Incontinence Care Products Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Adult Diapers, Protective Underwear, Disposable Pads & Liners, Male Guards, Underpads, Others), By Incontinence Type (Urinary Incontinence, Faecal Incontinence, Mixed Incontinence), By End-user (Homecare, Nursing Homes & Long-Term Care Facilities, Hospitals), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Channels, Hypermarkets/Supermarkets), and Geography

2025-12-19

Consumer Products

Jaya Bundele (Research Analyst)

Description

Incontinence

Care Products Market Overview

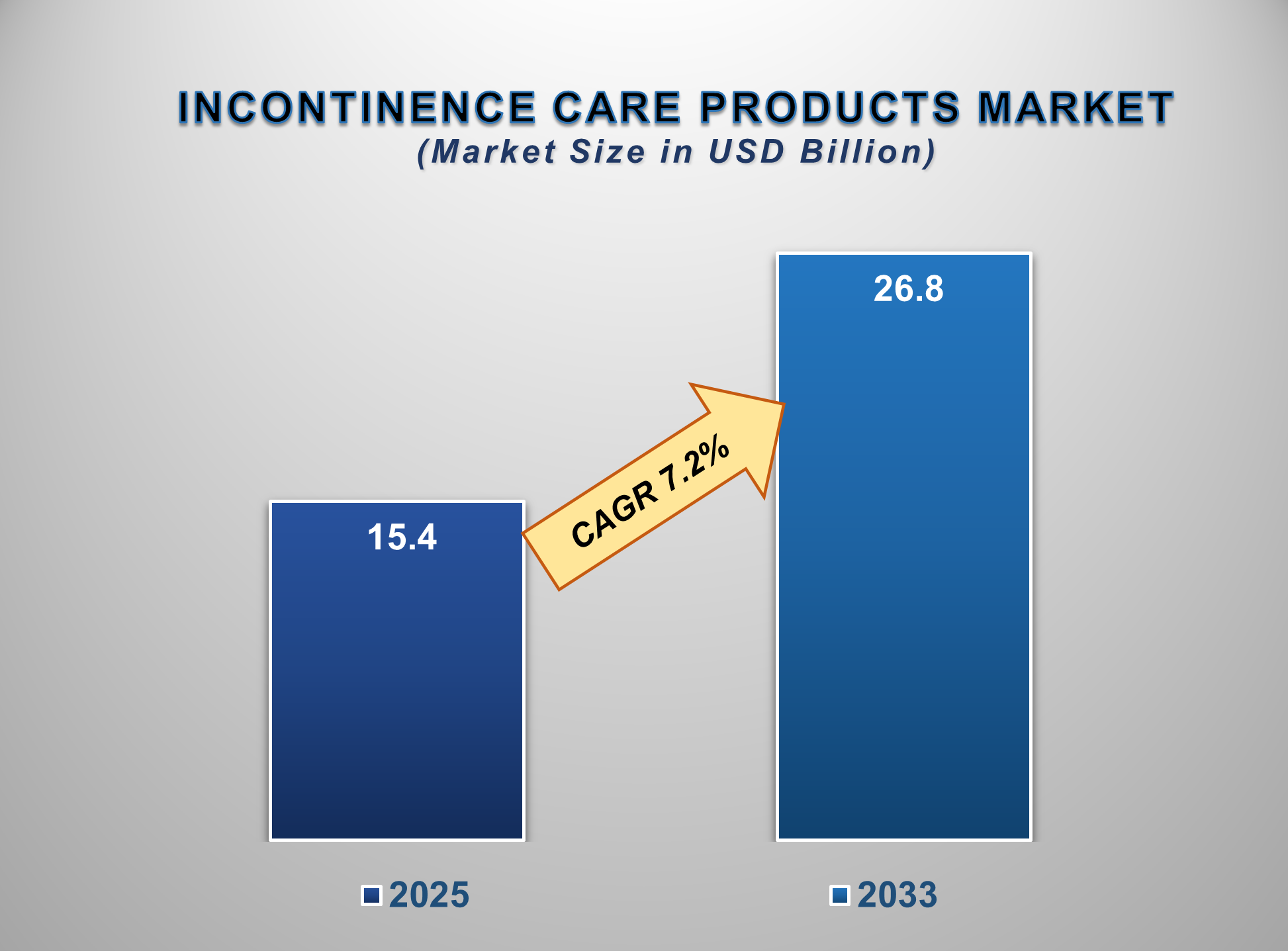

The Incontinence Care Products Market is set to witness strong and sustained growth between 2025 and 2033, driven by the aging global population, rising prevalence of chronic conditions affecting bladder control, and increasing consumer awareness regarding advanced hygiene solutions. The market is expected to be valued at USD 15.4 billion in 2025 and is projected to reach USD 26.8 billion by 2033, registering a CAGR of 7.2% during the forecast period.

Incontinence care products include absorbent hygiene items

such as adult diapers, disposable pads, liners, and protective underwear

designed to manage urinary and fecal

incontinence. These products enhance patient comfort, maintain hygiene, and

reduce the risk of skin infections and caregiver burden.

Growing life expectancy, particularly in developed markets,

is driving large-scale demand among the elderly population. Additionally,

lifestyle disorders, obesity, childbirth-related pelvic floor issues, and

urological surgeries contribute to a higher

incidence of incontinence in younger populations. Innovations in product design, such as odor control,

breathable fabrics, slim-fit absorbent cores, and skin-friendly materials,

have increased adoption rates. North America and

Europe remain leaders due to high awareness and advanced eldercare systems,

while Asia-Pacific is rapidly emerging as a high-growth region fueled by rising

healthcare expenditure and expanding retail access.

Incontinence Care Products Market Drivers and

Opportunities

Rising Geriatric Population and Increasing Prevalence of

Chronic Diseases Are the Primary Market Drivers

The global increase in the elderly population is the most

influential driver supporting market expansion. Individuals aged 65 and above

represent the group most susceptible to urinary and fecal incontinence due to

muscle weakening, chronic diseases, and neurodegenerative disorders such as

Parkinson’s and Alzheimer’s. This demographic shift is creating sustained

demand for effective hygiene solutions worldwide. Simultaneously, chronic illnesses, including diabetes, prostate enlargement, spinal cord

injuries, and post-surgical complications, are

significantly raising the prevalence of incontinence among adults. Healthcare

systems and governments are placing greater focus on elderly well-being,

driving wider availability of advanced incontinence products through retail and

medical channels. This combination of demographic and clinical factors firmly

positions incontinence care products as indispensable for long-term care and

home-based caregiving.

Growing Consumer Acceptance and Innovation in Product Design

Are Accelerating Market Adoption

Increasing awareness and destigmatization of incontinence

are critical to market penetration. Modern products are vastly more discreet,

comfortable, and effective compared to earlier bulky designs, encouraging

higher adoption across diverse age groups. Manufacturers are integrating

ultra-absorbent cores, rapid-dry layers, odor-neutralization technologies, and

hypoallergenic materials that cater to sensitive skin. Moreover,

gender-specific designs, reusable underwear, eco-friendly materials, and

advanced breathable components are appealing to health-conscious consumers.

Retail expansion, especially online channels offering private-label and

subscription-based delivery models, further supports market growth. As

consumers seek improved convenience and dignity, the shift toward premium,

high-performance products remains a strong and enduring catalyst.

Untapped Growth Potential in Emerging Markets and

Technological Advancements Present Significant Opportunities

Emerging markets in Asia-Pacific, Latin America, and parts

of Africa present substantial growth opportunities driven by improving

healthcare access, rising disposable income, and expanding elderly populations.

Increasing penetration of retail pharmacies and e-commerce platforms has

significantly boosted the availability of

incontinence products in these regions. Technological innovations such as smart

diapers that monitor moisture levels, biodegradable materials, and reusable

high-absorbency fabrics offer new pathways for product differentiation.

Additionally, long-term care facilities, home healthcare services, and

government-sponsored eldercare programs are expanding rapidly, creating strong

institutional demand. For manufacturers, opportunities lie in localized

production, cost-optimized product lines, and strategic partnerships with

healthcare providers to capture accelerating demand in developing markets.

Incontinence Care Products Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 15.4 Billion |

|

Market Forecast in 2033 |

USD 26.8 Billion |

|

CAGR % 2025-2033 |

7.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Incontinence

Type ●

By Distribution

Channel ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Incontinence Care Products Market Report

Segmentation Analysis

The global Incontinence Care

Products Market is segmented by Product Type, Incontinence Type, End-user,

Distribution Channel, and Region.

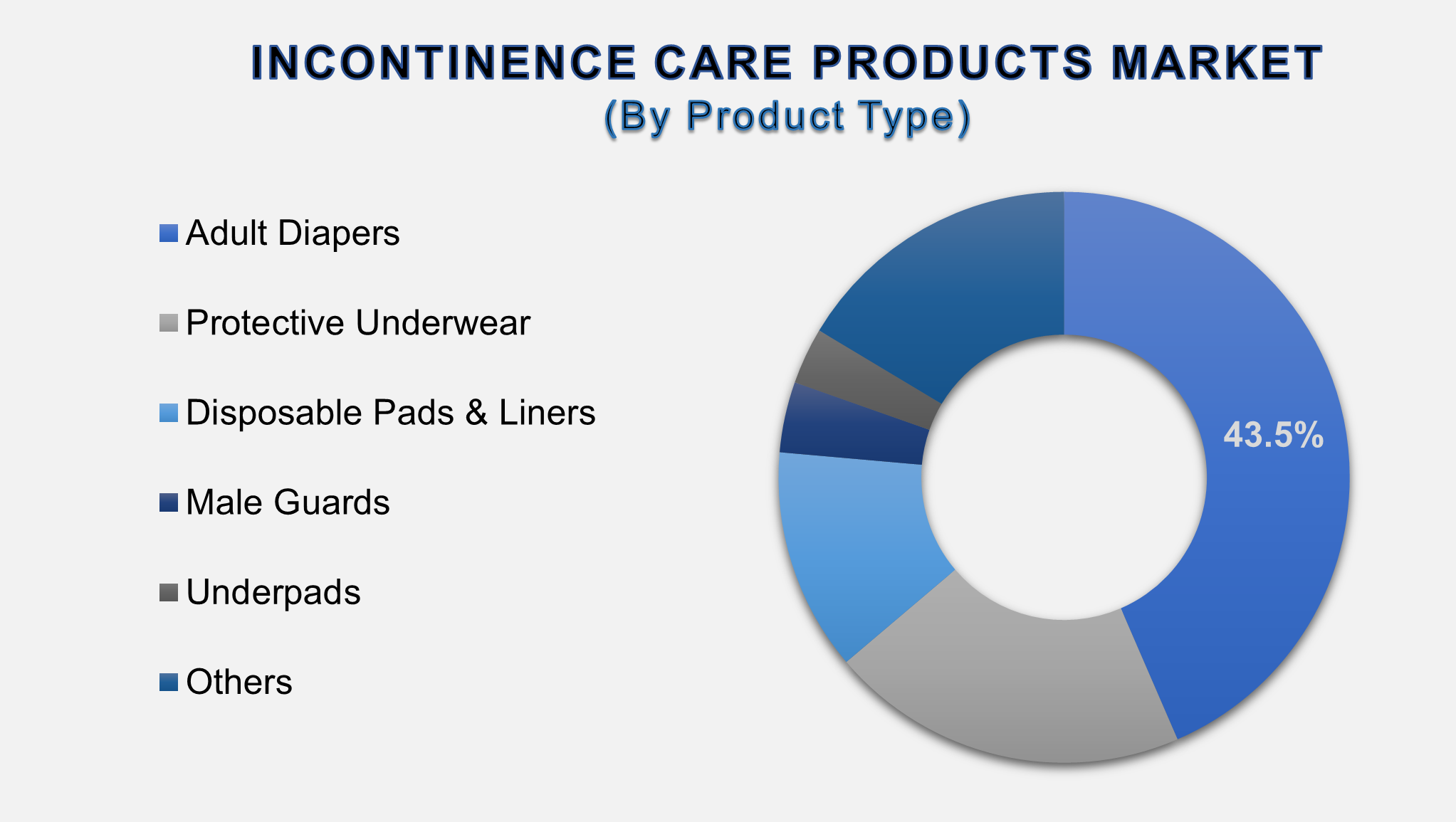

Adult Diapers Are

Anticipated to Command the Largest Market Share in 2025

Adult diapers dominate the Product Type segment due to their unmatched suitability for moderate to severe incontinence management across homecare, hospitals, and long-term care settings. Their market leadership is anchored in superior absorption capacity, multi-layer leak-guard structures, and enhanced comfort that ensures all-day protection for users with mobility challenges or advanced age-related incontinence. Continuous product innovation, such as breathable back sheets, ultra-thin high-capacity cores, pH-balancing materials, and odor-neutralizing technologies, has significantly improved wearability and skin health, driving large-scale adoption.

Premium

ergonomic designs targeted toward active adults, along with gender-specific

variants, are further expanding user acceptance. Rising geriatric populations,

increasing prevalence of chronic conditions like diabetes and stroke, and

growing societal acceptance of incontinence products strengthen demand for

adult diapers over pads or liners. Additionally, strategic distribution through

pharmacies, e-commerce, and institutional bulk supply programs ensures

consistent availability, solidifying adult diapers as the leading product

category in the global Incontinence Care Products Market.

The Urinary Incontinence

Segment Holds the Largest Share by Incontinence Type

Urinary

incontinence represents the most prevalent form of incontinence globally,

making it the leading segment by Incontinence Type. Its dominance stems from

the high incidence of stress incontinence, urge incontinence, overflow

incontinence, and overactive bladder, conditions commonly associated with

childbirth trauma, menopause-related hormonal changes, obesity, pelvic floor

weakening, and prostate disorders in men.

The

segment benefits from significant clinical awareness, with widespread screening

in primary care and urology practices leading to early diagnosis and

intervention. As the global population ages, degenerative neurological

conditions such as Parkinson’s disease, dementia, and diabetes-related

neuropathy are contributing to rising urinary incontinence cases. Healthcare

practitioners increasingly recommend structured continence management programs

involving absorbent products, behavioral

therapies, and pelvic floor rehabilitation, boosting product uptake. With

chronic diseases rising and women disproportionately affected, the need for

effective protection solutions continues to expand. This longstanding and

growing prevalence ensures urinary

incontinence remains the largest and most clinically significant segment.

Hospital Pharmacies Lead

the Distribution Channel Segment

Hospital

pharmacies hold the dominant share in the Distribution Channel segment, driven

by the high utilization of incontinence care products within hospitals,

rehabilitation centers, and long-term care

institutions. These facilities manage patients recovering from surgeries,

chronic illnesses, neurological conditions, and age-related mobility

limitations, groups that frequently require

absorbent products for daily hygiene and comfort. Hospital purchasing

departments typically procure adult diapers, underpads, and briefs in bulk,

ensuring stable and consistent demand.

Additionally,

hospitals serve as key points of first diagnosis for incontinence, where

physicians and nursing staff recommend specific brands or product types,

influencing patient preferences after discharge. The clinical emphasis on

preventing hospital-acquired infections (HAIs), maintaining skin integrity, and

ensuring patient dignity further supports the use of high-quality incontinence

products. With institutional protocols prioritizing premium, dermatologically

safe, and high-absorbency products, hospital pharmacies remain the preferred

and most trusted channel for both inpatients and post-acute care patients,

solidifying their leading position.

The following segments are

part of an in-depth analysis of the global Incontinence Care Products Market:

|

Market

Segments |

|

|

By Product

Type |

●

Adult Diapers ●

Protective Underwear ●

Disposable Pads

& Liners ●

Male Guards ●

Underpads ●

Others |

|

By

Incontinence Type |

●

Urinary Incontinence ●

Faecal Incontinence ●

Mixed Incontinence |

|

By Distribution Channel |

●

Retail Pharmacies ●

Hospital Pharmacies ●

Online Channels ●

Hypermarkets/Supermarkets |

|

By End-user |

●

Hospitals &

Clinics ●

Nursing Homes & Long-term Care

Facilities ●

Others |

Incontinence

Care Products Market Share Analysis by Region

The Asia-Pacific region

is anticipated to hold the largest portion of the Incontinence Care Products

Market globally throughout the forecast period.

Asia-Pacific’s

leadership is driven by its vast and rapidly growing elderly population,

particularly in China, Japan, and South Korea. China represents the largest

contributor due to its expanding healthcare infrastructure, rising elderly care

needs, and increasing adoption of personal hygiene products among the middle

class. Japan, with one of the world’s oldest populations, has extremely high per

capita consumption of adult incontinence products.

India, meanwhile, is witnessing fast-growing demand enabled by rising health

awareness and increasing penetration of retail and e-commerce channels.

The

region’s expansion is further supported by the presence of strong manufacturing

bases, cost-efficient production capabilities, and increasing investments in

eldercare programs. In Southeast Asia, economic growth and improving healthcare

affordability are accelerating product penetration. Collectively, these

dynamics position Asia-Pacific as the fastest-growing and largest market for

incontinence care products globally.

Incontinence Care Products Market Competition

Landscape Analysis

The global market is

moderately consolidated with a mix of multinational corporations and regional

players. Leading companies compete based on product innovation, absorbency

technology, skin-friendly materials, cost-efficiency, and strong distribution

networks. Long-term partnerships with healthcare facilities, investments in

biodegradable and sustainable materials, and strategic expansion across

emerging markets are key competitive strategies. E-commerce expansion and

subscription-based delivery models have become significant differentiators for

consumer convenience and retention.

Global Incontinence Care Products Market Recent Developments

News:

- In January 2025, Essity launched its next-generation TENA ProSkin

line with enhanced breathable layers for sensitive skin in elderly users.

- In October 2024, Kimberly-Clark expanded its adult incontinence

production facility in Indonesia to support rising demand across Southeast

Asia.

- In September 2024, Hartmann

Group introduced a smart incontinence monitoring system integrating

moisture sensors for nursing home applications.

- In July 2024, Ontex Group announced a partnership with healthcare

distributors in India to strengthen its presence in homecare incontinence

solutions.

The Global Incontinence Care Products Market Is

Dominated by a Few Large Companies, such as

●

Essity AB (TENA)

●

Kimberly-Clark

Corporation

●

Procter & Gamble

Co.

●

Cardinal Health, Inc.

●

Ontex Group NV

●

First Quality

Enterprises, Inc.

●

Domtar Corporation

(Attends)

●

Medline Industries, LP

●

B. Braun Melsungen AG

●

Coloplast A/S

●

ConvaTec Group PLC

●

Hollister Incorporated

●

Principle Business

Enterprises, Inc. (Prevail)

●

Unicharm Corporation

●

HARTMANN GROUP

(Molicare)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Incontinence Care

Products Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Incontinence Care Products Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Incontinence Care

Products Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Incontinence

Care Products Market

1.3.2.Incontinence Type of

Global Incontinence Care Products Market

1.3.3.Distribution Channel of Global

Incontinence Care Products Market

1.3.4.End-user of Global Incontinence

Care Products Market

1.3.5.Region of Global Incontinence

Care Products Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Incontinence Care Products Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Incontinence Care Products Market

Estimates & Forecast Trend Analysis, by Product

Type

4.1.

Global

Incontinence Care Products Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Adult Diapers

4.1.2.Protective Underwear

4.1.3.Disposable Pads &

Liners

4.1.4.Male Guards

4.1.5.Underpads

4.1.6.Others

5. Global

Incontinence Care Products Market

Estimates & Forecast Trend Analysis, by Incontinence

Type

5.1.

Global

Incontinence Care Products Market Revenue (US$ Bn) Estimates and Forecasts, by Incontinence

Type, 2020 - 2033

5.1.1.Urinary Incontinence

5.1.2.Fecal Incontinence

5.1.3.Mixed Incontinence

6. Global

Incontinence Care Products Market

Estimates & Forecast Trend Analysis, by End-user

6.1.

Global

Incontinence Care Products Market Revenue (US$ Bn) Estimates and Forecasts, by

End-user 2020 - 2033

6.1.1.Hospitals & Clinics

6.1.2. Nursing Homes &

Long-term Care Facilities

6.1.3.Others

7. Global

Incontinence Care Products Market

Estimates & Forecast Trend Analysis, by Distribution

Channel

7.1.

Global

Incontinence Care Products Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

7.1.1.Retail Pharmacies

7.1.2.Hospital Pharmacies

7.1.3.Online Channels

7.1.4.Hypermarkets/Supermarkets

8. Global

Incontinence Care Products Market

Estimates & Forecast Trend Analysis, by region

8.1.

Global

Incontinence Care Products Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Incontinence

Care Products Market: Estimates &

Forecast Trend Analysis

9.1.

North

America Incontinence Care Products Market Assessments & Key Findings

9.1.1.North America Incontinence

Care Products Market Introduction

9.1.2.North America Incontinence

Care Products Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Incontinence

Type

9.1.2.3. By Distribution

Channel

9.1.2.4. By End-user

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Incontinence

Care Products Market: Estimates &

Forecast Trend Analysis

10.1.

Europe

Incontinence Care Products Market Assessments & Key Findings

10.1.1.

Europe

Incontinence Care Products Market Introduction

10.1.2.

Europe

Incontinence Care Products Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Incontinence

Type

10.1.2.3. By Distribution

Channel

10.1.2.4. By End-user

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Incontinence

Care Products Market: Estimates &

Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Incontinence Care Products Market Introduction

11.1.2.

Asia

Pacific Incontinence Care Products Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Incontinence

Type

11.1.2.3. By Distribution

Channel

11.1.2.4. By End-user

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Incontinence

Care Products Market: Estimates &

Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Incontinence Care Products Market

Introduction

12.1.2.

Middle East & Africa Incontinence Care Products Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Incontinence

Type

12.1.2.3. By Distribution

Channel

12.1.2.4. By End User

12.1.2.5.

By

Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Incontinence Care Products Market:

Estimates & Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Incontinence Care Products Market Introduction

13.1.2.

Latin

America Incontinence Care Products Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

13.1.2.1. By Product

Type

13.1.2.2. By Incontinence

Type

13.1.2.3. By Distribution

Channel

13.1.2.4. By End-user

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Incontinence Care Products Market Product Mapping

15.2.

Global

Incontinence Care Products Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

15.3.

Global

Incontinence Care Products Market Tier Structure Analysis

15.4.

Global

Incontinence Care Products Market Concentration & Company Market Shares (%)

Analysis, 2024

16.

Company

Profiles

16.1.

Essity AB (TENA)

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2. Kimberly-Clark

Corporation

16.3. Procter &

Gamble Co.

16.4. Cardinal

Health, Inc.

16.5. Ontex Group

NV

16.6. First Quality

Enterprises, Inc.

16.7. Domtar

Corporation (Attends)

16.8. Medline

Industries, LP

16.9. B. Braun

Melsungen AG

16.10. Coloplast A/S

16.11. ConvaTec

Group PLC

16.12. Hollister

Incorporated

16.13. Principle

Business Enterprises, Inc. (Prevail)

16.14. Unicharm

Corporation

16.15. HARTMANN

GROUP (Molicare)

16.16. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables