Home Entertainment Devices Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Smart Televisions, Soundbars, Home Theater Systems, Gaming Consoles, Streaming Devices, Blu-ray Players), By Technology (4K/UHD, 8K, HDR, OLED, QLED, Dolby Atmos) And Geography

2025-12-02

Consumer Products

Jaya Bundele (Research Analyst)

Description

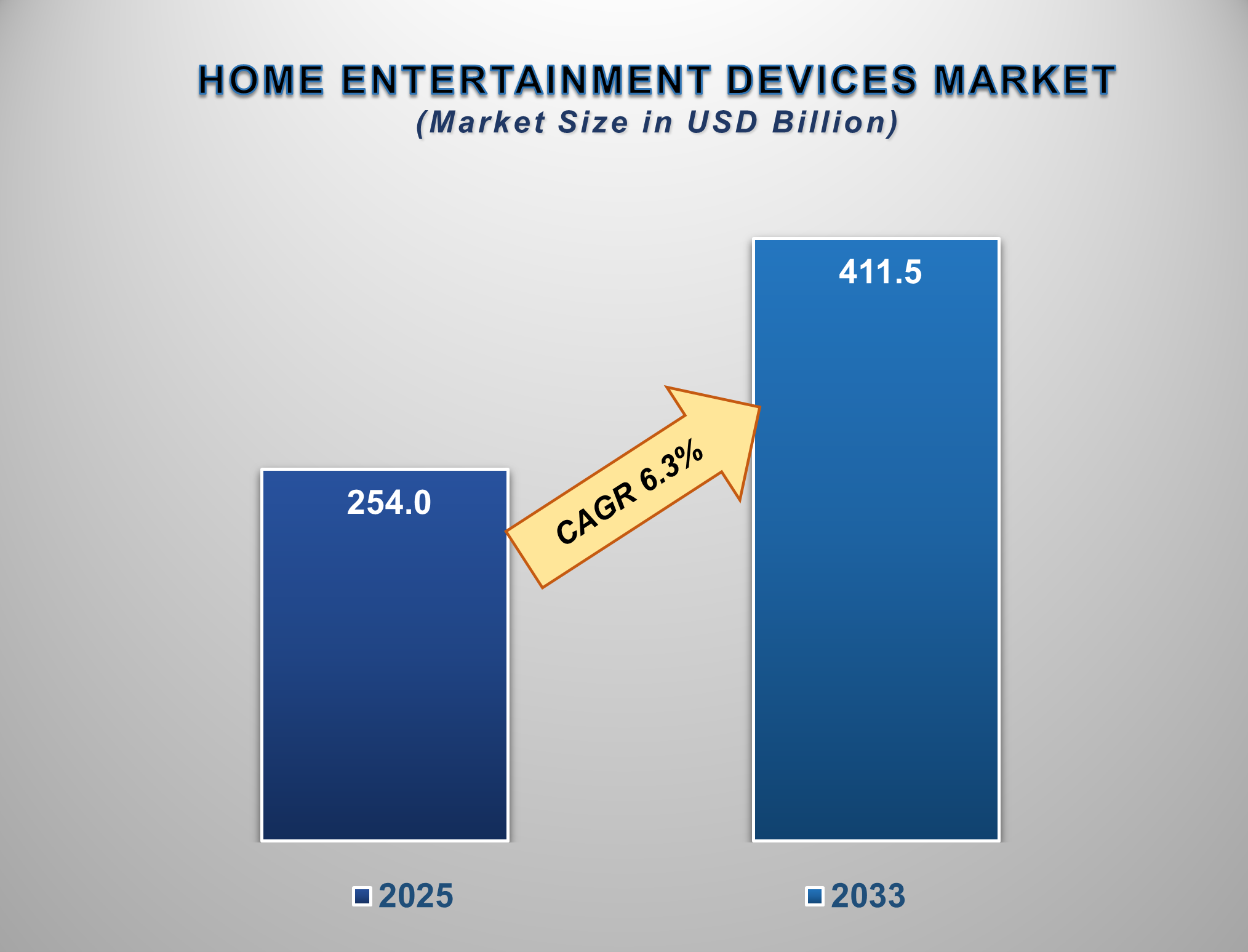

Home Entertainment Devices Market Overview

The Home Entertainment Devices Market is poised for a dynamic and transformative growth phase from 2025 to 2033, driven by the relentless consumer pursuit of immersive experiences, technological advancements in display and audio, and the ever-expanding ecosystem of digital content. The market is projected to be valued at approximately USD 254.0 billion in 2025 and is forecasted to reach nearly USD 411.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.3% during this period.

Home entertainment devices encompass a range of

consumer electronics designed for audio-visual enjoyment within the home,

including televisions, audio systems, and gaming hardware. The market's robust

expansion is primarily fueled by the global proliferation of over-the-top (OTT)

streaming services, which have created a

sustained demand for high-quality viewing hardware.

The transition towards premium, cinema-like

experiences at home is a significant factor, with consumers investing in

large-screen Smart TVs, high-fidelity sound systems, and next-generation gaming

consoles. Furthermore, the increasing affordability of advanced technologies

like 4K/UHD and the emergence of 8K are accelerating upgrade cycles. The

integration of Artificial Intelligence (AI) and the Internet of Things (IoT) for smart home connectivity and voice

control is further enhancing device functionality and user engagement. North

America and the Asia-Pacific are the dominant

markets, with the latter expected to witness the fastest growth due to a rising

middle class and rapid digitalization.

Home

Entertainment Devices Market Drivers and Opportunities

The Proliferation of Streaming Services and

Demand for High-Quality Content is the Primary Market Driver

The explosive growth of digital streaming

platforms like Netflix, Disney+, and Amazon Prime Video is the most powerful

engine driving the home entertainment devices market. The constant release of

high-budget, high-quality original content in 4K, HDR, and with immersive audio

formats like Dolby Atmos has created a compelling need for hardware that can

fully realize this potential. Consumers are no longer satisfied with basic

screens and built-in TV speakers; they are actively seeking smart TVs with robust operating systems, dedicated streaming

devices for smoother apps, and sophisticated audio equipment to replicate a

theatrical experience. This symbiotic relationship between content and hardware

ensures a continuous cycle of demand, as better content drives hardware

upgrades, and advanced hardware makes content more enjoyable, creating a solid,

long-term foundation for sustained market growth.

The Rise of the "Connected Home"

and Gaming as a Mainstream Entertainment is Driving Adoption

The evolution of the living room into a central

hub for a wide array of entertainment activities is a powerful catalyst for the

market. The deep integration of gaming consoles, such as the PlayStation and

Xbox series, which now serve as all-in-one entertainment centers, has

significantly boosted the demand for compatible high-performance TVs and audio

systems. Simultaneously, the smart home revolution has made voice-controlled

assistants and interconnected devices a standard expectation. Modern home entertainment

devices are increasingly designed to be part of this ecosystem, allowing for

seamless control and integration. This convergence of gaming, streaming, and

smart home functionality is driving consumers to invest in upgrading their

entire home entertainment setup, making it more versatile and central to daily

life.

The Advent of Next-Generation Technologies

and the Personalization of Audio-Visual Experiences Present Significant

Opportunities

The strategic development and commercialization

of cutting-edge technologies and the trend towards personalized setups are

creating significant growth frontiers for the home entertainment devices

market. Key opportunities lie in the gradual market penetration of 8K

resolution, MicroLED displays, and advanced audio formats like Dolby Atmos for

a more immersive soundscape.

Furthermore, there is immense potential in

catering to niche but growing segments, such as retro-gaming consoles, high-end

audiophile equipment, and projectors for dedicated home theaters. For

manufacturers, investing in AI-driven features like automated picture and sound

calibration, content-aware upscaling, and personalized content recommendations

allows them to command a premium price. Exploring new product categories, such

as VR/AR headsets for home entertainment, and leveraging direct-to-consumer channels

for curated, high-margin audio products are key strategies to capture untapped

market potential.

Home Entertainment

Devices Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 254.0 Billion |

|

Market Forecast in 2033 |

USD 411.5 Billion |

|

CAGR % 2025-2033 |

6.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product ●

By Technology |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Home Entertainment

Devices Market Report Segmentation Analysis

The global Home Entertainment

Devices Market industry analysis is segmented by Product, by Technology, and by

Region.

The Smart Televisions

product segment is anticipated to command the largest market share in 2025

The Product segment is categorised into Smart

Televisions, Soundbars, Home Theater Systems, Gaming Consoles, Streaming

Devices, and Blu-ray Players. The dominance of the Smart Televisions segment is

attributed to its central role as the primary display and control hub for all

home entertainment. Modern smart TVs are no longer just for watching

broadcast TV; they are the gateway to streaming services, gaming consoles, and

online content. Continuous innovation in display technologies (OLED, QLED),

resolutions (4K, 8K), and smart platforms (webOS, Tizen, Android TV) drives

frequent replacement cycles. Their all-in-one functionality, integrating apps,

voice assistants, and connectivity, makes them the most essential and

high-value purchase in the home entertainment ecosystem, solidifying their

position as the product with the largest market share.

The 4K/UHD technology segment is projected to

grow at a significant CAGR.

The Technology segment includes 4K/UHD, 8K, HDR,

OLED, QLED, and Dolby Atmos. The 4K/UHD segment's projected significant growth

is driven by its transition from a premium feature to a market standard. As the

cost of 4K panels continues to decrease, it is becoming the default resolution

for mid-range and even entry-level televisions, driving mass adoption. The

widespread availability of 4K content from streaming services, gaming consoles,

and Ultra HD Blu-ray provides a compelling reason for consumers to upgrade.

Furthermore, 4K serves as the foundational technology that enhances the value

of complementary features like HDR, creating a superior overall viewing

experience. Its widespread cultivation by manufacturers and suitability for a

broad range of price points underpin this segment's robust expansion.

The Gaming Consoles product segment is projected

to witness the highest growth rate.

The Product segment is divided into Smart

Televisions, Soundbars, Home Theater Systems, Gaming Consoles, Streaming

Devices, and Blu-ray Players. The Gaming Consoles segment's position as the

fastest-growing channel is a direct result of the escalating global popularity

of video gaming as a mainstream form of entertainment. The launch of powerful

next-generation consoles (e.g., PlayStation 5, Xbox Series X/S) has catalyzed a

major upgrade cycle. These devices are not just for gaming; they are

comprehensive entertainment hubs for streaming, music, and social interaction.

The growth of cloud gaming services and subscription models (Xbox Game Pass,

PlayStation Plus) is making gaming more accessible, thereby increasing the

addressable market for consoles. The high-performance requirements of these

consoles also spur complementary sales of high-refresh-rate 4K/120 Hz

TVs and immersive audio equipment, amplifying their impact on the entire

market.

The following segments are part of an in-depth analysis of

the global Home Entertainment Devices Market:

|

Market

Segments |

|

|

By Product |

●

Smart Televisions ●

Soundbars ●

Home Theater Systems ●

Gaming Consoles ●

Streaming Devices ●

Blu-ray Players |

|

By Technology |

●

4K/UHD ●

8K ●

HDR ●

OLED ●

QLED ●

Dolby Atmos ●

Others |

Home Entertainment

Devices Market Share Analysis by Region

The Asia-Pacific

region is anticipated to hold the largest portion of the Home

Entertainment Devices Market globally throughout the forecast period.

Asia-Pacific's dominance is attributed to its

massive population, rapidly growing middle class, and increasing disposable

incomes. The region is a global manufacturing hub for electronic components and

finished goods, leading to competitive pricing and strong supply chains.

Countries like China, India, and South Korea have highly tech-savvy populations

with a strong appetite for the latest entertainment technologies. The

penetration of high-speed internet and the popularity of local and

international streaming services are driving demand for Smart TVs and streaming

devices. Furthermore, the vibrant gaming culture in countries like Japan, South

Korea, and China fuels significant demand for gaming consoles and peripherals.

The combination of high domestic consumption and massive production capacity

creates a formidable and self-reinforcing market ecosystem.

China alone accounts for a significant percentage

of the world's home entertainment device production and consumption. The

country benefits from a dense network of OEMs and leading brands, alongside a

vast domestic market. The presence of major tech giants and a strong e-commerce

infrastructure makes the latest devices widely accessible. The combination of

high domestic consumption driven by urbanization and a powerful export-oriented

industry focused on innovation and cost-effectiveness cements the region's

market leadership. Government support for the tech and semiconductor industries

also contributes to the region's dominance.

Home Entertainment

Devices Market Competition Landscape Analysis

The global home entertainment

devices market is highly competitive and consolidated, dominated by a few major

multinational corporations alongside several strong regional players.

Competition is intense and based on technological innovation, brand value,

picture and sound quality, design, and the integration of smart features and

ecosystems. Key strategies include heavy investment in R&D for new display

technologies, strategic partnerships with content providers, and expanding

product portfolios to include a full range of audio and accessory products. The

market also sees fierce price competition, particularly in the mid-range

segment, and a constant race to launch the next groundbreaking feature.

Global Home Entertainment

Devices Market Recent Developments News:

o

In February 2025, Samsung Electronics unveiled its next-generation

QD-OLED TV lineup with significantly improved brightness and a new AI-powered

processor for real-time content optimization.

o

In December 2024, Sony Group Corporation announced a strategic

partnership with a major gaming studio to bundle exclusive content with its

PlayStation 5 consoles, aiming to boost hardware sales.

o

In October 2024, LG Electronics launched a new series of OLED evo

TVs with wireless video and audio transmission, reducing cable clutter and

enhancing the minimalist design appeal.

o

In August 2024, Sonos, Inc. introduced its first Dolby

Atmos-enabled soundbar with a dedicated voice control assistant, further

bridging the gap between audio hardware and smart home functionality.

The Global Home Entertainment Devices Market Is Dominated by

a Few Large Companies, such as

●

Samsung Electronics

●

Sony Group Corporation

●

LG Electronics

●

TCL Technology

●

Hisense

●

Vizio Inc.

●

Sonos, Inc.

●

Bose Corporation

●

Microsoft (Xbox)

●

Nintendo

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Home Entertainment

Devices Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Home Entertainment Devices Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Home Entertainment

Devices Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Home

Entertainment Devices Market

1.3.2.Technology of Global Home

Entertainment Devices Market

1.3.3.Region of Global Home

Entertainment Devices Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Home Entertainment Devices Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Home Entertainment Devices Market

Estimates & Forecast Trend Analysis, by Product

4.1.

Global

Home Entertainment Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Smart Televisions

4.1.2.Soundbars

4.1.3.Home Theater Systems

4.1.4.Gaming Consoles

4.1.5.Streaming Devices

4.1.6.Blu-ray Players

5. Global

Home Entertainment Devices Market

Estimates & Forecast Trend Analysis, by Technology

5.1.

Global

Home Entertainment Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Technology,

2020 - 2033

5.1.1.4K/UHD

5.1.2.8K

5.1.3.HDR

5.1.4.OLED

5.1.5.QLED

5.1.6.Dolby Atmos

5.1.7.Others

6. Global

Home Entertainment Devices Market

Estimates & Forecast Trend Analysis, by region

6.1.

Global

Home Entertainment Devices Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Home

Entertainment Devices Market: Estimates

& Forecast Trend Analysis

7.1. North America Home

Entertainment Devices Market Assessments & Key Findings

7.1.1.North America Home

Entertainment Devices Market Introduction

7.1.2.North America Home

Entertainment Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1.

By Product

7.1.2.2.

By Technology

7.1.2.3. By Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Home

Entertainment Devices Market: Estimates

& Forecast Trend Analysis

8.1. Europe Home Entertainment

Devices Market Assessments & Key Findings

8.1.1.Europe Home Entertainment

Devices Market Introduction

8.1.2.Europe Home Entertainment

Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product

8.1.2.2.

By Technology

8.1.2.3. By Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Home

Entertainment Devices Market: Estimates

& Forecast Trend Analysis

9.1. Asia Pacific Market

Assessments & Key Findings

9.1.1.Asia Pacific Home

Entertainment Devices Market Introduction

9.1.2.Asia Pacific Home

Entertainment Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product

9.1.2.2.

By Technology

9.1.2.3. By Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Home

Entertainment Devices Market: Estimates

& Forecast Trend Analysis

10.1. Middle East & Africa

Market Assessments & Key Findings

10.1.1. Middle

East & Africa

Home Entertainment Devices Market Introduction

10.1.2. Middle

East & Africa

Home Entertainment Devices Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Product

10.1.2.2.

By Technology

10.1.2.3. By Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Home Entertainment Devices Market:

Estimates & Forecast Trend Analysis

11.1. Latin America Market

Assessments & Key Findings

11.1.1. Latin America Home

Entertainment Devices Market Introduction

11.1.2. Latin America Home

Entertainment Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product

11.1.2.2.

By Technology

11.1.2.3. By Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12.

Country

Wise Market: Introduction

13.

Competition

Landscape

13.1. Global Home Entertainment

Devices Market Product Mapping

13.2. Global Home Entertainment

Devices Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

13.3. Global Home Entertainment

Devices Market Tier Structure Analysis

13.4. Global Home Entertainment

Devices Market Concentration & Company Market Shares (%) Analysis, 2024

14.

Company

Profiles

14.1.

Samsung Electronics

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

PerProductance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2.

Sony Group Corporation

14.3.

LG Electronics

14.4.

TCL Technology

14.5.

Hisense

14.6.

Vizio Inc.

14.7.

Sonos, Inc.

14.8.

Bose Corporation

14.9.

Microsoft (Xbox)

14.10.

Nintendo

14.11.

Other Prominent Players

15. Research

Methodology

15.1. External Transportations /

Databases

15.2. Internal Proprietary

Database

15.3. Primary Research

15.4. Secondary Research

15.5. Assumptions

15.6. Limitations

15.7. Report FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables