IVF Services Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Cycle Type (Fresh IVF Cycles, Thawed IVF Cycles, Donor Egg Cycles), By End-User (Fertility Clinics, Hospitals, Surgical Centers, Clinical Research Institutes), By Patient Age (Under 35, 35-39, 40-42, Over 42), and Geography

2025-12-03

Healthcare

Swetal (Research Analyst)

Description

IVF Services Market Overview

The IVF Services Market is poised for strong and sustained growth from 2025 to 2033, driven by factors such as rising infertility rates due to lifestyle changes, delayed parenthood decisions, increasing awareness and social acceptance of assisted reproductive technology (ART), and significant technological advancements in embryology. The market is projected to be valued at approximately USD 25.1 billion in 2025 and is forecasted to reach nearly USD 48.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.8% during this period.

In Vitro Fertilization (IVF) is a complex series

of procedures used to help with fertility or prevent genetic problems and

assist in the conception of a child. The market's robust expansion is primarily

fueled by the growing prevalence of infertility disorders, influenced by

factors like stress, obesity, smoking, and environmental pollutants. The trend

of postponing pregnancy to later ages for career and educational pursuits is a significant contributor, as female fertility declines

markedly after the age of 35.

Furthermore, progressive government initiatives

in some countries, including insurance coverage and subsidies for IVF

treatments, are making these services more accessible. Technological

innovations such as preimplantation genetic testing (PGT), time-lapse imaging,

and intracytoplasmic sperm injection (ICSI) are improving success rates,

thereby boosting patient confidence and demand. North America and Europe

currently hold significant market shares due to high awareness and favourable

reimbursement policies, while the Asia-Pacific region is expected to witness

the fastest growth due to its large population, improving healthcare

infrastructure, and growing medical tourism.

IVF

Services Market Drivers and Opportunities

Rising Infertility Prevalence and Shifting

Sociodemographic Trends are the Primary Market

Drivers

The increasing global incidence of infertility

is the most powerful driver for the IVF services market. Modern lifestyle

factors, including high levels of stress, sedentary habits, poor nutrition, and

rising obesity rates, are contributing to a higher prevalence of fertility

issues in both men and women. Concurrently, a major sociodemographic shift is

underway, with individuals and couples choosing to have children later in life.

As maternal age advances, the natural probability of conception decreases, leading

a growing number of people to seek ART solutions like IVF. This combination of

a higher baseline need for fertility treatments and a demographic tailwind from

delayed parenthood creates a strong, sustained demand for IVF services

worldwide.

Technological Advancements, Enhancing Success Rates and Patient Experience, are Driving Adoption

Continuous innovation in ART laboratories and

procedures is a critical catalyst for the IVF services market. Technologies

such as PGT for aneuploidy screening allow for the selection of embryos with

the highest chance of implantation, reducing the risk of miscarriage and

genetic disorders. Time-lapse incubation systems enable continuous embryo

monitoring without removing them from a stable culture environment, leading to

better embryo selection. Techniques like ICSI have revolutionized the treatment

of male factor infertility. These advancements directly address the core

concerns of patients—achieving a successful pregnancy in fewer cycles and

reducing the emotional and physical burden of treatment. As success rates

improve and protocols become more refined, the appeal and adoption of IVF

services expand significantly.

Expansion into Untapped Markets and the

Development of Value-Added Services Present Significant Opportunities

The strategic expansion into emerging

geographical markets and the development of specialized, high-value service

lines are creating substantial growth frontiers for the IVF services market.

Key opportunities lie in the rapidly developing economies of Asia-Pacific,

Latin America, and the Middle East, where growing medical tourism, rising

disposable incomes, and gradually improving insurance coverage are unlocking

vast new patient pools. Furthermore, there is immense potential in offering

adjunct services such as comprehensive fertility preservation (egg and sperm

freezing) for individuals undergoing medical treatments or those who wish to

delay childbearing for social reasons. The integration of AI and data analytics

for predicting embryo viability and personalizing treatment protocols

represents a cutting-edge opportunity. For clinics, differentiating through

superior patient-centric care, offering financial plans, and providing holistic

support services are key strategies to capture market share and build brand

loyalty in a competitive landscape.

IVF Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 25.1 Billion |

|

Market Forecast in 2033 |

USD 48.5 Billion |

|

CAGR % 2025-2033 |

8.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Cycle Type ●

By Patient Age ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

IVF Services Market Report Segmentation Analysis

The global IVF

Services Market industry analysis is segmented by Cycle Type, by End-User, by

Patient Age, and by Region.

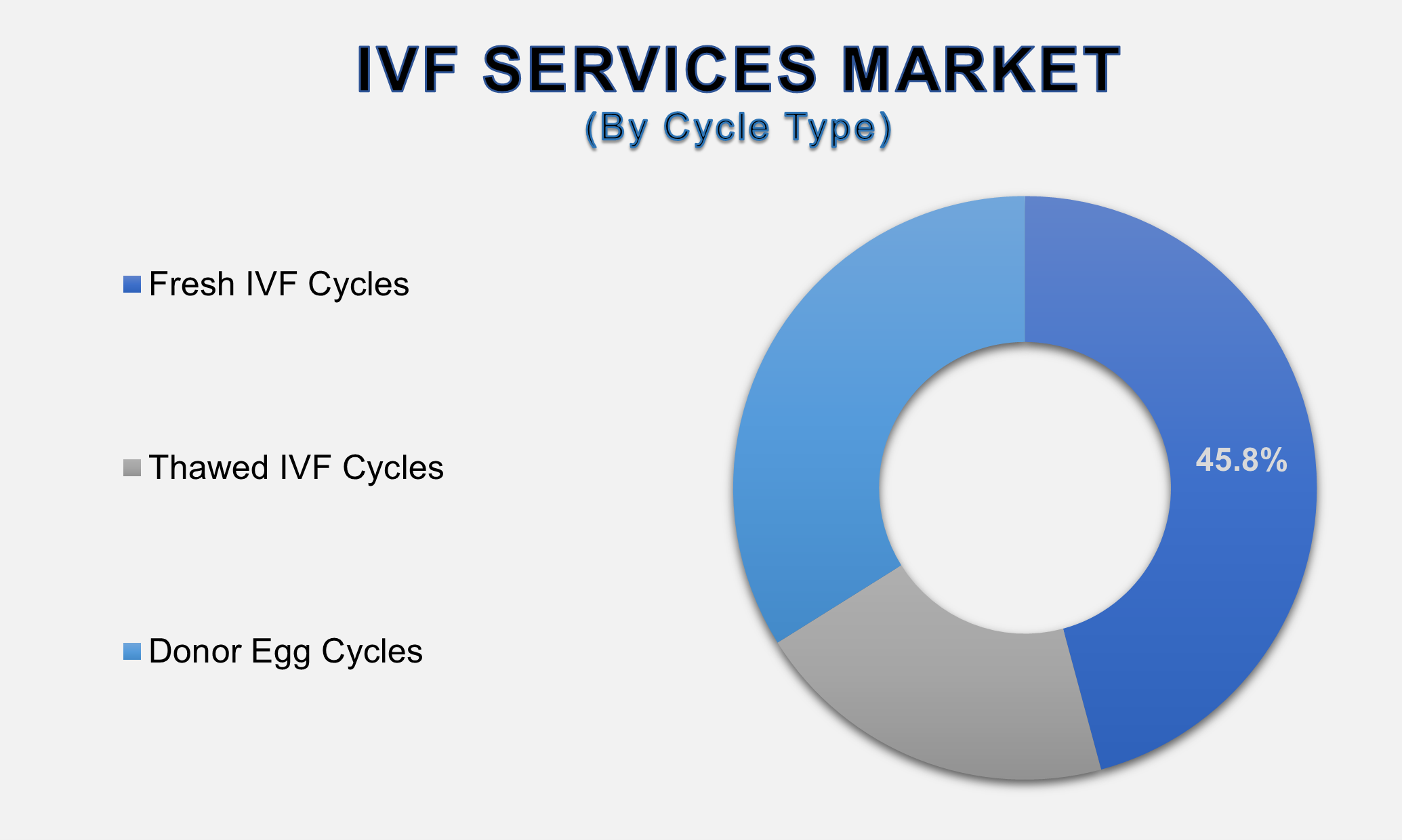

The Fresh IVF

Cycles segment is anticipated to command the largest market share in 2025

The Cycle Type segment is categorized into Fresh IVF Cycles, Thawed IVF Cycles, and Donor Egg

Cycles. The dominance of the Fresh IVF Cycles segment is attributed to its

status as the standard and most commonly initiated treatment protocol for a

majority of first-time IVF patients. In a fresh cycle, eggs are retrieved

and fertilized, and the resulting embryos are

transferred within the same menstrual cycle without being frozen. It is often

the primary approach for couples without specific indications for freezing,

such as those requiring PGT. While frozen embryo transfer (FET) cycles are

growing rapidly due to their high success rates and flexibility, the volume of

fresh cycles remains the foundation of IVF clinic activity, as every patient

undergoing egg retrieval begins with a fresh cycle, securing its position as

the segment with the largest market share.

The 35-39 age group segment is projected to grow at a

significant CAGR.

The Patient Age segment includes Under 35, 35-39, 40-42,

and Over 42. The 35-39 age group's projected significant growth is driven by

the central demographic trend of delayed childbearing. Women in this age

bracket experience a marked decline in ovarian reserve and egg quality, leading

to a significant drop in natural fertility. Consequently, this group represents

a large and rapidly expanding cohort seeking medical assistance to conceive.

Many individuals and couples in this age group have established careers and

financial stability, making them able to afford IVF treatments. They are also

highly motivated to pursue treatment promptly due to the understanding of their

biological clock, making this age segment a critical and fast-growing driver of

demand for IVF services.

The Fertility Clinics end-user segment is projected to

witness the highest growth rate.

The End-User segment is divided into Fertility Clinics,

Hospitals, Surgical Centers, and Clinical Research Institutes. The Fertility

Clinics segment's position as the fastest-growing channel is a direct result of

its specialized nature and focused service

model. These dedicated centers often offer higher success rates due to their

experienced staff, state-of-the-art embryology labs, and high procedural

volume. They provide a comprehensive, patient-centric environment tailored

specifically to the emotional and medical needs of individuals undergoing

fertility treatments. The trend towards chain-owned and branded fertility

clinics, which can leverage economies of scale, invest in the latest

technology, and maintain consistent quality

standards, is further propelling the growth and market share of this segment

compared to general hospitals.

The

following segments are part of an in-depth analysis of the global IVF Services

Market:

|

Market

Segments |

|

|

By Cycle Type |

●

Fresh IVF Cycles ●

Thawed IVF Cycles ●

Donor Egg Cycles |

|

By Patient Age |

●

Under 35 ●

35-39 ●

40-42 ●

Over 42 |

|

By End-user |

●

Fertility Clinics ●

Hospitals ●

Surgical Centers ●

Clinical Research

Institutes |

IVF Services Market Share Analysis by Region

The

Asia-Pacific region is anticipated to hold the largest portion of the IVF

Services Market globally throughout the forecast period.

Asia-Pacific's dominance is driven by a confluence of

powerful factors: a massive population base, a high prevalence of infertility,

rapidly improving healthcare infrastructure, and the emergence of the region as

a global hub for medical tourism. Countries like India, China, and Japan have

large patient pools, and growing awareness is reducing the social stigma

associated with infertility treatments. The cost of IVF procedures in countries

like India and Thailand is significantly lower than in Western countries,

attracting international patients ("reproductive tourism").

Furthermore, governments in some APAC countries are beginning to implement

supportive policies to address declining birth rates, which is expected to

further stimulate the market. The presence of a large number of skilled medical

professionals and a competitive clinic landscape also contributes to the

region's leadership.

India alone is a key growth engine within the APAC region.

The country offers a highly favorable cost

structure without compromising on quality, with treatment costs being a

fraction of those in the US or Europe. This has made it a premier destination

for medical tourism. A growing middle class with increasing disposable income

is making IVF treatments more accessible to the domestic population. The

presence of numerous highly qualified fertility specialists and technologically

advanced clinics in major metropolitan areas creates a robust and expanding

market ecosystem. Increasing media coverage and public discourse about

fertility are also normalizing the use of these services.

IVF Services Market Competition Landscape Analysis

The global IVF

services market is competitive and fragmented, featuring a mix of large

international chains, regional players, and standalone clinics. Competition is

based on clinical success rates, service quality, technological capabilities,

brand reputation, and cost. Key strategies include geographic expansion through

acquisitions and partnerships, heavy investment in the latest ART technologies

(e.g., PGT, time-lapse systems), and focusing on patient experience and support

services. The market also sees competition from local clinics that compete

effectively on price and personalized care.

Global IVF Services Market Recent Developments News:

- In February 2025, IVI RMA announced a strategic

partnership with a leading healthcare group in Southeast Asia to open a

new state-of-the-art fertility clinic in Singapore.

- In December 2024, Virtus Health launched a new

AI-based embryo selection platform across its network of clinics in

Australia and Europe to improve implantation rates.

- In October 2024, The Cooper Companies

(CooperSurgical) acquired a specialized media company to enhance its

portfolio of products and services for IVF laboratories.

- In August 2024, Monash IVF Group reported

successful pilot program results for a new, less invasive endometrial

receptivity test, aiming to improve outcomes for patients with recurrent

implantation failure.

The Global IVF Services Market Is Dominated by a

Few Large Companies, such as

●

IVI RMA

●

Virtus Health

●

The Cooper Companies

Inc. (CooperSurgical)

●

Monash IVF Group

●

CARE Fertility

●

Boston IVF

●

FUJIFILM Irvine

Scientific

●

Cook Medical

●

Genea Biomedx

●

Progyny, Inc.

●

Institut Méric

●

INVO Bioscience

●

Shanghai United Family

Hospital

●

Bloom IVF Group

●

Repromed Limited

●

Panthea Bioscience (a

subsidiary of Gedeon Richter)

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global IVF Services Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

IVF Services Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global IVF Services Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Cycle Type of Global IVF

Services Market

1.3.2.Patient Age of Global IVF

Services Market

1.3.3.End-user of Global IVF

Services Market

1.3.4.Region of Global IVF

Services Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Overview

of Global IVF Treatment and Access

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

IVF Services Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

IVF Services Market Estimates

& Forecast Trend Analysis, by Cycle Type

4.1.

Global

IVF Services Market Revenue (US$ Bn) Estimates and Forecasts, by Cycle Type,

2020 - 2033

4.1.1.Fresh IVF Cycles

4.1.2.Thawed IVF Cycles

4.1.3.Donor Egg Cycles

5. Global

IVF Services Market Estimates

& Forecast Trend Analysis, by Patient Age

5.1.

Global

IVF Services Market Revenue (US$ Bn) Estimates and Forecasts, by Patient Age, 2020

- 2033

5.1.1.Under 35

5.1.2.35-39

5.1.3.40-42

5.1.4.Over 42

6. Global

IVF Services Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

IVF Services Market Revenue (US$ Bn) Estimates and Forecasts, by End-user 2020

- 2033

6.1.1.Fertility Clinics

6.1.2.Hospitals

6.1.3.Surgical Centers

6.1.4.Clinical Research

Institutes

7. Global

IVF Services Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

IVF Services Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 -

2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America IVF

Services Market: Estimates &

Forecast Trend Analysis

8.1. North America IVF Services

Market Assessments & Key Findings

8.1.1.North America IVF Services

Market Introduction

8.1.2.North America IVF Services

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Cycle Type

8.1.2.2.

By Patient Age

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe IVF

Services Market: Estimates &

Forecast Trend Analysis

9.1. Europe IVF Services Market

Assessments & Key Findings

9.1.1.Europe IVF Services Market

Introduction

9.1.2.Europe IVF Services Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Cycle Type

9.1.2.2.

By Patient Age

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific IVF

Services Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific IVF Services Market Introduction

10.1.2.

Asia

Pacific IVF Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Cycle Type

10.1.2.2.

By Patient Age

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa IVF

Services Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

IVF Services Market Introduction

11.1.2. Middle

East & Africa

IVF Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Cycle Type

11.1.2.2.

By Patient Age

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

IVF Services Market: Estimates &

Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America IVF Services

Market Introduction

12.1.2. Latin America IVF Services

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Cycle Type

12.1.2.2.

By Patient Age

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global IVF Services Market

Product Mapping

14.2. Global IVF Services Market

Concentration Analysis, by Leading Players / Innovators / Emerging Players /

New Entrants

14.3. Global IVF Services Market

Tier Structure Analysis

14.4. Global IVF Services Market

Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

IVI RMA

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Virtus Health

15.3.

The Cooper Companies Inc. (CooperSurgical)

15.4.

Monash IVF Group

15.5.

CARE Fertility

15.6.

Boston IVF

15.7.

FUJIFILM Irvine Scientific

15.8.

Cook Medical

15.9.

Genea Biomedx

15.10.

Progyny, Inc.

15.11.

Institut Méric

15.12.

INVO Bioscience

15.13.

Shanghai United Family Hospital

15.14.

Bloom IVF Group

15.15.

Repromed Limited

15.16.

Panthea Bioscience

15.17.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables