Inorganic Salts Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Application (Agriculture, Pharmaceuticals, Cement, Rubber Processing, Food, Others), By Type (Sodium Salts, Magnesium Salts, Calcium Salts, Potassium Salts, Ammonium Salts), and Geography

2026-02-02

Chemicals & Materials

Jaya Bundele (Research Analyst)

Description

Inorganic Salts Market Overview

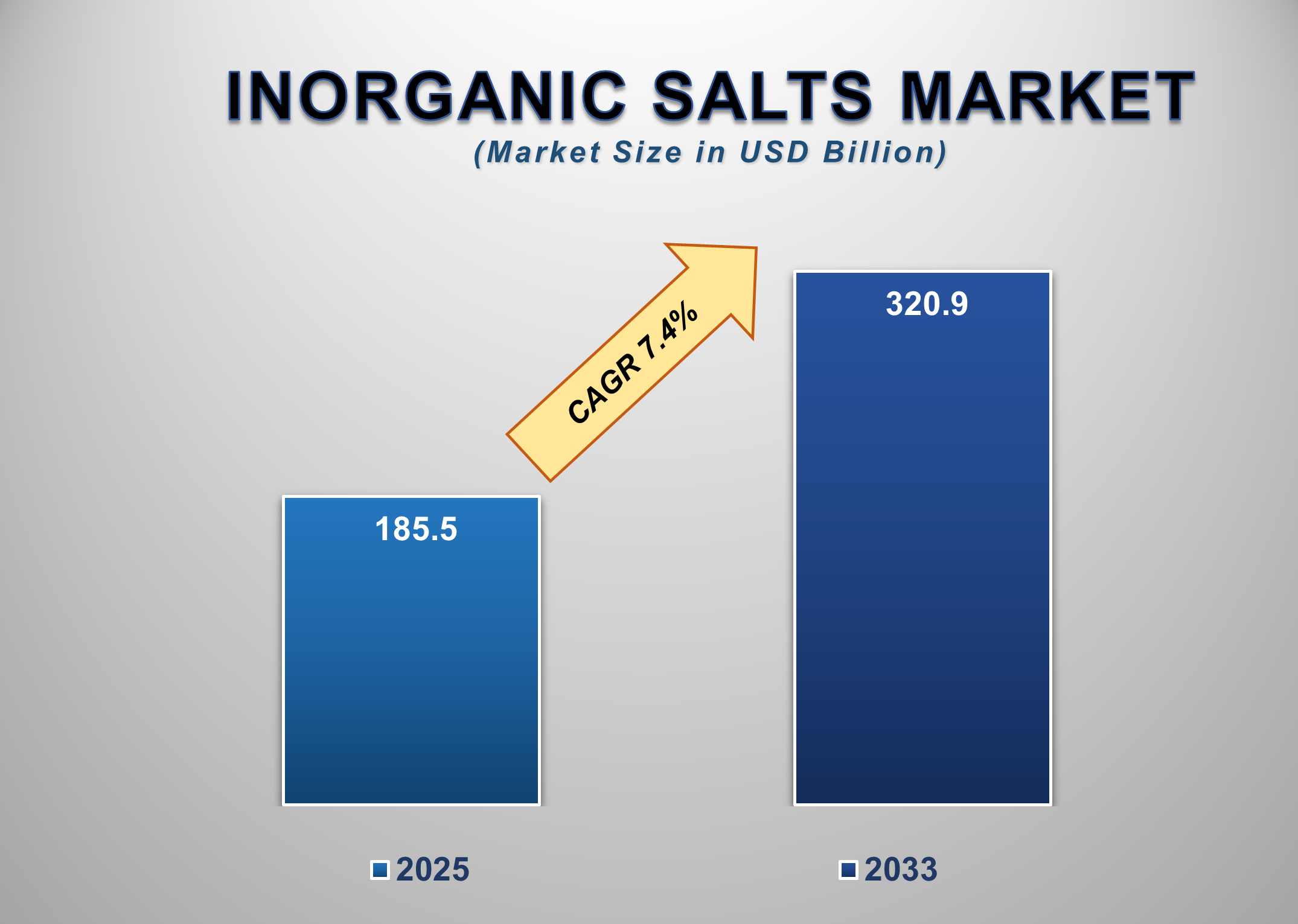

The global inorganic salts market represents a foundational segment of the chemical industry, supporting a wide spectrum of downstream applications ranging from agriculture and food processing to pharmaceuticals, construction, and rubber manufacturing. In 2025, the market is valued at USD 185.5 billion and is projected to reach USD 320.9 billion by 2033, expanding at a CAGR of 7.4% over the forecast period. This growth reflects the essential and non-substitutable role of inorganic salts across both industrial and consumer-facing value chains.

Inorganic salts such as sodium,

calcium, potassium, magnesium, and ammonium compounds are integral to nutrient

delivery, pH regulation, preservation, catalysis, and material strengthening.

Their demand remains resilient even during economic slowdowns due to their

widespread use in staple industries such as food production, fertilizers,

cement, and pharmaceuticals. Sodium salts, in particular, form the backbone of

the market owing to their extensive application across food, agriculture, and

industrial processing.

Inorganic Salts Market

Drivers and Opportunities

Expanding Agricultural and Food Production Is Driving Global

Demand for Inorganic Salts

Agriculture remains one of the most significant demand centers for

inorganic salts, particularly sodium, potassium, calcium, and ammonium

compounds used in fertilizers, soil conditioning, and crop nutrition. Rising

global population levels and increasing food security concerns are pushing

governments and agribusinesses to improve crop yields and farming efficiency,

directly boosting the consumption of inorganic salts. These compounds play a

critical role in nutrient replenishment, pH stabilization, and pest management,

making them indispensable in modern agriculture. Parallel to this, the food

processing industry relies heavily on inorganic salts for preservation, flavor

enhancement, texture control, and shelf-life extension. Sodium salts, in

particular, are extensively used across packaged foods, beverages, dairy

products, and meat processing. As urbanization accelerates and consumption of

processed and convenience foods rises, especially in the Asia Pacific, demand

for food-grade inorganic salts continues to grow steadily. This dual demand

from the agriculture and food sectors provides a strong and recurring growth

base for the market.

Growth of Construction, Cement, and Rubber Processing

Industries Is Supporting Market Expansion

The building and construction industry is another key driver of

inorganic salt demand, especially calcium and sodium-based compounds used in

cement manufacturing, concrete acceleration, and corrosion inhibition. Rapid

urban development, infrastructure investments, and housing projects across

emerging economies are significantly increasing cement production, thereby

driving the consumption of inorganic salts as essential input materials. In

addition, the rubber processing industry relies on inorganic salts for

vulcanization, stabilization, and performance enhancement of rubber products.

Applications span automotive tires, industrial belts, hoses, and seals. With

automotive production and industrial manufacturing expanding in the Asia

Pacific and North America, the use of inorganic salts in rubber processing is

gaining momentum. The non-discretionary nature of these applications ensures

consistent volume demand, reinforcing the market’s growth trajectory over the

forecast period.

Pharmaceutical and Specialty Applications Present High-Value

Growth Opportunities

While traditional applications dominate volume consumption, pharmaceuticals and specialty chemical applications represent a significant value-based growth opportunity for the inorganic salts market. Magnesium, calcium, and sodium salts are widely used in drug formulations, excipients, electrolyte solutions, and diagnostic agents. The global expansion of healthcare access, aging populations, and rising prevalence of chronic diseases are fueling demand for pharmaceutical-grade inorganic salts. Moreover, increasing regulatory emphasis on product purity and traceability is encouraging manufacturers to invest in high-quality and specialty-grade salt production. These premium segments offer higher margins compared to bulk industrial salts and are particularly prominent in North America and developed Asia Pacific markets. As pharmaceutical manufacturing scales up globally, inorganic salt suppliers with strong quality control and regulatory compliance capabilities are well-positioned to capture long-term growth opportunities

Inorganic Salts Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 185.5 Billion |

|

Market Forecast in 2033 |

USD 320.9 Billion |

|

CAGR % 2025-2033 |

7.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors

and more |

|

Segments Covered |

●

By Application,

By Type |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Inorganic Salts Market

Report Segmentation Analysis

The Global Inorganic Salts Market

Industry Analysis is segmented by Application and Type, and by Region.

Sodium Salts Segment Dominates Due to Broad Industrial and

Food Applications

The

sodium salts segment accounts for 30.8% of the global inorganic salts market,

making it the largest type segment. Sodium-based compounds are extensively used

across food processing, agriculture, pharmaceuticals, and industrial

manufacturing due to their chemical stability, cost-effectiveness, and

versatility. In the food industry, sodium salts are critical for preservation,

flavor enhancement, and texture modification, ensuring consistent demand from

packaged and processed food manufacturers.

Beyond food, sodium salts are widely used in agriculture for soil conditioning and nutrient delivery, as well as in chemical processing and water treatment. Their large-scale production capabilities and established supply chains further strengthen their market dominance. As food consumption and industrial output continue to rise globally, particularly in the Asia Pacific, sodium salts are expected to maintain their leading position throughout the forecast period.

Agriculture

Application Segment Benefits from Rising Global Food Demand

Agriculture

represents one of the most important application segments within the inorganic

salts market. Inorganic salts are essential components of fertilizers,

micronutrient blends, and soil enhancers that improve crop yield and quality.

Growing global food demand, coupled with shrinking arable land, has intensified

the need for efficient agricultural inputs, directly boosting inorganic salt

consumption. Emerging economies in the Asia

Pacific heavily rely on inorganic salts to support intensive farming practices

and enhance food self-sufficiency. Additionally,

government-backed agricultural productivity programs and fertilizer subsidies

further support market growth. The consistent requirement for crop nutrients

across multiple growing cycles ensures stable, recurring demand for inorganic

salts in this segment.

The following segments are

part of an in-depth analysis of the global Inorganic Salts market:

|

Market Segments |

|

|

By Application |

●

Sodium salts ●

Magnesium salts ●

Calcium salts ●

Potassium salts ●

Ammonium Salts |

|

By Type |

●

Agriculture ●

Pharmaceuticals ●

Cement ●

Rubber processing ●

Food ●

Others |

Inorganic Salts Market

Share Analysis by Region

Asia Pacific is

anticipated to hold the biggest portion of the Inorganic Salts Market globally

throughout the forecast period.

The Asia Pacific dominates the

global inorganic salts market, accounting for a 41.8% share, driven by its

massive agricultural base, rapidly expanding food processing industry, and

growing construction activity. Countries across the region rely heavily on

inorganic salts to support fertilizer production, cement manufacturing, and

large-scale industrial processing. The presence of cost-efficient manufacturing

facilities and abundant raw material availability further strengthens the

region’s leadership position.

North America is expected to

witness the fastest CAGR over the forecast period, supported by strong demand

from the pharmaceutical, food, and specialty chemical industries. The region’s

focus on high-purity, regulated-grade inorganic salts for healthcare and food

safety applications is driving value-based growth. Additionally, ongoing

investments in infrastructure and industrial modernization are contributing to

rising demand for calcium and sodium salts.

Inorganic Salts Market

Competition Landscape Analysis

The inorganic salts market is

moderately consolidated, with global chemical majors and regional producers

competing on scale, product quality, and application-specific expertise.

Leading companies focus on expanding production capacities, enhancing product

purity, and strengthening supply chains to serve diverse end-use industries.

Strategic investments in agriculture, food-grade, and pharmaceutical-grade

salts are key competitive priorities, particularly in high-growth regions such

as the Asia Pacific and North America.

Global Inorganic Salts

Market Recent Developments News:

- In September 2021 – Arkema announced a 15% price

increase for its hydrogen peroxide and sodium chlorate products, with the

new pricing becoming effective on October 1, 2021.

- In April 2021 – The K+S Group completed the

divestment of its Americas salts business (part of the Operating Unit

Americas) to a consortium comprising Stone Canyon Industries Holdings LLC

and Mark Demetree and Partners for a total price of USD 2.93 billion.

- In April 2020 – GFS Chemicals Inc. launched a new

corporate profile page and a redesigned e-commerce website to enhance its

digital presence and customer interface.

The Global Inorganic Salts Market

Is Dominated by a Few Large Companies, such as

●

BASF SE

●

Evonik Industries

●

AkzoNobel

●

Tata Chemicals

●

Solvay

●

Dow Chemical Company

●

Honeywell

●

Lanxess

●

Eastman Chemical

Company

●

Clariant

●

Celanese Corporation

●

Nouryon

●

K+S

●

ICL Group

●

Innophos Holdings

●

Tosoh Corporation

●

Sumitomo Chemical

●

Arkema

●

Gujarat Heavy

Chemicals

●

Chemours

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Inorganic Salts

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Inorganic Salts Market Scope and Market Estimation

1.2.1.Global Inorganic Salts Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Inorganic Salts

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Application of Global Inorganic

Salts Market

1.3.2.Type of Global Inorganic

Salts Market

1.3.3.Region of Global Inorganic

Salts Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Inorganic Salts Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Inorganic Salts Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Inorganic Salts Market Estimates

& Forecast Trend Analysis, by Application

4.1.

Global

Inorganic Salts Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

4.1.1.Sodium salts

4.1.2.Magnesium salts

4.1.3.Calcium salts

4.1.4.Potassium salts

4.1.5.Ammonium Salts

5. Global

Inorganic Salts Market Estimates

& Forecast Trend Analysis, by Type

5.1.

Global

Inorganic Salts Market Revenue (US$ Bn) Estimates and Forecasts, by Type, 2020

- 2033

5.1.1.Agriculture

5.1.2.Pharmaceuticals

5.1.3.Cement

5.1.4.Rubber processing

5.1.5.Food

5.1.6.Others

6. Global

Inorganic Salts Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Inorganic Salts Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Inorganic

Salts Market: Estimates & Forecast

Trend Analysis

7.1.

North

America Inorganic Salts Market Assessments & Key Findings

7.1.1.North America Inorganic

Salts Market Introduction

7.1.2.North America Inorganic

Salts Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Application

7.1.2.2. By Type

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Inorganic

Salts Market: Estimates & Forecast

Trend Analysis

8.1.

Europe

Inorganic Salts Market Assessments & Key Findings

8.1.1.Europe Inorganic Salts

Market Introduction

8.1.2.Europe Inorganic Salts

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Application

8.1.2.2. By Type

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Inorganic

Salts Market: Estimates & Forecast

Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Inorganic

Salts Market Introduction

9.1.2.Asia Pacific Inorganic

Salts Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Application

9.1.2.2. By Type

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Inorganic

Salts Market: Estimates & Forecast

Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Inorganic Salts Market Introduction

10.1.2.

Middle East & Africa Inorganic Salts Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Application

10.1.2.2. By Type

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Inorganic Salts Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Inorganic Salts Market Introduction

11.1.2.

Latin

America Inorganic Salts Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Application

11.1.2.2. By Type

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Inorganic Salts Market Product Mapping

13.2.

Global

Inorganic Salts Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

13.3.

Global

Inorganic Salts Market Tier Structure Analysis

13.4.

Global

Inorganic Salts Market Concentration & Company Market Shares (%) Analysis,

2024

14.

Company

Profiles

14.1.

BASF SE

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Evonik

Industries

14.3. AkzoNobel

14.4. Tata

Chemicals

14.5. Solvay

14.6. Dow

Chemical Company

14.7. Honeywell

14.8. Lanxess

14.9. Eastman

Chemical Company

14.10. Clariant

14.11. Celanese

Corporation

14.12. Nouryon

14.13. K+S

14.14. ICL

Group

14.15. Innophos

Holdings

14.16. Tosoh

Corporation

14.17. Sumitomo

Chemical

14.18. Arkema

14.19. Gujarat

Heavy Chemicals

14.20. Chemours

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables