IoT Engineering Services Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Service Type (Product Engineering, Embedded Engineering, Connectivity Engineering, Cloud Engineering, Data Analytics & AI Integration, Security Engineering, Testing & Validation Services, Others); By Deployment Model (Cloud-based, On-premises, Hybrid); By Enterprise Size (Large Enterprises, Small & Medium Enterprises); By End-use Industry (Manufacturing, Healthcare, Automotive & Transportation, Energy & Utilities, Retail & E-commerce, Telecommunications, Aerospace & Defense, Smart Cities, Others), and Geography

2026-06-22

ICT

Ekta Chaurasia (Team Lead)

Description

IoT Engineering Services Market

Overview

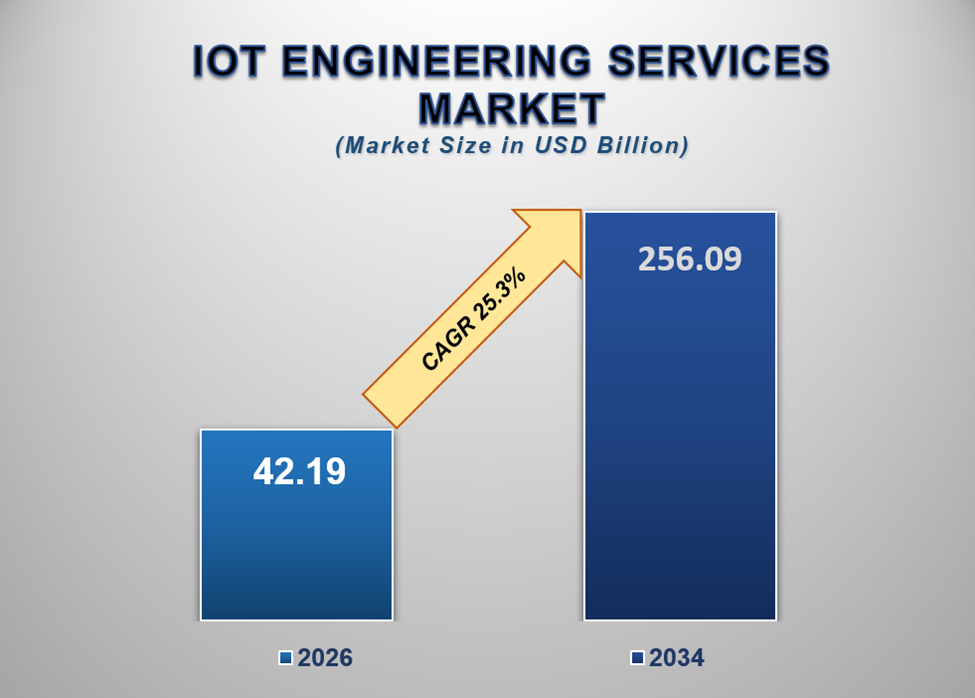

The global IoT

Engineering Services Market was valued at USD 42.19 billion in 2026

and is projected to reach USD 256.09 billion by 2034, expanding at a

remarkable CAGR of 25.3% during the forecast period. The market is

witnessing substantial growth as organizations across industries accelerate

digital transformation initiatives, expand connected device deployments, invest

in smart infrastructure, and increasingly rely on specialized engineering

expertise to develop, integrate, manage, and optimize IoT ecosystems.

The Internet of

Things has emerged as one of the most transformative technological paradigms of

the modern digital era. It enables physical devices, machines, sensors,

vehicles, industrial equipment, healthcare systems, and consumer products to

communicate, exchange data, and perform intelligent actions through connected

networks. As IoT adoption expands globally, organizations increasingly require

specialized engineering services to design, develop, deploy, secure, and manage

sophisticated IoT solutions.

IoT engineering

services encompass a broad range of activities, including hardware engineering,

firmware development, embedded software design, cloud integration, connectivity

architecture, edge computing implementation, cybersecurity engineering, data analytics

integration, and lifecycle management. These services help organizations

accelerate innovation while reducing the complexity associated with large-scale

IoT deployments.

The market is

experiencing rapid growth due to the increasing adoption of Industry 4.0

technologies across manufacturing sectors. Industrial enterprises are deploying

connected machinery, predictive maintenance systems, digital twins, industrial

sensors, and automated production systems to improve operational efficiency and

productivity. These deployments require comprehensive engineering support

throughout the development and implementation lifecycle.

Furthermore, the

growing adoption of connected healthcare systems, smart transportation

infrastructure, autonomous vehicles, intelligent energy management solutions,

and smart city projects is creating significant demand for advanced IoT

engineering capabilities.

The rapid

evolution of technologies such as 5G, artificial intelligence, machine

learning, edge computing, cloud computing, digital twins, blockchain, and

advanced analytics is further increasing the complexity of IoT ecosystems.

Organizations often lack the specialized expertise required to integrate these

technologies effectively, creating strong demand for external engineering

service providers.

Cybersecurity

considerations are also becoming increasingly important as connected device

deployments expand. Organizations require engineering partners capable of

implementing secure architectures, threat detection systems, encryption

protocols, identity management solutions, and regulatory compliance frameworks.

In addition,

growing investments in connected consumer devices, wearable technologies,

industrial automation systems, smart buildings, and intelligent logistics

networks are generating new opportunities for engineering service providers

worldwide.

As enterprises continue embracing digital transformation and connected technologies become integral to business operations, the IoT engineering services market is expected to experience sustained and accelerated growth through 2034.

IoT Engineering Services Market

Drivers and Opportunities

Rapid

Expansion of Industry 4.0 and Industrial IoT Deployments Is Driving Market

Growth

One of the most

significant factors fueling the growth of the IoT engineering services market

is the increasing adoption of Industry 4.0 technologies.

Manufacturing

organizations worldwide are investing heavily in smart factories, connected

production systems, industrial automation platforms, predictive maintenance

solutions, digital twins, and real-time operational monitoring technologies.

These initiatives aim to improve productivity, reduce downtime, optimize

resource utilization, and enhance overall operational performance.

The successful

implementation of industrial IoT environments requires extensive engineering

expertise across multiple disciplines, including embedded systems, connectivity

protocols, cloud platforms, sensor integration, industrial networking, and

cybersecurity.

Many industrial

organizations lack sufficient internal resources to manage large-scale IoT

transformation initiatives independently. Consequently, they increasingly rely

on specialized engineering service providers to support design, deployment,

integration, testing, and ongoing optimization activities.

Furthermore,

industrial enterprises are increasingly seeking scalable and interoperable IoT

architectures capable of supporting future technological advancements. This

trend continues to create significant opportunities for engineering service

providers with deep industrial expertise.

As Industry 4.0 adoption accelerates globally, demand for IoT engineering services is expected to increase substantially.

Increasing

Adoption of Connected Devices Across Industries Is Accelerating Market

Expansion

The

proliferation of connected devices across commercial, industrial, healthcare,

transportation, and consumer environments is another major driver of market

growth.

Organizations

are deploying billions of connected sensors, smart devices, intelligent

equipment, and autonomous systems to improve operational efficiency, customer

experiences, and decision-making capabilities.

Each connected

device ecosystem requires specialized engineering expertise related to hardware

design, firmware development, connectivity management, data processing, cloud

integration, and lifecycle maintenance.

The healthcare

industry, for example, is increasingly adopting connected medical devices,

wearable health monitors, remote patient monitoring systems, and intelligent

healthcare infrastructure. Similarly, the automotive sector is deploying

connected vehicles, telematics platforms, vehicle-to-everything communication

systems, and autonomous driving technologies.

Retail

organizations are utilizing IoT-enabled inventory management systems, smart

shelves, customer analytics platforms, and intelligent logistics networks.

As connected

device ecosystems continue expanding in scale and complexity, organizations are

increasingly partnering with engineering service providers to accelerate

deployment and improve system performance.

This trend is expected to remain a major growth catalyst throughout the forecast period.

Edge

Computing, AI Integration, and Smart Infrastructure Projects Present

Significant Opportunities

Emerging

technologies and large-scale digital infrastructure projects are creating

substantial opportunities within the IoT engineering services market.

Edge computing

is becoming increasingly important as organizations seek to process data closer

to the source, reduce latency, improve reliability, and enhance real-time

decision-making capabilities. Engineering service providers are helping

organizations design and implement sophisticated edge computing architectures

optimized for specific operational requirements.

Artificial

intelligence integration is another major opportunity area. Organizations are

increasingly combining IoT systems with machine learning algorithms, predictive

analytics platforms, computer vision technologies, and intelligent automation

solutions to extract greater value from connected device data.

Smart city

initiatives represent a particularly promising growth opportunity. Governments

worldwide are investing in intelligent transportation systems, smart lighting

networks, environmental monitoring platforms, connected public infrastructure,

and urban safety systems.

Similarly,

energy companies are deploying smart grids, intelligent metering systems,

renewable energy monitoring platforms, and predictive asset management

solutions.

The growing

convergence of IoT, AI, edge computing, cloud technologies, and advanced

analytics is expected to generate significant long-term demand for specialized

engineering expertise.

Organizations

capable of delivering end-to-end engineering services across these domains are

likely to experience substantial growth opportunities in the coming years.

IoT Engineering Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 42.19 Billion |

|

Market Forecast in 2034 |

USD 256.09 Billion |

|

CAGR % 2026-2034 |

25.3% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production, Service Type, Growth

Factors and more |

|

Segments Covered |

∙ By Service Type |

|

Regional Scope |

● North America |

|

Country Scope |

U.S. |

IoT

Engineering Services Market Report Segmentation Analysis

The global IoT engineering services market industry analysis is segmented by service type, by deployment model, by enterprise size, by end-use industry, and by region.

Product

Engineering Segment Is Expected to Dominate the Market During the Forecast

Period

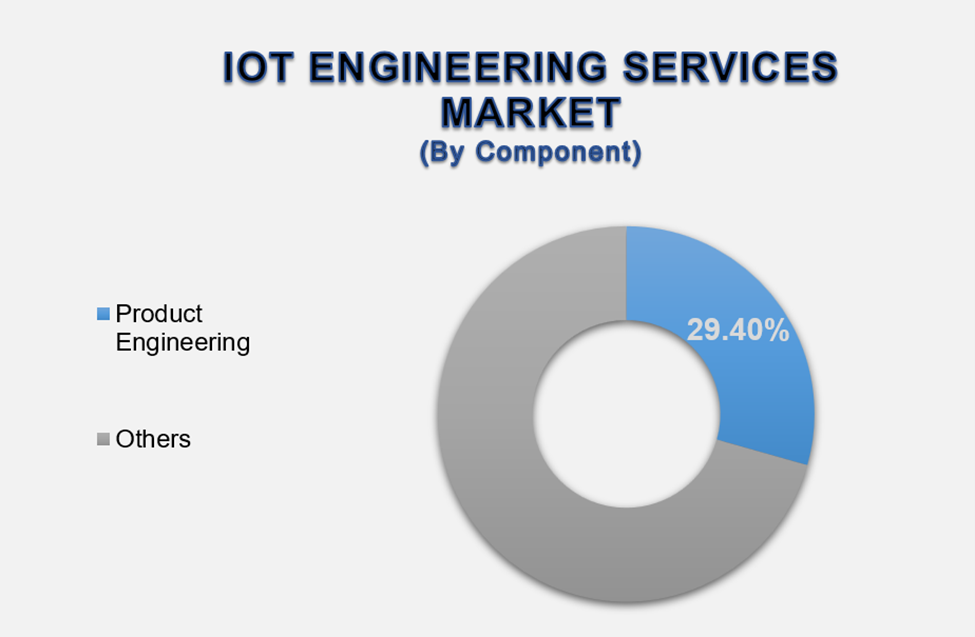

The product

engineering segment accounted for approximately 29.4% of the global market,

making it the leading service category.

Product

engineering services form the foundation of IoT solution development and

encompass the design, development, prototyping, testing, optimization, and

lifecycle management of connected products. As organizations increasingly

launch IoT-enabled devices and intelligent systems, demand for specialized

product engineering expertise continues to rise.

Companies across

industries require customized connected products tailored to specific

operational, regulatory, and customer requirements. Engineering service

providers support these initiatives by delivering end-to-end product

development capabilities that accelerate time-to-market while minimizing

development risks.

The increasing

complexity of connected devices is further strengthening demand for product

engineering services. Modern IoT products must integrate hardware components,

embedded software, cloud connectivity, security frameworks, data analytics

capabilities, and user experience functionalities within a unified ecosystem.

Furthermore,

rapid innovation cycles require continuous product enhancements and feature

upgrades. Engineering service providers help organizations maintain

competitiveness through ongoing product evolution and optimization.

Given its strategic importance within the IoT development lifecycle, the product engineering segment is expected to maintain market leadership throughout the forecast period.

Cloud-based

Segment Is Expected to Lead the Market by Deployment Model

Cloud-based

deployment represents the dominant segment within the IoT engineering services

market.

Cloud platforms

provide the scalability, flexibility, storage capacity, and computational power

necessary to support large-scale IoT ecosystems. Organizations increasingly

prefer cloud-based deployments because they enable centralized management of

connected devices, data analytics workflows, artificial intelligence

applications, and system integrations.

The growing

volume of data generated by connected devices makes cloud infrastructure

essential for efficient processing and storage. Engineering service providers

are helping organizations design cloud-native IoT architectures optimized for

performance, scalability, and security.

Furthermore,

cloud-based deployments facilitate remote monitoring, predictive maintenance,

software updates, and multi-site management capabilities. These advantages

continue driving adoption across industries.

As organizations increasingly migrate digital operations to cloud environments, demand for cloud-focused IoT engineering services is expected to grow significantly.

Large

Enterprises Segment Is Expected to Dominate the Market by Enterprise Size

Large

enterprises account for the largest share of the IoT engineering services

market due to their extensive digital transformation initiatives and

significant technology investments.

These

organizations typically operate complex business environments involving

large-scale infrastructure, distributed operations, extensive supply chains,

and substantial data generation requirements. Consequently, they are among the

earliest adopters of advanced IoT technologies.

Large

enterprises frequently deploy connected manufacturing systems, intelligent

logistics networks, predictive maintenance platforms, smart buildings,

connected healthcare infrastructure, and advanced analytics solutions.

The scale and

complexity of these projects often require external engineering expertise

capable of supporting architecture design, implementation, integration,

testing, and ongoing optimization activities.

Additionally,

large organizations increasingly pursue enterprise-wide IoT strategies aimed at

improving operational efficiency, customer experiences, and business

intelligence capabilities.

These factors continue to support strong demand from the large enterprise segment.

Manufacturing

Segment Is Expected to Lead the Market by End-use Industry

Manufacturing

remains the largest end-use industry within the IoT engineering services

market.

The sector is

undergoing a profound digital transformation driven by Industry 4.0

initiatives, automation technologies, smart factory deployments, and connected

production systems. Manufacturers increasingly utilize IoT technologies to

improve equipment utilization, reduce operational costs, enhance quality

control, and optimize supply chain performance.

Engineering

service providers play a critical role in supporting these initiatives by

developing industrial IoT platforms, integrating sensors and devices,

implementing predictive maintenance solutions, and enabling real-time

operational visibility.

The growing

adoption of digital twins, robotics, machine learning, and industrial analytics

is further increasing demand for specialized engineering expertise.

As manufacturing organizations continue investing in intelligent production environments, the sector is expected to remain the largest consumer of IoT engineering services globally.

The following

segments are part of an in-depth analysis of the global IoT Engineering

Services market:

|

Market Segments |

|

|

By Offering |

∙ Product Engineering |

|

By

Type |

∙ Cloud-based |

|

By Application |

∙ Large Enterprises |

|

By End User |

∙ Manufacturing |

IoT

Engineering Services Market Share Analysis By Region

North America is

projected to dominate the global IoT engineering services market, accounting

for approximately 37.8% of global revenue in 2026.

The region

benefits from strong digital infrastructure, widespread adoption of advanced

technologies, significant investments in industrial automation, and the

presence of major technology companies. The United States remains the primary

growth engine due to extensive IoT deployments across manufacturing,

healthcare, transportation, telecommunications, and smart infrastructure

sectors.

Europe

represents another major market supported by Industry 4.0 adoption, smart

manufacturing initiatives, and increasing investments in digital engineering

services. Germany, the United Kingdom, and France remain key contributors to

regional growth.

Asia-Pacific is

expected to witness the fastest expansion during the forecast period. Rapid

industrialization, growing smart city investments, expanding telecommunications

infrastructure, and increasing adoption of connected technologies are fueling

regional demand.

China, India,

Japan, and South Korea are investing heavily in industrial automation, 5G

infrastructure, connected manufacturing systems, and digital transformation

initiatives, creating substantial opportunities for IoT engineering service

providers.

Meanwhile, the Middle East is increasingly investing in smart city development programs, while Latin America is experiencing growing adoption of connected business solutions.

IoT

Engineering Services Market Competition Landscape Analysis

The global IoT

engineering services market is highly competitive and characterized by rapid

technological innovation, strategic partnerships, and expanding service

portfolios.

Leading

companies are investing heavily in artificial intelligence integration, cloud

engineering capabilities, cybersecurity services, edge computing expertise, and

industry-specific IoT solutions. Organizations increasingly seek engineering

partners capable of delivering comprehensive end-to-end services rather than

isolated technical capabilities.

Strategic

collaborations between technology providers, cloud vendors, semiconductor

companies, telecommunications operators, and engineering service firms are

becoming increasingly common as market participants seek to accelerate

innovation and improve service offerings.

Competition is

also intensifying as enterprises demand faster deployment timelines, stronger

cybersecurity capabilities, improved interoperability, and measurable business

outcomes from IoT initiatives.

Companies that successfully combine engineering expertise, industry knowledge, and advanced technology capabilities are expected to maintain strong competitive positions throughout the forecast period.

Global IoT

Engineering Services Market Recent Developments News:

∙ In April 2026, several engineering

service providers expanded AI-integrated IoT development offerings to support

intelligent automation initiatives.

∙ In February 2026, industrial

organizations accelerated investments in smart factory projects and connected

manufacturing platforms.

∙ In November 2025, multiple technology

firms introduced next-generation edge computing solutions designed for

industrial IoT environments.

∙ In August 2025, enterprises increased

deployment of connected asset monitoring systems to improve operational

efficiency and predictive maintenance capabilities.

∙ In June 2025, service providers expanded cybersecurity-focused IoT engineering services to address growing connected device security concerns.

The Global

IoT Engineering Services Market is Dominated by a Few Large Companies, Such as

∙ Accenture plc

∙ Capgemini SE

∙ Tata Consultancy Services (TCS)

∙ Infosys Limited

∙ Wipro Limited

∙ HCL Technologies Limited

∙ Cognizant Technology Solutions Corporation

∙ Tech Mahindra Limited

∙ LTIMindtree Limited

∙ EPAM Systems, Inc.

∙ IBM Corporation

∙ Bosch Global Software Technologies

∙ Cyient Limited

∙ Happiest Minds Technologies Limited

∙ Persistent Systems Limited

∙ Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global IoT Engineering

Services Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global IoT Engineering Services Market Scope and Market Estimation

1.2.1.

Global IoT Engineering Services

Market Size (US$ Million), Market CAGR (%), Market Forecast (2026 - 2034)

1.2.2.

Global IoT Engineering Services

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1.

Service Type of Global IoT

Engineering Services Market

1.3.2.

Deployment Model of Global IoT

Engineering Services Market

1.3.3.

Enterprise Size of Global IoT

Engineering Services Market

1.3.4.

End-use Industry of Global IoT

Engineering Services Market

1.3.5.

Region of Global IoT

Engineering Services Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Million) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Tariff, Regulatory Landscape and Standards

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global IoT Engineering

Services Market Estimates & Historical Trend Analysis (2021 - 2025)

4.

Global IoT Engineering

Services Market Estimates & Forecast Trend Analysis, by Service Type

4.1. Global IoT Engineering Services Market Revenue (US$ Million)

Estimates and Forecasts, by Service Type, 2021 - 2034

4.1.1.

Product Engineering

4.1.2.

Embedded Engineering

4.1.3.

Connectivity Engineering

4.1.4.

Cloud Engineering

4.1.5.

Data Analytics & AI

Integration

4.1.6.

Security Engineering

4.1.7.

Testing & Validation

Services

4.1.8.

Others

5.

Global IoT Engineering

Services Market Estimates & Forecast Trend Analysis, by Deployment Model

5.1. Global IoT Engineering Services Market Revenue (US$ Million)

Estimates and Forecasts, by Deployment Model, 2021 - 2034

5.1.1.

Cloud-based

5.1.2.

On-premises

5.1.3.

Hybrid

6.

Global IoT Engineering

Services Market Estimates & Forecast Trend Analysis, by Enterprise Size

6.1. Global IoT Engineering Services Market Revenue (US$ Million)

Estimates and Forecasts, by Enterprise Size, 2021 - 2034

6.1.1.

Large Enterprises

6.1.2.

Small & Medium Enterprises

7.

Global IoT Engineering

Services Market Estimates & Forecast Trend Analysis, by End-use Industry

7.1. Global IoT Engineering Services Market Revenue (US$ Million)

Estimates and Forecasts, by End-use Industry, 2021 - 2034

7.1.1.

Manufacturing

7.1.2.

Healthcare

7.1.3.

Automotive & Transportation

7.1.4.

Energy & Utilities

7.1.5.

Retail & E-commerce

7.1.6.

Telecommunications

7.1.7.

Aerospace & Defense

7.1.8.

Smart Cities

7.1.9.

Others

8.

Global IoT Engineering

Services Market Estimates & Forecast Trend Analysis, by Region

8.1. Global IoT Engineering Services Market Revenue (US$ Million)

Estimates and Forecasts, by Region, 2021 - 2034

8.1.1.

North America

8.1.2.

Europe

8.1.3.

Asia Pacific

8.1.4.

Middle East & Africa

8.1.5.

Latin America

9.

North America IoT

Engineering Services Market: Estimates & Forecast Trend Analysis

9.1. North America IoT Engineering Services Market Assessments & Key

Findings

9.1.1.

North America IoT Engineering

Services Market Introduction

9.1.2.

North America IoT Engineering

Services Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

9.1.2.1.

By Service Type

9.1.2.2.

By Deployment Model

9.1.2.3.

By Enterprise Size

9.1.2.4.

By End-use Industry

9.1.2.5.

By Country

9.1.2.5.1.

The U.S.

9.1.2.5.2.

Canada

10. Europe IoT Engineering Services Market: Estimates & Forecast

Trend Analysis

10.1.

Europe IoT Engineering Services

Market Assessments & Key Findings

10.1.1.

Europe IoT Engineering Services

Market Introduction

10.1.2.

Europe IoT Engineering Services

Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

10.1.2.1.

By Service Type

10.1.2.2.

By Deployment Model

10.1.2.3.

By Enterprise Size

10.1.2.4.

By End-use Industry

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest of Europe

11. Asia Pacific IoT Engineering Services Market: Estimates &

Forecast Trend Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific IoT Engineering

Services Market Introduction

11.1.2.

Asia Pacific IoT Engineering

Services Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

11.1.2.1.

By Service Type

11.1.2.2.

By Deployment Model

11.1.2.3.

By Enterprise Size

11.1.2.4.

By End-use Industry

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6.

Rest of Asia Pacific

12. Middle East & Africa IoT Engineering Services Market: Estimates

& Forecast Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa IoT

Engineering Services Market Introduction

12.1.2.

Middle East & Africa IoT

Engineering Services Market Size Estimates and Forecast (US$ Million) (2021 -

2034)

12.1.2.1.

By Service Type

12.1.2.2.

By Deployment Model

12.1.2.3.

By Enterprise Size

12.1.2.4.

By End-use Industry

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4.

Rest of MEA

13. Latin America IoT Engineering Services Market: Estimates &

Forecast Trend Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America IoT Engineering

Services Market Introduction

13.1.2.

Latin America IoT Engineering

Services Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

13.1.2.1.

By Service Type

13.1.2.2.

By Deployment Model

13.1.2.3.

By Enterprise Size

13.1.2.4.

By End-use Industry

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global IoT Engineering Services

Market Product Mapping

14.2.

Global IoT Engineering Services

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3.

Global IoT Engineering Services

Market Tier Structure Analysis

14.4.

Global IoT Engineering Services

Market Concentration & Company Market Shares (%) Analysis, 2025

15. Company Profiles

15.1.

Accenture plc

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Service Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

*Similar details would be provided for all

the players mentioned below

15.2.

Capgemini SE

15.3.

Tata Consultancy Services (TCS)

15.4.

Infosys Limited

15.5.

Wipro Limited

15.6.

HCL Technologies Limited

15.7.

Cognizant Technology Solutions

Corporation

15.8.

Tech Mahindra Limited

15.9.

LTIMindtree Limited

15.10.

EPAM Systems, Inc.

15.11.

IBM Corporation

15.12.

Bosch Global Software

Technologies

15.13.

Cyient Limited

15.14.

Happiest Minds Technologies

Limited

15.15.

Persistent Systems Limited

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables