Herbal Tea Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (ChamAomile Tea, Peppermint Tea, Ginger Tea, Hibiscus Tea, Green Herbal Tea Blends, Others); By Form (Tea Bags, Loose Leaf Tea, Instant Herbal Tea, Ready-to-Drink Herbal Tea); By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Convenience Stores, Others); By Application (Health & Wellness, Relaxation & Stress Management, Digestive Health, Immunity Support, Weight Management, Others), and Geography

2026-06-30

Consumer Products

Jaya Bundele (Research Analyst)

Description

Herbal Tea Market Overview

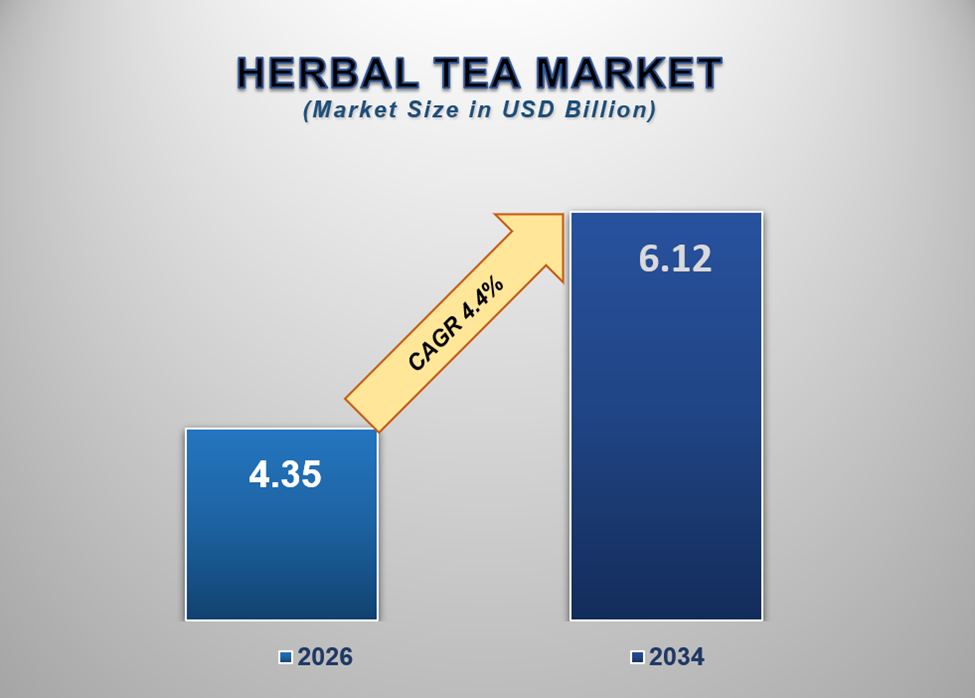

The global Herbal Tea Market was

valued at USD 4.35 billion in 2026 and is projected to reach USD 6.12

billion by 2034, expanding at a CAGR of 4.4% during the forecast period.

Market growth is being driven by increasing consumer awareness regarding

preventive healthcare, rising demand for natural and plant-based beverages,

growing preference for clean-label products, expanding interest in traditional

herbal remedies, and the increasing popularity of wellness-focused lifestyles

worldwide.

Herbal tea has evolved from a traditional

home remedy consumed in specific regions into a globally recognized wellness

beverage category. Unlike conventional teas derived from the Camellia sinensis

plant, herbal teas are prepared from a variety of herbs, flowers, spices,

fruits, roots, seeds, and other botanical ingredients, offering distinctive

flavors and potential health benefits. The growing consumer shift toward

healthier beverage alternatives has significantly contributed to the expansion

of the herbal tea industry.

Modern consumers are becoming increasingly

conscious of the relationship between diet and long-term health. As a result,

demand for beverages perceived as natural, functional, and minimally processed

has increased substantially. Herbal teas are often associated with benefits

such as relaxation, digestive support, immunity enhancement, detoxification,

hydration, and overall wellness, making them attractive to health-focused

consumers.

The rising prevalence of lifestyle-related

health concerns, including obesity, stress, digestive disorders, sleep

disturbances, and weakened immunity, is encouraging consumers to seek natural

wellness solutions. Herbal teas are frequently incorporated into daily routines

as a convenient and enjoyable way to support general health and well-being

without relying heavily on synthetic supplements or sugary beverages.

Consumer preference for clean-label

products has become a major factor influencing purchasing behavior. Shoppers

increasingly examine ingredient lists and favor products containing

recognizable botanical ingredients without artificial preservatives, colors, or

additives. Herbal tea manufacturers are responding by emphasizing transparency,

organic sourcing, sustainability, and ingredient authenticity.

The growing popularity of plant-based

lifestyles is further supporting market expansion. Consumers adopting

vegetarian, vegan, and flexitarian diets often seek beverages that align with

their broader health and sustainability values. Herbal teas naturally fit

within these preferences and are increasingly marketed as part of holistic

wellness lifestyles.

Innovation within the herbal tea sector

continues to create new growth opportunities. Manufacturers are introducing

blends featuring adaptogens, functional herbs, superfoods, probiotics,

antioxidants, and region-specific botanicals to meet evolving consumer demands.

Premiumization trends are also encouraging the development of specialty herbal

teas that emphasize unique flavor profiles, artisanal sourcing, and

wellness-focused positioning.

E-commerce platforms have significantly

improved consumer access to diverse herbal tea products. Online retail channels

allow brands to reach broader customer bases while educating consumers about

ingredient benefits, brewing methods, and wellness applications. This

accessibility has accelerated product discovery and adoption across global

markets.

Furthermore, increasing interest in

traditional medicinal systems such as Ayurveda, Traditional Chinese Medicine,

and other herbal healing practices is influencing consumer preferences. Many

herbal tea products incorporate ingredients historically associated with these

traditions, further enhancing their appeal among wellness-oriented consumers.

As demand for natural health-supporting beverages continues to grow and consumers increasingly prioritize preventive wellness strategies, the herbal tea market is expected to maintain steady expansion throughout the forecast period.

Herbal Tea Market Drivers and Opportunities

Rising Consumer Focus on Health and

Wellness Is Driving Market Growth

One of the primary factors fueling growth

in the herbal tea market is the increasing emphasis on health-conscious

consumption patterns.

Consumers worldwide are actively seeking

healthier beverage alternatives that offer both enjoyable taste experiences and

perceived wellness benefits. Growing awareness regarding the adverse effects

associated with excessive sugar consumption, artificial ingredients, and highly

processed beverages has encouraged a shift toward natural drink options.

Herbal teas are widely perceived as beverages

that support hydration and overall wellness while providing functional benefits

linked to specific botanical ingredients. Ingredients such as chamomile,

peppermint, ginger, turmeric, hibiscus, lemongrass, and echinacea are commonly

associated with relaxation, digestive support, immune health, and antioxidant

properties.

The growing prevalence of stress-related

health concerns has further increased demand for herbal tea products positioned

for relaxation and emotional well-being. Many consumers incorporate herbal tea

into daily routines as part of self-care practices aimed at promoting balance

and relaxation.

Additionally, increasing public awareness

regarding preventive healthcare is encouraging individuals to adopt lifestyle

habits that may support long-term health. Herbal teas align well with these

preferences due to their natural composition and wellness-oriented image.

As health and wellness continue to influence global purchasing decisions, herbal tea consumption is expected to increase steadily.

Growing Demand for Natural and

Plant-Based Products Is Accelerating Market Expansion

The broader shift toward plant-based

consumption is another major driver supporting market growth.

Consumers increasingly favor food and

beverage products derived from natural botanical sources. This trend is driven

by growing environmental awareness, ethical considerations, and interest in

minimally processed products. Herbal teas naturally appeal to these preferences

because they are plant-derived and often contain simple ingredient

compositions.

The clean-label movement has amplified

demand for products that offer transparency and recognizable ingredients.

Herbal tea manufacturers are responding by highlighting organic certifications,

sustainable sourcing practices, non-GMO ingredients, and environmentally

responsible packaging solutions.

Plant-based lifestyles are becoming more

mainstream across both developed and developing economies. As consumers seek

alternatives to conventional beverages, herbal teas provide a versatile option

that fits within various dietary patterns and wellness goals.

Additionally, consumers increasingly

appreciate the diversity of flavors available within the herbal tea category.

Botanical blends featuring fruits, flowers, spices, and herbs allow

manufacturers to create unique taste experiences while maintaining natural

product positioning.

As demand for plant-based and clean-label products continues to expand globally, the herbal tea market is expected to benefit significantly.

Functional Herbal Formulations and

Premium Product Innovation Present Major Opportunities

Product innovation is creating substantial

opportunities for growth within the herbal tea industry.

Consumers increasingly seek beverages that

provide targeted functional benefits beyond basic hydration. This has

encouraged manufacturers to develop herbal tea blends designed to support

specific wellness objectives such as immunity enhancement, digestive comfort,

stress management, sleep support, cognitive performance, detoxification, and

metabolic health.

The incorporation of adaptogenic herbs,

superfoods, botanical extracts, probiotics, and antioxidant-rich ingredients is

enabling brands to differentiate their offerings and appeal to health-conscious

consumers. Functional positioning is becoming an increasingly important

competitive strategy across the market.

Premiumization trends are also creating

attractive opportunities. Consumers are demonstrating willingness to pay higher

prices for herbal teas featuring premium ingredients, artisanal sourcing

methods, organic certifications, and unique regional botanicals. Specialty tea

products often emphasize authenticity, craftsmanship, and superior ingredient

quality.

Ready-to-drink herbal tea products

represent another rapidly expanding opportunity area. Busy consumers

increasingly seek convenient wellness beverages that can be consumed without

preparation. Manufacturers are responding with innovative packaged herbal tea

offerings that combine convenience with health-focused positioning.

Furthermore, digital commerce platforms

enable brands to educate consumers, promote ingredient benefits, and build

direct relationships with customers. This capability supports stronger brand

loyalty and facilitates market expansion.

As innovation continues driving consumer

engagement, manufacturers are expected to benefit from expanding premium and

functional herbal tea segments.

Herbal Tea Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 4.35 Billion |

|

Market Forecast in 2034 |

USD 6.12 Billion |

|

CAGR % 2026-2034 |

4.4% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production, Service Type, Growth Factors

and more |

|

Segments Covered |

∙ By Product Type |

|

Regional Scope |

● North America |

|

Country Scope |

U.S. |

Herbal Tea Market Report Segmentation Analysis

The global herbal tea market industry analysis is segmented into product type, form, distribution channel, application, and region.

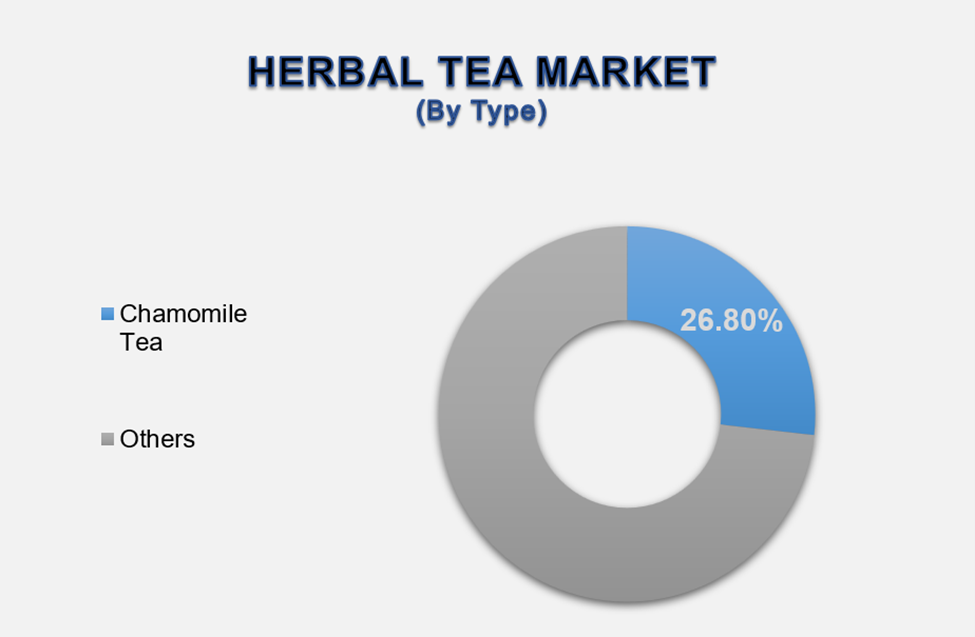

Chamomile Tea Segment Is Expected to

Dominate the Market During the Forecast Period

The chamomile tea segment accounted for

approximately 26.8% of the global market, making it one of the most

prominent product categories.

Chamomile tea remains highly popular among

consumers due to its longstanding association with relaxation, sleep support,

and stress reduction. Its mild flavor profile and broad consumer familiarity

contribute significantly to market demand.

The segment benefits from increasing

consumer interest in natural approaches to managing stress and improving sleep

quality. Many wellness-focused consumers regularly incorporate chamomile tea

into evening routines as part of broader self-care practices.

Manufacturers continue expanding

chamomile-based product offerings through innovative blends featuring

complementary ingredients such as lavender, lemon balm, honey, and mint. These

formulations enhance both flavor and perceived wellness benefits.

As awareness of natural wellness beverages continues growing, chamomile tea is expected to maintain its leading position within the herbal tea market.

Tea Bags Segment Is Expected to Lead the

Market by Form

Tea bags represent the largest form segment

within the herbal tea market.

Consumers highly value convenience,

consistency, portability, and ease of preparation, all of which contribute to

the widespread popularity of tea bag products. Tea bags enable consumers to

quickly prepare herbal beverages at home, at work, or while traveling.

Manufacturers have introduced a wide

variety of tea bag formats, including pyramid sachets, biodegradable materials,

and premium packaging solutions designed to enhance brewing performance and

sustainability.

The segment also benefits from strong

retail availability across supermarkets, convenience stores, specialty tea

outlets, and online platforms.

As convenience continues to influence purchasing decisions, tea bags are expected to remain the dominant product format.

Health & Wellness Segment Is

Expected to Dominate the Market by Application

Health and wellness applications account

for the largest share of herbal tea consumption globally.

Consumers increasingly view herbal tea as a

simple and enjoyable way to support broader wellness objectives. Products

positioned around immunity support, digestive health, stress management,

hydration, and antioxidant intake continue gaining popularity across diverse

demographic groups.

The growing emphasis on preventive

healthcare and self-directed wellness practices is encouraging regular herbal

tea consumption. Consumers are incorporating herbal beverages into daily

routines as part of holistic approaches to maintaining overall well-being.

Additionally, increasing educational

content regarding botanical ingredients and functional benefits is

strengthening consumer confidence in herbal tea products.

As wellness-oriented lifestyles continue

expanding globally, this application segment is expected to maintain its

leading market position.

Supermarkets & Hypermarkets Segment

Is Expected to Lead the Market by Distribution Channel

Supermarkets and hypermarkets represent the

largest distribution channel within the herbal tea market.

These retail formats provide extensive

product variety, convenient access, competitive pricing, and strong brand

visibility. Consumers frequently purchase herbal tea products during routine

grocery shopping trips, making supermarkets an important sales channel.

Retailers are increasingly expanding shelf

space dedicated to wellness beverages, organic products, and specialty teas in

response to growing consumer demand. Product promotions, sampling initiatives,

and in-store educational displays further support category growth.

The availability of both premium and mass-market herbal tea brands within these channels contributes to their continued dominance.

The following segments are part of an

in-depth analysis of the global Herbal Tea market:

|

Market Segments |

|

|

By Product Type |

∙ Chamomile Tea |

|

By

Form |

∙ Tea Bags |

|

Distribution

Channel |

∙ Supermarkets & Hypermarkets |

|

By

Application |

∙ Health &

Wellness |

Herbal Tea Market Share Analysis By Region

Europe is projected to dominate the global

herbal tea market, accounting for approximately 34.5% of total market

revenue in 2026.

The region benefits from a long-established

tea-drinking culture, strong consumer awareness regarding natural wellness

products, and increasing demand for organic and functional beverages. Countries

such as Germany, the United Kingdom, France, and Italy represent major

consumption markets.

North America remains a significant market

due to rising health consciousness, growing demand for plant-based beverages,

and increasing consumer interest in preventive wellness practices.

Asia-Pacific is expected to witness the

fastest growth during the forecast period, driven by expanding middle-class

populations, increasing disposable incomes, growing wellness awareness, and

strong cultural acceptance of herbal beverages.

Latin America and the Middle East & Africa are also experiencing growing demand as consumers increasingly embrace natural and health-focused beverage alternatives.

Herbal Tea Market Competition Landscape Analysis

The global herbal tea market is

characterized by intense competition, product innovation, brand

differentiation, and increasing emphasis on wellness-oriented marketing

strategies.

Market participants are focusing on organic

product development, sustainable sourcing practices, premium ingredient

selection, and functional formulation innovation. Companies are investing in

research and development to create unique botanical blends that address

evolving consumer wellness preferences.

Brand storytelling, ingredient

transparency, and sustainability initiatives are becoming increasingly

important competitive differentiators. Manufacturers are also leveraging

e-commerce channels and direct-to-consumer strategies to strengthen customer

engagement and brand loyalty.

As consumer demand for natural wellness beverages continues growing, competition is expected to intensify across both established and emerging market segments.

Global Herbal Tea Market Recent

Developments News:

∙ In April 2026, several beverage companies

expanded organic herbal tea product portfolios to address growing consumer

demand for clean-label wellness beverages.

∙ In January 2026, manufacturers introduced

new adaptogenic herbal tea formulations targeting stress management and

emotional wellness.

∙ In October 2025, premium tea brands

launched specialty botanical blends featuring regionally sourced herbs and

flowers.

∙ In July 2025, beverage companies expanded

ready-to-drink herbal tea offerings to capitalize on growing convenience

trends.

∙ In May 2025, major tea producers increased investments in sustainable sourcing programs and environmentally friendly packaging solutions.

The Global Herbal Tea Market is

Dominated by a Few Large Companies, Such As

∙ Unilever PLC

∙ Associated British Foods plc (Twinings)

∙ Celestial Seasonings, Inc.

∙ Traditional Medicinals, Inc.

∙ Yogi Tea GmbH

∙ The Republic of Tea, Inc.

∙ Bigelow Tea Company

∙ Tata Consumer Products Limited

∙ Dilmah Ceylon Tea Company PLC

∙ Pukka Herbs Ltd.

∙ Harney & Sons Fine Teas

∙ Numi Organic Tea

∙ Teavana Corporation

∙ Organic India Pvt. Ltd.

∙ Davidson's Organics

∙ Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Herbal Tea Market

Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Herbal Tea Market Scope and Market Estimation

1.2.1.

Global Herbal Tea Market

Overall Market Size (US$ Billion), Market CAGR (%), Market Forecast (2026 -

2034)

1.2.2.

Global Herbal Tea Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1.

Product Type of Global Herbal

Tea Market

1.3.2.

Form of Global Herbal Tea

Market

1.3.3.

Distribution Channel of Global

Herbal Tea Market

1.3.4.

Application of Global Herbal

Tea Market

1.3.5.

Region of Global Herbal Tea

Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Billion) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Functional Beverage Ecosystem and Herbal Wellness

Framework

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global Herbal Tea Market

Estimates & Historical Trend Analysis (2021 - 2025)

4.

Global Herbal Tea Market

Estimates & Forecast Trend Analysis, by Product Type

4.1. Global Herbal Tea Market Revenue (US$ Billion) Estimates and

Forecasts, by Product Type, 2021 - 2034

4.1.1.

Chamomile Tea

4.1.2.

Peppermint Tea

4.1.3.

Ginger Tea

4.1.4.

Hibiscus Tea

4.1.5.

Green Herbal Tea Blends

4.1.6.

Others

5.

Global Herbal Tea Market

Estimates & Forecast Trend Analysis, by Form

5.1. Global Herbal Tea Market Revenue (US$ Billion) Estimates and

Forecasts, by Form, 2021 - 2034

5.1.1.

Tea Bags

5.1.2.

Loose Leaf Tea

5.1.3.

Instant Herbal Tea

5.1.4.

Ready-to-Drink Herbal Tea

6.

Global Herbal Tea Market

Estimates & Forecast Trend Analysis, by Distribution Channel

6.1. Global Herbal Tea Market Revenue (US$ Billion) Estimates and

Forecasts, by Distribution Channel, 2021 - 2034

6.1.1.

Supermarkets & Hypermarkets

6.1.2.

Specialty Stores

6.1.3.

Online Retail

6.1.4.

Convenience Stores

6.1.5.

Others

7.

Global Herbal Tea Market

Estimates & Forecast Trend Analysis, by Application

7.1. Global Herbal Tea Market Revenue (US$ Billion) Estimates and

Forecasts, by Application, 2021 - 2034

7.1.1.

Health & Wellness

7.1.2.

Relaxation & Stress

Management

7.1.3.

Digestive Health

7.1.4.

Immunity Support

7.1.5.

Weight Management

7.1.6.

Others

8.

Global Herbal Tea Market

Estimates & Forecast Trend Analysis, by Region

8.1. Global Herbal Tea Market Revenue (US$ Billion) Estimates and

Forecasts, by Region, 2021 - 2034

8.1.1.

North America

8.1.2.

Europe

8.1.3.

Asia Pacific

8.1.4.

Middle East & Africa

8.1.5.

Latin America

9.

North America Herbal Tea

Market: Estimates & Forecast Trend Analysis

9.1. North America Herbal Tea Market Assessments & Key Findings

9.1.1.

North America Herbal Tea Market

Introduction

9.1.2.

North America Herbal Tea Market

Size Estimates and Forecast (2021 - 2034)

9.1.2.1.

By Product Type

9.1.2.2.

By Form

9.1.2.3.

By Distribution Channel

9.1.2.4.

By Application

9.1.2.5.

By Country

9.1.2.5.1.

U.S.

9.1.2.5.2.

Canada

10. Europe Herbal Tea Market: Estimates & Forecast Trend Analysis

10.1.

Europe Herbal Tea Market

Assessments & Key Findings

10.1.1.

Europe Herbal Tea Market

Introduction

10.1.2.

Europe Herbal Tea Market Size

Estimates and Forecast (2021 - 2034)

10.1.2.1.

By Product Type

10.1.2.2.

By Form

10.1.2.3.

By Distribution Channel

10.1.2.4.

By Application

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest of Europe

11. Asia Pacific Herbal Tea Market: Estimates & Forecast Trend

Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific Herbal Tea Market

Introduction

11.1.2.

Asia Pacific Herbal Tea Market

Size Estimates and Forecast (2021 - 2034)

11.1.2.1.

By Product Type

11.1.2.2.

By Form

11.1.2.3.

By Distribution Channel

11.1.2.4.

By Application

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6.

Rest of Asia Pacific

12. Middle East & Africa Herbal Tea Market: Estimates & Forecast

Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa Herbal

Tea Market Introduction

12.1.2.

Middle East & Africa Herbal

Tea Market Size Estimates and Forecast (2021 - 2034)

12.1.2.1.

By Product Type

12.1.2.2.

By Form

12.1.2.3.

By Distribution Channel

12.1.2.4.

By Application

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4.

Rest of MEA

13. Latin America Herbal Tea Market: Estimates & Forecast Trend

Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America Herbal Tea Market

Introduction

13.1.2.

Latin America Herbal Tea Market

Size Estimates and Forecast (2021 - 2034)

13.1.2.1.

By Product Type

13.1.2.2.

By Form

13.1.2.3.

By Distribution Channel

13.1.2.4.

By Application

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global Herbal Tea Market

Product Mapping

14.2.

Global Herbal Tea Market

Concentration Analysis

14.3.

Global Herbal Tea Market Tier

Structure Analysis

14.4.

Global Herbal Tea Market Share

Analysis (2025)

15. Company Profiles

15.1.

Unilever PLC

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

15.2.

Associated British Foods plc

(Twinings)

15.3.

Celestial Seasonings, Inc.

15.4.

Traditional Medicinals, Inc.

15.5.

Yogi Tea GmbH

15.6.

The Republic of Tea, Inc.

15.7.

Bigelow Tea Company

15.8.

Tata Consumer Products Limited

15.9.

Dilmah Ceylon Tea Company PLC

15.10.

Pukka Herbs Ltd.

15.11.

Harney & Sons Fine Teas

15.12.

Numi Organic Tea

15.13.

Teavana Corporation

15.14.

Organic India Pvt. Ltd.

15.15.

Davidson's Organics

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables