Infertility Treatment Market Size and Forecast (2025–2033), Global and Regional Share, Trends, and Industry Analysis Report Coverage: By Product (Equipment, Media & Consumables, Accessories), By Procedure (Assisted Reproductive Technology, Artificial Insemination, Fertility Surgeries), By Patient Type (Female Infertility Treatment, Male Infertility Treatment), By End User (Fertility Centers, Hospitals & Surgical Clinics, Cryobanks, Research Institutes), and Geography

2025-12-18

Healthcare

Swetal (Research Analyst)

Description

Infertility

Treatment Market Overview

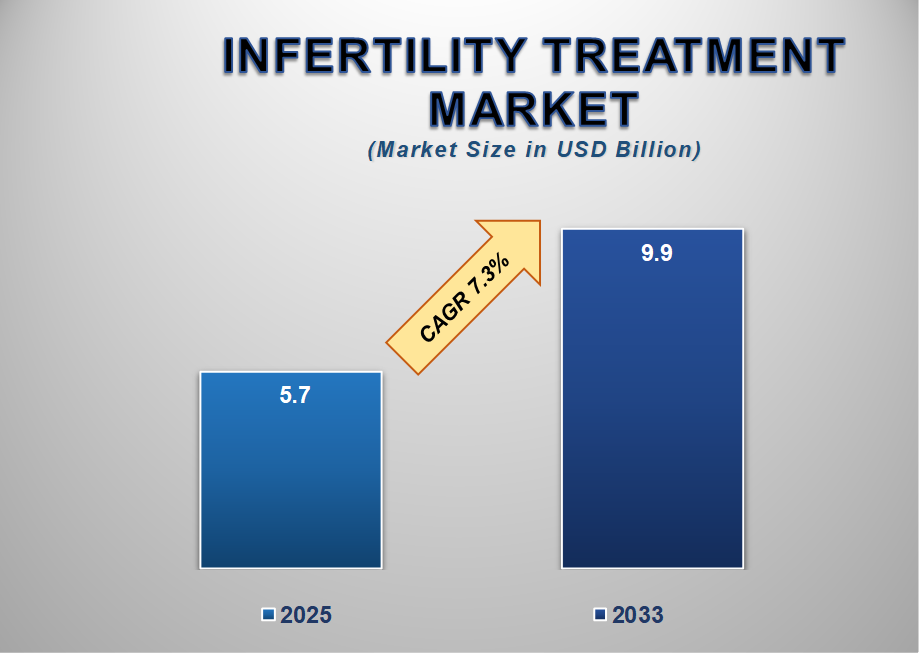

The Global Infertility Treatment Market Size is projected to increase from USD 5.7 billion in 2025 to USD 9.9 billion by 2033, growing at a CAGR of 7.3%. This growth is driven by rising infertility prevalence caused by lifestyle changes, delayed pregnancies, hormonal disorders, and growing awareness about reproductive health. Technological advancements in assisted reproductive technologies (ART), including improved embryo selection techniques, innovative sperm analysis systems, and high-precision ovum aspiration pumps, are supporting adoption in both developed and emerging markets.

The demand for higher success

rates in fertility procedures has pushed clinics and hospitals to adopt

advanced microscopes, incubators, and micromanipulator systems. The expansion

of fertility centers, increased medical tourism for IVF treatments, and reimbursement

improvements in countries such as the U.S., Japan, and parts of Europe further

support market growth. Meanwhile, growing investments by major pharmaceutical

and biotech companies in fertility drugs, specialized media, and consumables

are strengthening the overall treatment ecosystem.

Infertility

Treatment Market Drivers and Opportunities

Rising Infertility Rates and

Lifestyle Disorders Are Driving the Infertility Treatment Market Growth

Sedentary lifestyles, obesity,

stress, smoking, alcohol consumption, and hormonal imbalances have become

widespread globally, substantially increasing infertility rates in both men and

women. Polycystic ovary syndrome (PCOS), one of the most common causes of

female infertility, continues to rise sharply worldwide, contributing to a

heightened demand for ovulation induction, ICSI, and IVF procedures. In men,

issues such as declining sperm count, poor motility, and genetic abnormalities

are increasingly diagnosed due to improved sperm analyzer systems and advanced

imaging tools. Environmental pollution and exposure to endocrine-disrupting

chemicals have also been linked to deteriorating reproductive health. As these

conditions become more prevalent, couples are seeking timely diagnosis and

treatment, which is increasing the adoption of ART procedures, fertility

surgeries, and assisted insemination. Healthcare providers are also offering

personalized treatment plans based on patient-specific conditions, supported by

advanced lab technologies such as micromanipulators, incubators, and

cryopreservation systems.

Government programs promoting

awareness and early diagnosis of infertility are emerging as strong enablers of

market growth. As the number of affected individuals rises globally,

infertility treatment services are becoming a standard component of women’s and

men’s reproductive care.

Technological Advancements in

ART and Lab Equipment Are Strengthening Market Expansion

The infertility treatment

landscape has evolved significantly with rapid advancements in ART

technologies, laboratory equipment, and assisted reproduction methodologies.

High-resolution microscopes, precision micromanipulator systems, and AI-enabled

sperm analysis tools have enhanced fertility clinics’ ability to diagnose

infertility accurately and improve fertilization success rates. Similarly,

advanced incubators with controlled temperature and atmospheric conditions have

boosted embryo viability, while innovative cryosystems enable long-term storage

of gametes and embryos with minimal degradation.

Laser-assisted hatching,

time-lapse embryo imaging, and automated ovum aspiration pumps are further

improving procedural efficiency and outcomes. These developments have also

increased the global acceptance of fertility treatments, especially among couples

seeking higher success probabilities in their first treatment cycle.

Furthermore, gamete donation, surrogacy solutions, and minimally invasive

fertility surgeries have become more technologically sophisticated, allowing

clinicians to address complex infertility cases. As fertility centers

increasingly invest in modern laboratory environments, demand for consumables,

media, and accessories continues to rise. The integration of digital

technologies such as teleconsultation platforms and electronic patient records

enables more streamlined workflows, expanding the effectiveness of fertility

practices globally.

Emerging Fertility Tourism in

Asia-Pacific and Eastern Europe Is Creating Significant Market Opportunities

The expansion of fertility

tourism driven by cost advantages, advanced treatment availability, and

favorable regulatory environments represents a major growth opportunity for the

infertility treatment market. Asia-Pacific countries such as India, Thailand,

Malaysia, and Vietnam have become global hubs for IVF and ART procedures due to

lower treatment costs, highly skilled embryologists, and the presence of

world-class fertility centers. These countries attract patients from North

America, Europe, and the Middle East seeking affordable treatment options

without compromising success rates. Eastern Europe, including Ukraine, Georgia,

and the Czech Republic, has also emerged as a competitive destination for

surrogacy and IVF due to supportive legal frameworks and access to high-quality

procedures. Many clinics offer comprehensive treatment packages combining

surgical procedures, IVF cycles, embryo transfer, and donor programs, making

fertility tourism more accessible. This trend not only boosts the demand for

ART procedures but also increases the consumption of laboratory equipment,

imaging systems, consumables, and cryopreservation technologies. As more

countries establish specialized fertility zones and streamline medical visa

processes, fertility tourism is expected to accelerate significantly over the

next decade.

Infertility Treatment Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 5.7 Billion |

|

Market Forecast in 2033 |

USD 9.9 Billion |

|

CAGR % 2025-2033 |

7.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

Product,

Procedure, Patient Type, End User |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Infertility Treatment Market Report Segmentation Analysis

The Infertility Treatment Market

is segmented into Product, Procedure, Patient Type, End User, and region.

The Equipment Segment

Accounted for the Largest Market Share in the Global Infertility Treatment

Market

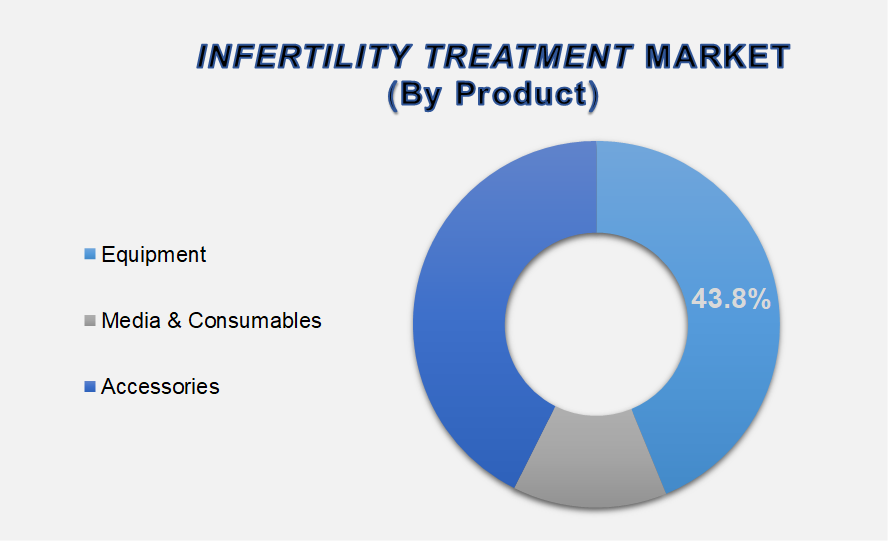

By Product, the market is segmented into Equipment, Microscopes, Imaging Systems, Sperm Analyzer Systems, Ovum Aspiration Pumps, Micromanipulator Systems, Incubators, Gas Analyzers, Laser Systems, Cryosystems, Sperm Separation Devices, Media & Consumables, and Accessories. The Equipment segment dominated the global infertility treatment market in 2025, holding the largest share due to the increasing adoption of advanced laboratory systems required for ART procedures. Growing demand for incubators, ovum aspiration pumps, and micromanipulation systems is driving this segment’s expansion, as fertility centers prioritize technologies that enhance embryo viability and fertilization success. The rising number of IVF cycles, increasing investments in fertility clinic infrastructure, and the need for high-efficiency lab environments are strengthening equipment usage. As clinics focus on improving clinical outcomes and reducing procedure time, the demand for technologically advanced equipment will continue to grow.

Assisted Reproductive

Technology Segment Held the Largest Market Share

By Procedure, the market is

segmented into Assisted Reproductive Technology, In Vitro Fertilization,

Intracytoplasmic Morphologically Selected Sperm Injection, Gamete Donation,

Intracytoplasmic Sperm Injection, Surrogacy, Artificial Insemination, Intrauterine

Insemination, Intracervical Insemination, Intratubal Insemination, and

Fertility Surgeries. The Assisted Reproductive Technology (ART) segment

accounted for the largest share in 2025, driven by the rising adoption of IVF,

ICSI, and related procedures as primary solutions for infertility.

ART offers higher success rates

and is widely recommended for both male and female infertility cases.

Advancements in embryo screening, cryopreservation, and micromanipulation

techniques further support ART adoption across fertility centers globally. Growing

medical tourism for IVF and the increasing availability of cost-effective ART

clinics in APAC and Eastern Europe are boosting this segment.

Female Infertility Treatment

Segment Led the Market

By

Patient Type, the market is segmented into Female Infertility Treatment and

Male Infertility Treatment. The Female Infertility Treatment segment held the

largest market share in 2025, attributed to the higher prevalence of PCOS,

ovulation disorders, age-related fertility decline, and fallopian tube

complications. Increasing awareness about reproductive health, rising adoption

of IVF and IUI procedures, and growing demand for hormonal therapies are

contributing to the dominance of this segment. Additionally, delayed

pregnancies due to career-oriented lifestyles are increasing infertility risks

among women, amplifying treatment adoption. The availability of advanced

diagnostic tools and personalized treatment protocols further supports growth.

The following segments are

part of an in-depth analysis of the global Infertility Treatment Market:

|

Market

Segments |

|

|

By Product |

●

Equipment o

Microscopes o

Imaging Systems o

Sperm Analyzer

Systems o

Ovum Aspiration

Pumps o

Micromanipulator

Systems o

Incubators o

Gas Analyzers o

Laser Systems o

Cryosystems o

Sperm Separation

Devices ●

Media &

Consumables ●

Accessories |

|

By Procedure |

●

Assisted

Reproductive Technology o

In Vitro

Fertilization o

Intracytoplasmic

Morphologically Selected Sperm Injection o

Gamete Donation o

Intracytoplasmic

Sperm Injection o

Surrogacy ●

Artificial

Insemination o

Intrauterine

Insemination o

Intracervical

Insemination o

Intratubal

Insemination ●

Fertility

Surgeries o

Laparoscopy o

Hysteroscopy o

Myomectomy o

Laparotomy o

Tubal Ligation

Reversal o

Varicocelectomy o

Microsurgical

Reconstruction o

Vasovasostomy o

Vasoepididymostomy ●

Other Infertility

Treatment Procedures |

|

By Patient

Type |

●

Female Infertility

Treatment ●

Male Infertility

Treatment |

|

By End User |

●

Fertility Centers ●

Hospitals &

Surgical Clinics ●

Cryobanks ●

Research Institutes |

Infertility

Treatment Market Share Analysis by Region

The North America region is

projected to hold the largest share of the global Infertility Treatment market

over the forecast period.

North America accounted for the

largest share of 40.6% in the global infertility treatment market in 2025. The

region’s dominance is supported by advanced healthcare infrastructure, high

infertility screening rates, widespread availability of ART clinics, and strong

insurance support for fertility treatments in select U.S. states. The presence

of major players, including Merck KGaA, Ferring Pharmaceuticals, and

CooperSurgical, further strengthens the market landscape. Increasing cases of

delayed parenthood and lifestyle-driven fertility decline continue to fuel

treatment demand across the U.S. and Canada.

Asia-Pacific is projected to grow

at the highest CAGR during the forecast period. Countries such as India, China,

Japan, South Korea, and Australia are witnessing the rapid expansion of IVF

centers, rising affordability, increasing fertility tourism, and improving

technological capabilities. Supportive government initiatives, reduced

treatment costs, and the availability of highly skilled fertility specialists

make APAC an emerging global hub for ART procedures. As awareness improves and

patient volumes increase, APAC is expected to significantly outpace other

regions.

Infertility Treatment Market Competition Landscape Analysis

The global

infertility treatment market is moderately competitive, with key players

focusing on expanding their ART portfolios, improving success rates, and

strengthening laboratory product offerings. Leading companies include Merck

KGaA, Ferring Pharmaceuticals, Merck & Co., Bayer AG, AbbVie, Thermo Fisher

Scientific, Vitrolife, Cook Medical, CooperSurgical, Irvine Scientific, Genea

Biomedx, Esco Micro, The Baker Company, IVFtech, Kitazato Corporation, Rocket

Medical, MediCult, and Nidacon International.

Global Infertility Treatment Market Recent Developments

News:

- In 2021, CooperSurgical

partnered with Virtus Health to enhance access to advanced fertility

technologies, expanding treatment options for couples experiencing

infertility through shared expertise and innovative solutions.

- In 2021, Hamilton Thorne Ltd.

received FDA approval and European market clearance for GYNEMED GM501, a

ready-to-use medium for washing and handling human oocytes and embryos

during in vitro fertilization (IVF) procedures.

The Global Infertility Treatment Market is dominated

by a few large companies, such as

●

Merck KGaA

●

Ferring

Pharmaceuticals

●

Merck & Co.

●

Bayer AG

●

AbbVie

●

Thermo Fisher

Scientific

●

Vitrolife

●

Cook Medical

●

CooperSurgical

●

Irvine Scientific

●

Genea Biomedx

●

Esco Micro

●

The Baker Company

●

IVFtech

●

Kitazato Corporation

●

Rocket Medical

●

MediCult

●

Nidacon International

●

Wallach Surgical

●

Gynotec

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Infertility

Treatment Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Infertility Treatment Market Scope and Market Estimation

1.2.1.Global Infertility

Treatment Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast

(2025 - 2033)

1.2.2.Global Infertility

Treatment Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Infertility

Treatment Market

1.3.2.Procedure of Global Infertility

Treatment Market

1.3.3.Patient Type of Global Infertility

Treatment Market

1.3.4.End-user of Global Infertility

Treatment Market

1.3.5.Region of Global Infertility

Treatment Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Infertility Treatment Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Infertility Treatment Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Infertility

Treatment Market Estimates

& Forecast Trend Analysis, by Product

4.1.

Global

Infertility Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Equipment

4.1.1.1.

Microscopes

4.1.1.2.

Imaging

Systems

4.1.1.3.

Sperm

Analyzer Systems

4.1.1.4.

Ovum

Aspiration Pumps

4.1.1.5.

Micromanipulator

Systems

4.1.1.6.

Incubators

4.1.1.7.

Gas

Analyzers

4.1.1.8.

Laser

Systems

4.1.1.9.

Cryosystems

4.1.1.10.

Sperm

Separation Devices

4.1.2.Media & Consumables

4.1.3.Accessories

5.

Global Infertility

Treatment Market Estimates

& Forecast Trend Analysis, by Procedure

5.1.

Global

Infertility Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Procedure,

2020 - 2033

5.1.1.Assisted Reproductive

Technology

5.1.1.1.

In

Vitro Fertilization

5.1.1.2.

Intracytoplasmic

Morphologically Selected Sperm Injection

5.1.1.3.

Gamete

Donation

5.1.1.4.

Intracytoplasmic

Sperm Injection

5.1.1.5.

Surrogacy

5.1.2.Artificial Insemination

5.1.2.1.

Intrauterine

Insemination

5.1.2.2.

Intracervical

Insemination

5.1.2.3.

Intratubal

Insemination

5.1.3. Fertility Surgeries

5.1.3.1.

Laparoscopy

5.1.3.2.

Hysteroscopy

5.1.3.3.

Myomectomy

5.1.3.4.

Laparotomy

5.1.3.5.

Tubal

Ligation Reversal

5.1.3.6.

Varicocelectomy

5.1.3.7.

Microsurgical

Reconstruction

5.1.3.8.

Vasovasostomy

5.1.3.9.

Vasoepididymostomy

5.1.4.Other Infertility

Treatment Procedures

6.

Global Infertility

Treatment Market Estimates

& Forecast Trend Analysis, by Patient Type

6.1.

Global

Infertility Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by Patient

Type, 2020 - 2033

6.1.1.Female Infertility

Treatment

6.1.2.Male Infertility Treatment

7.

Global Infertility

Treatment Market Estimates

& Forecast Trend Analysis, by End-user

7.1.

Global

Infertility Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

7.1.1.Fertility Centers

7.1.2.Hospitals & Surgical

Clinics

7.1.3.Cryobanks

7.1.4.Research Institutes

8. Global

Infertility Treatment Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Infertility Treatment Market Revenue (US$ Bn) Estimates and Forecasts, by

region, 2020 - 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

9. North America Infertility

Treatment Market: Estimates &

Forecast Trend Analysis

9.1.

North

America Infertility Treatment Market Assessments & Key Findings

9.1.1.North America Infertility

Treatment Market Introduction

9.1.2.North America Infertility

Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

9.1.2.2. By Procedure

9.1.2.3. By Patient

Type

9.1.2.4. By End-user

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Infertility

Treatment Market: Estimates &

Forecast Trend Analysis

10.1.

Europe

Infertility Treatment Market Assessments & Key Findings

10.1.1.

Europe

Infertility Treatment Market Introduction

10.1.2.

Europe

Infertility Treatment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

10.1.2.2. By Procedure

10.1.2.3. By Patient

Type

10.1.2.4. By End-user

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Infertility

Treatment Market: Estimates &

Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Infertility Treatment Market Introduction

11.1.2.

Asia

Pacific Infertility Treatment Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Product

11.1.2.2. By Procedure

11.1.2.3. By Patient

Type

11.1.2.4. By End-user

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Infertility

Treatment Market: Estimates &

Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Infertility Treatment Market

Introduction

12.1.2.

Middle East & Africa Infertility Treatment Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

12.1.2.2. By Procedure

12.1.2.3. By Patient

Type

12.1.2.4. By End-user

12.1.2.5.

By

Country

12.1.2.5.1. South

Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi

Arabia

12.1.2.5.4. Rest

of MEA

13. Latin America

Infertility Treatment Market: Estimates

& Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Infertility Treatment Market Introduction

13.1.2.

Latin

America Infertility Treatment Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

13.1.2.1. By Product

13.1.2.2. By Procedure

13.1.2.3. By Patient

Type

13.1.2.4. By End-user

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Infertility Treatment Market Product Mapping

15.2.

Global

Infertility Treatment Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

15.3.

Global

Infertility Treatment Market Tier Structure Analysis

15.4.

Global

Infertility Treatment Market Concentration & Company Market Shares (%)

Analysis, 2023

16.

Company

Profiles

16.1. Merck

KGaA

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2. Ferring

Pharmaceuticals

16.3. Merck &

Co.

16.4. Bayer AG

16.5. AbbVie

16.6. Thermo Fisher

Scientific

16.7. Vitrolife

16.8. Cook Medical

16.9. CooperSurgical

16.10. Irvine

Scientific

16.11. Genea Biomedx

16.12. Esco Micro

16.13. The Baker

Company

16.14. IVFtech

16.15. Kitazato

Corporation

16.16. Rocket

Medical

16.17. MediCult

16.18. Nidacon

International

16.19. Wallach

Surgical

16.20. Gynotec

16.21. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables