to pursue

operational effectiveness, prompting an increase in the rate of adoption of

BPO. Outsourcing also provides access to talent and the most updated

technologies without the need to bear the huge costs of setup. According to

market analysis patterns, the driver will remain key in shaping market size and

composition, particularly in the case of developing economies where the

healthcare system continues to grow.

Stringent regulatory requirements and administrative burden

are vital drivers for influencing the growth of the global healthcare BPO

market

The increasing complexity of healthcare

regulation in various countries has created an administrative workload on

hospitals and insurers, hence fueling the healthcare BPO market. Meeting HIPAA

(Health Insurance Portability and Accountability Act), ICD-10 standards, and

other data security requirements takes devoted resources and know-how.

Healthcare BPO service companies furnish specialized compliance solutions,

allowing the provider to stay compliant and minimize liability exposures.

Outsourcing compliance-intensive processes like medical coding, claim

adjudications, and patient data management frees internal resources.

Furthermore, the market research suggests that healthcare organizations

increasingly depend on vendors to handle documentation and regulation updates

to stay abreast of the continuously changing global regulation landscape. With

ongoing shifts in insurance policy and government healthcare reform, the

resource and agility of the BPO come to the fore to adapt rapidly. This trend

is projected to fuel steady market growth, as healthcare organizations, in

particular small and mid-size providers, increasingly discover the advantage of

delegating compliance-related processes to stay clear of penalties and devote

more time to the medical competencies.

Rising Demand for Revenue Cycle Management (RCM) is poised to

create significant opportunities in the global Healthcare BPO Market

The increasing significance of efficient revenue

cycle management (RCM) in healthcare facilities creates a vital business

opportunity for BPO providers. RCM encompasses the tracking of patient care

from the first appointment to final payment, including registration, insurance

verification, medical coding, submission of claims, and collections. With

intricate billing cycles, regular policy modifications, and denial of insurance

claims, RCM has grown increasingly difficult for healthcare organizations to tackle

in-house. BPO companies provide specialized RCM services that automate

processes, minimize billing inaccuracies, and accelerate reimbursements. This

benefits the financial health and operational effectiveness of a provider

directly. The demand for RCM services also increases with the number of insured

patients and the increasing regulatory examination of billing correctness. With

healthcare organizations looking back at ways to minimize revenue leakage and

maximize claim success, the outsourcing of RCM becomes a key business

imperative. Projected trends foretell major market size growth in the RCM

outsource market, particularly in North America and Europe, where healthcare

expenses remain the highest. End-to-end RCM service specialists among the BPO

vendors will be in a great position to capitalize on the swelling demand.

Healthcare BPO Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 404.3 Billion |

|

Market Forecast in 2033 |

USD 715.5 Billion |

|

CAGR % 2025-2033 |

7.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Payer Service ●

By Provider Service ●

By Pharmaceutical Service |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Healthcare BPO Market Report Segmentation Analysis

The Global Healthcare BPO Market

Industry Analysis is Segmented By Payer Service, By Provider Service, By

Pharmaceutical Service, and By Region.

The claims management segment is anticipated to hold the

highest share of the global healthcare BPO market during the projected

timeframe

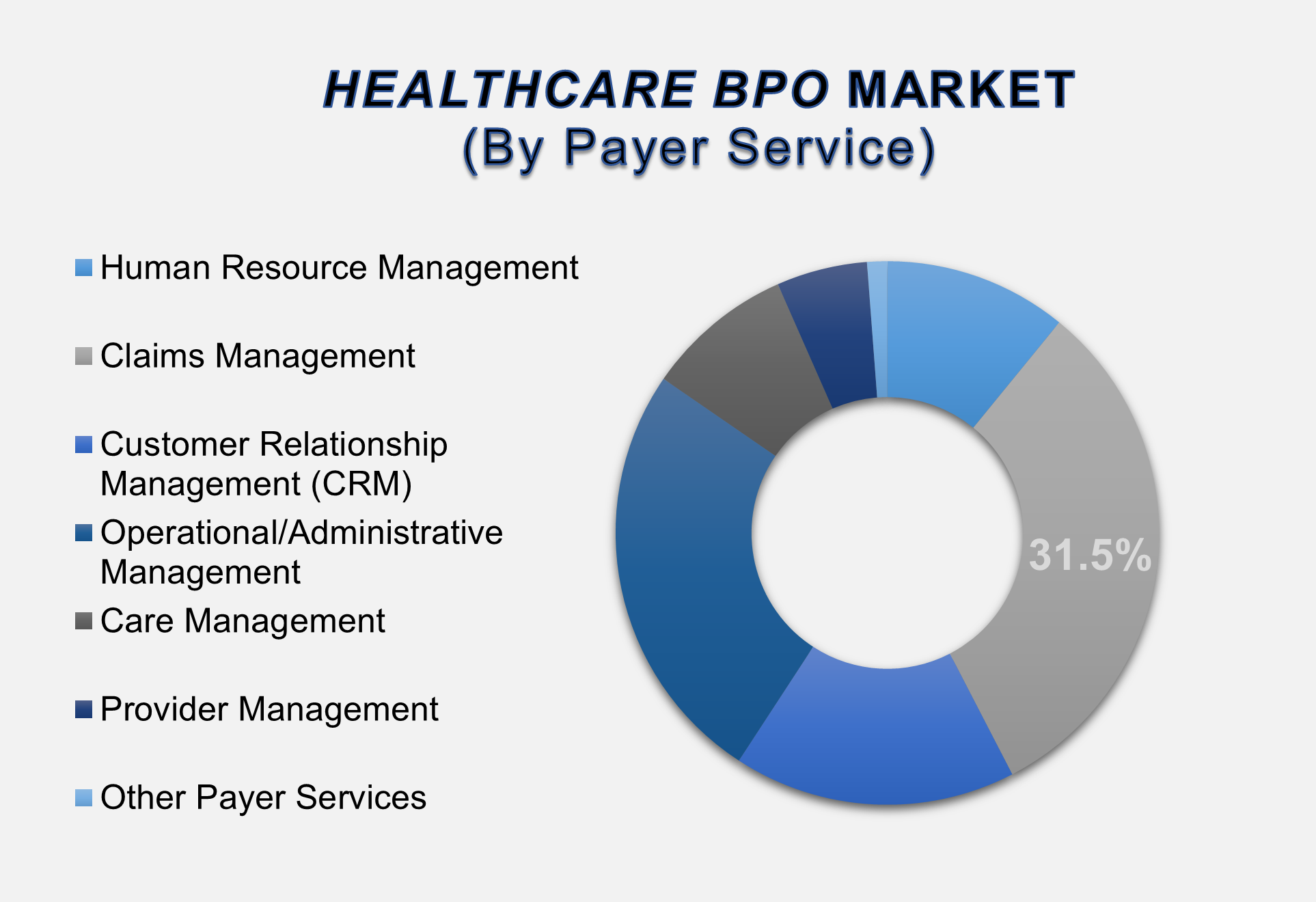

Based on Payer Service, the market is segmented into Human Resource Management, Claims Management, Customer Relationship Management (CRM), Operational/Administrative Management, Care Management, Provider Management, and Other Payer Services. The Claims Management segment is expected to account for the largest market share of 31.5% in the global Healthcare BPO Market. This owes to the growing sophistication of healthcare claim processes, increasing enrollments in insurance, and the necessity for accuracy and promptness in the reimbursement process. Insurers and healthcare providers increasingly outsource claim processing to third-party vendors to minimize administrative errors, cut down on delays, and meet the requirements of regulation.

The revenue cycle management segment is anticipated to hold

the highest share of the market over the forecast period

Based on Provider Service, the

market is segmented into Patient Enrolment and Strategic Planning, Patient Care

Service, and Revenue Cycle Management (RCM). In 2024, the segment of revenue

cycle management is expected to have the maximum market share in the forecast

period. This is due to the growing complexity in healthcare billing operations,

coding regulations, insurance verification processes, and the focus on

enhancing cash flow and minimizing denials of claims. RCM allows the healthcare

provider to maximize revenue generation while facilitating timely reimbursement

of services rendered.

The research and development segment dominated the market in

2024 and is predicted to grow at the highest CAGR over the forecast period

Based on Pharmaceutical Service,

the market is segmented into Research and Development, Manufacturing,

Non-clinical Services, Supply Chain Management and Logistics, Sales and

Marketing Services, and Other Non-clinical Services. The Research and Development

(R&D) segment is dominating and is also expected to grow at the highest

CAGR through the forecast period. With the increasing need for faster drug

discovery, R&D cost-cutting in processes, and compliance with regulations,

pharmaceutical firms have been increasingly outsourcing their R&D processes

to specialized BPO service providers.

The following segments are part of an in-depth analysis of the global

Healthcare BPO Market:

|

Market Segments |

|

|

By Payer Service |

●

Human Resource

Management ●

Claims Management ●

Customer

Relationship Management (CRM) ●

Operational/Administrative

Management ●

Care Management ●

Provider Management ●

Other Payer Services |

|

By Provider Service |

●

Patient Enrolment

and Strategic Planning ●

Patient Care Service ●

Revenue Cycle

Management |

|

By Pharmaceutical Service |

●

Research and

Development ●

Manufacturing ●

Non-clinical

Services ●

Supply Chain

Management and Logistics ●

Sales and Marketing

Services ●

Other Non-clinical

Services |

Healthcare BPO Market

Share Analysis by Region

North America is

projected to hold the largest share of the global healthcare BPO market over

the forecast period

The North America region

dominated the Global Healthcare BPO Market and held a significant 41.6% market

share in 2024. This dominance in the region can be attributed to the region’s

highly developed healthcare ecosystem, the prevalence of top pharmaceutical and

healthcare service companies, and the earliest adoption of the technique of

contracting out to curtail administrative costs and enhance business process

efficiencies. More importantly, the U.S. has been at the forefront in

contracting out services involving the management of claims, revenue cycles,

and pharmaceutical research and development, owing to the mounting healthcare

costs and rising regulation complexity. Further, the use of electronic health

records (EHR), the growing concentration in value-based healthcare models, and

the incorporation of sophisticated IT solutions also contribute to the demand

for the contracting out of non-core healthcare services. The region’s

established contracting out ecosystem, coupled with the presence of skilled personnel

and the permissiveness of the regulation regime, continues to boost the market

growth in North America.

Further, the Asia Pacific region

is also expected to have the highest CAGR in the period under consideration.

Growth in the region is largely fuelled by the growing healthcare

infrastructure, investments in digital healthcare, and the trend of business process

offshoring from developed countries to affordable destinations such as India

and the Philippines. The region has abundant talent and resources, and the

development of telehealth, IT, and data management capabilities makes it the

region to watch in the growth of the healthcare BPO market in the long run.

Healthcare BPO Market

Competition Landscape Analysis

The Healthcare Payer BPO market

features major players such as Cognizant, Hinduja Global Solutions Limited,

EXLService Holdings, Inc., Hewlett Packard Enterprise, Accenture, Genpact, HCL

Technologies Limited, Wipro, and Capgemini. To strengthen their market

position, these companies are actively expanding their customer base through

strategic initiatives, including mergers, acquisitions, and partnerships with

other healthcare and BPO firms.

Global Healthcare BPO

Market Recent Developments News:

●

In April 2024,

Accenture Plc completed its acquisition of Health Unlimited, a strategic move

to bolster its healthcare services and amplify its generative AI capabilities.

The deal enhances Accenture’s expertise in behavioral science, customer

strategy, and CRM activation, positioning the firm to deliver more data-driven,

patient-centric solutions.

●

In May 2024, Wipro

Limited announced a collaboration with Independent Health, a leading nonprofit

health plan, to implement its Medicare Prescription Payment Plan (MPPP360)

platform. This initiative aims to simplify and optimize the prescription

payment process for Medicare beneficiaries across Western New York.

The Global Healthcare

BPO Market is dominated by a few large

companies, such as

●

Accenture plc.

●

Cognizant Technology Solutions Corporation

●

Tata Consultancy Services Limited

●

Xerox Corporation

●

WNS (Holdings) Limited

●

Omega Healthcare Management Services

●

R1 RCM

●

Invensis Technologies

●

UnitedHealth Group

●

HCL Technologies Limited

●

NTT Data Corporation

●

IQVIA Holdings Inc.

●

Mphasis

●

Genpact Limited

●

Wipro Limited

●

Infosys BPM

●

Firstsource

●

International Business Machines Corporation

●

GeBBS Healthcare Solutions

●

Capgemini SE

●

Parexel International

●

Access Healthcare

●

Sutherland Global

●

Akurate Management Solutions

●

AGS Health

● Others

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Healthcare BPO Market Introduction and Market Overview

- Objectives of the Study

- Global Healthcare BPO Market Scope and Market Estimation

- Global Healthcare BPO Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Healthcare BPO Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Payer Service of Global Healthcare BPO Market

- Provider Service of Global Healthcare BPO Market

- Pharmaceutical Service of Global Healthcare BPO Market

- Region of Global Healthcare BPO Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Key Product/Brand Analysis

- Technological Advancements

- Key Developments

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Insights on Cost-effectiveness of Healthcare BPO

- Key Regulation

- Global Healthcare BPO Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Healthcare BPO Market Estimates & Forecast Trend Analysis, by Payer Service

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Payer Service, 2020 - 2033

- Human Resource Management

- Claims Management

- Customer Relationship Management (CRM)

- Operational/Administrative Management

- Care Management

- Provider Management

- Other Payer Services

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Payer Service, 2020 - 2033

- Global Healthcare BPO Market Estimates & Forecast Trend Analysis, by Provider Service

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Provider Service, 2020 - 2033

- Patient Enrolment and Strategic Planning

- Patient Care Service

- Revenue Cycle Management

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Provider Service, 2020 - 2033

- Global Healthcare BPO Market Estimates & Forecast Trend Analysis, by Pharmaceutical Service

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Pharmaceutical Service, 2020 - 2033

- Research and Development

- Manufacturing

- Non-clinical Services

- Supply Chain Management and Logistics

- Sales and Marketing Services

- Other Non-Clinical Services

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Pharmaceutical Service, 2020 - 2033

- Global Healthcare BPO Market Estimates & Forecast Trend Analysis, by Region

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Healthcare BPO Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Healthcare BPO Market: Estimates & Forecast Trend Analysis

- North America Healthcare BPO Market Assessments & Key Findings

- North America Healthcare BPO Market Introduction

- North America Healthcare BPO Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Payer Service

- By Provider Service

- By Pharmaceutical Service

- By Country

- The U.S.

- Canada

- North America Healthcare BPO Market Assessments & Key Findings

- Europe Healthcare BPO Market: Estimates & Forecast Trend Analysis

- Europe Healthcare BPO Market Assessments & Key Findings

- Europe Healthcare BPO Market Introduction

- Europe Healthcare BPO Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Payer Service

- By Provider Service

- By Pharmaceutical Service

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Rest of Europe

- Europe Healthcare BPO Market Assessments & Key Findings

- Asia Pacific Healthcare BPO Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Healthcare BPO Market Introduction

- Asia Pacific Healthcare BPO Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Payer Service

- By Provider Service

- By Pharmaceutical Service

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Healthcare BPO Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Healthcare BPO Market Introduction

- Middle East & Africa Healthcare BPO Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Payer Service

- By Provider Service

- By Pharmaceutical Service

- By Country

- UAE

- Saudi Arabia

- Turkey

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Healthcare BPO Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Healthcare BPO Market Introduction

- Latin America Healthcare BPO Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Payer Service

- By Provider Service

- By Pharmaceutical Service

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Healthcare BPO Market Product Mapping

- Global Healthcare BPO Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Healthcare BPO Market Tier Structure Analysis

- Global Healthcare BPO Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Accenture plc.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Accenture plc.

* Similar details would be provided for all the players mentioned below

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Xerox Corporation

- WNS (Holdings) Limited

- Omega Healthcare Management Services

- R1 RCM

- Invensis Technologies

- UnitedHealth Group

- HCL Technologies Limited

- NTT Data Corporation

- IQVIA Holdings Inc.

- Mphasis

- Genpact Limited

- Wipro Limited

- Infosys BPM

- Firstsource

- International Business Machines Corporation

- GeBBS Healthcare Solutions

- Capgemini SE

- Parexel International

- Access Healthcare

- Sutherland Global

- Akurate Management Solutions

- AGS Health

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables