Linerless Labels Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Adhesion Type (Permanent, Removable, Repositionable, Others), By Printing Technologies (Direct Thermal, Thermal Transfer, Laser, Inkjet, Others), By Application (Food & Beverage, Pharmaceutical & Personal Care, Retail, Logistics, Others), By Component (Facestock, Adhesive, Release Coating), and Geography

2025-12-18

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Linerless

Labels Market Overview

The Global Linerless Labels Market is projected to reach USD 2.5 billion by 2033, up from USD 1.6 billion in 2025, registering a CAGR of 6.1% during 2025–2033. The market is witnessing robust expansion as industries increasingly shift toward sustainable labeling technologies that reduce waste, enhance efficiency, and minimize overall production costs. Linerless labels, which eliminate the need for traditional release liners, offer a more environmentally friendly solution and enable higher label roll capacity, reducing downtime and material usage. As global sustainability regulations tighten and companies adopt eco-friendly packaging standards, linerless labels are emerging as a preferred alternative across multiple end-use industries, including food & beverage, retail, and logistics.

Growing adoption of automation in

packaging lines, advancements in thermal printing technologies, and rising

e-commerce activities further support market growth. Food & beverage

manufacturers remain the largest adopters due to increasing demand for efficient

labeling solutions with excellent adhesion and temperature resistance.

Linerless

Labels Market Drivers and Opportunities

Rising Adoption of Sustainable

and Cost-Efficient Packaging Solutions Is Driving Market Growth

The demand for sustainable

labeling solutions is one of the primary drivers boosting the linerless labels

market worldwide. With global regulations emphasizing waste reduction,

recyclability, and resource efficiency, industries are increasingly shifting away

from liner-backed labels, which generate tons of silicone-coated paper waste

annually. Linerless labels eliminate liner disposal requirements, offering

companies significant environmental and financial benefits. These labels also

enable greater space utilization, allowing more labels per roll, reducing

changeovers, lowering transportation costs, and improving operational

efficiency in high-volume packaging lines.

In addition, the strong consumer

and regulatory push toward sustainability is compelling brands to adopt

packaging that aligns with circular economy principles. The rise of green

manufacturing and carbon footprint reduction initiatives is accelerating investment

in linerless labeling technology. Industries such as food, retail, and

logistics appreciate the cost savings stemming from reduced raw material usage,

simpler handling, and fewer workplace injuries associated with liner waste. As

environmental, operational, and economic advantages converge, linerless labels

are becoming an essential component of modern packaging ecosystems, supporting

long-term market expansion.

Increasing Demand from Food

& Beverage and E-Commerce Industries Fuels Market Expansion

The expanding global food &

beverage sector, paired with rapid growth in e-commerce and omnichannel retail,

is a major force driving linerless label adoption. Food manufacturers rely

heavily on linerless labels for pricing, shelf marking, weigh-scale labeling,

and product identification due to their superior adhesion, resistance to

moisture, and compatibility with cold-chain logistics. The surge in

ready-to-eat meals, packaged foods, and delivery-based consumption patterns is

driving a substantial increase in labeling volume, significantly benefiting the

market. At the same time, the logistics and retail industries are experiencing

exponential growth driven by online shopping and last-mile delivery. Linerless

labels provide efficiency in warehouse labeling, shipping, and inventory

management, offering high-speed printing and excellent scannability. Thermal

printing technologies, especially direct thermal, enable fast, on-demand label

creation without the need for ribbons or toners, making them ideal for fast-moving

logistics operations. As global trade expands and supply chain digitization

accelerates, linerless labels will continue to see strong momentum across

distribution centers, fulfillment hubs, and retail environments.

Technological Advancements in

Printing and Labeling Equipment Create Significant Opportunities

Advancements in thermal printing,

adhesive formulations, and facestock durability are opening new growth avenues

for the linerless labels market. Direct thermal and thermal transfer printing

technologies have significantly evolved, allowing high-resolution, long-lasting

images suitable for critical applications such as pharmaceutical labeling,

perishable food tracking, and logistics documentation. Improvements in inkjet

and laser printing compatibility are further expanding the range of substrates

suitable for linerless labels. Additionally, manufacturers are developing

innovative facestock materials that offer enhanced heat and abrasion

resistance, improved tensile strength, and greater versatility for both indoor

and outdoor applications. The evolution of repositionable and high-performance

adhesives is also enabling wider adoption in sectors requiring label

flexibility and reusability. Equipment manufacturers are integrating advanced

sensors, automatic cutters, and real-time monitoring features into linerless

label applicators, increasing efficiency and reducing downtime. These

technological innovations are expected to unlock new opportunities across

high-volume manufacturing and regulated industries in the coming years.

Linerless Labels Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 1.6 Billion |

|

Market Forecast in 2033 |

USD 2.5 Billion |

|

CAGR % 2025-2033 |

6.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Adhesion Type ●

By Printing

Technologies ●

By Application ●

By Component |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Linerless Labels Market Report Segmentation Analysis

The global Linerless Labels

Market industry analysis is segmented by Adhesion Type, by Printing

Technologies, by Application, by Component, and by region.

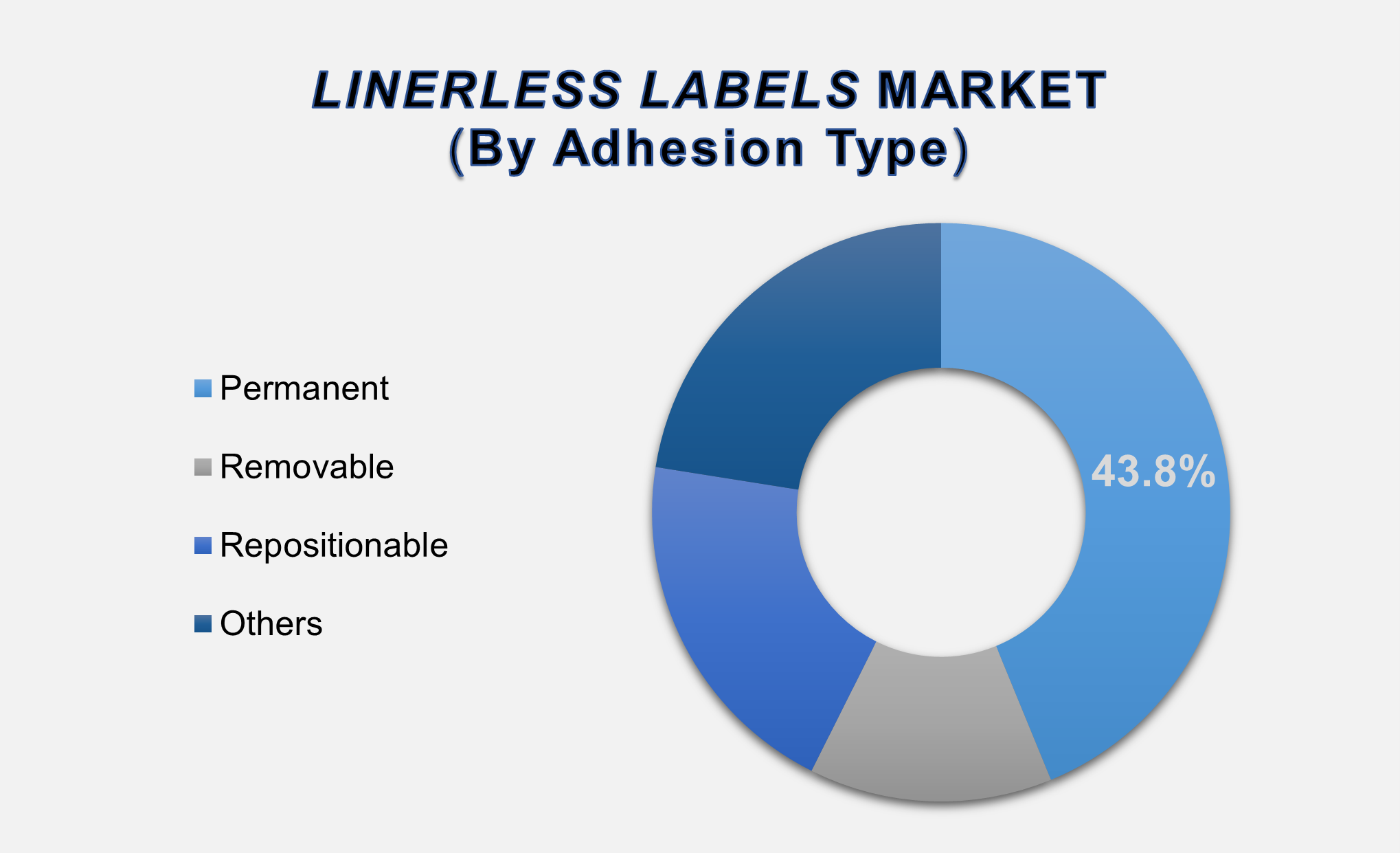

Permanent Adhesion Type

Segment Accounted for the Largest Market Share in the Global Linerless Labels

Market

By adhesion type, the market is categorized into Permanent, Removable, Repositionable, and Others. The Permanent segment dominated the global market in 2025, accounting for 43.8% of total revenue. Permanent linerless labels are preferred for applications requiring strong, long-lasting adhesion, particularly in the food & beverage and logistics sectors. Their ability to withstand moisture, temperature changes, and handling makes them ideal for packaging, shipping, and retail environments. Increasing demand for durable labeling solutions in high-volume packaging operations and advancements in adhesive chemistry continue to reinforce the segment’s leadership.

Direct Thermal Printing

Technology Accounted for the Largest Market Share in 2025

By printing technology, the

market includes Direct Thermal, Thermal Transfer, Laser, Inkjet, and Others.

The Direct Thermal segment leads the market due to its cost efficiency, high

printing speed, and compatibility with linerless label rolls. It is widely used

in retail point-of-sale systems, logistics operations, and food labeling due to

its ease of use and elimination of ribbons or toners. Rapid growth in

e-commerce, inventory tracking, and weigh-scale labeling further contributes to

the strong adoption of direct thermal printing technology in linerless label

applications.

Food & Beverage

Application Segment Held the Largest Market Share Globally

By application, the market is

divided into Food & Beverage, Pharmaceutical & Personal Care, Retail,

Logistics, and Others. The Food & Beverage segment dominated the global

market in 2025. Linerless labels are extensively used in food packaging for

pricing, product identification, and regulatory compliance. Their eco-friendly

nature, cost-effectiveness, and ability to perform well under varying storage

conditions make them a preferred choice for fresh produce, frozen foods, and

ready meals. Rising demand for packaged food and growing emphasis on efficient

labeling systems further propel the segment’s significant share.

The following segments are

part of an in-depth analysis of the global Linerless Labels Market:

|

Market

Segments |

|

|

By Adhesion Type |

●

Permanent ●

Removable ●

Repositionable ●

Others |

|

By Printing

Technologies |

●

Direct Thermal ●

Thermal Transfer ●

Laser ●

Inkjet ●

Others |

|

By Application |

●

Food & Beverage ●

Pharmaceutical &

Personal Care ●

Retail ●

Logistics ●

Others |

|

By Component |

●

Facestock ●

Adhesive ●

Release Coating |

Linerless

Labels Market Share Analysis by Region

The

Asia-Pacific region is projected to hold the largest share of the global

Linerless Labels market over the forecast period.

The Asia-Pacific (APAC) region

accounted for the largest share of 41.4% in the global linerless labels market

in 2025. The region’s dominance is driven by rapid industrialization, expanding

food manufacturing activity, and strong growth in retail and e-commerce sectors

across China, India, Japan, and Southeast Asia. Additionally, rising

sustainability initiatives and investments in automated packaging technologies

are accelerating the adoption of linerless labeling solutions in APAC.

North America is expected to grow

at the highest CAGR during the forecast period. The region’s growth is driven

by advanced retail infrastructures, increased adoption of smart labeling

solutions, and stringent regulatory standards promoting waste reduction and

sustainable packaging. Strong technological innovation and the presence of

major retail chains continue to support the region’s expanding market

potential.

Linerless Labels Market Competition Landscape Analysis

The global

linerless labels market is moderately competitive, with major players focusing

on sustainability initiatives, product innovation, and expansion of thermal

printing capabilities. Companies are investing in high-performance adhesive

technologies, durable facestock materials, and automated linerless applicators

to cater to diverse industry requirements.

Global Linerless Labels Market Recent Developments News:

- In May 2021, CCL Industries

acquired Lux Global Label Asia Pte Ltd, rebranding the entity as CCL Label

Singapore to strengthen its presence and capabilities in the Asian

labeling market.

- In February 2021, Avery

Dennison introduced its recycled PET (rPET) liner portfolio in Europe,

featuring four labeling constructions designed to support brand

sustainability goals and circular packaging initiatives.

The Global Linerless Labels Market is dominated by a

few large companies, such as

●

Avery Dennison

●

CCL Industries

●

Multi-Color

Corporation

●

UPM Raflatac

●

Coveris Holdings

●

SATO Holdings

●

Zebra Technologies

●

Herma GmbH

●

Ravenwood Packaging

●

Reflex Labels

●

Gipako

●

ImageTek Labels

●

Lintec Corporation

●

Lecta Group

●

PMC Label

●

Stickythings

●

Label Logic

●

Advanced Labels

●

L&N Label Company

●

Primary Labels

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Linerless Labels

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Linerless Labels Market Scope and Market Estimation

1.2.1.Global Linerless Labels

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Linerless Labels

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Adhesion Type of Global Linerless

Labels Market

1.3.2.Printing Technologies of

Global Linerless Labels Market

1.3.3.Application of Global Linerless

Labels Market

1.3.4.Component of Global Linerless

Labels Market

1.3.5.Region of Global Linerless

Labels Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Linerless Labels Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Linerless Labels Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Linerless Labels

Market Estimates & Forecast Trend

Analysis, by Adhesion Type

4.1.

Global

Linerless Labels Market Revenue (US$ Bn) Estimates and Forecasts, by Adhesion

Type, 2020 - 2033

4.1.1.Removable

4.1.2.Repositionable

4.1.3.Others

5.

Global Linerless Labels

Market Estimates & Forecast Trend

Analysis, by Printing Technologies

5.1.

Global

Linerless Labels Market Revenue (US$ Bn) Estimates and Forecasts, by Printing

Technologies, 2020 - 2033

5.1.1.Direct Thermal

5.1.2.Thermal Transfer

5.1.3.Laser

5.1.4.Inkjet

5.1.5.Others

6.

Global Linerless Labels

Market Estimates & Forecast Trend

Analysis, by Application

6.1.

Global

Linerless Labels Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Food & Beverage

6.1.2.Pharmaceutical &

Personal Care

6.1.3.Retail

6.1.4.Logistics

6.1.5.Others

7.

Global Linerless Labels

Market Estimates & Forecast Trend

Analysis, by Component

7.1.

Global

Linerless Labels Market Revenue (US$ Bn) Estimates and Forecasts, by Component,

2020 - 2033

7.1.1.Facestock

7.1.2.Adhesive

7.1.3.Release Coating

8. Global

Linerless Labels Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Linerless Labels Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

9. North America Linerless

Labels Market: Estimates & Forecast

Trend Analysis

9.1.

North

America Linerless Labels Market Assessments & Key Findings

9.1.1.North America Linerless

Labels Market Introduction

9.1.2.North America Linerless

Labels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Adhesion

Type

9.1.2.2. By Printing

Technologies

9.1.2.3. By Application

9.1.2.4. By Component

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Linerless

Labels Market: Estimates & Forecast

Trend Analysis

10.1.

Europe

Linerless Labels Market Assessments & Key Findings

10.1.1.

Europe

Linerless Labels Market Introduction

10.1.2.

Europe

Linerless Labels Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Adhesion

Type

10.1.2.2. By Printing

Technologies

10.1.2.3. By Application

10.1.2.4. By Component

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Linerless

Labels Market: Estimates & Forecast

Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Linerless Labels Market Introduction

11.1.2.

Asia

Pacific Linerless Labels Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Adhesion

Type

11.1.2.2. By Printing

Technologies

11.1.2.3. By Application

11.1.2.4. By Component

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Linerless

Labels Market: Estimates & Forecast

Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Linerless Labels Market Introduction

12.1.2.

Middle East & Africa Linerless Labels Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Adhesion

Type

12.1.2.2. By Printing

Technologies

12.1.2.3. By Application

12.1.2.4. By Component

12.1.2.5.

By

Country

12.1.2.5.1. South

Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi

Arabia

12.1.2.5.4. Rest

of MEA

13. Latin America

Linerless Labels Market: Estimates

& Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Linerless Labels Market Introduction

13.1.2.

Latin

America Linerless Labels Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

13.1.2.1. By Adhesion

Type

13.1.2.2. By Printing

Technologies

13.1.2.3. By Application

13.1.2.4. By Component

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Linerless Labels Market Product Mapping

15.2.

Global

Linerless Labels Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

15.3.

Global

Linerless Labels Market Tier Structure Analysis

15.4.

Global

Linerless Labels Market Concentration & Company Market Shares (%) Analysis,

2023

16.

Company

Profiles

16.1. Avery

Dennison

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2. CCL

Industries

16.3. Multi-Color

Corporation

16.4. UPM Raflatac

16.5. Coveris

Holdings

16.6. SATO Holdings

16.7. Zebra

Technologies

16.8. Herma GmbH

16.9. Ravenwood

Packaging

16.10. Reflex Labels

16.11. Gipako

16.12. ImageTek

Labels

16.13. Lintec

Corporation

16.14. Lecta Group

16.15. PMC Label

16.16. Stickythings

16.17. Label Logic

16.18. Advanced

Labels

16.19. L&N Label

Company

16.20. Primary

Labels

16.21. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables