Industrial Cleaner Market Size and Forecast (2020-2035), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Acidic Cleaner, Disinfectants, Degreasers, General Cleaners, Surfactants, and Others), By End-Use Industry (Oil, Gas & Petrochemicals, Food & Beverages, Healthcare, Manufacturing, and Others) and Geography

2025-12-30

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Industrial

Cleaner Market Overview

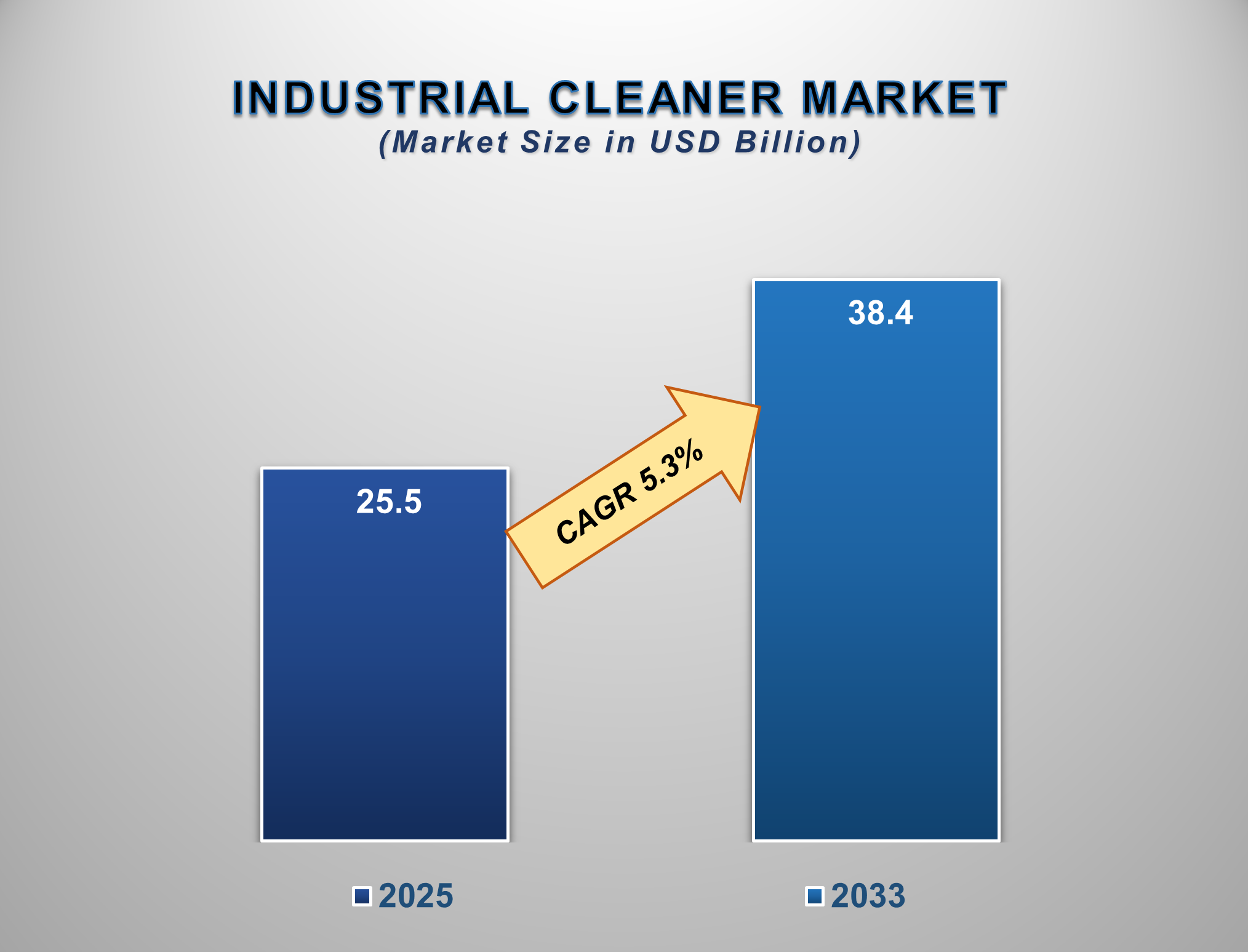

The global Industrial Cleaner Market is poised for steady and sustainable growth from 2025 to 2035, driven by stringent regulatory standards for workplace hygiene, heightened health and safety awareness, and rapid industrialization in emerging economies. The market is projected to be valued at approximately USD 25.5 billion in 2025 and is forecasted to reach nearly USD 38.4 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.3% during this period.

Industrial cleaners encompass a wide range of chemical

formulations and specialized products designed to remove dirt, grease, oil,

microbial contaminants, and other soils from surfaces and equipment in

commercial, institutional, and industrial settings. The market's expansion is

underpinned by the critical objective of ensuring operational safety, extending

equipment lifespan, maintaining product quality, and complying with

increasingly strict environmental and health regulations. A key trend is the

paradigm shift towards sustainable, eco-friendly solutions, including

bio-based, low-VOC (volatile organic compounds), and biodegradable

formulations. Factors such as the lasting impact of COVID-19 on hygiene

protocols, technological integration through automation and IoT, and the

expansion of end-use industries like pharmaceuticals and food processing are

key contributors to market growth. North America currently holds the largest

market share due to well-established regulatory frameworks and high hygiene standards,

while the Asia-Pacific region is expected to be the fastest-growing market,

fueled by massive industrial expansion and rising governmental focus on

sanitation.

Industrial Cleaner Market Drivers and

Opportunities

Stringent Hygiene Regulations and Heightened Health Awareness

are the Primary Market Drivers

The most significant driver for the industrial cleaner

market is the global tightening of health, safety, and environmental

regulations, enforced by agencies like the U.S. Environmental Protection Agency

(EPA), the European Chemicals Agency (ECHA), and the Occupational Safety and

Health Administration (OSHA). The COVID-19 pandemic permanently elevated

baseline hygiene expectations, making infection control a top operational

priority across healthcare, food service, hospitality, and manufacturing

sectors. This regulatory and societal pressure compels businesses to adopt

certified, high-performance cleaning chemicals and validated protocols to avoid

penalties, ensure consumer safety, and protect their brand reputation, creating

consistent and growing demand.

Shift Towards Sustainability and Green Chemistry Presents a

Major Growth Vector

A powerful and defining trend is the accelerating demand

for sustainable and eco-friendly cleaning solutions. Driven by corporate

Environmental, Social, and Governance (ESG) goals, consumer preference, and

regulatory restrictions on harmful chemicals (e.g., PFAS, high-VOC solvents),

industries are actively seeking biodegradable, plant-based, and non-toxic

formulations. This shift is moving sustainability from a niche consideration to

a core strategic driver, opening a multi-billion-dollar opportunity for manufacturers to innovate with

enzyme-based cleaners, biosurfactants, and products featuring recyclable

packaging. Companies that lead in green chemistry and offer comprehensive

sustainability consulting are gaining a significant competitive edge.

Digital Transformation and Automation Unlock Efficiency and

New Business Models

The integration of advanced technologies is creating

substantial growth opportunities. The rise of IoT-enabled dispensing systems,

AI-powered robotic cleaners, and predictive analytics is transforming

traditional cleaning into intelligent, data-driven processes. These smart

systems enable real-time monitoring of chemical usage, optimize cleaning

schedules, ensure compliance through automated reporting, and reduce resource

waste. Furthermore, this digital shift is facilitating new service-based

business models, such as chemical management subscriptions and

"Cleaning-as-a-Service," which deepen vendor-customer relationships

and provide recurring revenue streams for market players.

Industrial Cleaner Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 25.5 Billion |

|

Market Forecast in 2033 |

USD 38.4 Billion |

|

CAGR % 2025-2033 |

5.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By End-Use

Industry |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Industrial Cleaner Market Report Segmentation

Analysis

The

global Industrial Cleaner Market is segmented by Product Type, End-user

Industry, and Region.

The Disinfectants and

Sanitizers segment is anticipated to command a significant market share.

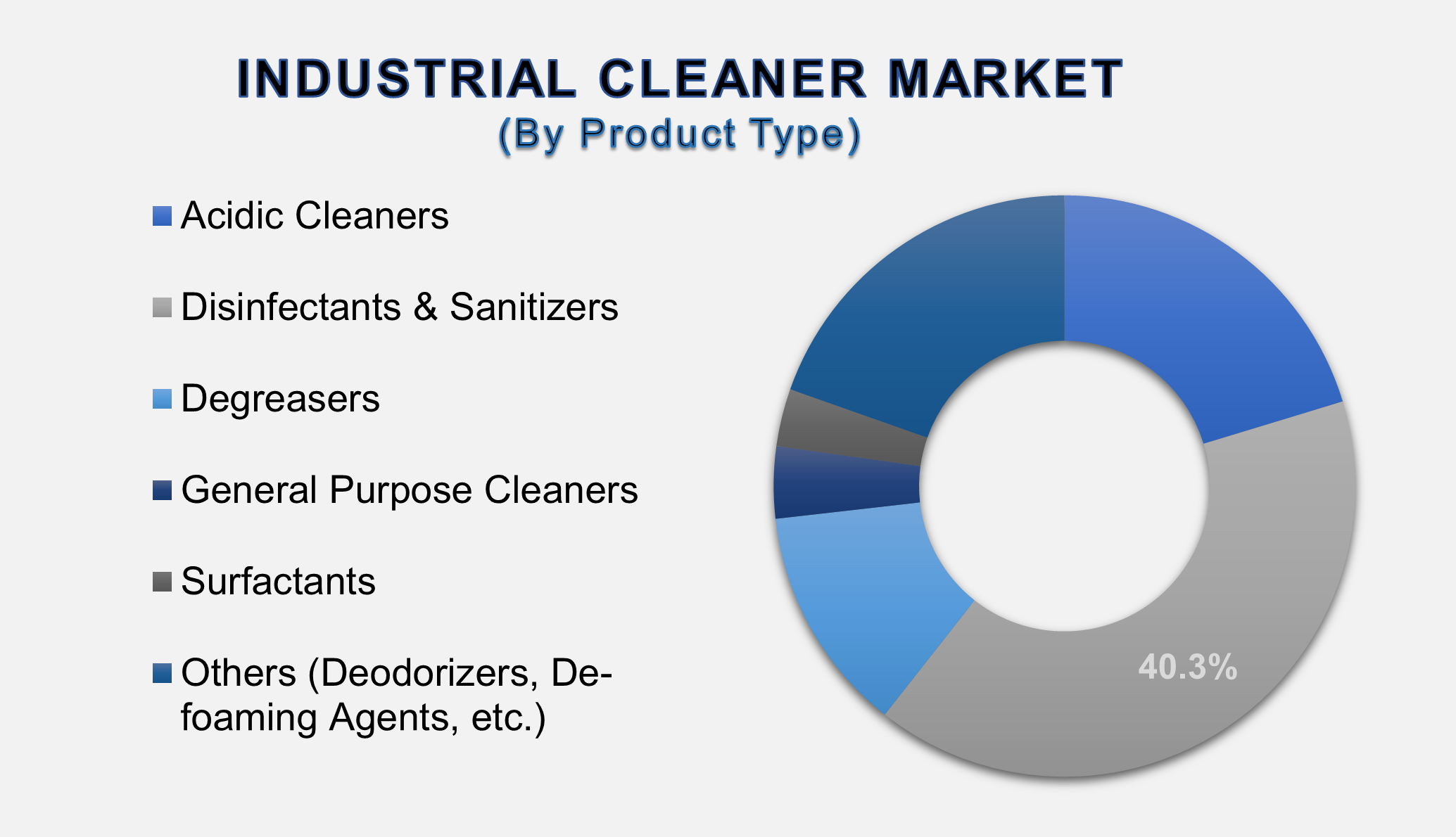

The Product Type segment includes Acidic Cleaners, Disinfectants, Degreasers, General Purpose Cleaners, Surfactants, and others. Disinfectants and Sanitizers represent one of the largest and fastest-growing categories, with a forecasted CAGR of 6.7%. This dominance is a direct result of the post-pandemic "new normal," where elevated hygiene vigilance in healthcare, foodservice, hospitality, and public spaces has become permanent. The segment is innovating with broad-spectrum, quaternary-ammonium-free, and extended-efficacy formulations to meet evolving regulatory and consumer demands.

The Oil, Gas &

Petrochemicals (OG&P) segment is the cornerstone of the market.

The

End-Use Industry segment is categorized into Oil, Gas & Petrochemicals,

Food & Beverages, Healthcare, Manufacturing, and others. The OG&P

segment dominates, holding approximately 58.3% of the market share. This is due

to the industry's intensive and non-negotiable requirements for cleaning

pipelines, storage tanks, and refinery equipment to ensure operational safety,

prevent corrosion, and maintain efficiency. The segment's growth is tied

directly to global energy demand and investments in upstream and downstream

infrastructure, creating consistent demand for heavy-duty degreasers and

refinery-specific cleaners.

The following segments are

part of an in-depth analysis of the global Industrial Cleaner Market:

|

Market

Segments |

|

|

By Product

Type |

●

Acidic Cleaners ●

Disinfectants &

Sanitizers ●

Degreasers ●

General Purpose

Cleaners ●

Surfactants ●

Others (Deodorizers,

De-foaming Agents, etc.) |

|

By End-user

Industry |

●

Oil, Gas &

Petrochemicals ●

Food & Beverages ●

Healthcare ●

Manufacturing &

Commercial Offices ●

Others (Automotive,

Textiles, Power Generation, etc.) |

Industrial Cleaner Market Share Analysis by

Region

North America is expected

to account for the major share of the global industrial cleaner market over the

forecast period

North

America's dominance is attributed to its mature industrial base and the world's

most stringent and well-enforced regulatory environment governed by the EPA,

OSHA, and FDA. The region has a high concentration of leading chemical

manufacturers, advanced healthcare infrastructure, and a food processing

industry that mandates premium, fully documented cleaning solutions. High

consumer and corporate awareness regarding hygiene and sustainability further

consolidates North America's position as the leading value market.

The

Asia-Pacific region is poised to be the fastest-growing market, driven by

explosive industrialization, rapid urbanization, and proactive government

hygiene campaigns like India's "Swachh Bharat Abhiyan." The massive expansion of manufacturing, food processing,

and healthcare sectors in China, India, and Southeast Asia is creating

unprecedented demand for both basic and advanced cleaning chemicals.

Furthermore, governments in the region are progressively tightening chemical

control and food safety laws (similar to REACH and FDA standards), which is

professionalizing procurement and favoring

quality-certified products, thereby accelerating market growth.

Industrial Cleaner Market Competition Landscape

Analysis

The global industrial cleaner

market is moderately consolidated and highly competitive, featuring a mix of

diversified chemical conglomerates and specialized cleaning solution providers.

Competition centers on technological innovation in sustainable formulations,

breadth of product portfolio, technical service and support, and the ability to

offer integrated, value-added services like on-site training, compliance

auditing, and smart chemical management systems. Key strategies include heavy

investment in R&D for bio-based alternatives, strategic partnerships with

enzyme specialists and technology firms, geographic expansion into high-growth

APAC markets, and mergers & acquisitions to bolster technological

capabilities or market reach

Global Industrial Cleaner Market Recent Developments News:

- In January 2025, Brenntag, a global chemical distributor, expanded

its distribution agreement with Kao Chemicals Europe to strengthen its

supply of sustainable industrial cleaning ingredients in the U.S. market.

- In 2024, Ecolab and Novonesis (formerly Novozymes) partnered to

co-develop enzyme-driven Clean-in-Place (CIP) solutions for the dairy

industry, aiming to slash chlorine use by 80%.

- In 2024, regulatory pressure led 3M to announce the discontinuation

of all PFAS manufacturing by the end of 2025, triggering an industry-wide scramble and creating a

massive opportunity for alternative chemical technologies.

- The EU is progressing towards a potential complete prohibition of

approximately 10,000 PFAS substances by 2026-2030, representing the

largest-ever regulatory shift for the industry and forcing a fundamental

reformulation of many specialty cleaners

The Global Industrial Cleaner Market Is Dominated

by a Few Large Companies, such as

●

BASF SE

●

Ecolab Inc.

●

Dow Chemical Company

●

3M Company

●

Solvay S.A.

●

Evonik Industries AG

●

Clariant AG

●

Stepan Company

●

Croda International

Plc

●

Huntsman Corporation

●

Diversey Holdings Ltd.

●

Henkel AG & Co.

KGaA

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Industrial Cleaner

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Industrial Cleaner Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Industrial Cleaner

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Industrial

Cleaner Market

1.3.2.End-user Industry of

Global Industrial Cleaner Market

1.3.3.Region of Global Industrial

Cleaner Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Industrial Cleaner Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Industrial Cleaner Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Industrial Cleaner Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Acidic Cleaners

4.1.2.Disinfectants &

Sanitizers

4.1.3.Degreasers

4.1.4.General Purpose Cleaners

4.1.5.Surfactants

4.1.6.Others (Deodorizers,

De-foaming Agents, etc.)

5. Global

Industrial Cleaner Market Estimates

& Forecast Trend Analysis, by End-user Industry

5.1.

Global

Industrial Cleaner Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

Industry, 2020 - 2033

5.1.1.Oil, Gas &

Petrochemicals

5.1.2.Food & Beverages

5.1.3.Healthcare

5.1.4.Manufacturing &

Commercial Offices

5.1.5.Others (Automotive,

Textiles, Power Generation, etc.)

6. Global

Industrial Cleaner Market Estimates

& Forecast Trend Analysis, by region

6.1.

Global

Industrial Cleaner Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Industrial

Cleaner Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Industrial Cleaner Market Assessments & Key Findings

7.1.1.North America Industrial

Cleaner Market Introduction

7.1.2.North America Industrial

Cleaner Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Product

Type

7.1.2.2. By End-user

Industry

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Industrial

Cleaner Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Industrial Cleaner Market Assessments & Key Findings

8.1.1.Europe Industrial Cleaner

Market Introduction

8.1.2.Europe Industrial Cleaner

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By End-user

Industry

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Industrial

Cleaner Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Industrial

Cleaner Market Introduction

9.1.2.Asia Pacific Industrial

Cleaner Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By End-user

Industry

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Industrial

Cleaner Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Industrial Cleaner Market

Introduction

10.1.2.

Middle East & Africa Industrial Cleaner Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By End-user

Industry

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Industrial Cleaner Market: Estimates

& Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Industrial Cleaner Market Introduction

11.1.2.

Latin

America Industrial Cleaner Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Product

Type

11.1.2.2. By End-user

Industry

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Industrial Cleaner Market Product Mapping

13.2.

Global

Industrial Cleaner Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

13.3.

Global

Industrial Cleaner Market Tier Structure Analysis

13.4.

Global

Industrial Cleaner Market Concentration & Company Market Shares (%)

Analysis, 2024

14.

Company

Profiles

14.1.

BASF SE

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Ecolab Inc.

14.3. Dow Chemical

Company

14.4. 3M Company

14.5. Solvay S.A.

14.6. Evonik

Industries AG

14.7. Clariant AG

14.8. Stepan

Company

14.9. Croda

International Plc

14.10. Huntsman

Corporation

14.11. Diversey

Holdings Ltd.

14.12. Henkel AG

& Co. KGaA

14.13. Other

Prominent Players

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables