Infectious Disease Diagnostics Market Size and Forecast (2025-2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product (Assays & Reagents, Instruments, Software); By Disease Type (Human Immunodeficiency Virus, Hepatitis, Influenza, Others); By Technology (Immunodiagnostics, Clinical Microbiology, Polymerase Chain Reaction, Next Generation Sequencing, Others); and Geography

2025-11-27

Healthcare

Swetal (Research Analyst)

Description

Infectious Disease Diagnostics Market Overview

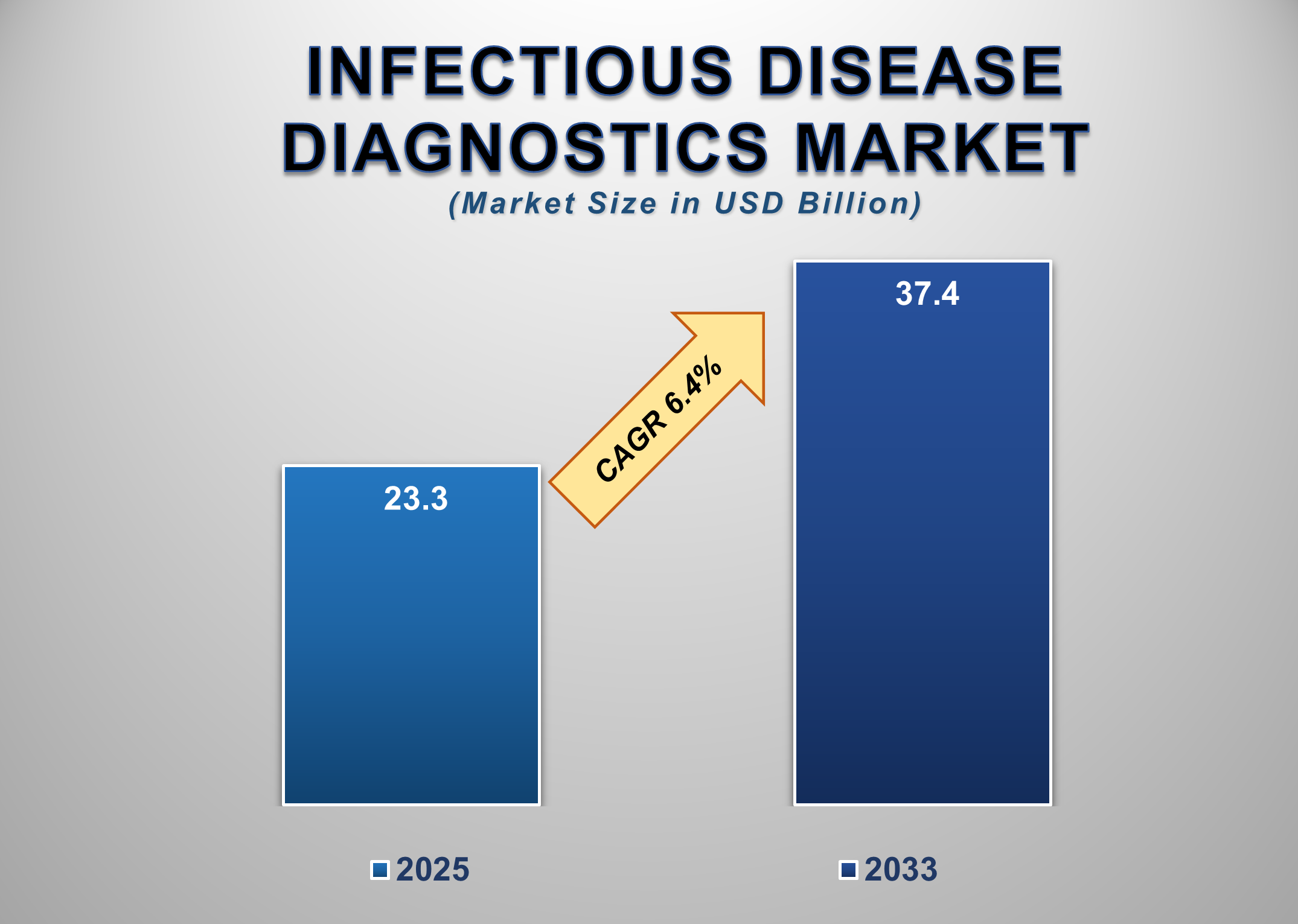

The Global Infectious Disease Diagnostics Market is witnessing robust growth, driven by the increasing prevalence of infectious diseases, rising global health awareness, and advancements in molecular diagnostic technologies. Valued at USD 23.3 billion in 2025, the market is projected to reach USD 37.4 billion by 2033, growing at a CAGR of 6.4% during the forecast period.

Infectious disease diagnostics

encompasses the testing and identification of pathogenic organisms such as

bacteria, viruses, fungi, and parasites in human samples. These diagnostics are

crucial for early detection, prevention, and management of diseases including

HIV, hepatitis, influenza, tuberculosis, and COVID-19. Growing global concerns

about emerging infectious threats, coupled with a strong focus on preparedness

and surveillance, have significantly expanded the role of diagnostic testing in

healthcare systems.

Infectious Disease

Diagnostics Market Drivers and Opportunities

Widening Burden of Infectious Diseases and Expanded Screening

Programs Are Driving Market Growth

The persistent global burden of infectious diseases such as HIV,

hepatitis, and seasonal influenza continues to drive investments in

diagnostics. National screening programs, vaccination campaigns, and

surveillance efforts have increased testing volumes across public health

systems and private providers. Early detection and rapid diagnosis are critical

for controlling outbreaks and enabling timely treatment; this has resulted in

higher demand for validated assays and robust reagent kits. Additionally, efforts

to expand access to diagnostics in low- and middle-income countries through

donor-funded programs and public-private partnerships are increasing

utilization of standardized tests and point-of-care solutions. The resultant

scale-up of testing infrastructure is stimulating demand for instruments,

consumables, and integrated diagnostic workflows. As healthcare systems

prioritize preparedness and routine screening, the infectious disease

diagnostics market is expected to benefit from consistent demand and policy-backed

spending.

Rapid Adoption of Molecular and Point-of-Care Technologies Is

Accelerating Market Expansion

Technological advances, particularly in molecular diagnostics

(PCR) and point-of-care immunodiagnostics, are reshaping the infectious disease

testing landscape. PCR-based assays offer high sensitivity and specificity for

pathogen detection and are now widely used in centralized labs and near-patient

settings. Concurrently, improved immunodiagnostic rapid tests and multiplex

panels are enabling decentralized screening with immediate clinical utility.

The convergence of automation, microfluidics, and digital diagnostics

(including connected platforms and cloud-based reporting) is improving

throughput, reducing manual error, and enabling rapid epidemiological

surveillance. Additionally, adoption of next-generation sequencing (NGS) for

pathogen characterization and antimicrobial resistance surveillance is creating

new high-value use cases. These technological trends are prompting laboratories

and healthcare systems to upgrade equipment portfolios and adopt integrated

software solutions, driving overall market growth.

Integration of Diagnostics with Digital Health and

Surveillance Systems Presents Major Upside

The integration of infectious disease diagnostics with digital

health platforms, electronic health records (EHRs), and national surveillance

systems offers a significant growth opportunity. Real-time data flows from

diagnostic instruments and connected point-of-care devices enable faster public

health responses, automated case reporting, and better resource allocation

during outbreaks. Diagnostic companies that provide end-to-end solutions, assay

kits, instruments, and interoperable software are well-positioned to capture

incremental value by offering subscription or data analytics services. In

addition, expanding telehealth and remote testing models creates demand for

validated home-collection kits and companion diagnostics linked to laboratory

workflows. Investments in digital integration, regulatory-compliant data

pipelines, and analytics-driven decision support will create differentiated

offerings and open commercial models beyond traditional product sales.

Infectious Disease

Diagnostics Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 23.3 Billion |

|

Market Forecast in 2033 |

USD 37.4 Billion |

|

CAGR % 2025-2033 |

6.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Product ●

By Disease Type ●

By Technology |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Infectious Disease

Diagnostics Market Report Segmentation Analysis

The global Infectious Disease

Diagnostics Market is segmented by Product, by Disease Type, by Technology, and

by Region.

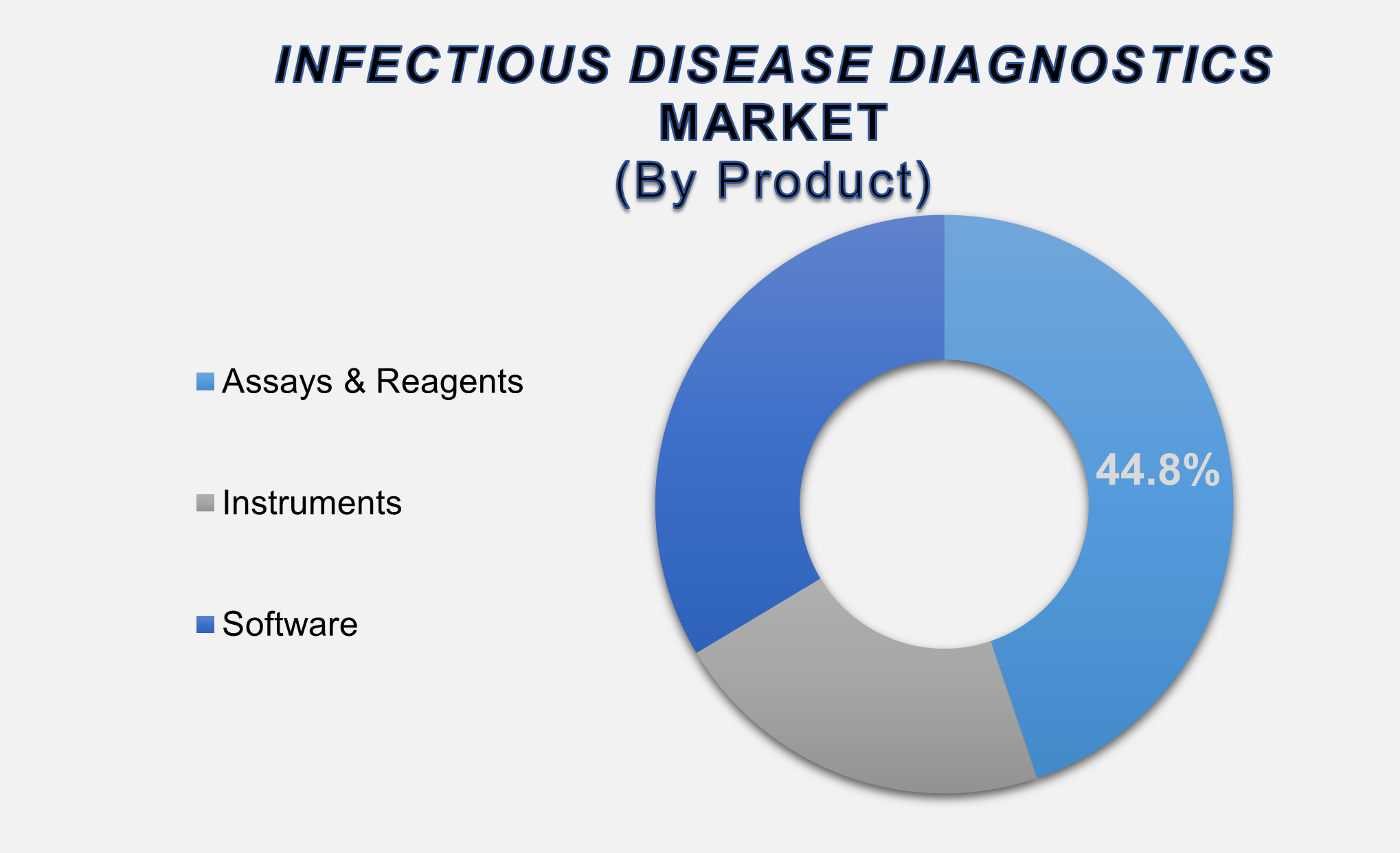

Assays & Reagents segment accounted for the largest

market share in the global Infectious Disease Diagnostics market

By

Product, the market is segmented into Assays & Reagents, Instruments,

Software, and Others. The Assays & Reagents segment accounted for the

largest share of the market in 2025 (approximately 44.8%), driven by high

demand for consumables required across centralized laboratories and

decentralized testing sites. Assays and reagent kits covering immunoassays, PCR

reagents, rapid antigen/antibody tests, and multiplex panels are recurring

revenue sources for diagnostic companies due to repeat testing and programmatic

screening needs. The segment benefits from continuous assay development

responding to emerging pathogens and strain variations, as well as from the

expanding use of multiplex panels for differential diagnosis. Given their clinically

critical role and recurring purchasing cycles, assays

& reagents are expected to remain the most significant revenue contributor.

The Human

Immunodeficiency Virus (HIV) segment holds a major

share in the Infectious Disease Diagnostics market

By

Disease Type, the market is divided into Human

Immunodeficiency Virus (HIV), Hepatitis, Influenza, and Others. The HIV segment

holds the largest share in 2025 due to the persistent global burden of HIV/AIDS

and widespread implementation of screening programs. Continuous WHO and CDC

efforts to promote early diagnosis, antiretroviral therapy (ART) monitoring,

and viral load testing have strengthened this segment’s growth. Technological

progress in molecular and immunoassay-based detection has improved test

reliability and accessibility, particularly in low-resource regions.

Furthermore, self-testing kits and rapid diagnostic devices have expanded

patient reach, driving higher testing rates. As healthcare systems strive

toward achieving UNAIDS 95-95-95 targets, the demand for accurate, fast, and

user-friendly diagnostic solutions for HIV remains exceptionally strong.

The Immunodiagnostics technology segment leads the global Infectious Disease

Diagnostics market

By

Technology, the market is segmented into Immunodiagnostics, Clinical

Microbiology, Polymerase Chain Reaction (PCR), Next Generation Sequencing

(NGS), and Others.

The Immunodiagnostics segment dominates the market and is widely used for detecting infectious agents through

antigen-antibody interactions. Its reliability, cost-effectiveness, and high

throughput make it the preferred choice in clinical laboratories and

point-of-care settings. Techniques such as enzyme immunoassays (EIA),

chemiluminescence assays (CLIA), and lateral flow assays are key components in

detecting diseases like HIV, hepatitis, and influenza. Advances in automation

and integration with digital analyzers have further improved assay accuracy and

turnaround times. The versatility of immunodiagnostic platforms across multiple

sample types, combined with the rapid response

to emerging pathogens, ensures their continued leadership in the infectious

disease diagnostics market.

The following segments are

part of an in-depth analysis of the global Infectious Disease Diagnostics

market:

|

Market Segments |

|

|

By Component |

●

Assays &

Reagents ●

Instruments ●

Software |

|

By Technology |

●

Immunodiagnostics ●

Clinical

Microbiology ●

Polymerase Chain

Reaction ●

Next-Generation

Sequencing ●

Others |

|

By Disease

Type |

●

Human

Immunodeficiency Virus ●

Hepatitis ●

Influenza ●

Others |

Infectious Disease

Diagnostics Market Share Analysis by Region

The Asia

Pacific region is projected to hold the largest share of the global Infectious

Disease Diagnostics market over the forecast period

The

Asia Pacific (APAC) region held the largest share of 39.4% in 2025 and is

expected to maintain its dominance during the forecast period. The region’s

growth is fueled by high infection prevalence, growing healthcare expenditure,

and rapid adoption of advanced diagnostic technologies. Governments in China,

India, and Japan are actively expanding infectious disease control programs,

vaccination initiatives, and diagnostic infrastructure to strengthen pandemic

preparedness and surveillance. The region’s large population base and increased

accessibility to affordable testing kits further drive market demand. Local

manufacturing initiatives and collaborations with global diagnostic companies

have also accelerated innovation and availability.

Meanwhile,

North America is expected to record the fastest growth rate, supported by

continuous R&D investments, well-established healthcare infrastructure, and

the presence of leading diagnostic firms. Strong regulatory frameworks,

government funding, and the early adoption of molecular and digital diagnostic

platforms position North America as a key growth engine in the coming years.

Infectious Disease

Diagnostics Market Competition Landscape Analysis

The global infectious disease

diagnostics market is highly competitive, characterized by innovation-driven

strategies, product diversification, and extensive R&D investments. Key

players focus on developing rapid, high-accuracy diagnostic solutions while

expanding their global distribution networks.

Global Infectious Disease

Diagnostics Market Recent Developments News:

- In March

2025, DiaSorin received

U.S. FDA 510(k) clearance for the LIAISON PLEX platform and its inaugural

test, the LIAISON PLEX® Respiratory Flex Assay. The multiplex platform is

designed to streamline and enhance respiratory infection testing,

supporting efficient and accurate diagnostic workflows.

- In April 2025,

BD (Becton, Dickinson and Company) secured U.S. FDA 510(k) clearance

for its Respiratory Viral Panel (RVP) on the BD MAX™ System. The panel

enables the simultaneous detection and differentiation of Influenza A,

Influenza B, SARS-CoV-2, and Respiratory Syncytial Virus (RSV), providing

rapid, high-throughput results to aid in the management of respiratory

infections.

The Global Infectious Disease

Diagnostics Market Is Dominated by a Few Large Companies, such as

●

Roche Diagnostics

●

Abbott Laboratories

●

Thermo Fisher

Scientific

●

bioMérieux

●

BD

●

Danaher

●

Siemens Healthineers

●

Qiagen

●

Hologic

●

Cepheid

●

Sysmex Corporation

●

Bio-Rad Laboratories

●

DiaSorin

●

Luminex Corporation

●

QuidelOrtho

●

GenMark Diagnostics

●

Mesa Biotech

●

Seegene

●

Ellume

●

Guangzhou Wondfo

Biotech

● Others

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Infectious Disease

Diagnostics Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Infectious Disease Diagnostics Market Scope and Market Estimation

1.2.1.Global Infectious Disease

Diagnostics Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.Global Infectious Disease

Diagnostics Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Infectious

Disease Diagnostics Market

1.3.2.Technology of Global Infectious

Disease Diagnostics Market

1.3.3.Disease Type of Global Infectious

Disease Diagnostics Market

1.3.4.Region of Global Infectious

Disease Diagnostics Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Infectious Disease Diagnostics Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Infectious Disease Diagnostics Market

Estimates & Historical Trend Analysis (2020 - 2024)

4.

Global Infectious Disease

Diagnostics Market Estimates

& Forecast Trend Analysis, by Product

4.1.

Global

Infectious Disease Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts,

by Product, 2020 - 2033

4.1.1.Assays & Reagents

4.1.2.Instruments

4.1.3.Software

5.

Global Infectious Disease

Diagnostics Market Estimates

& Forecast Trend Analysis, by Technology

5.1.

Global

Infectious Disease Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts,

by Technology, 2020 - 2033

5.1.1.Immunodiagnostics

5.1.2.Clinical Microbiology

5.1.3.Polymerase Chain Reaction

5.1.4.Next Generation Sequencing

5.1.5.Others

6.

Global Infectious Disease

Diagnostics Market Estimates

& Forecast Trend Analysis, by Disease Type

6.1.

Global

Infectious Disease Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts,

by Disease Type, 2020 - 2033

6.1.1.Human Immunodeficiency

Virus

6.1.2.Hepatitis

6.1.3.Influenza

6.1.4.Others

7. Global

Infectious Disease Diagnostics Market

Estimates & Forecast Trend Analysis, by region

1.1.

Global

Infectious Disease Diagnostics Market Revenue (US$ Bn) Estimates and Forecasts,

by region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Infectious

Disease Diagnostics Market: Estimates

& Forecast Trend Analysis

8.1. North America Infectious

Disease Diagnostics Market Assessments & Key Findings

8.1.1.North America Infectious

Disease Diagnostics Market Introduction

8.1.2.North America Infectious

Disease Diagnostics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

8.1.2.2. By Technology

8.1.2.3. By Disease

Type

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Infectious

Disease Diagnostics Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Infectious Disease Diagnostics Market Assessments & Key Findings

9.1.1.Europe Infectious Disease

Diagnostics Market Introduction

9.1.2.Europe Infectious Disease

Diagnostics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

9.1.2.2. By Technology

9.1.2.3. By Disease

Type

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Infectious

Disease Diagnostics Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Infectious Disease Diagnostics Market Introduction

10.1.2.

Asia

Pacific Infectious Disease Diagnostics Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Product

10.1.2.2. By Technology

10.1.2.3. By Disease

Type

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Infectious

Disease Diagnostics Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Infectious Disease Diagnostics

Market Introduction

11.1.2.

Middle East & Africa Infectious Disease Diagnostics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

11.1.2.2. By Technology

11.1.2.3. By Disease

Type

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Infectious Disease Diagnostics Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Infectious Disease Diagnostics Market Introduction

12.1.2.

Latin

America Infectious Disease Diagnostics Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Product

12.1.2.2. By Technology

12.1.2.3. By Disease

Type

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Infectious Disease Diagnostics Market Product Mapping

14.2.

Global

Infectious Disease Diagnostics Market Concentration Analysis, by Leading

Players / Innovators / Emerging Players / New Entrants

14.3.

Global

Infectious Disease Diagnostics Market Tier Structure Analysis

14.4.

Global

Infectious Disease Diagnostics Market Concentration & Company Market Shares

(%) Analysis, 2024

15.

Company

Profiles

15.1. Roche

Diagnostics

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Abbott

Laboratories

15.3. Thermo Fisher

Scientific

15.4. bioMérieux

15.5. BD

15.6. Danaher

15.7. Siemens

Healthineers

15.8. Qiagen

15.9. Hologic

15.10. Cepheid

15.11. Sysmex

Corporation

15.12. Bio-Rad

Laboratories

15.13. DiaSorin

15.14. Luminex

Corporation

15.15. QuidelOrtho

15.16. GenMark

Diagnostics

15.17. Mesa Biotech

15.18. Seegene

15.19. Ellume

15.20. Guangzhou

Wondfo Biotech

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables