Industrial Packaging Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; Product Type (Drums, IBCs, Sacks, Pails, and Crates/Totes), Material (Paperboard, Plastic, Metal, Wood, and Fiber), Application (Chemical and Pharmaceuticals, Building and Construction, Food and Beverages, Oil and Lubricants, Agriculture and Horticulture, and Others), and Geography

2026-02-23

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Industrial

Packaging Market Overview

The global

industrial packaging market is experiencing strong growth, driven by rising

demand for clean energy, supportive government policies, and declining solar

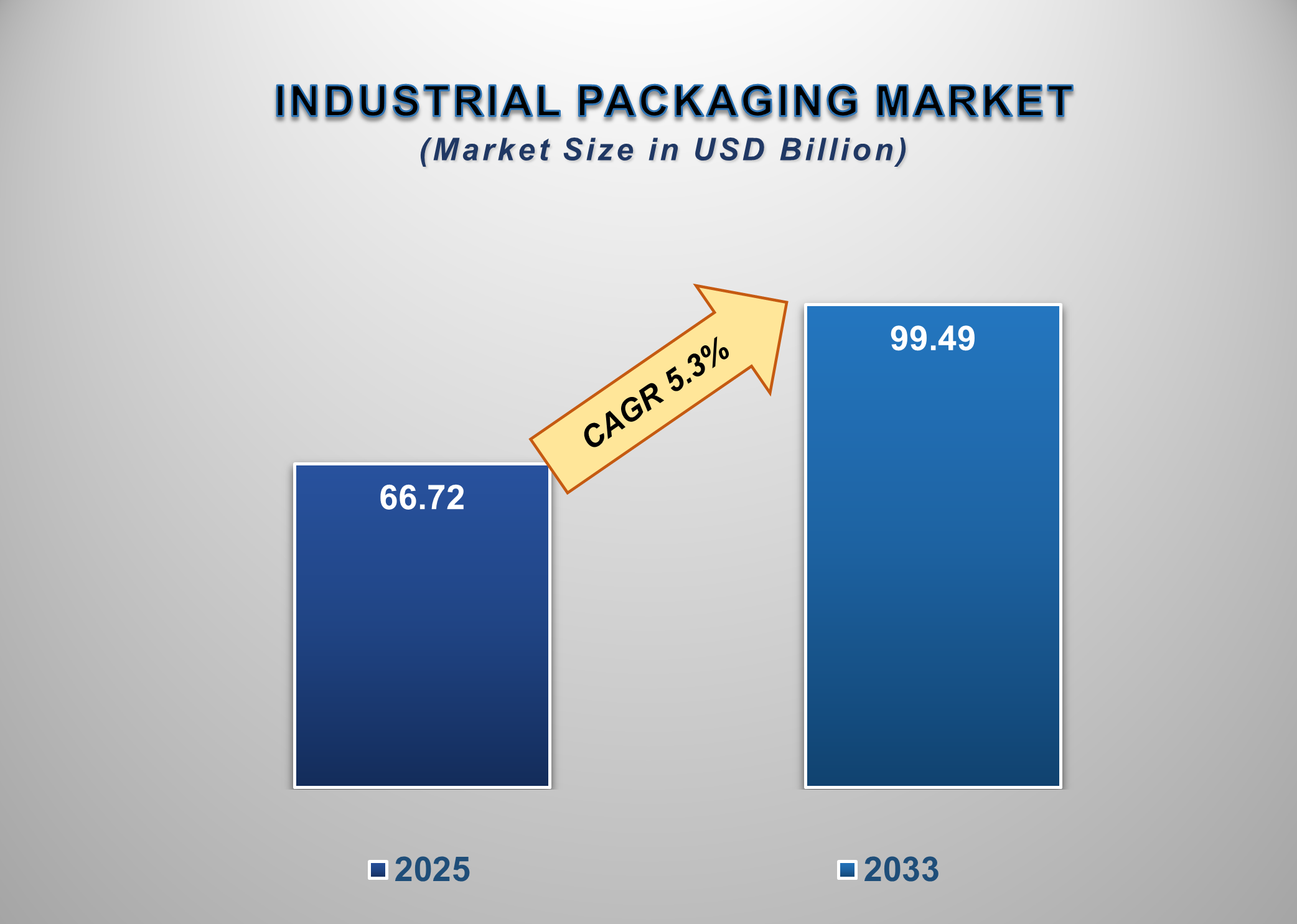

product costs. Valued at USD 66.72 billion in 2025, the market is

projected to reach USD 99.49 billion by 2033, growing at a CAGR of 5.3% during

the forecast period.

The market for industrial packaging is

essential to global supply chains because it makes it possible for bulk raw

materials, semi-finished commodities, and finished industrial products to be

handled, stored, and transported safely. In a variety of industries, including

chemicals, pharmaceuticals, food and beverage, construction, agriculture, and

oil and gas, industrial packaging solutions are made to withstand difficult

handling circumstances, shield contents from contamination or damage, and

adhere to safety and regulatory requirements.

The market includes a variety of packaging

styles made of materials like plastics, metals, paperboard, and wood, such as

drums, pails, sacks (FIBCs), intermediate bulk containers (IBCs), and

crates/totes. Sacks predominate in dry bulk applications, but drums and IBCs

make up a significant proportion of these due to their widespread use in the

transportation of liquids and hazardous goods. As companies aim for

sustainability and economic effectiveness, reusable and returnable packaging

technologies are becoming more and more popular.

Growing industrial production, increased

international trade, and the rising need for bulk packaging solutions that

boost logistics effectiveness are the main drivers of the industrial packaging

market's growth. Demand has been further increased by emerging economies' rapid

industrialization, especially in the Asia-Pacific. Simultaneously, the adoption

of standardized, high-performance packaging is supported by regulations

pertaining to the safe handling of chemicals and dangerous materials.

Sustainability is now a major market trend. Manufacturers are investing in

lightweight designs, recyclable materials, reconditioned containers, and

closed-loop packaging technologies to lessen their influence on the environment

and achieve business sustainability objectives. Product value is also being

increased by technological innovations like smart IBCs, track-and-trace

capabilities, and better barrier qualities. As a result, the industrial

packaging market is anticipated to rise steadily over the next ten years because

of industrial expansion, material and design innovation, and an increasing

focus on sustainability, efficiency, and safety throughout international supply

chains.

Industrial

Packaging Market Drivers and Opportunities

Growth in E-Commerce and Global Trade

The rapid expansion of international trade and e-commerce has significantly increased the demand for industrial packaging solutions. Industrial packaging, including pallets, crates, intermediate bulk containers (IBCs), and corrugated bulk boxes, ensures the safe handling, storage, and transportation of heavy or bulky goods. To minimize damage and logistical losses, cross-border trade in chemicals, automotive components, electronics, and FMCG products requires durable and standardized packaging. For example, companies such as Amazon use bulk industrial packaging formats in fulfillment centers to streamline distribution processes. The automotive industry also relies on returnable pallets and heavy-duty containers for global supply chains. As global supply networks become increasingly complex, the need for cost-effective, efficient, and protective industrial packaging continues to grow.

Expansion of Manufacturing and Chemical Industries

The expansion of manufacturing industries, including chemicals, pharmaceuticals, food processing, and construction materials, is a key driver of the industrial packaging market. Bulk chemicals, lubricants, paints, and food ingredients require specialized packaging such as steel drums, rigid plastic containers, and IBC tanks to ensure safety and regulatory compliance. For instance, multinational chemical manufacturers like BASF use high-strength industrial drums and containers to transport hazardous materials globally. Rising industrial output in emerging economies across Asia-Pacific and Latin America is further driving demand for large-capacity and durable packaging formats. Additionally, stringent regulations related to hazardous material handling and product safety are encouraging manufacturers to invest in certified and standardized industrial packaging solutions.

Rising Demand for Sustainable and Reusable Packaging

Sustainability initiatives present significant growth opportunities in the industrial packaging market. Increasing environmental regulations and corporate ESG commitments are encouraging companies to adopt recyclable, reusable, and lightweight packaging materials. Reusable transit packaging (RTP), such as foldable crates and returnable pallets, reduces long-term logistics costs and carbon emissions. For example, CHEP operates a global pallet pooling system that promotes circular packaging usage across various industries. Companies are also investing in recycled plastics and biodegradable materials to meet sustainability targets. As industries strive to reduce packaging waste and enhance supply chain efficiency, demand for innovative and environmentally friendly industrial packaging solutions is expected to increase substantially in the coming years.

Industrial Packaging Market Scope

|

Report Attributes |

Description |

|

Market Size in

2025 |

USD 66.72

Billion |

|

Market Forecast

in 2033 |

USD 99.49

Billion |

|

CAGR % 2025-2033 |

5.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Comprehensive,

data-driven analysis of the global Industrial Packaging market, offering

market size and forecast assessments, segmented insights by product type,

material, and application, along with regional and country-level dynamics.

The study includes detailed evaluations of market performance, competitive

landscape, technological trends, growth drivers, challenges, opportunities,

and strategic recommendations for packaging manufacturers, distributors,

end-users, investors, regulators, and supply chain stakeholders |

|

Segments Covered |

●

By

Product Type ●

By

Material ●

By

Application |

|

Regional Scope |

●

North

America ●

Europe ●

APAC ●

Latin

America ●

Middle

East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada

3)

U.K. 4)

Germany

5)

France

6)

Italy 7)

Spain 8)

Switzerland

9)

China

10)

India

11)

Japan 12)

South

Korea 13)

Australia 14)

Mexico

15)

Brazil

16)

Argentina

17)

Saudi

Arabia 18)

UAE 19)

South

Africa |

Industrial

Packaging Market Report Segmentation Analysis

The global

Industrial Packaging Market analysis is segmented by Product Type, Material,

Application, and Region.

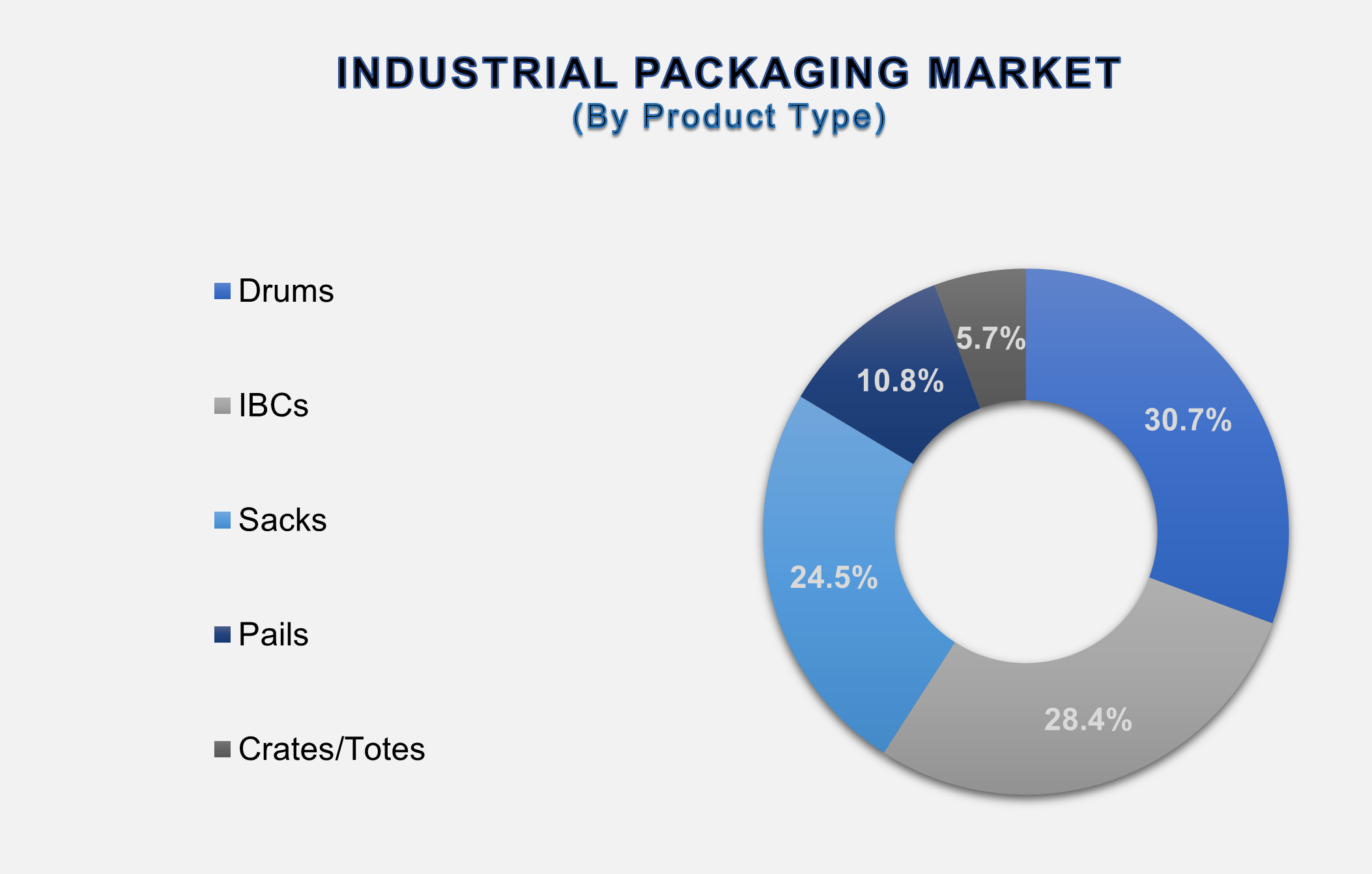

The Crates/Totes

segment dominated the market in 2025 and is projected to grow at the highest

CAGR during the forecast period.

By Product Type, the industrial packaging market is segmented into drums, IBCs, sacks, pails, and crates/totes. The crates/totes segment accounts for the largest share of the global industrial packaging market. The handling, storage, and transportation of solid and semi-finished items are the main uses for crates and totes, which are crucial parts of the industrial packaging industry. Usually made of metal, plastic, or wood, these containers are made to withstand continuous usage in harsh industrial settings and to be stackable. The automotive, industrial, food processing, logistics, and warehousing industries all make extensive use of crates and totes. By lowering the waste from single-use packaging, its reusable nature promotes sustainability and cost-effectiveness objectives. The use of crates and totes in contemporary industrial supply chains is being further propelled by an increasing focus on returnable packaging technologies, effective material handling, and automated logistics.

Plastic Platforms

holds the highest share of the Material Segment over the forecast period

Based on Material, the market is bifurcated into paperboard, plastic,

metal, wood, and fiber. The plastic platforms segment accounts for the largest

share of the market since plastic platforms are strong, lightweight, and

resistant to corrosion, moisture, and chemicals. The plastic platforms offer

sturdy support for drums, IBCs, sacks, and boxes during storage and transit and

are frequently utilized as pallets, modular platforms, and load bases. Plastic

platforms are appropriate for food, pharmaceutical, and chemical applications

because they have a longer service life, consistent dimensions, and better

hygiene than their wood and metal counterparts. Their interoperability with

automated handling systems improves efficiency throughout contemporary industrial

supply chains, and their recyclable and reusable nature supports environmental

initiatives.

The Chemical

and Pharmaceuticals Segment will probably dominate the market during the

forecast period

In terms of

Application, the industrial packaging market is segmented into chemicals and

pharmaceuticals, building and construction, oil and lubricant, agriculture and

horticulture, and others. The chemical and pharmaceutical segment holds the

largest share of the Industrial packaging market. Strict safety, hygienic, and

regulatory requirements make the chemicals and pharmaceuticals industry one of

the biggest end consumers of industrial packaging. Bulk formulations, active

pharmaceutical ingredients (APIs), intermediates, and hazardous chemicals are

frequently stored and transported using packaging options such as drums, IBCs,

and high-performance bags. Growing chemical output, increased pharmaceutical

manufacture, and international trading of restricted chemicals all contribute

to demand. Adoption of certified, high-barrier, reusable industrial packaging

solutions is expanding due to important features such as product integrity,

contamination prevention, and compliance with international standards.

The following

segments are part of an in-depth analysis of the global Industrial packaging

market:

|

Market Segments |

|

|

By

Product Type |

●

Drums ●

IBCs ●

Sacks ●

Pails ●

Crates/Totes |

|

By

Material |

●

Paperboard ●

Plastic ●

Metal ●

Wood ●

Fiber |

|

By

Application |

●

Chemicals

and Pharmaceuticals ●

Building

and Construction ●

Food and

Beverages ●

Oil and

Lubricants ●

Agriculture

and Horticulture ●

Others |

Industrial Packaging Market Share Analysis

by Region

The Asia-Pacific

region is projected to hold the largest share of the global industrial

packaging market over the forecast period.

The

Asia-Pacific region is projected to hold the largest share of the global

industrial packaging market over the forecast period and is also expected to be

the fastest-growing region due to its rapid industrialization, growing

manufacturing bases, and robust export activity. The expansion of chemicals, pharmaceuticals, food processing,

and building materials has led to significant contributions from nations like

South Korea, China, India, and Japan. For instance, India's pharmaceutical and

agrochemical industries support the growing usage of FIBCs and plastic

containers, while China's sizable chemical and petrochemical industries fuel

the country's high demand for drums and IBCs. Due to manufacturing relocation

and foreign direct investment, demand is increasing in Southeast Asian

economies, such as Vietnam and Indonesia. Infrastructure development,

cost-competitive production, and supportive government policies all contribute

to the expansion of regional markets.

Global

Industrial Packaging Market Recent Developments News:

●

In March 2024,

Mauser collaborated with RIKUTEC to create sustainable reusable IBCs (1,000 L)

manufactured from recycled plastics to advance circular economy activities.

●

In February

2024, Israeli liquid packaging manufacturer Aran Group purchased IBA Germany to

increase its IBC manufacturing and market share in Europe.

●

In March 2024,

a modified GCUBE IBC Flex for safe handling of delicate liquid materials was

jointly introduced by Greif and CDF Corporation.

●

In April 2024,

International Paper strengthened its Asia-Pacific expertise in food,

electronics, and chemical packaging by acquiring a South Korean packaging

company.

●

In May 2024,

Time Technoplast unveiled biodegradable bulk containers tailored for

pharmaceutical applications to meet sustainability and regulatory demands.

The Global Industrial packaging market is dominated by a few large

companies, such as

●

Greif, Inc.

●

Mauser

Packaging Solutions

●

Berry Global,

Inc.

●

Amcor plc

●

Mondi Group

●

Sonoco

Products Company

●

International

Paper

●

WestRock

Company

●

Sigma Plastics

Group

●

Orora Limited

●

SCHÜTZ GmbH

& Co. KGaA

●

Time

Technoplast Ltd.

●

Snyder

Industries

●

Chem-Tainer

Industries

●

Balmer Lawrie

& Co. Ltd.

●

Cleveland

Steel Container

●

Hoover

Container Solutions

●

LC Packaging

●

Qbig Packaging

B.V.

● Composite Containers LLC

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1.

Global Industrial Packaging Market Introduction and Market

Overview

1.1.

Objectives of the Study

1.2.

Global Industrial Packaging Market Scope and Market Estimation

1.2.1.Global Industrial

Packaging Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Industrial

Packaging Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market Segmentation

1.3.1.Product Type

of Global Industrial Packaging Market

1.3.2.Material of

Global Industrial Packaging Market

1.3.3.Application of

Global Industrial Packaging Market

1.3.4.Region of

Global Industrial Packaging Market

2.

Executive

Summary

2.1.

Demand Side Trends

2.2.

Key Market Trends

2.3.

Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand and Opportunity Assessment

2.5.

Market Dynamics

2.5.1.Drivers

2.5.2.Limitations

2.5.3.Opportunities

2.5.4.Impact

Analysis of Drivers and Restraints

2.6.

Porter’s Five Forces Analysis

2.7.

PEST Analysis

2.8.

Key Regulation

2.9.

Key Developments

2.10. Value

Chain / Ecosystem Analysis

3.

Global

Industrial Packaging Market Estimates & Historical Trend Analysis (2020 - 2024)

4. Global Industrial Packaging Market Estimates & Forecast Trend Analysis, by Product Type

4.1.

Global Industrial Packaging Market Revenue (US$ Bn) Estimates and

Forecasts, by Product Type, 2020 - 2033

4.1.1.Drums

4.1.2.IBCs

4.1.3.Sacks

4.1.4.Pails

4.1.5.Crates/Totes

5. Global Industrial Packaging Market Estimates & Forecast Trend Analysis, by Material

5.1.

Global Industrial Packaging Market Revenue (US$ Bn) Estimates and

Forecasts, by Material, 2020 - 2033

5.1.1.Paperboard

5.1.2.Plastic

5.1.3.Metal

5.1.4.Wood

5.1.5.Fiber

6. Global Industrial Packaging Market Estimates & Forecast Trend Analysis, by Application

6.1.

Global Industrial Packaging Market Revenue (US$ Bn) Estimates and

Forecasts, by Application, 2020 - 2033

6.1.1.Chemical and

Pharmaceuticals

6.1.2.Building and

Construction

6.1.3.Food and

Beverages

6.1.4.Oil and

Lubricants

6.1.5.Agriculture

and Horticulture

6.1.6.Others

7.

Global

Industrial Packaging Market Estimates & Forecast Trend Analysis, by Region

7.1.

Global Industrial Packaging Market Revenue (US$ Bn) Estimates and

Forecasts, by Region, 2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East

& Africa

7.1.5.Latin America

8.

North America Industrial

Packaging Market: Estimates &

Forecast Trend Analysis

8.1.

North America Industrial Packaging Market Assessments & Key

Findings

8.1.1.North America

Industrial Packaging Market Introduction

8.1.2.North America

Industrial Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product Type

8.1.2.2. By Material

8.1.2.3. By Application

8.1.2.4.

By Country

8.1.2.4.1.

The U.S.

8.1.2.4.2.

Canada

9.

Europe Industrial

Packaging Market: Estimates &

Forecast Trend Analysis

9.1.

Europe Industrial Packaging Market Assessments & Key Findings

9.1.1.Europe Industrial

Packaging Market Introduction

9.1.2.Europe Industrial

Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product Type

9.1.2.2. By Material

9.1.2.3. By Application

9.1.2.4. By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Russia

9.1.2.4.7.

Rest

of Europe

10.

Asia Pacific Industrial

Packaging Market: Estimates &

Forecast Trend Analysis

10.1. Asia

Pacific Industrial Packaging Market Assessments & Key Findings

10.1.1.

Asia Pacific Industrial Packaging Market Introduction

10.1.2.

Asia Pacific Industrial Packaging Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

10.1.2.1. By Product Type

10.1.2.2. By Material

10.1.2.3. By Application

10.1.2.4.

By Country

10.1.2.4.1.

China

10.1.2.4.2.

Japan

10.1.2.4.3.

India

10.1.2.4.4.

Australia

10.1.2.4.5.

South Korea

10.1.2.4.6. Rest

of Asia Pacific

11.

Middle East & Africa Industrial Packaging Market:

Estimates & Forecast Trend Analysis

11.1. Middle

East & Africa Industrial Packaging Market Assessments & Key Findings

11.1.1.

Middle East & Africa Industrial

Packaging Market Introduction

11.1.2.

Middle East & Africa Industrial

Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product Type

11.1.2.2. By Material

11.1.2.3. By Application

11.1.2.4.

By Country

11.1.2.4.1.

UAE

11.1.2.4.2.

Saudi Arabia

11.1.2.4.3.

South Africa

11.1.2.4.4. Rest of MEA

12.

Latin America Industrial

Packaging Market: Estimates &

Forecast Trend Analysis

12.1. Latin

America Event Industry Assessments & Key Findings

12.1.1.

Latin America Industrial Packaging Market Introduction

12.1.2.

Latin America Industrial Packaging Market Size Estimates and Forecast

(US$ Billion) (2020 - 2033)

12.1.2.1. By Product Type

12.1.2.2. By Material

12.1.2.3. By Application

12.1.2.4.

By Country

12.1.2.4.1.

Brazil

12.1.2.4.2.

Mexico

12.1.2.4.3.

Argentina

12.1.2.4.4. Rest of LATAM

13.

Country Wise Market: Introduction

14. Competition

Landscape

14.1. Global

Industrial Packaging Market Product Mapping

14.2. Global

Industrial Packaging Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3. Global

Industrial Packaging Market Tier Structure Analysis

14.4. Global

Industrial Packaging Market Concentration & Company Market Shares (%)

Analysis, 2024

15. Company

Profiles

15.1.

Greif, Inc.

15.1.1.

Company Overview & Key Stats

15.1.2.

Financial Performance & KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

15.2.

Mauser Packaging Solutions

15.3.

Berry Global, Inc.

15.4.

Amcor plc

15.5.

Mondi Group

15.6.

Sonoco Products Company

15.7.

International Paper

15.8.

WestRock Company

15.9.

Sigma Plastics Group

15.10.

Orora Limited

15.11.

SCHÜTZ GmbH & Co. KGaA

15.12.

Time Technoplast Ltd.

15.13.

Snyder Industries

15.14.

Chem-Tainer Industries

15.15.

Balmer Lawrie & Co. Ltd.

15.16.

Cleveland Steel Container

15.17.

Hoover Container Solutions

15.18.

LC Packaging

15.19.

Qbig Packaging B.V.

15.20.

Other Prominent Players

16.

Research

Methodology

16.1. External

Transportations / Databases

16.2. Internal

Proprietary Database

16.3. Primary

Research

16.4. Secondary

Research

16.5. Assumptions

16.6. Limitations

16.7. Report

FAQs

17.

Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables