Hospital Acquired Infections Diagnostics Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (Instruments, Mass spectrometers, Reagents and Consumables and Software & Services); By Infection Type (Bloodstream Infections (BSIs), Urinary Tract Infections (UTIs), Surgical Site Infections (SSIs), Ventilator-Associated Pneumonia, Gastrointestinal Infections and Other HAIs); By End-user (Hospitals & Clinics, Diagnostic Centres, Ambulatory Surgical Centres (ASCs) Others) and Geography

2025-07-16

Healthcare

Swetal (Research Analyst)

Description

Hospital Acquired Infections Diagnostics Market

Overview

The Hospital Acquired Infections

Diagnostics Market is projected to witness significant growth between 2025 and

2035, driven by number of surgical operations performed annually has been

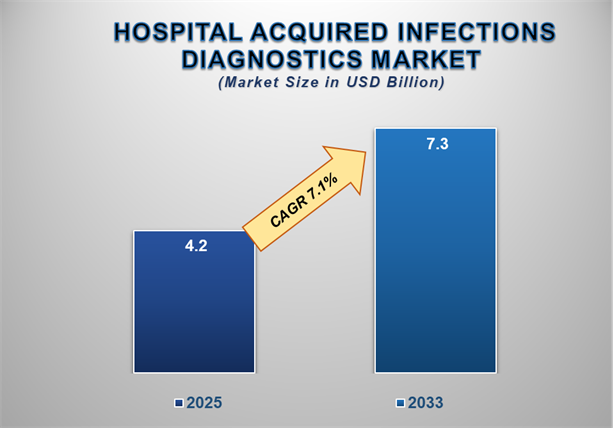

rising gradually all over the world. Valued at approximately USD 4.2 billion in

2025, the market is expected to soar to USD 7.3 billion by 2035, reflecting a

strong compound annual growth rate (CAGR) of 7.1% over the ten-year period.

Hospital Acquired Infections, also

referred to as nosocomial infections, are infections acquired by patients

during treatment in a healthcare center, e.g., a hospital, that were neither

present upon, nor incubating at, admission. They usually appear 48 hours or

more following admission but may also appear after discharge. They are a

serious threat to health, extend hospitalization time, drive up healthcare

expenditure, and are a factor in increased morbidity and mortality rates.

Common categories of HAI include

bloodstream infections (BSI), urinary tract infection (UTI), surgical site

infection (SSI), pneumonia, particularly ventilator-associated, and

gastrointestinal infections like Clostridioides difficile infection. HAI infections

are frequently a result of antibiotic-resistant bacteria, such as

Staphylococcus aureus (MRSA), Pseudomonas aeruginosa, Escherichia coli, and

Klebsiella pneumoniae.

Diagnosis of HAIs occurs through a

mixture of clinical evaluation and laboratory testing. Molecular tests, such as

PCR and NAATs, are used extensively because of high sensitivity coupled with

quick results. Conventional microbiology tests like culture tests continue to

find utility in determining susceptibility to antibiotics as well as

identifying pathogens. Immunoassay and serology tests identify infections by

focusing specifically on antigens or antibodies. Techniques such as mass

spectrometry and next-generation sequencing are being adopted more frequently

in advanced environments to conduct an overall profiling of pathogens. Early,

precise diagnosis of HAIs is instrumental in starting targeted therapy,

preventing outbreaks, and curbing transmission in a healthcare facility

setting. Anti-microbial stewardship, surveillance, and regular screening are

vital to controlling HAIs effectively.

Hospital Acquired Infections Diagnostics Market

Drivers and Opportunities

Rising prevalence of

antibiotic-resistant pathogens driving the Hospital Acquired Infections

Diagnostics Market during the forecast period

One of the key drivers of Hospital

Acquired Infections (HAIs) diagnostics market growth is the increased incidence

of antibiotic-resistant infections. Misuse and overprescription of antibiotics

have contributed to the development of multidrug-resistant organisms (MDROs),

which are more difficult to treat and need more sophisticated diagnostic

equipment to identify early on. Healthcare settings are also under immense

pressure to identify these infections promptly to contain their spread and

choose optimal treatment methods. Such has boosted demand for fast, precise

diagnostic technology in the form of molecular diagnostics and point-of-care

technology products, capable of identifying resistance genes and pathogens with

enhanced sensitivity. Regulatory agencies, along with international health

agencies, are actively encouraging infection surveillance programs, further

fueling market growth.

growing awareness and

emphasis on patient safety and infection control in healthcare settings drives

global Hospital Acquired Infections Diagnostics Market

Another key driving force is increased

awareness and focus on infection control and patient safety in healthcare

environments. Governments, together with healthcare agencies, have implemented

rigorous guidelines, as well as reimbursement schemes, that encourage hospitals

to lower infection levels. The monetary penalties linked to high HAI rates in

most healthcare systems, particularly in developed nations, are driving

hospitals to invest in enhanced diagnosis infrastructure. Diagnostic testing is

increasingly being adopted as a part of day-to-day hospital practice, from

admission through to follow-up, driving increased uptake of enhanced HAI

diagnostic equipment across healthcare centres of all types.

Opportunity for the Hospital Acquired Infections

Diagnostics Market

Adoption of advanced

technologies in emerging economies is significant opportunities in the global Hospital

Acquired Infections Diagnostics Market

One of the prime opportunities in the

HAIs diagnosis marketplace exists in the uptake of newer technologies across

emerging economies. Asia-Pacific, Latin America, and parts of Middle East and

Africa are experiencing healthcare infrastructure improvements, coupled with

increasing healthcare spends and infection control practice awareness, creating

untapped potential in these geographies to be seized by diagnostic companies

through offering affordable, scalable diagnostic solutions. Access to more

skilled healthcare professionals, as well as enhanced lab capabilities, also

supports incorporating molecular diagnostics, as well as automated testing

platforms, into these geographies. Additionally, public-private partnerships

and global health projects are financially supporting HAI prevention and

control programs, which are frequently accompanied by diagnosis tools and

equipment. Diagnostic companies that are able to adjust products to fit

budgets, as well as regulatory environments, of these opening-up markets—while

providing fast, reliable diagnoses—have a competitive edge in these

geographies. By making solutions more affordable, as well as accessible,

diagnostic companies can dramatically increase their addressable markets, as

well as help drive better patient outcomes across regions where historically

infection rates have been high, as well as infection control budgets are low.

Hospital Acquired Infections Diagnostics Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.2 Billion |

|

Market Forecast in

2035 |

USD

7.3 Billion |

|

CAGR % 2025-2035 |

7.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption, company

share, company heatmap, company production Capacity, growth factors and more |

|

Segments Covered |

·

By

Product Type ·

By

Infection Type ·

By

Technology ·

By

End-user |

|

Regional Scope |

·

North America ·

Western Europe ·

Eastern Europe ·

Asia Pacific ·

Latin America ·

Middle East and Africa |

|

Country Scope |

1) U.S. 2) Canada 3) U.K. 4) Germany 5) France 6) Italy 7) Spain 8) Benelux 9) Nordic Countries 10)

Russia

11)

China

12)

India

13)

Japan 14)

South

Korea 15)

Australia

16)

Indonesia

17)

Thailand

18)

Mexico

19)

Brazil

20)

Argentina

21)

Saudi

Arabia 22)

UAE

23)

Egypt

24)

South

Africa 25)

Nigeria |

Hospital Acquired Infections Diagnostics Market Report

Segmentation Analysis

The reagents and

consumables product type segment is anticipated to hold the highest share of

the global hospital acquired infections diagnostics market during the projected

timeframe.

The reagent and consumables segment is

anticipated to command the highest share of the Hospital Acquired Infections

(HAIs) diagnostics market throughout the forecast period, owing to its

recurring as well as essential nature in diagnostic testing. Such products

consist of test kits, detection reagents, culture media, and other disposable

products used across most diagnostic platforms, especially in molecular as well

as immunoassay-based tests. As against diagnostic equipment, where reagent

replenishment involves periodic replacement, reagent and consumable products

are employed in each diagnostic analysis, resulting in steady demand. As

healthcare professionals move towards high-throughput as well as automated

diagnosis platforms, utilization of standardized reagents of higher quality

also becomes essential to improve accuracy as well as efficiency. Rising

awareness about infection prevention, increased rates of multidrug-resistant

infections, as well as more common routine screening in hospitals, also help drive

this segment. In turn, companies are focusing on developing sophisticated

reagents, allowing faster turn-around, along with greater sensitivity,

especially in point-of-care, as well as in molecular diagnosis.

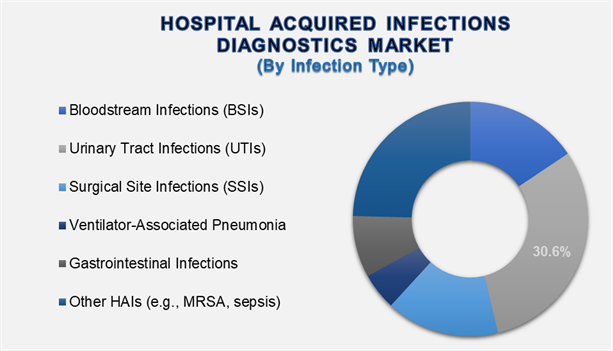

The Urinary Tract

Infections (UTIs) type segment dominated the market in 2024 and is predicted to

grow at the highest CAGR over the forecast period.

The Urinary

Tract Infections (UTIs) segment led the Hospital Acquired Infections

diagnostics segment in 2024 and has been anticipated to register the highest

Compound Annual Growth Rate (CAGR) through the forecast period. UTIs are among

the most prevalent hospital-acquired infections, especially in patients with

indwelling catheters, urological procedure recipients, and individuals with

compromised immunity. The infections are found in multiple healthcare settings

owing to factors such as excessive hospitalization, unhygienic catheter

management, and compliance failures in hygiene practices. The rise in

catheter-associated urinary tract infections (CAUTIs) has increased pressure to

implement early detection and intervention, propelling the need for quickening

diagnostic tools without compromising accuracy. The growth of the segment also

derives traction from advances in diagnostic methods, such as molecular tests

that can identify targeted germs and antibiotic resistance in a urine specimen

in a quick turnaround time. Additionally, regulatory requirements and hospital

accreditation standards now emphasize monitoring and reporting UTI, compelling

hospitals to invest in enhanced diagnostic tools.

Molecular Diagnostics

Technology Segment hold significant share for HAI Diagnostics Market

The share of

the Hospital Acquired Infections (HAIs) diagnostic market by the molecular

diagnostic sector is significant owing to its accuracy, speed, and increased

usage in clinical practices. Molecular methods, i.e., PCR, NAATs, and next

generation sequencing (NGS), enable immediate identification of pathogens along

with resistance genes straight from clinical specimens. In contrast to culture

methods, where results are received after days, molecular diagnosis provides

results in hours, facilitating targeted therapeutic decisions at appropriate

time.

It is

especially important in hospital settings where timely interventions can avert

infection transmission and enhance patient prognosis. Additionally, the

emergence of drug resistance has put more emphasis on diagnostic tools that can

not only detect infection but also detect resistance genetic markers.

Technological innovation has also contributed to an array of user-friendly,

point-of-care molecular platforms that are finding applications both in central

labs, as well as at the bedside.

The Hospitals &

Clinics segments dominated the Hospital Acquired Infections Diagnostics Market

The hospital

and clinics segment led the Hospital Acquired Infections diagnostics market and

is anticipated to continue its leadership position owing to its high patient

flow and enhanced infection transmission risks in these environments. ICUs, in

particular, are top spots where HAIs are common, owing to increased utilization

of invasive devices such as catheters, ventilators, and central lines. Early

diagnosis, along with its accuracy, plays a pivotal role in controlling

infection in such high-risk environments, hence fueling demand from diagnostic

tests.

Clinics also

make a substantial contribution to this sector, especially those that conduct

minor surgical interventions or have patients that are immunocompromised.

Regulation to ensure infection control, as well as surveillance, has also

driven hospitals and clinics to incorporate diagnostic testing into everyday

practice. Such establishments routinely have on-site laboratories or access to

diagnostic laboratories, allowing regular utilization of complex testing

platforms, encompassing molecular diagnosis, immunoassay, and culture methods.

The

following segments are part of an in-depth analysis of the global hospital

acquired infections diagnostics market:

|

Market

Segments |

|

|

By Product Type |

·

Instruments o PCR (Polymerase Chain Reaction) instruments o Microarrays o Immunoassay analysers ·

Mass spectrometers ·

Reagents and Consumables ·

Software & Services |

|

By Infection Type |

·

Bloodstream Infections (BSIs) ·

Urinary Tract Infections (UTIs) ·

Surgical Site Infections (SSIs) ·

Ventilator-Associated Pneumonia ·

Gastrointestinal Infections ·

Other HAIs (e.g., MRSA, sepsis) |

|

By Technology |

·

Molecular Diagnostics ·

Immunoassays ·

Mass Spectrometry ·

Microbiology Culture Tests ·

Other Traditional Diagnostic

Techniques |

|

By End-user |

·

Hospitals & Clinics ·

Diagnostic Laboratories ·

Ambulatory Surgical Centers ·

Long-Term Care Facilities ·

Others |

Hospital Acquired Infections Diagnostics Market

Share Analysis by Region

North America is

projected to hold the largest share of the global Hospital Acquired Infections

Diagnostics Market over the forecast period.

North America has been expected to

account for the largest share of the worldwide Hospital Acquired Infections

Diagnostics Market because of its highly developed healthcare infrastructure,

infection control awareness, and prevalent usage of advanced diagnostic

technology. There is a high incidence of hospital-acquired infections,

especially in the United States, resulting in stringent regulatory requirements

and national infection surveillance programs.

Government bodies like Centers for

Disease Control and Prevention (CDC) and Centers for Medicare & Medicaid

Services (CMS) encourage infection surveillance as well as reporting actively,

further enhancing the utilization of diagnostic products. There is also strong

healthcare expenditure along with a well-equipped diagnostics sector in North

America, coupled with prominent players in the industry. Demand for fast,

precise molecular diagnostic assays also increases, given the issue of

antibiotic resistance across regions. All these factors combine to make North

America the leading region in the HAIs diagnostics market, where growth would

be steady.

Hospital Acquired Infections Diagnostics Market Competition

Landscape Analysis

The market

is competitive, with several established players and new entrants Product Type

a range of hospital acquired infection diagnostic products. Some of the key

players Becton, Dickinson and Company (BD), bioMérieux SA, F. Hoffmann-La Roche

Ltd, Thermo Fisher Scientific Inc., Abbott Laboratories, Siemens Healthineers,

Danaher Corporation and Others

Global Hospital

Acquired Infections Diagnostics Market Recent Developments News:

o

February 2024 saw

an exclusive agreement between PathAI and Roche Tissue Diagnostics (RTD) to

design companion diagnostic-enabled AI-powered digital pathology

algorithms. The agreement has been formed to improve cancer diagnosis as well

as infectious disease diagnosis accuracy by incorporating PathAI's

sophisticated image analysis algorithms into Roche's navify® Digital Pathology

platform.

o

In July 2024, Becton, Dickinson, and Company

(BD) entered into a worldwide partnership with Quest Diagnostics to develop,

produce, and commercialize flow cytometry-based companion diagnostics (CDx).

The purpose of these diagnostics is to help choose appropriate treatments for

cancer patients and patients afflicted by other ailments.

o

HiMedia Laboratories introduced in April 2024

a portfolio of molecular solutions to detect antimicrobial resistance (AMR).

These solutions comprise state-of-the-art PCR kits as well as sequencing

services capable of detecting resistance genes across various pathogens.

The Global Hospital

Acquired Infections Diagnostics Market is dominated by a few large companies,

such as

·

Becton, Dickinson and Company (BD)

·

bioMérieux SA

·

F. Hoffmann-La Roche Ltd

·

Thermo Fisher Scientific

Inc.

·

Abbott Laboratories

·

Siemens Healthineers

·

Danaher Corporation

·

Qiagen N.V.

·

Hologic, Inc.

·

Luminex Corporation

·

Bio-Rad Laboratories,

Inc.

·

Cepheid (a Danaher

company)

·

GenMark Diagnostics (part of Roche)

·

Merck KGaA

·

T2 Biosystems, Inc.

·

Others

· Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Hospital Acquired Infections Diagnostics Market Introduction and Market Overview

- Objectives of the Study

- Global Hospital Acquired Infections Diagnostics Market Scope and Market Estimation

- Global Hospital Acquired Infections Diagnostics Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2035)

- Global Hospital Acquired Infections Diagnostics Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2035

- Market Segmentation

- Product Type of Global Hospital Acquired Infections Diagnostics Market

- Infection Type of Global Hospital Acquired Infections Diagnostics Market

- Technology of Global Hospital Acquired Infections Diagnostics Market

- End-user of Global Hospital Acquired Infections Diagnostics Market

- Region of Global Hospital Acquired Infections Diagnostics Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2035

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Hospital Acquired Infections Diagnostics Market

- Technological Advancements in Hospital Acquired Infections Diagnostics Market

- Key Product/Brand Analysis

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Technology Factors

- Key Regulation

- Global Hospital Acquired Infections Diagnostics Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Hospital Acquired Infections Diagnostics Market Estimates & Forecast Trend Analysis, by Product Type

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- Instruments

- PCR (Polymerase Chain Reaction) instruments

- Microarrays

- Immunoassay analyzers

- Mass spectrometers

- Reagents and Consumables

- Software & Services

- Instruments

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- Global Hospital Acquired Infections Diagnostics Market Estimates & Forecast Trend Analysis, by Infection Type

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Bloodstream Infections (BSIs)

- Urinary Tract Infections (UTIs)

- Surgical Site Infections (SSIs)

- Ventilator-Associated Pneumonia

- Gastrointestinal Infections

- Other HAIs (e.g., MRSA, sepsis)

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Global Hospital Acquired Infections Diagnostics Market Estimates & Forecast Trend Analysis, by Technology

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- Molecular Diagnostics

- Immunoassays

- Mass Spectrometry

- Microbiology Culture Tests

- Other Traditional Diagnostic Techniques

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- Global Hospital Acquired Infections Diagnostics Market Estimates & Forecast Trend Analysis, by End-user

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Hospitals & Clinics

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Long-Term Care Facilities

- Others

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Global Hospital Acquired Infections Diagnostics Market Estimates & Forecast Trend Analysis, by region

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2035

- North America

- Eastern Europe

- Western Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Hospital Acquired Infections Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2035

- North America Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- North America Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- North America Hospital Acquired Infections Diagnostics Market Introduction

- North America Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- The U.S.

- Canada

- Mexico

- North America Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- Western Europe Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- Western Europe Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- Western Europe Hospital Acquired Infections Diagnostics Market Introduction

- Western Europe Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Benelux

- Nordics

- Rest of W. Europe

- Western Europe Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- Eastern Europe Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- Eastern Europe Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- Eastern Europe Hospital Acquired Infections Diagnostics Market Introduction

- Eastern Europe Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- Russia

- Hungary

- Poland

- Balkan & Baltics

- Rest of E. Europe

- Eastern Europe Hospital Acquired Infections Diagnostics Market Assessments & Key Findings

- Asia Pacific Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Hospital Acquired Infections Diagnostics Market Introduction

- Asia Pacific Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- China

- Japan

- India

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Hospital Acquired Infections Diagnostics Market Introduction

- Middle East & Africa Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- UAE

- Saudi Arabia

- Turkey

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Hospital Acquired Infections Diagnostics Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Hospital Acquired Infections Diagnostics Market Introduction

- Latin America Hospital Acquired Infections Diagnostics Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Infection Type

- By Technology

- By End-user

- By Country

- Brazil

- Argentina

- Colombia

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Hospital Acquired Infections Diagnostics Market Product Mapping

- Global Hospital Acquired Infections Diagnostics Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Hospital Acquired Infections Diagnostics Market Tier Structure Analysis

- Global Hospital Acquired Infections Diagnostics Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Becton, Dickinson and Company (BD)

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Becton, Dickinson and Company (BD)

* Similar details would be provided for all the players mentioned below

- bioMérieux SA

- Hoffmann-La Roche Ltd

- Thermo Fisher Scientific Inc.

- Abbott Laboratories

- Siemens Healthineers

- Danaher Corporation

- Qiagen N.V.

- Hologic, Inc.

- Luminex Corporation

- Bio-Rad Laboratories, Inc.

- Cepheid (a Danaher company)

- GenMark Diagnostics (part of Roche)

- Merck KGaA

- T2 Biosystems, Inc.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables