IoT Identity Access Management (IAM) Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (Solutions, Services); By Deployment Mode (Cloud-Based, On-Premises, Hybrid); By Organization Size (Large Enterprises, Small & Medium Enterprises); By Authentication Type (Multi-Factor Authentication, Certificate-Based Authentication, Biometric Authentication, Passwordless Authentication, Others); By End-use Industry (Manufacturing, Healthcare, BFSI, Retail & E-commerce, Energy & Utilities, Automotive, Government & Defense, Telecommunications, Others), and Geography

2026-06-23

ICT

Ekta Chaurasia (Team Lead)

Description

IoT Identity Access Management (IAM)

Market Overview

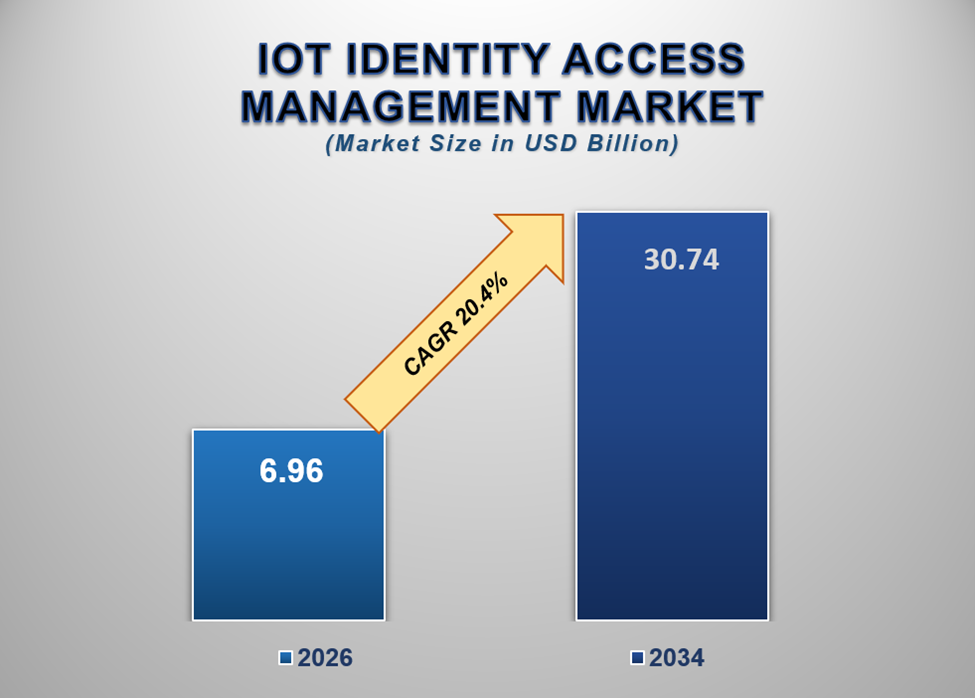

The global IoT

Identity Access Management (IAM) Market was valued at USD 6.96 billion

in 2026 and is projected to reach USD 30.74 billion by 2034,

expanding at a CAGR of 20.4% during the forecast period. The market is

experiencing rapid growth due to the exponential increase in connected devices,

rising cybersecurity threats targeting IoT ecosystems, growing regulatory

compliance requirements, increasing adoption of zero-trust security

architectures, and expanding investments in enterprise-grade identity governance

solutions.

The Internet of

Things has fundamentally transformed how organizations collect, process, and

utilize data by connecting billions of devices across industrial, commercial,

consumer, healthcare, transportation, and government environments. However,

this rapid expansion of connected ecosystems has also created significant

security challenges related to device authentication, identity verification,

access control, authorization management, and cybersecurity governance.

IoT Identity

Access Management solutions are designed to address these challenges by

enabling organizations to establish, manage, authenticate, monitor, and secure

the identities of connected devices, users, applications, and systems

throughout their lifecycle. These solutions ensure that only authorized

entities gain access to critical networks, devices, and data resources.

As organizations

deploy increasingly complex IoT infrastructures, traditional identity

management approaches are becoming insufficient. Unlike conventional IT

environments, IoT ecosystems may involve millions of connected devices

operating across multiple networks, geographical locations, cloud environments,

and edge computing platforms. Managing identities and access rights at such a

scale require specialized IAM solutions specifically designed for IoT

environments.

The market is

witnessing substantial growth due to the rising frequency of cyberattacks

targeting connected devices. Threat actors increasingly exploit weak

authentication mechanisms, unsecured endpoints, default credentials, and poorly

managed device identities to gain unauthorized access to enterprise systems. As

a result, organizations are prioritizing investments in advanced identity and

access management frameworks.

Furthermore, the

adoption of Industry 4.0 technologies, smart cities, connected healthcare

systems, autonomous vehicles, intelligent energy infrastructure, and smart

consumer devices is creating a growing need for scalable identity management

solutions capable of supporting billions of interconnected devices.

Regulatory

compliance requirements are also driving market expansion. Governments and

industry regulators worldwide are introducing stricter cybersecurity standards

focused on identity governance, data protection, device authentication, and

access management. Organizations must implement robust IAM frameworks to meet

these evolving requirements while minimizing security risks.

The emergence of

zero-trust security models is further accelerating demand for IoT IAM

solutions. Modern cybersecurity strategies increasingly require continuous

verification of users, devices, applications, and network activities rather

than relying solely on traditional perimeter-based defenses.

Additionally,

advancements in artificial intelligence, machine learning, behavioral

analytics, blockchain-based identity management, and passwordless

authentication technologies are enhancing the effectiveness of modern IAM

platforms.

As connected ecosystems continue expanding across industries, IoT identity and access management solutions are expected to become a critical component of enterprise cybersecurity strategies throughout the forecast period.

IoT Identity Access Management (IAM)

Market Drivers and Opportunities

Rising

Cybersecurity Threats Across Connected Ecosystems Are Driving Market Growth

The increasing

sophistication and frequency of cyberattacks targeting IoT environments

represent one of the strongest growth drivers for the IoT IAM market.

Organizations

worldwide are deploying millions of connected devices across operational

environments. While these devices improve efficiency and enable digital

transformation, they also expand the potential attack surface available to

cybercriminals.

Many connected

devices historically lacked robust security mechanisms, making them attractive

targets for unauthorized access, malware deployment, ransomware attacks, data

theft, and distributed denial-of-service attacks. Weak identity management

practices further exacerbate these vulnerabilities.

IoT IAM

solutions help address these challenges by establishing strong authentication

mechanisms, enforcing access control policies, managing digital identities, and

continuously monitoring user and device activities.

Organizations

increasingly recognize that effective identity governance is essential for

protecting connected ecosystems from evolving cyber threats. Consequently,

investments in advanced IAM platforms are growing rapidly across industries.

As cyber threats continue becoming more sophisticated, the demand for comprehensive IoT identity management solutions is expected to increase significantly.

Expansion of

Connected Devices and IoT Deployments Is Accelerating Market Adoption

The rapid growth

of IoT deployments across industrial, commercial, and consumer environments is

creating substantial demand for identity and access management solutions.

Billions of

connected devices are being deployed globally across manufacturing facilities,

healthcare institutions, transportation systems, smart cities, energy

infrastructure, retail environments, and residential applications. Each device

requires a unique identity and secure access controls to prevent unauthorized

activities.

Managing

identities for large-scale IoT ecosystems presents significant operational

challenges. Organizations must authenticate devices, manage credentials, define

access privileges, monitor activity patterns, and revoke permissions when

necessary.

Traditional

identity management systems were not designed to support the scale, diversity,

and complexity of modern IoT environments. Consequently, enterprises are

increasingly adopting specialized IoT IAM platforms capable of automating

identity lifecycle management and access governance processes.

Furthermore, the

integration of edge computing, cloud platforms, artificial intelligence, and

machine learning technologies is increasing the complexity of connected

environments, further strengthening the need for advanced IAM capabilities.

As IoT adoption continues accelerating worldwide, demand for scalable and intelligent identity management solutions is expected to expand substantially.

Zero-Trust

Security and Passwordless Authentication Present Significant Opportunities

The growing

adoption of zero-trust cybersecurity architectures is creating significant

opportunities within the IoT IAM market.

Zero-trust

frameworks operate on the principle that no user, device, or application should

be trusted by default. Instead, every access request must be continuously

verified based on identity, context, behavior, and risk factors.

IoT IAM

solutions play a central role in enabling zero-trust strategies by providing

authentication, authorization, identity governance, and continuous access

validation capabilities.

Additionally,

organizations are increasingly moving toward passwordless authentication

technologies to improve security and user experiences. Biometric

authentication, hardware security keys, digital certificates, behavioral

analytics, and AI-driven authentication methods are gaining widespread

adoption.

Emerging

technologies such as decentralized identity systems, blockchain-based identity

verification, and self-sovereign identity frameworks are also creating new

growth opportunities.

The increasing

integration of artificial intelligence and machine learning into IAM platforms

enables organizations to detect anomalous behaviors, identify potential

threats, and automate security responses in real time.

As cybersecurity

strategies continue evolving toward identity-centric security models,

opportunities for advanced IoT IAM solutions are expected to increase

significantly.

IoT Identity Access Management (IAM)

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 6.96 Billion |

|

Market Forecast in 2034 |

USD 30.74 Billion |

|

CAGR % 2026-2034 |

20.4% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production, Service Type, Growth

Factors and more |

|

Segments Covered |

∙ By Component |

|

Regional Scope |

● North America |

|

Country Scope |

U.S. |

IoT Identity

Access Management (IAM) Market Report Segmentation Analysis

The global IoT Identity Access Management market industry analysis is segmented by component, by deployment mode, by organization size, by authentication type, by end-use industry, and by region.

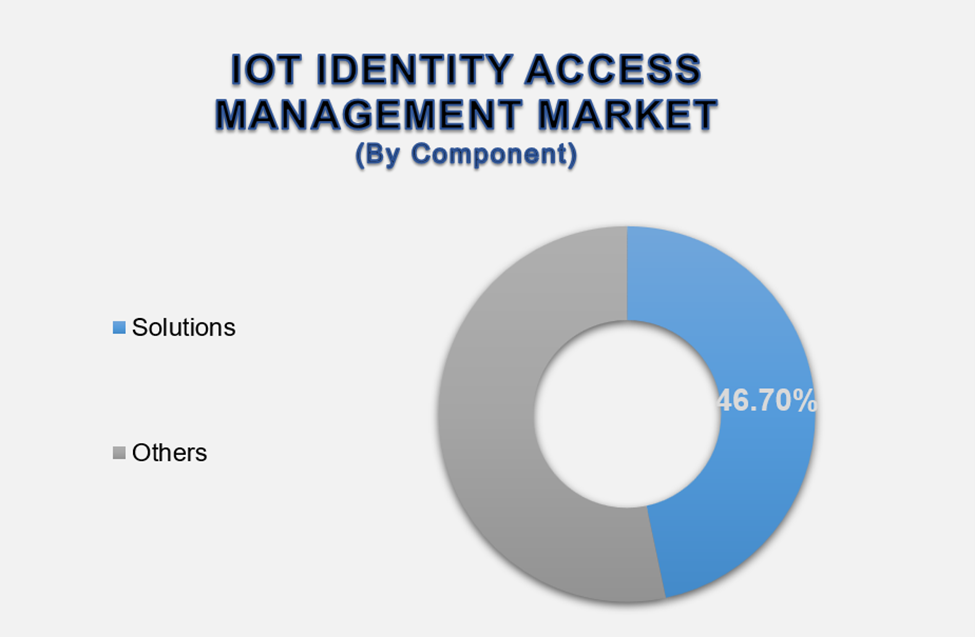

Solutions

Segment Is Expected to Dominate the Market During the Forecast Period

The solutions

segment accounted for approximately 64.3% of the global market, making

it the leading component category.

The solutions

segment dominates the market because organizations increasingly require

comprehensive identity management platforms capable of securing rapidly

expanding IoT ecosystems. These solutions provide centralized identity

governance, authentication management, access control, credential lifecycle

management, threat detection, and compliance monitoring capabilities.

Modern

enterprises are deploying thousands or even millions of connected devices

across distributed environments. Managing identities manually in such

environments is impractical, driving demand for automated IAM platforms.

Organizations

are also prioritizing integrated solutions capable of supporting cloud

environments, edge computing infrastructures, industrial IoT networks, and

hybrid deployment models from a unified management interface.

The increasing

adoption of artificial intelligence-enabled IAM solutions is further

strengthening segment growth. Advanced solutions can automatically detect

anomalies, identify suspicious activities, and enforce adaptive security

policies based on contextual risk assessments.

As cybersecurity threats continue evolving, organizations are expected to invest heavily in advanced identity management platforms, supporting the continued dominance of the solutions segment.

Cloud-Based

Segment Is Expected to Lead the Market by Deployment Mode

Cloud-based

deployment represents the largest segment within the IoT IAM market.

Organizations

increasingly prefer cloud-based IAM solutions because they offer scalability,

flexibility, centralized management capabilities, lower infrastructure costs,

and simplified deployment processes.

The rapid

expansion of connected devices often requires organizations to manage

identities across geographically dispersed locations and multiple operational

environments. Cloud-based IAM platforms enable centralized administration and

real-time visibility across these complex ecosystems.

Furthermore,

cloud deployment models facilitate automatic software updates, threat

intelligence integration, disaster recovery capabilities, and seamless

scalability as connected device volumes increase.

The growing

adoption of multi-cloud and hybrid-cloud strategies is further supporting

cloud-based IAM adoption.

As enterprises continue accelerating digital transformation initiatives, cloud-based deployment is expected to remain the dominant market segment.

Large

Enterprises Segment Is Expected to Dominate the Market by Organization Size

Large

enterprises account for the largest share of the IoT IAM market due to their

extensive connected device deployments, complex operational environments, and

substantial cybersecurity investments.

These

organizations often manage large-scale industrial networks, smart

infrastructure systems, connected manufacturing facilities, healthcare

platforms, and global operational ecosystems. Such environments require

sophisticated identity management frameworks capable of securing millions of

users, devices, applications, and services.

Large

enterprises are also subject to stringent regulatory requirements related to

cybersecurity, privacy protection, risk management, and operational resilience.

Consequently, they are among the earliest adopters of advanced IAM

technologies.

Furthermore,

increasing digital transformation initiatives and cloud migration strategies

are encouraging enterprises to strengthen identity-centric security frameworks.

These factors

collectively support the continued dominance of the large enterprise segment.

Manufacturing

Segment Is Expected to Lead the Market by End-use Industry

Manufacturing

represents the largest end-use industry within the IoT IAM market.

The rapid

adoption of Industry 4.0 technologies, industrial automation systems, connected

machinery, predictive maintenance platforms, and smart factory initiatives has

significantly increased the number of connected devices within manufacturing

environments.

Industrial

organizations must secure machine identities, user access privileges,

operational technology systems, and industrial control networks while ensuring

uninterrupted production operations.

IoT IAM

solutions help manufacturers establish secure authentication frameworks,

prevent unauthorized access, protect intellectual property, and maintain

compliance with cybersecurity regulations.

Additionally,

manufacturers are increasingly integrating cloud computing, edge computing,

digital twins, and artificial intelligence into production environments,

further increasing identity management complexity.

As industrial digitalization continues to accelerate globally, manufacturing is expected to remain the largest consumer of IoT IAM solutions.

The following segments are part of an in-depth analysis of the global IoT Identity Access Management (IAM) market

|

Market Segments |

|

|

By Component |

∙ Solutions |

|

By

Deployment mode |

∙ Cloud-Based |

|

By

Organization Size |

∙ Large Enterprises |

|

By

Authentication Type |

∙ Multi-Factor

Authentication |

|

By End User |

∙

Manufacturing |

IoT Identity

Access Management (IAM) Market Share Analysis By Region

North America is

projected to dominate the global IoT IAM market, accounting for approximately 39.2%

of total market revenue in 2026.

The region

benefits from advanced cybersecurity infrastructure, widespread IoT adoption,

strong regulatory frameworks, and significant investments in digital

transformation initiatives. The United States remains the largest contributor

due to the presence of major technology companies, cybersecurity vendors, cloud

service providers, and large-scale enterprise IoT deployments.

Europe

represents another significant market driven by stringent data protection

regulations, increasing cybersecurity awareness, and growing adoption of

identity-centric security strategies. Countries such as Germany, the United

Kingdom, and France are leading regional growth.

Asia-Pacific is

expected to witness the fastest growth throughout the forecast period. Rapid

industrialization, expanding IoT deployments, increasing cybersecurity

investments, and accelerating digital transformation initiatives are creating

substantial opportunities across the region.

China, India,

Japan, and South Korea are investing heavily in smart manufacturing, smart city

infrastructure, connected healthcare systems, and digital governance platforms,

all of which require robust identity management capabilities.

Meanwhile, the Middle East is strengthening cybersecurity investments through national digital transformation programs, while Latin America continues expanding enterprise cybersecurity adoption.

IoT Identity

Access Management (IAM) Market Competition Landscape Analysis

The global IoT

IAM market is highly competitive and characterized by continuous innovation,

strategic partnerships, acquisitions, and technology advancements.

Leading

companies are investing heavily in artificial intelligence-driven

authentication systems, behavioral analytics, passwordless authentication

technologies, zero-trust security frameworks, and decentralized identity

management solutions.

Market

participants are increasingly focusing on integrated security platforms that

combine identity governance, access management, privileged access control,

threat detection, and compliance management capabilities.

Strategic

collaborations between cybersecurity providers, cloud vendors, IoT platform

providers, and telecommunications companies are becoming increasingly common as

organizations seek comprehensive security solutions.

As cyber threats continue evolving and connected ecosystems expand, competition is expected to intensify across all market segments.

Global IoT

Identity Access Management (IAM) Market Recent Developments News:

∙ In April 2026, cybersecurity providers

expanded AI-powered identity verification solutions designed for large-scale

IoT ecosystems.

∙ In February 2026, several enterprises

accelerated the deployment of zero-trust security architectures to strengthen

connected device security.

∙ In November 2025, technology vendors

introduced advanced passwordless authentication platforms for industrial IoT

environments.

∙ In August 2025, organizations increased

investments in identity governance solutions to support regulatory compliance

initiatives.

∙ In June 2025, cybersecurity companies launched automated certificate management tools designed for connected device authentication.

The Global

IoT Identity Access Management (IAM) Market is Dominated by a Few Large

Companies, Such As

∙ Microsoft Corporation

∙ IBM Corporation

∙ Cisco Systems, Inc.

∙ Okta, Inc.

∙ ForgeRock, Inc.

∙ Ping Identity Holding Corp.

∙ CyberArk Software Ltd.

∙ Thales Group

∙ Entrust Corporation

∙ One Identity LLC

∙ Broadcom Inc.

∙ Oracle Corporation

∙ SailPoint Technologies Holdings, Inc.

∙ HID Global Corporation

∙ DigiCert, Inc.

∙ Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1.

Global IoT Identity

Access Management (IAM) Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global IoT Identity Access Management (IAM) Market Scope and Market

Estimation

1.2.1.

Global IoT Identity Access

Management (IAM) Overall Market Size (US$ Million), Market CAGR (%), Market

Forecast (2026 - 2034)

1.2.2.

Global IoT Identity Access

Management (IAM) Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 -

2034

1.3. Market Segmentation

1.3.1.

Component of Global IoT

Identity Access Management (IAM) Market

1.3.2.

Deployment Mode of Global IoT

Identity Access Management (IAM) Market

1.3.3.

Organization Size of Global IoT

Identity Access Management (IAM) Market

1.3.4.

Authentication Type of Global

IoT Identity Access Management (IAM) Market

1.3.5.

End-use Industry of Global IoT

Identity Access Management (IAM) Market

1.3.6.

Region of Global IoT Identity

Access Management (IAM) Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Million) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Tariff, Regulatory Landscape and Standards

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global IoT Identity

Access Management (IAM) Market Estimates & Historical Trend Analysis (2021

- 2025)

4.

Global IoT Identity

Access Management (IAM) Market Estimates & Forecast Trend Analysis, by

Component

4.1. Global IoT Identity Access Management (IAM) Market Revenue (US$

Million) Estimates and Forecasts, by Component, 2021 - 2034

4.1.1.

Solutions

4.1.2.

Services

5.

Global IoT Identity

Access Management (IAM) Market Estimates & Forecast Trend Analysis, by

Deployment Mode

5.1. Global IoT Identity Access Management (IAM) Market Revenue (US$

Million) Estimates and Forecasts, by Deployment Mode, 2021 - 2034

5.1.1.

Cloud-Based

5.1.2.

On-Premises

5.1.3.

Hybrid

6.

Global IoT Identity

Access Management (IAM) Market Estimates & Forecast Trend Analysis, by

Organization Size

6.1. Global IoT Identity Access Management (IAM) Market Revenue (US$

Million) Estimates and Forecasts, by Organization Size, 2021 - 2034

6.1.1.

Large Enterprises

6.1.2.

Small & Medium Enterprises

7.

Global IoT Identity

Access Management (IAM) Market Estimates & Forecast Trend Analysis, by

Authentication Type

7.1. Global IoT Identity Access Management (IAM) Market Revenue (US$

Million) Estimates and Forecasts, by Authentication Type, 2021 - 2034

7.1.1.

Multi-Factor Authentication

7.1.2.

Certificate-Based

Authentication

7.1.3.

Biometric Authentication

7.1.4.

Passwordless Authentication

7.1.5.

Others

8.

Global IoT Identity

Access Management (IAM) Market Estimates & Forecast Trend Analysis, by

End-use Industry

8.1. Global IoT Identity Access Management (IAM) Market Revenue (US$

Million) Estimates and Forecasts, by End-use Industry, 2021 - 2034

8.1.1.

Manufacturing

8.1.2.

Healthcare

8.1.3.

BFSI

8.1.4.

Retail & E-commerce

8.1.5.

Energy & Utilities

8.1.6.

Automotive

8.1.7.

Government & Defense

8.1.8.

Telecommunications

8.1.9.

Others

9.

North America IoT

Identity Access Management (IAM) Market: Estimates & Forecast Trend

Analysis

9.1. North America IoT Identity Access Management (IAM) Market

Assessments & Key Findings

9.1.1.

North America IoT Identity

Access Management (IAM) Market Introduction

9.1.2.

North America IoT Identity

Access Management (IAM) Market Size Estimates and Forecast (US$ Million) (2021

- 2034)

9.1.2.1.

By Component

9.1.2.2.

By Deployment Mode

9.1.2.3.

By Organization Size

9.1.2.4.

By Authentication Type

9.1.2.5.

By End-use Industry

9.1.2.6.

By Country

9.1.2.6.1.

The U.S.

9.1.2.6.2.

Canada

10. Europe IoT Identity Access Management (IAM) Market: Estimates &

Forecast Trend Analysis

10.1.

Europe IoT Identity Access

Management (IAM) Market Assessments & Key Findings

10.1.1.

Europe IoT Identity Access

Management (IAM) Market Introduction

10.1.2.

Europe IoT Identity Access

Management (IAM) Market Size Estimates and Forecast (US$ Million) (2021 - 2034)

10.1.2.1.

By Component

10.1.2.2.

By Deployment Mode

10.1.2.3.

By Organization Size

10.1.2.4.

By Authentication Type

10.1.2.5.

By End-use Industry

10.1.2.6.

By Country

10.1.2.6.1.

Germany

10.1.2.6.2.

Italy

10.1.2.6.3.

U.K.

10.1.2.6.4.

France

10.1.2.6.5.

Spain

10.1.2.6.6.

Switzerland

10.1.2.6.7.

Rest of Europe

11. Asia Pacific IoT Identity Access Management (IAM) Market: Estimates

& Forecast Trend Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific IoT Identity

Access Management (IAM) Market Introduction

11.1.2.

Asia Pacific IoT Identity

Access Management (IAM) Market Size Estimates and Forecast (US$ Million) (2021

- 2034)

11.1.2.1.

By Component

11.1.2.2.

By Deployment Mode

11.1.2.3.

By Organization Size

11.1.2.4.

By Authentication Type

11.1.2.5.

By End-use Industry

11.1.2.6.

By Country

11.1.2.6.1.

China

11.1.2.6.2.

Japan

11.1.2.6.3.

India

11.1.2.6.4.

Australia

11.1.2.6.5.

South Korea

11.1.2.6.6.

Rest of Asia Pacific

12. Middle East & Africa IoT Identity Access Management (IAM)

Market: Estimates & Forecast Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa IoT Identity

Access Management (IAM) Market Introduction

12.1.2.

Middle East & Africa IoT

Identity Access Management (IAM) Market Size Estimates and Forecast (US$

Million) (2021 - 2034)

12.1.2.1.

By Component

12.1.2.2.

By Deployment Mode

12.1.2.3.

By Organization Size

12.1.2.4.

By Authentication Type

12.1.2.5.

By End-use Industry

12.1.2.6.

By Country

12.1.2.6.1.

UAE

12.1.2.6.2.

Saudi Arabia

12.1.2.6.3.

South Africa

12.1.2.6.4.

Rest of MEA

13. Latin America IoT Identity Access Management (IAM) Market: Estimates

& Forecast Trend Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America IoT Identity

Access Management (IAM) Market Introduction

13.1.2.

Latin America IoT Identity

Access Management (IAM) Market Size Estimates and Forecast (US$ Million) (2021

- 2034)

13.1.2.1.

By Component

13.1.2.2.

By Deployment Mode

13.1.2.3.

By Organization Size

13.1.2.4.

By Authentication Type

13.1.2.5.

By End-use Industry

13.1.2.6.

By Country

13.1.2.6.1.

Brazil

13.1.2.6.2.

Mexico

13.1.2.6.3.

Argentina

13.1.2.6.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global IoT Identity Access

Management (IAM) Market Product Mapping

14.2.

Global IoT Identity Access

Management (IAM) Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

14.3.

Global IoT Identity Access

Management (IAM) Market Tier Structure Analysis

14.4.

Global IoT Identity Access

Management (IAM) Market Concentration & Company Market Shares (%) Analysis,

2025

15. Company Profiles

15.1.

Microsoft Corporation

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

*Similar details would be provided for all

the players mentioned below

15.2.

IBM Corporation

15.3.

Cisco Systems, Inc.

15.4.

Okta, Inc.

15.5.

ForgeRock, Inc.

15.6.

Ping Identity Holding Corp.

15.7.

CyberArk Software Ltd.

15.8.

Thales Group

15.9.

Entrust Corporation

15.10.

One Identity LLC

15.11.

Broadcom Inc.

15.12.

Oracle Corporation

15.13.

SailPoint Technologies

Holdings, Inc.

15.14.

HID Global Corporation

15.15.

DigiCert, Inc.

15.16.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables