Insulation Materials Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Material Type (Fiberglass, Mineral Wool, Plastic Foams [EPS, XPS, Polyurethane, Polyisocyanurate], Others); By Application (Residential Construction, Non-Residential Construction, Industrial, HVAC & Appliances and Others); By Form (Batts & Rolls, Boards, Loose-fill, Others)

2025-10-27

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Insulation Materials Market Overview

The insulation materials market size is projected to witness robust growth from 2025 to 2033, propelled by the escalating demand for energy-efficient buildings, stringent government regulations promoting green construction, and rising industrialization. Valued at approximately USD 68.5 billion in 2025, the market is expected to surge to USD 112.4 billion by 2033, reflecting a steady compound annual growth rate (CAGR) of 6.4% over the forecast period.

The insulation materials market

is experiencing significant expansion, driven by the indispensable role of

thermal insulation in reducing energy consumption, minimizing carbon

footprints, and enhancing occupant comfort across the construction and industrial

sectors. Materials, including fiberglass, plastic foams, and mineral wool, are

fundamental components that determine the thermal resistance, fire safety, and

acoustic performance of buildings and equipment. Technological advancements in

material science, leading to the development of high-performance, eco-friendly,

and lightweight insulation solutions like aerogels and vacuum insulation

panels, are a primary growth engine.

The market is also benefiting

from the global construction boom, particularly in the residential sector,

where insulation is vital for meeting new energy codes. Europe and North

America currently dominate the market due to strong regulatory frameworks like

the Energy Performance of Buildings Directive (EPBD) and robust renovation

activities, while the Asia-Pacific region is poised to be the fastest-growing

market, fueled by rapid urbanization, massive infrastructure development, and

increasing government focus on sustainable building practices. The market is

characterized by the presence of global chemical and material conglomerates and

specialized manufacturers, with competition centered on product performance,

cost-effectiveness, sustainability credentials, and strategic supply chain

integration.

Insulation Materials

Market Drivers and Opportunities

Stringent Energy Efficiency and Green Building Regulations

The

implementation of stringent energy efficiency codes and the global push for

green buildings are the most significant drivers for the insulation materials

market. Governments worldwide are enacting policies and building codes, such as

net-zero energy targets and green building certifications (LEED, BREEAM), that

mandate high levels of thermal insulation in both new construction and building

retrofits. This regulatory push, aimed at reducing greenhouse gas emissions

from the building sector, creates a sustained, compliance-driven demand for

high-performance insulation materials, ensuring a steady market stream.

Growth in Construction and Industrial Sectors

Rapid

urbanization and population growth are fueling construction activities

globally, particularly in emerging economies. The rising number of residential,

commercial, and industrial buildings directly translates to higher consumption

of insulation materials. Furthermore, the industrial sector utilizes insulation

for piping, equipment, and storage tanks in oil & gas, chemical, and

manufacturing plants to improve process efficiency and safety. This dual demand

from the construction and industrial segments provides a strong foundation for

market growth.

Opportunity for the

Insulation Materials Market

Expansion in Retrofitting Activities and Emerging Economies

A

significant opportunity lies in the vast potential of the building renovation

and retrofitting market, especially in developed regions with aging building

stock. Governments are increasingly offering incentives and subsidies for

energy-efficient upgrades, creating a massive aftermarket for insulation

materials. Simultaneously, countries in the Asia-Pacific,

Latin America, and the Middle East are witnessing unprecedented investments in

their construction and industrial infrastructure. The rising middle class,

increasing disposable income, and growing awareness of energy conservation in

these regions present a substantial untapped market for insulation material

suppliers. Companies that focus on developing easy-to-install solutions for

retrofits and establishing strong local manufacturing and distribution networks

are well-positioned to capitalize on this high-growth potential.

Insulation Materials

Market Scope

|

Report Attributes |

Description |

|

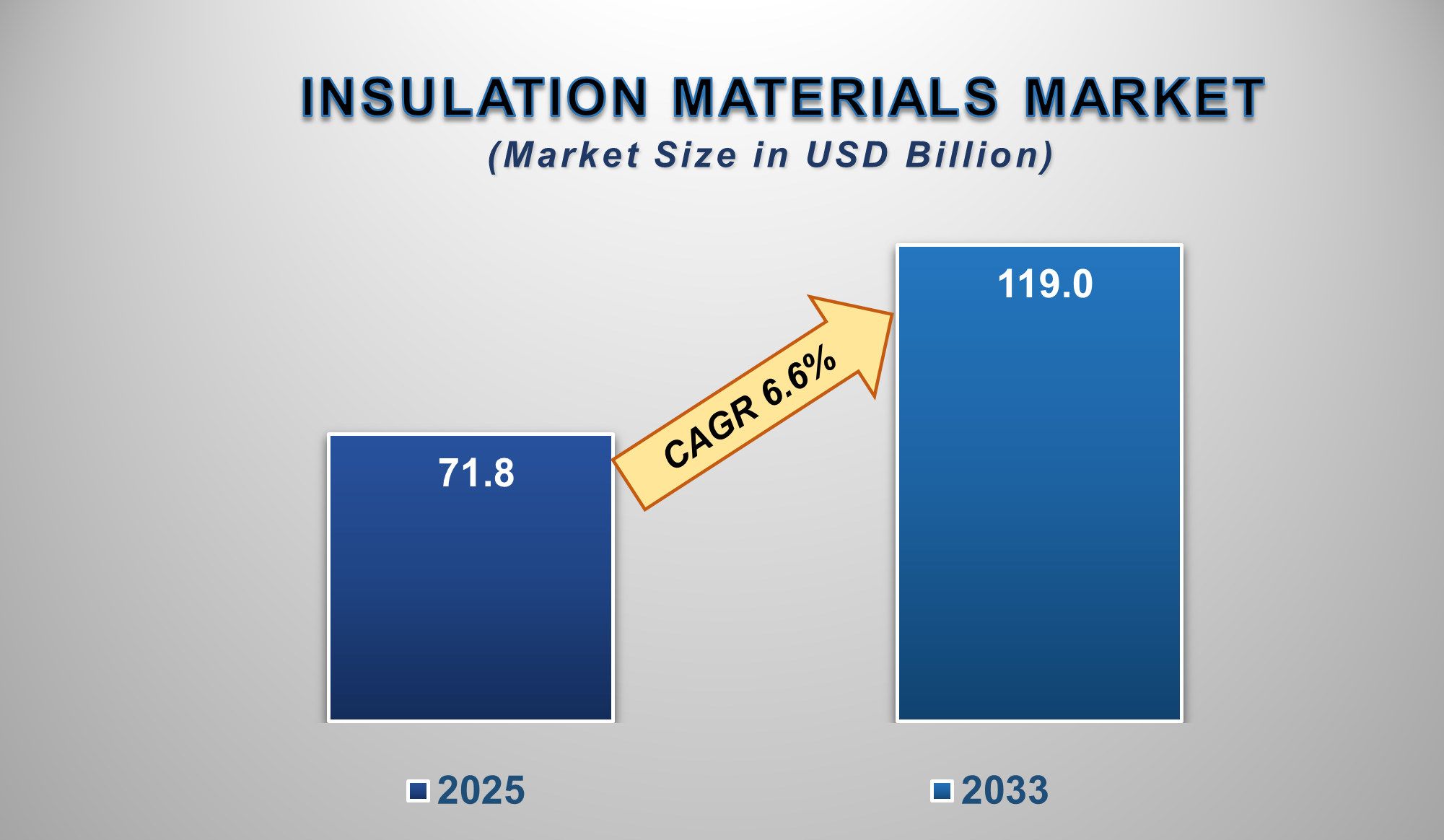

Market Size in 2025 |

USD71.8 Billion |

|

Market Forecast in 2033 |

USD 119.0 Billion |

|

CAGR % 2025-2033 |

8.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production, growth factors, and more |

|

Segments Covered |

●

By Material Type ●

By Form ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherlands 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Insulation Materials

Market Report Segmentation Analysis

The global Insulation Materials

Market industry analysis is segmented by material type, by application, by

form, and by region.

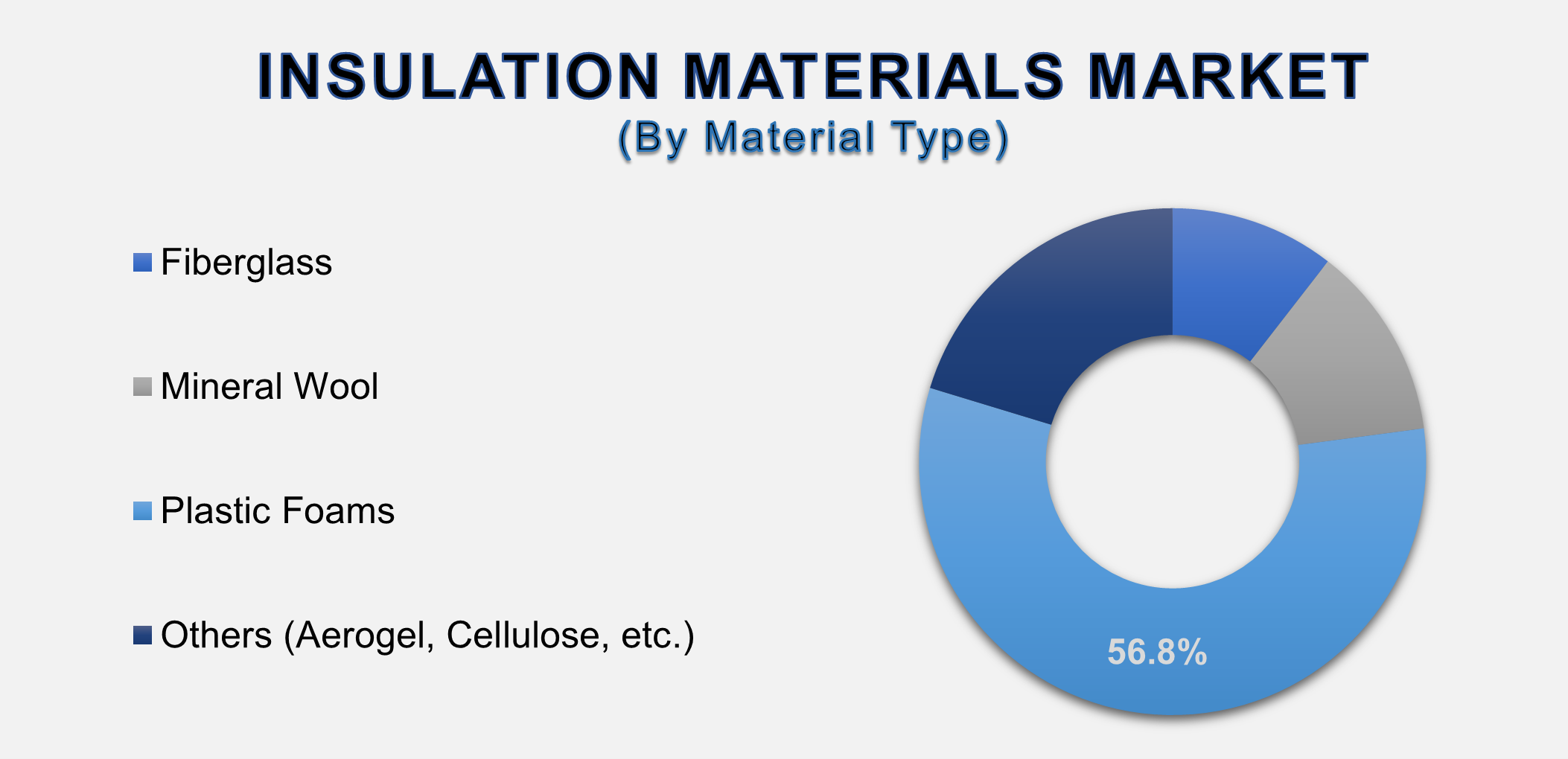

The Plastic Foams material type segment is anticipated to

hold the major share of the global Insulation Materials Market during the

projected timeframe.

The Plastic Foams segment is projected to be the dominant material type in the global insulation materials market, a position solidified by its unparalleled combination of performance, versatility, and cost-efficiency. This category, encompassing expanded polystyrene (EPS), extruded polystyrene (XPS), and polyurethane foams (PUR/PIR), excels due to its superior thermal resistance, often referred to as a high R-value per inch of thickness. This key characteristic allows for the creation of highly energy-efficient building envelopes without excessively thick walls, making it a preferred choice for architects and builders.

Furthermore,

materials like XPS offer exceptional moisture resistance, which is critical for

applications in foundations, roofs, and exterior walls, where preventing thermal degradation and significant

growth is paramount. The versatility of plastic foams is another significant

driver; they are manufactured in various forms, including rigid boards and

spray foam, making them suitable for a wide range of applications from cavity

wall insulation and roofing to flooring and perimeter insulation. Finally, the

cost-effectiveness of EPS, coupled with the ease and speed of installation for

many foam products, provides a compelling economic advantage for both

large-scale commercial projects and residential construction, ensuring its leading market share throughout the forecast period.

The Residential Construction segment is contributing majorly

to the market.

The

Residential Construction application segment holds a major market share, driven

by global housing demand, stringent energy codes for new homes, and growing

consumer awareness regarding energy savings. The sheer volume of new

residential units being built, coupled with the increasing trend of

retrofitting existing homes for improved efficiency, makes this segment the

largest consumer of insulation materials. Government incentives for

energy-efficient homes in many countries further propel this growth.

The Boards form segment is anticipated to hold the highest

share of the market over the forecast period.

The

Boards form segment is projected to be the leading category due to its

widespread use in various applications, including exterior walls, roofs, and

foundations. Insulation boards, particularly those made from XPS, PUR, and PIR,

offer excellent compressive strength, dimensional stability, and ease of

handling, making them a preferred choice for contractors in both new

construction and renovation projects. Their versatility and high performance in

critical building envelopes secure their dominant market share.

The following segments are part of an in-depth analysis of the global

Insulation Materials Market:

|

Market Segments |

|

|

By Material Type |

●

Fiberglass ●

Mineral Wool ●

Plastic Foams (EPS,

XPS, Polyurethane, Polyisocyanurate) ●

Others (Aerogel,

Cellulose, etc.) |

|

By Form |

●

Batts & Rolls ●

Boards ●

Loose-fill ●

Others (Spray,

Reflective) |

|

By Application |

●

Residential

Construction ●

Non-Residential

Construction ●

Industrial ●

HVAC &

Appliances ●

Others |

Insulation Materials

Market Share Analysis by Region

The Europe region is expected to dominate

the Global Insulation Materials Market during the forecast period.

Europe is anticipated to lead the global Insulation

Materials Market, owing to its ambitious climate goals and the world's most

stringent building energy efficiency regulations, such as the Energy

Performance of Buildings Directive (EPBD). The region has a strong focus on

renovating its existing, often inefficient, building stock to meet its 2050

decarbonization targets, which drives consistent and high demand for insulation

materials. According to the European Commission, buildings account for 40% of the

EU's energy consumption, making renovation a top priority funded by initiatives

like the Renovation Wave. The region's mature construction industry, high

awareness of sustainability, and supportive government policies create a

premium market for high-performance, environmentally compliant insulation

products.

Global Insulation Materials Market Recent

Developments News:

- In January 2025, Kingspan Group plc launched a new

bio-based rigid insulation board, incorporating renewable raw materials to

achieve a significantly lower embodied carbon footprint while maintaining

high thermal performance.

- In February 2025, Saint-Gobain S.A. announced a

major investment to expand its glass wool production capacity in North

America, citing rising demand from the residential construction and

industrial markets.

- In March 2025, Owens Corning introduced a

next-generation fiberglass insulation product with enhanced recycled

content and improved handling characteristics for faster installation.

- In April 2025, BASF SE and a leading European

construction firm partnered to develop integrated insulation solutions for

modular building systems, aiming to streamline the construction process

and improve energy efficiency.

The Global Insulation Materials Market is

dominated by a few large companies, such as

●

Saint-Gobain S.A.

●

Owens Corning

●

Kingspan Group plc

●

BASF SE

●

Rockwool International

A/S

●

Knauf Insulation

●

Johns Manville

(Berkshire Hathaway)

●

Recticel NV/SA

●

Armacell International

S.A.

●

Huntsman Corporation

●

GAF Materials

Corporation

●

Carlisle Companies

Inc.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

- Global Insulation Materials Market Introduction and Market Overview

- Objectives of the Study

- Global Insulation Materials Market Scope and Market Estimation

- Global Insulation Materials Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Insulation Materials Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Material Type of Global Insulation Materials Market

- Form of Global Insulation Materials Market

- Application of Global Insulation Materials Market

- Region of Global Insulation Materials Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Insulation Materials Market

- Key Products/Brand Analysis

- Pricing Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Insulation Materials Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Insulation Materials Market Estimates & Forecast Trend Analysis, by Material Type

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Material Type, 2020 - 2033

- Fiberglass

- Mineral Wool

- Plastic Foams (EPS, XPS, Polyurethane, Polyisocyanurate)

- Others (Aerogel, Cellulose, etc.)

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Material Type, 2020 - 2033

- Global Insulation Materials Market Estimates & Forecast Trend Analysis, by Form

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Form, 2020 - 2033

- Batts & Rolls

- Boards

- Loose-fill

- Others (Spray, Reflective)

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Form, 2020 - 2033

- Global Insulation Materials Market Estimates & Forecast Trend Analysis, by Application

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Residential Construction

- Non-Residential Construction

- Industrial

- HVAC & Appliances

- Others

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Insulation Materials Market Estimates & Forecast Trend Analysis, by region

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Insulation Materials Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Insulation Materials Market: Estimates & Forecast Trend Analysis

- North America Insulation Materials Market Assessments & Key Findings

- North America Insulation Materials Market Introduction

- North America Insulation Materials Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material Type

- By Form

- By Application

- By Country

- The U.S.

- Canada

- North America Insulation Materials Market Assessments & Key Findings

- Europe Insulation Materials Market: Estimates & Forecast Trend Analysis

- Europe Insulation Materials Market Assessments & Key Findings

- Europe Insulation Materials Market Introduction

- Europe Insulation Materials Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material Type

- By Form

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Netherland

- Rest of Europe

- Europe Insulation Materials Market Assessments & Key Findings

- Asia Pacific Insulation Materials Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Insulation Materials Market Introduction

- Asia Pacific Insulation Materials Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material Type

- By Form

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Insulation Materials Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Insulation Materials Market Introduction

- Middle East & Africa Insulation Materials Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material Type

- By Form

- By Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Insulation Materials Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Insulation Materials Market Introduction

- Latin America Insulation Materials Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material Type

- By Form

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Insulation Materials Market Product Mapping

- Global Insulation Materials Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Insulation Materials Market Tier Structure Analysis

- Global Insulation Materials Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Saint-Gobain S.A.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Saint-Gobain S.A.

* Similar details would be provided for all the players mentioned below

- Owens Corning

- Kingspan Group plc

- BASF SE

- Rockwool International A/S

- Knauf Insulation

- Johns Manville (Berkshire Hathaway)

- Recticel NV/SA

- Armacell International S.A.

- Huntsman Corporation

- GAF Materials Corporation

- Carlisle Companies Inc.

- Other Prominent Players

- Research Methodology

- External Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables