Industrial Lubricants Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Product (Process Oils, General Industrial Oils, Metalworking Fluids, Industrial Engine Oils, Greases, Others), By Application (Metalworking, Textiles, Energy, Chemical Manufacturing, Food Processing, Hydraulic, Others) And Geography

2025-08-12

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Industrial

Lubricants Market Overview

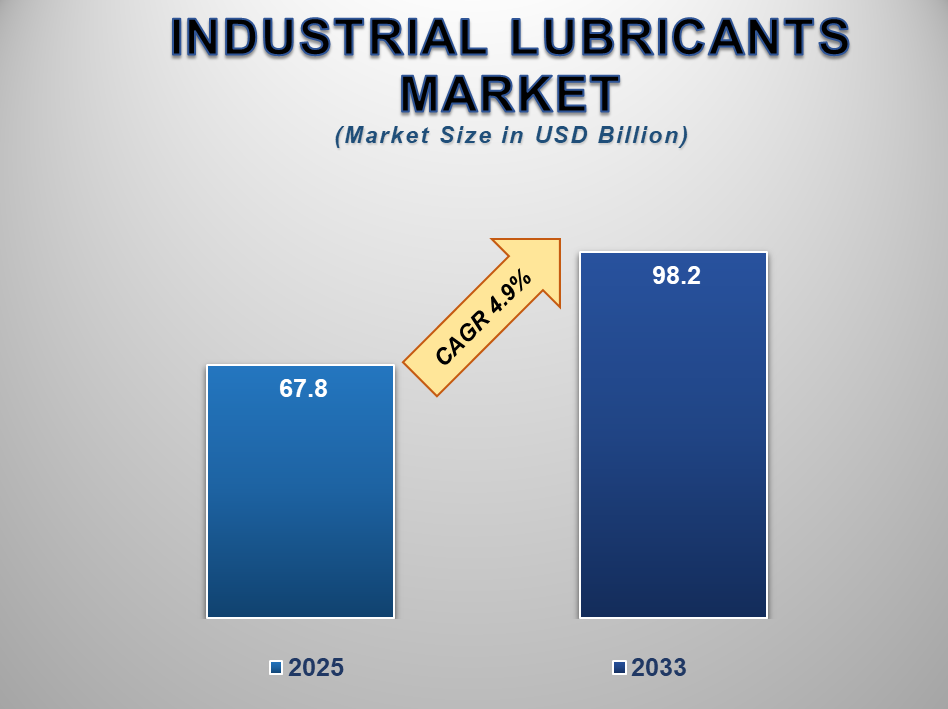

The global Industrial Lubricants market size is projected to reach US$ 98.2 Billion by 2033 from US$ 67.8 Billion in 2025. The market is expected to register a CAGR of 4.9% during 2025–2033. This growth is driven by the increasing demand for high-performance machinery across industries such as manufacturing, automotive, energy, and construction.

Industrial lubricants play a

crucial role in reducing friction, decreasing wear and tear, and promoting

efficiency and longevity of machinery and equipment. With industries becoming

increasingly automation- and efficiency-driven, advanced lubrication solutions

are increasingly becoming necessary. The market is growing due to technological

upgrades, industrial output, and the increased focus on preventive maintenance

globally. Based on market analysis and projected trends, the industrial

lubricant market is expected to grow strongly in the next ten years. The growth

of global industrialization, particularly in burgeoning economies such as

China, India, and Brazil, is one of the key growth drivers. Greater demands for

synthetic and bio-based lubricants, owing to higher properties and

environmental regulation compliance, are further boosting market development.

Additionally, energy efficiency demands in various industries are compelling

lubricant manufacturers to innovate and design high-quality, long-lasting products.

Industrial

Lubricants Market Drivers and Opportunities

Growing

demand for high-performance machinery across industries is anticipated to lift

the industrial lubricants market

The increasing need for

high-performance equipment in manufacturing, mining, construction, automotive,

and power generation industries is one of the main drivers of the international

market for industrial lubrication. With an expanding base of these industries,

there is an increased requirement for efficient and long-lasting equipment,

which in turn requires high-quality lubrication to provide smooth operation and

longevity. Various industrial lubrication products, from hydraulic and gear

lubrication to compressor and turbine lubrication, play crucial roles in

friction reduction, corrosion prevention, and maximizing equipment

functionality even in extreme working conditions. The global push toward

automation and intelligent manufacturing has also increased the requirement for

high-accuracy machinery, which largely depends on optimal lubrication for

smooth, uninterrupted operation. This is most evident in developing economies,

where galloping industrialization is leading to heavy investments in modernized

infrastructure and sophisticated machinery. Apart from that, businesses are

becoming increasingly concerned about reducing maintenance expenses and

achieving maximum operational uptime, which is creating an increased sense of

reliance on effective lubrication methods. The application of high-performing

synthetic and half-synthetic lubrication is also increasing due to higher

properties, such as improved thermal stability, increased life, and improved

load-carrying capacity. With increased global competition, industries are

compelled to enhance output and minimize machine downtime, further accelerating

lubricant usage. An increase in heavy-duty and power-intensive activities,

particularly in the mining and construction industries, is also fueling

lubrication demands.

Rising

emphasis on preventive maintenance and equipment longevity is a vital driver

for influencing the growth of the global industrial lubricants market

The heightened attention to

preventive maintenance tactics and the requirement to lengthen equipment life

cycles an essential impetuses driving the industrial lubricant market further.

Industrial machinery is subject to high stress, rigorous temperatures, and

heavy workloads, subjecting it to wear and fatigue. In such scenarios,

lubricants become an indispensable element in upholding mechanical integrity,

avoiding breakages, and maximizing overall system efficiency. Organizations

across industries recognize the exorbitant expenses involved in unscheduled

breakages, repairs, and component replacement, which have resulted in shifting

from reactive to preventive maintenance paradigms. Lubricant application in an

organized, methodical manner plays an important role in ensuring machinery

health, easing friction and corrosion, and optimizing energy efficiency. This

has encouraged organizations to invest in superior-quality lubricants that

complement long-term asset manageability objectives. Moreover, advances in condition

monitoring instruments and intelligent lubrication systems enable real-time

tracking of lubricant efficiency, which allows timely actions and recharging.

This context of lubricant integration into predictive attention not just lowers

expenses but also maximizes safety and operational reliability. Original

Equipment Manufacturers (OEMs) also suggest specific lubricant usage for

specific machinery, further advancing lubricant usage among end-users. In

industries like aerospace, marine, and heavy manufacturing, where replacement

of machinery is capital-heavy, the position of industrial lubricant plays an

even more significant role for industries. Governmental norms and standards

pertaining to equipment safety and environmental conservation are also pushing

industries to dedicate time to upkeep using quality lubrication. The market

dynamics that change, keeping asset optimization and cost-effectiveness as key

priorities, lay a strong foundation for the ongoing growth of the industrial

lubricant market.

Growing

adoption of bio-based and environmentally friendly lubricants is poised to

create significant opportunities in the global industrial lubricants market

The rising global emphasis on

sustainability and environmental conservation is creating a promising

opportunity for the growth of bio-based and environmentally friendly lubricants

within the industrial lubricants market. With increasing scrutiny on the environmental

impact of petroleum-based products, industries are exploring alternatives that

can reduce carbon footprints, improve biodegradability, and comply with

evolving environmental regulations. Bio-based lubricants, derived from

vegetable oils and other renewable sources, offer several advantages such as

low toxicity, high biodegradability, and improved lubricity. These attributes

make them highly suitable for applications in environmentally sensitive areas

like marine, forestry, agriculture, and food processing. Governments and

regulatory bodies across North America, Europe, and the Asia-Pacific are

implementing strict regulations and offering incentives to promote the adoption

of eco-friendly lubricants, thereby creating a conducive environment for market

growth. For instance, the EU Ecolabel and USDA BioPreferred Program certify

products that meet specific environmental performance criteria, encouraging

manufacturers to invest in green technologies. In addition, corporate

sustainability goals are driving companies to transition from conventional to

environmentally responsible operations, with lubricants playing a key role in

that shift. Technological advancements have also improved the thermal

stability, oxidation resistance, and shelf life of bio-lubricants, making them

more viable for heavy-duty industrial use. Furthermore, consumer awareness

regarding environmental issues and the growing demand for green-certified

products are pushing industrial buyers to opt for sustainable lubrication

solutions.

Industrial

Lubricants Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 67.8 Billion |

|

Market Forecast in 2033 |

USD 98.2 Billion |

|

CAGR % 2025-2033 |

4.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Product ●

By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Industrial

Lubricants Market Report Segmentation Analysis

The Global Industrial Lubricants

Market industry analysis is segmented by Product, by Application, and by

Region.

The

metalworking fluids segment is anticipated to hold the highest share of the

global industrial lubricants market during the projected timeframe

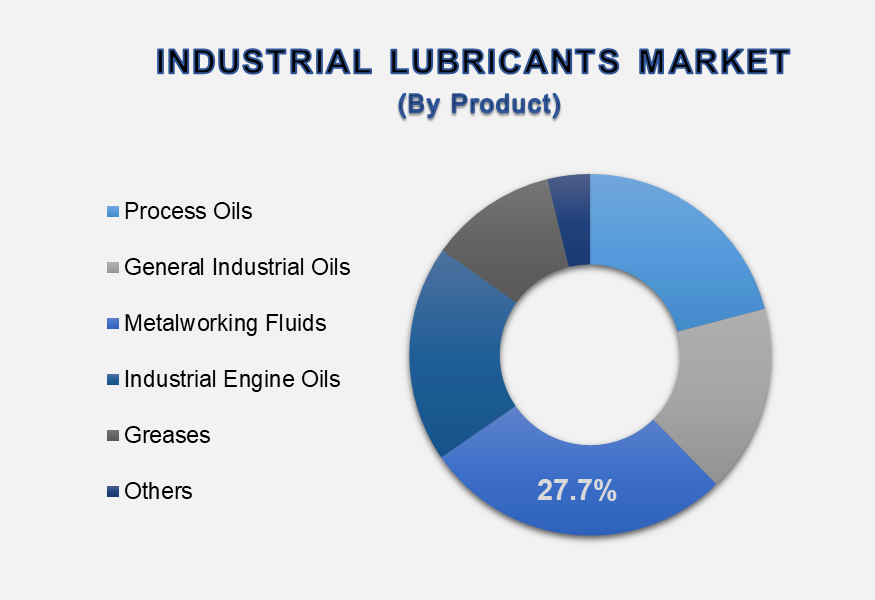

By product, it is segmented into Process Oils, General Industrial Oils, Metalworking Fluids, Industrial Engine Oils, Greases, and Others. The segment of metalworking fluids is expected to command the largest share of 27.7% in the global market for industrial lubricants. This dominance is attributed, to a large extent, to the extensive application of metalworking fluids in cutting, grinding, milling, and other machining processes in major manufacturing industries like automotive, aerospace, and heavy machinery. These fluids serve to reduce heat, reduce friction, and provide accuracy in metal shaping and fabrication. Moreover, the transition towards precision engineering, CNC machining, and sophisticated manufacturing technologies has increased dependence on effective lubrication solutions to aid efficiency, tool life, and product quality. Increased focus on optimizing productivity and decreasing operating downtime further backs the segment's growth, rendering it most prominent in the product category.

The

metalworking segment is anticipated to hold the highest share of the market

over the forecast period

By Application, the market is

divided into Metalworking, Textiles, Energy, Chemical Manufacturing, Food

Processing, Hydraulic, and Other segments. The metalworking segment is

anticipated to command the top market share within the industrial lubricant market

in 2024, based on forecast period segmentations. The high demand for lubricant

within metal fabrication and machining processes is fueled by accelerating

industrialization, especially within emerging economies, as well as rising

output levels within automotive and general manufacturing industries. Lubricant

is highly dependent upon metalworking processes to increase cutting efficiency,

enhance surface finish, and prolong machinery and tool life. In addition,

technological advances within synthetic and semi-synthetic formulations

designed for advanced equipment and harsh working conditions further spur the

segment's growth. With metalworking processes being the core of global

industrial manufacturing, this segment is likely to be the leading application

for the forecast period ahead.

The following segments are part of an in-depth analysis of the global

industrial lubricants market:

|

Market Segments |

|

|

By Product |

●

Process Oils ●

General Industrial

Oils ●

Metalworking Fluids ●

Industrial Engine

Oils ●

Greases ●

Others |

|

By Application |

●

Metalworking ●

Textiles ●

Energy ●

Chemical

Manufacturing ●

Food Processing ●

Hydraulic ●

Others |

Industrial

Lubricants Market Share Analysis by Region

The

Asia Pacific is projected to hold the largest share of the global industrial

lubricants market over the forecast period

The Asia-Pacific region is in the

leading position in the global industrial lubricant market, where it is

estimated to hold about 43.6% of the total market share. This dominance is

fueled by strong industrial development, urbanization, and a rising manufacturing

base in leading economies like China, India, Japan, and South Korea. The region

is also where many of the largest automotive, machinery, electronics, and metal

processing industries of the world are based, which serve as heavy consumers of

industrial lubricants. Efforts by governments to encourage industrialization,

development of infrastructure, and foreign direct manufacturing investment

further drive lubricant consumption. The increasing adoption of advanced

manufacturing technologies and added attention to equipment reliability and

efficiency also support the consumption of high-end lubricant products, mostly

metalworking lubricants and hydraulic lubricants. Availability and cheap labor

and a supportive business environment continue to lure global manufacturers to

establish manufacturing capacity in the region to support market growth in the

long run.

In addition, North America is likely to exhibit the highest CAGR over the forecasted period. The growth is triggered by surging investments in manufacturing automation, energy creation, and infrastructure upgrades in the United States as well as Canada. The rising interest of the region in high-efficiency, as well as eco-friendly lubricants, complemented by robust government regulation and technological innovation, is driving market growth. North America's development of cleaner industrial processes and adoption of intelligent lubrication systems is likely to fuel growth in synthetic and specialty lubricant demand in the next few years.

Industrial

Lubricants Market Competition Landscape Analysis

The global industrial lubricants

market is marked by robust competition among key players focusing on

innovation, strategic expansion, and sustainability. Continuous research and

development efforts lead to the introduction of advanced industrial lubricant

formulations with improved performance characteristics, catering to evolving

industry demands.

Global

Industrial Lubricants Market Recent Developments News:

- In January

2024, Shell plc finalized its purchase of MIDEL and MIVOLT from

UK-based M&I Materials Ltd. Separately, BP p.l.c. expanded its digital

capabilities by establishing a Pune-based hub in January 2021, enhancing

its ability to deliver innovative and sustainable solutions. These

strategic moves underscore both companies' focus on technological

advancement and energy transition.

- In October

2023, Chevron Corporation partnered with Hindustan Petroleum

Corporation Ltd (HPCL) to reintroduce its Caltex lubricant brand in India

after a 12-year hiatus. Under the agreement, HPCL will license,

manufacture, and distribute Chevron’s lubricants, targeting industrial and

commercial vehicle segments. This strategic collaboration marks Chevron’s

re-entry into India’s growing lubricants market, leveraging HPCL’s

extensive distribution network.

- In

June 2021, FUCHS bolstered its

specialty lubricants division through the full acquisition of Gleitmo

Technik AB’s lubricants business. The transaction, integrated under FUCHS

LUBRICANTS SWEDEN AB, includes Gleitmo’s complete product portfolio,

customer base, employees, and lease agreements. This move enhances FUCHS’

market position in niche lubricant solutions and strengthens its

operational footprint in the region.

The

Global Industrial Lubricants Market is dominated by a few large companies, such

as

●

Exxonmobil Corp

●

Fuchs Group

●

The Lubrizol Corporation

●

Royal Dutch Shell

●

Phillips 66

●

Lucas Oil Products, Inc.

●

Amsoil, Inc.

●

Bel-Ray Co., Inc.

●

Total S.A.

●

Kluber Lubrication

●

Valvoline International, Inc.

●

Chevron Corp

●

Clariant

●

Quaker Chemical Corp

●

Houghton International, Inc.

●

Castrol

●

Blaser Swisslube, Inc.

●

Calumet Specialty Products Partners, L.P.

●

Petronas Lubricant International

●

Idemitsu Kosan Co., Ltd.

●

Yushiro Chemical Industry Co., Ltd.

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

- Global Industrial Lubricants Market Introduction and Market Overview

- Objectives of the Study

- Global Industrial Lubricants Market Scope and Market Estimation

- Global Industrial Lubricants Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Industrial Lubricants Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Product of Global Industrial Lubricants Market

- Devices of Global Industrial Lubricants Market

- Region of Global Industrial Lubricants Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Industrial Lubricants Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Industrial Lubricants Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Industrial Lubricants Market Estimates & Forecast Trend Analysis, by Product

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Process Oils

- General Industrial Oils

- Metalworking Fluids

- Industrial Engine Oils

- Greases

- Others

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Global Industrial Lubricants Market Estimates & Forecast Trend Analysis, by Application

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Metalworking

- Textiles

- Energy

- Chemical Manufacturing

- Food Processing

- Hydraulic

- Others

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Industrial Lubricants Market Estimates & Forecast Trend Analysis, by Region

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Industrial Lubricants Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Industrial Lubricants Market: Estimates & Forecast Trend Analysis

- North America Industrial Lubricants Market Assessments & Key Findings

- North America Industrial Lubricants Market Introduction

- North America Industrial Lubricants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By Country

- The U.S.

- Canada

- North America Industrial Lubricants Market Assessments & Key Findings

- Europe Industrial Lubricants Market: Estimates & Forecast Trend Analysis

- Europe Industrial Lubricants Market Assessments & Key Findings

- Europe Industrial Lubricants Market Introduction

- Europe Industrial Lubricants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Industrial Lubricants Market Assessments & Key Findings

- Asia Pacific Industrial Lubricants Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Industrial Lubricants Market Introduction

- Asia Pacific Industrial Lubricants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Industrial Lubricants Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Industrial Lubricants Market Introduction

- Middle East & Africa Industrial Lubricants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Industrial Lubricants Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Industrial Lubricants Market Introduction

- Latin America Industrial Lubricants Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By Application

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Industrial Lubricants Market Product Mapping

- Global Industrial Lubricants Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Industrial Lubricants Market Tier Structure Analysis

- Global Industrial Lubricants Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Exxonmobil Corp

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Exxonmobil Corp

* Similar details would be provided for all the players mentioned below

- Fuchs Group

- The Lubrizol Corporation

- Royal Dutch Shell

- Phillips 66

- Lucas Oil Products, Inc.

- Amsoil, Inc.

- Bel-Ray Co., Inc.

- Total S.A.

- Kluber Lubrication

- Valvoline International, Inc.

- Chevron Corp

- Clariant

- Quaker Chemical Corp

- Houghton International, Inc.

- Castrol

- Blaser Swisslube, Inc.

- Calumet Specialty Products Partners, L.P.

- Petronas Lubricant International

- Idemitsu Kosan Co., Ltd.

- Yushiro Chemical Industry Co., Ltd.

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables