Home Security Solutions Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Security Cameras, Alarm Systems, Smart Locks, Sensors & Detectors, and Professional Monitoring Services), By System (Professionally Installed & Monitored, Do-It-Yourself (DIY), and Self-Monitored), By Sales Channel (Retail, Online, and Direct-to-Consumer) And Geography

2025-12-02

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Home Security Solutions Market Overview

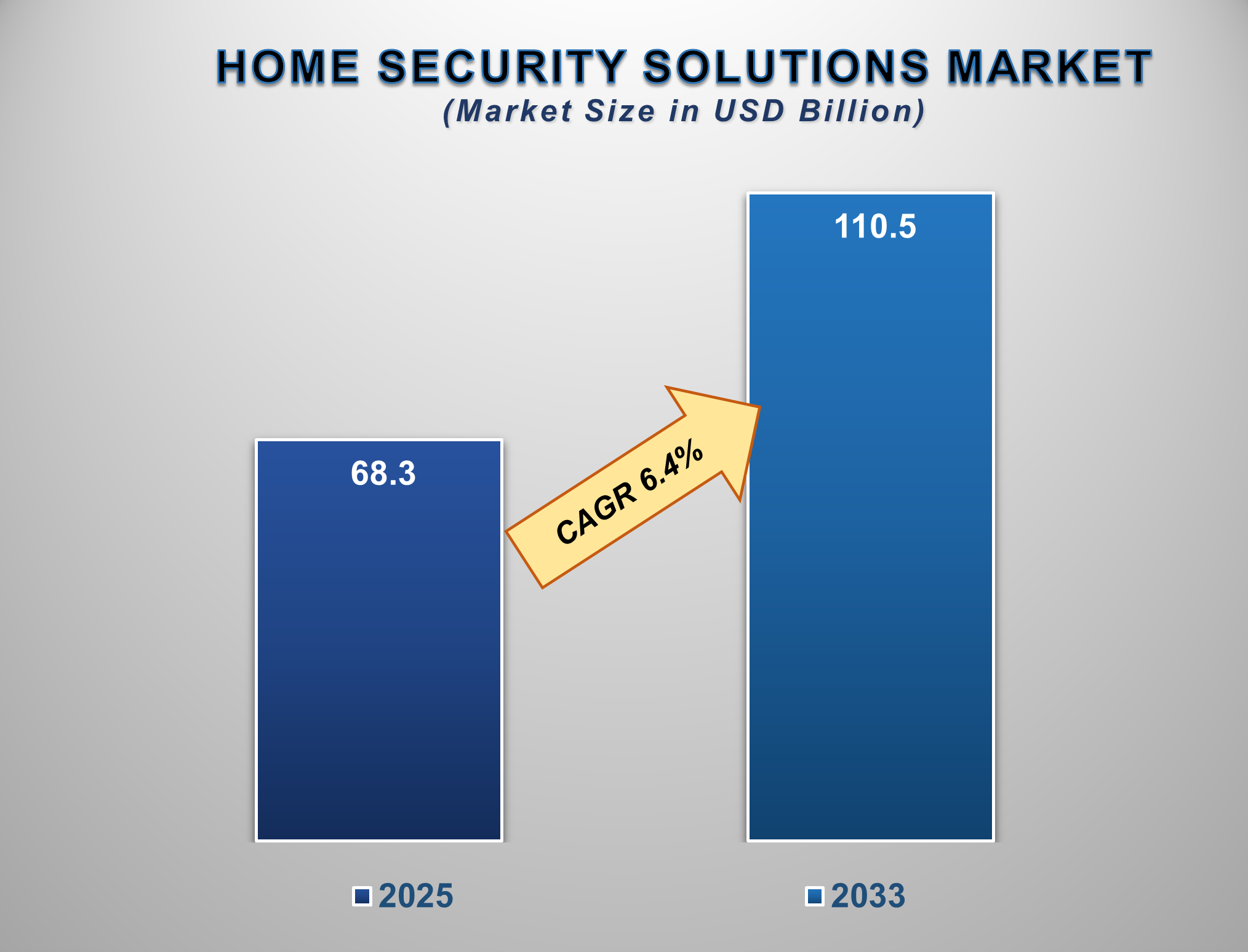

The Home Security Solutions Market is positioned for a period of dynamic and sustained growth from 2025 to 2033, fueled by rising consumer awareness regarding safety, technological advancements in smart home devices, increasing urbanization, and the growing prevalence of affordable DIY solutions. The market is projected to be valued at approximately USD 68.3 billion in 2025 and is forecasted to reach nearly USD 110.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.4% during this period.

Home security solutions encompass a wide range

of products and services designed to protect residences from burglary, fire,

and other emergencies. This includes hardware such as security cameras, alarm

systems, and smart locks, as well as software platforms and professional

monitoring services that provide real-time alerts and emergency response. The

market's robust expansion is primarily driven by the global integration of

Internet of Things (IoT) technology into residential spaces, which has made

sophisticated security systems more accessible and user-friendly.

Furthermore, rising crime rates in certain urban

areas, coupled with the increasing consumer desire for remote home monitoring

and control via smartphones, are significant contributors to market growth. The

proliferation of subscription-based models and the decreasing cost of sensors

and cloud storage are also making comprehensive home security more affordable.

North America currently holds the largest market share due to high consumer

spending and early technology adoption, while the Asia-Pacific region is

expected to witness the fastest growth, driven by its rapidly expanding middle

class and increasing smart city initiatives.

Home Security

Solutions Market Drivers and Opportunities

The Proliferation of Smart Home Ecosystems

and IoT Integration is the Primary Market Driver

The relentless expansion of the smart home

ecosystem is the most powerful force propelling the home security solutions

market. The convenience, control, and connectivity offered by IoT devices have

transformed home security from a standalone alarm system into an integrated

network of intelligent devices. Consumers can now monitor live video feeds,

lock and unlock doors, receive motion alerts, and control environmental sensors

remotely from their smartphones. This seamless integration is a key purchasing

driver, as security becomes a core component of the automated home. The ability

of these systems to learn user behavior and provide customized alerts enhances

their perceived value. Compatibility with popular voice assistants like Amazon

Alexa and Google Assistant further drives adoption by placing security control

at the center of the smart home experience. The sheer variety and

interoperability of connected devices are creating a robust ecosystem where

security is no longer an isolated function but an integral part of modern

living.

The global smart home market continues its rapid

ascent, fundamentally reshaping residential living and consumer expectations.

In 2024, the number of connected smart homes worldwide is estimated to exceed

400 million, with a penetration rate of over 25% in key markets like North

America and Western Europe. This figure is projected to grow to over 600

million homes by 2027. This growth is underpinned by advancements in wireless

communication protocols (like Wi-Fi, Bluetooth, and Zigbee), the falling cost

of hardware, and increased consumer familiarity with smart technology. The

Asia-Pacific region is becoming a major growth engine, with countries like

China and South Korea leading in adoption rates. This data underscores the

immense scale of the connected home landscape and highlights the central role

that security and safety products play within it, often serving as the initial

entry point for consumers into the broader smart home ecosystem.

Rising Urbanization and Crime Awareness are Driving Strategic Adoption

The global trend of urbanization and heightened

awareness of property crime is a powerful catalyst for the home security

solutions market. As populations increasingly concentrate in cities, concerns

about burglary and property theft often rise, driving demand for protective

measures. Widespread access to information through social media and local news

apps keeps residents informed about incidents in their neighborhoods, further

amplifying security concerns. This environment pushes homeowners and renters

alike to invest in systems that offer peace of mind. Furthermore, the

availability of renter-friendly DIY solutions has unlocked a massive market

segment previously hesitant to install hardwired systems. The demand is no

longer just about deterring break-ins; it extends to comprehensive safety,

including fire, carbon monoxide, and water leak detection, making a holistic

security system a standard consideration for modern urban living.

The Emergence of AI-Powered Features and the

Expansion of DIY Models Present Significant Opportunities

The strategic integration of artificial

intelligence and the booming DIY segment is

creating significant growth frontiers for the home security market. Key

opportunities lie in the application of advanced AI and machine learning to

enhance system intelligence and usability. AI-powered cameras can now

distinguish between people, pets, and vehicles, drastically reducing false

alarms and providing more relevant notifications. Advanced analytics can

identify unusual patterns of activity, offering proactive security.

Furthermore, the burgeoning DIY market represents a massive opportunity for

growth, as it appeals to cost-conscious consumers and renters who seek

flexibility and avoid long-term contracts. For security providers, investing in

developing more sophisticated AI algorithms, creating scalable and

user-friendly DIY platforms, and offering flexible monitoring plans are key

strategies to capture new customer segments and drive recurring revenue,

turning hardware sales into long-term service relationships.

Home Security Solutions

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 68.3 Billion |

|

Market Forecast in 2033 |

USD 110.5 Billion |

|

CAGR % 2025-2033 |

6.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product ●

By System ●

By Sales Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Home Security Solutions

Market Report Segmentation Analysis

The global Home Security

Solutions Market industry analysis is segmented by Product, by System, by Sales

Channel, and by region.

The Security Cameras Product segment is

anticipated to command a significant market share in 2025

The Product segment is categorised into Security

Cameras, Alarm Systems, Smart Locks, Sensors & Detectors, and Professional

Monitoring Services. The security cameras segment holds a substantial and

dominant share of the market due to their visual verification capabilities and

high consumer demand. Modern security cameras offer features such as

high-definition live streaming, night vision, two-way audio, and person

detection, making them one of the most visible and valued components of a home

security system.

Their utility extends beyond crime deterrence to include monitoring children, pets, and package deliveries. The ease of installation of wireless and battery-powered models, combined with the availability of low-cost cloud storage plans, has made them an accessible first purchase for many consumers. The continuous innovation in camera technology, including 4K resolution, solar power, and advanced AI analytics, ensures this segment remains a primary revenue driver and a cornerstone of the modern home security setup.

The Do-It-Yourself (DIY) System segment is

projected to grow at a significant CAGR.

The System segment includes Professionally

Installed & Monitored, Do-It-Yourself (DIY), and Self-Monitored. The DIY

system segment's projected significant growth is directly linked to its appeal

to cost-effectiveness, flexibility, and ease of installation. DIY systems

eliminate the need for scheduled appointments, professional installation fees,

and often, long-term contracts, which are common pain points of traditional

professionally installed systems.

They are designed for user-friendly self-setup,

typically using wireless components that can be configured via a smartphone app

in minutes. This model is particularly attractive to renters, tech-savvy

millennials, and budget-conscious homeowners who want control over their system

without a significant upfront investment. The ability to customize a system piece by piece and the availability of scalable monitoring options are powerful forces

propelling the DIY segment to become the fastest-growing system type in the

market.

The Online Sales Channel segment is projected to

witness the highest growth rate.

The Sales Channel segment is divided into Retail,

Online, and Direct-to-Consumer. The Online segment's position as the

fastest-growing channel is a direct consequence of shifting consumer purchasing

habits and the nature of the products. Consumers heavily rely on online

reviews, comparison tools, and detailed product specifications before making a

purchase decision for home security devices.

E-commerce platforms offer a wider selection,

competitive pricing, and the convenience of direct-to-doorstep delivery, which

is ideal for DIY products. Furthermore, many new, digitally-native brands

operate primarily or exclusively through online channels, using content

marketing and social media to reach their audience. The ability to easily

purchase individual components, sensors, or entire kits online, often with

direct access to customer support and subscription management, makes the online

channel the most dynamic and rapidly expanding sales avenue in the industry.

The following segments are part of an in-depth analysis of

the global Home Security Solutions Market:

|

Market

Segments |

|

|

By Product |

●

Security Cameras ●

Alarm Systems ●

Smart Locks ●

Sensors &

Detectors ●

Professional

Monitoring Services |

|

By System |

●

Professionally

Installed & Monitored ●

Do-It-Yourself (DIY) ●

Self-Monitored |

|

By Sales Channel |

●

Retail ●

Online ●

Direct-to-Consumer |

Home Security Solutions

Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Home Security Solutions

Market globally throughout the forecast period.

North America's dominance is attributed to its

high disposable income, strong technological infrastructure, and a deeply

ingrained culture of home ownership and security. The region has a mature

market with high awareness and penetration rates for both professional and DIY

security systems. The presence of major global players and tech giants, coupled

with a high adoption rate of smart home technologies, creates a sustained

demand for advanced and integrated security solutions. Furthermore, the

availability of reliable and high-speed internet across most of the region is a

critical enabler for connected security devices and cloud-based monitoring

services, solidifying North America's leading position.

The United States, in particular, is the world's

largest single market for home security solutions. The country's competitive

landscape, featuring a mix of traditional security companies, telecom

providers, and new tech entrants, drives continuous innovation and aggressive

marketing. High rates of suburban home ownership, coupled with a strong DIY

culture, fuel demand across both professional and self-installed segments. The

well-developed ecosystem of smart home devices and the consumer expectation for

seamless integration ensure a continuous cycle of upgrades and new product

adoption, maintaining the U.S. at the forefront of the global market.

Home Security Solutions

Market Competition Landscape Analysis

The global home security

solutions market is highly competitive and fragmented, featuring a diverse mix

of established security giants, telecommunications companies, specialized DIY

brands, and technology conglomerates. Competition is intensifying and centers

on product features, system reliability, brand trust, the user experience of

mobile apps, and the cost of monitoring services. Key strategies include

continuous investment in R&D for AI and new sensor technologies, strategic

partnerships with homebuilders and insurance companies, and the bundling of

security with other smart home services or internet/TV packages. The market

also sees fierce competition from tech startups offering innovative,

app-centric security solutions and low-cost monitoring alternatives.

Global Home Security

Solutions Market Recent Developments News:

- In February 2025, Google Nest announced a new

generation of its flagship indoor camera with enhanced radar-based sensing

for more accurate person and pet alerts, reducing false notifications.

- In December 2024, SimpliSafe, a leading DIY

security provider, partnered with a major national insurance company to

offer premium discounts to policyholders who install their system, driving

subscriber growth.

- In August 2024, Amazon announced that its Ring

Alarm system had surpassed 2 million active monitoring subscriptions,

highlighting the massive scale achievable through its e-commerce and

ecosystem integration.

- In October 2024, ADT Inc. launched a new integrated smart home panel

with built-in voice assistant capabilities, aiming to create a more

centralized and intuitive user experience for its customers.

The Global Home Security Solutions Market Is Dominated by a

Few Large Companies, such as

●

ADT Inc.

●

SimpliSafe, Inc.

●

Google LLC (Nest)

●

Amazon.com, Inc.

(Ring, Blink)

●

Johnson Controls

International plc (Tyco)

●

Resideo Technologies,

Inc.

●

Allegion plc

●

ASSA ABLOY

●

Comcast Corporation

(Xfinity Home)

●

Vivint Smart Home,

Inc.

●

Arlo Technologies,

Inc.

●

Axis Communications AB

●

Bosch

Sicherheitssysteme GmbH

●

Frontpoint Security

Solutions, LLC

●

Abode Systems, Inc.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Home Security

Solutions Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Home Security Solutions Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Home Security

Solutions Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Home

Security Solutions Market

1.3.2.System of Global Home

Security Solutions Market

1.3.3.Sales Channel of Global Home

Security Solutions Market

1.3.4.Region of Global Home

Security Solutions Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

3. Global

Home Security Solutions Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Home Security Solutions Market Estimates

& Forecast Trend Analysis, by Product

4.1.

Global

Home Security Solutions Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Security Cameras

4.1.2.Alarm Systems

4.1.3.Smart Locks

4.1.4.Sensors & Detectors

4.1.5.Professional Monitoring

Services

5. Global

Home Security Solutions Market Estimates

& Forecast Trend Analysis, by System

5.1.

Global

Home Security Solutions Market Revenue (US$ Bn) Estimates and Forecasts, by System,

2020 - 2033

5.1.1.Professionally Installed

& Monitored

5.1.2.Do-It-Yourself (DIY)

5.1.3.Self-Monitored

6. Global

Home Security Solutions Market Estimates

& Forecast Trend Analysis, by Sales Channel

6.1.

Global

Home Security Solutions Market Revenue (US$ Bn) Estimates and Forecasts, by Sales

Channel 2020 - 2033

6.1.1.Retail

6.1.2.Online

6.1.3.Direct-to-Consumer

7. Global

Home Security Solutions Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Home Security Solutions Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Home

Security Solutions Market: Estimates

& Forecast Trend Analysis

8.1. North America Home

Security Solutions Market Assessments & Key Findings

8.1.1.North America Home

Security Solutions Market Introduction

8.1.2.North America Home

Security Solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product

8.1.2.2.

By System

8.1.2.3.

By Sales Channel

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Home

Security Solutions Market: Estimates

& Forecast Trend Analysis

9.1. Europe Home Security

Solutions Market Assessments & Key Findings

9.1.1.Europe Home Security

Solutions Market Introduction

9.1.2.Europe Home Security

Solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product

9.1.2.2.

By System

9.1.2.3.

By Sales Channel

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Home

Security Solutions Market: Estimates

& Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Home Security Solutions Market Introduction

10.1.2.

Asia

Pacific Home Security Solutions Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1.

By Product

10.1.2.2.

By System

10.1.2.3.

By Sales Channel

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Home

Security Solutions Market: Estimates

& Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Home Security Solutions Market Introduction

11.1.2. Middle

East & Africa

Home Security Solutions Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1.

By Product

11.1.2.2.

By System

11.1.2.3.

By Sales Channel

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Home Security Solutions Market:

Estimates & Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Home

Security Solutions Market Introduction

12.1.2. Latin America Home

Security Solutions Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product

12.1.2.2.

By System

12.1.2.3.

By Sales Channel

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Home Security

Solutions Market Product Mapping

14.2. Global Home Security

Solutions Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

14.3. Global Home Security

Solutions Market Tier Structure Analysis

14.4. Global Home Security

Solutions Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

ADT Inc.

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

SimpliSafe, Inc.

15.3.

Google LLC (Nest)

15.4.

Amazon.com, Inc. (Ring, Blink)

15.5.

Johnson Controls International plc (Tyco)

15.6.

Resideo Technologies, Inc.

15.7.

Allegion plc

15.8.

ASSA ABLOY

15.9.

Comcast Corporation (Xfinity Home)

15.10.

Vivint Smart Home, Inc.

15.11.

Arlo Technologies, Inc.

15.12.

Axis Communications AB

15.13.

Bosch Sicherheitssysteme GmbH

15.14.

Frontpoint Security Solutions, LLC

15.15.

Abode Systems, Inc.

15.16.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables