Medical Electronics Market Size and Forecast (2020-2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Patient Monitoring Devices, Diagnostic Devices, Therapeutic Devices, Imaging Systems), By Component (Sensors, Batteries, Microprocessors/MCU, Displays, ASICs/FPGAs), By End-User (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Home Care Settings), and Geography

2025-12-02

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Medical Electronics Market Overview

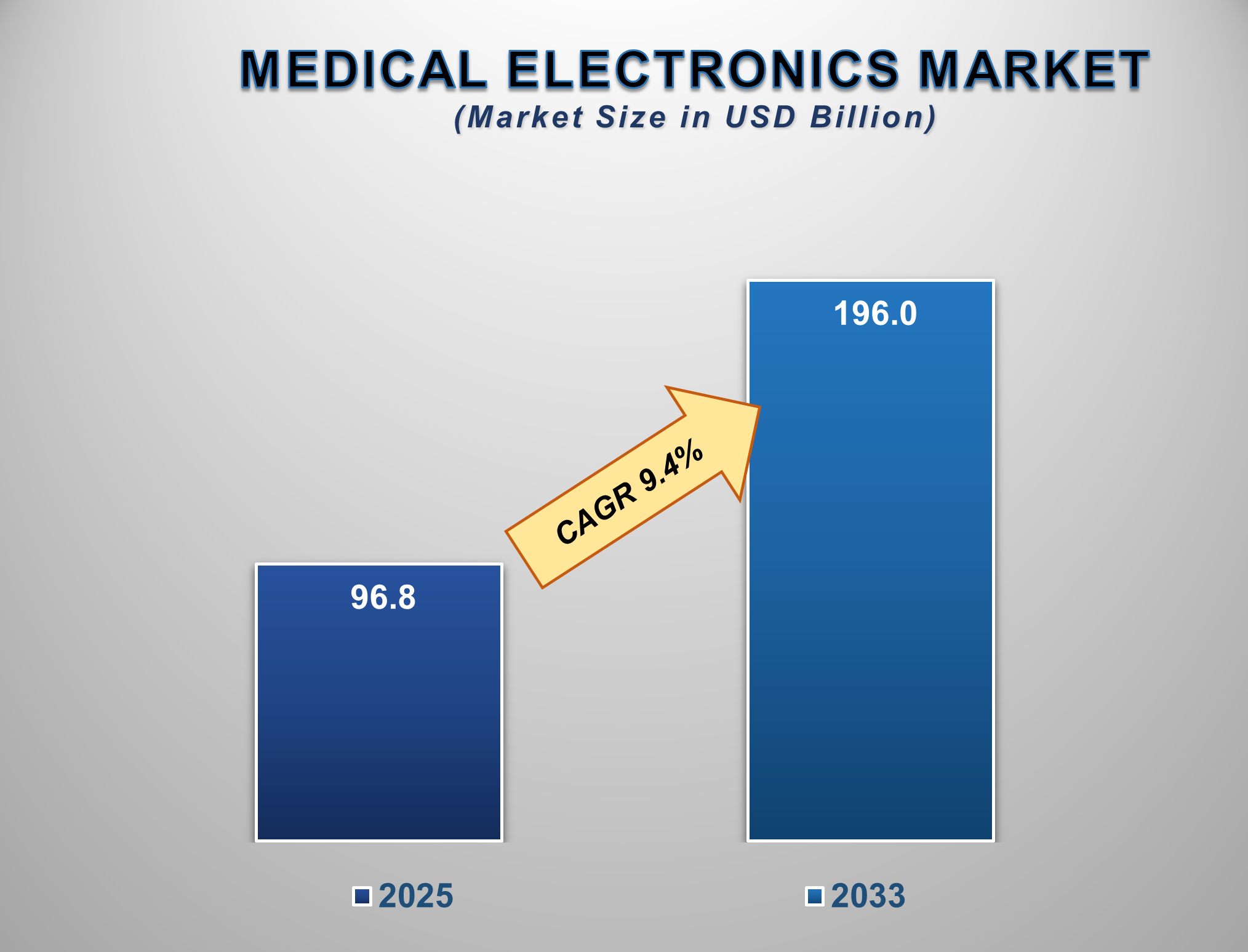

The Medical Electronics Market is poised for a period of explosive and transformative growth from 2025 to 2033, fueled by the global convergence of healthcare and digital technology, the rising prevalence of chronic diseases, and an escalating demand for advanced, personalized, and accessible medical care. The market is projected to be valued at approximately USD 96.8 billion in 2025 and is forecasted to reach nearly USD 196.0 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 9.4% during this period.

Medical electronics encompass the electronic

components, devices, and systems used for the diagnosis,

monitoring, and treatment of medical conditions. The market's robust expansion

is primarily driven by the technological revolution in healthcare, including

the proliferation of IoT-enabled devices, AI-powered diagnostics, and minimally

invasive surgical systems. The growing geriatric population, which requires

more frequent medical monitoring and intervention, is a key demographic driver.

Furthermore, increasing health awareness among consumers, supportive government

initiatives for digital health infrastructure, and the pressing need to reduce

healthcare costs through early diagnosis and remote patient management are

significantly contributing to market growth. North America currently holds the

largest market share due to high healthcare expenditure and early technology

adoption, while the Asia-Pacific region is expected to witness the fastest

growth, driven by its massive patient population, improving healthcare access,

and rising medical tourism.

Medical

Electronics Market Drivers and Opportunities

The Rising Burden of Chronic Diseases and the

Aging Global Population is the Primary Market Driver

The escalating global incidence of chronic

conditions such as cardiovascular diseases, diabetes, and respiratory disorders

is the most significant force propelling the medical electronics market. These

diseases require long-term management, continuous monitoring, and frequent

diagnostic procedures, creating a sustained demand for electronic medical

devices. Coupled with this is the demographic shift towards an older

population, which is inherently more susceptible to such chronic ailments and

age-related health issues. This dual pressure is straining traditional

healthcare systems, creating an urgent need for efficient, cost-effective

solutions. Medical electronics, particularly in the form of remote patient

monitoring systems and advanced diagnostic imaging, offer a pathway to manage

this burden by enabling proactive care, reducing hospital readmissions, and

facilitating early intervention. This clinical and economic imperative provides

a solid, long-term foundation for sustained market growth.

The global incidence of chronic conditions,

often referred to as non-communicable diseases (NCDs), represents a paramount

public health crisis and is the leading cause of death and disability

worldwide. According to the World Health Organization (WHO), NCDs are

responsible for a staggering 74% of all global deaths annually, equivalent

to 41 million people. The burden is not confined to high-income nations; over

three-quarters of these deaths occur in low- and middle-income countries. This surge is fueled by

aging populations and urbanization. The economic impact is profound, with

projections suggesting cumulative economic losses from NCDs could

exceed $47 trillion by 2030. This data underscores the urgent need for

robust global health strategies focused on prevention and control to curb this

escalating crisis.

The Technological Convergence and

Digitalization of Healthcare is Driving Adoption

The rapid integration of technologies like

Artificial Intelligence (AI), the Internet of Medical Things (IoMT), and big

data analytics into medical devices is a powerful catalyst for the medical

electronics market. This convergence is leading to a new generation of

"smart" devices that are more accurate, connected, and intelligent.

AI algorithms enhance the diagnostic capabilities of imaging systems, IoMT

enables seamless data flow from wearable monitors to electronic health records,

and miniaturized electronics facilitate the development of implantable and

ingestible devices. This digital transformation empowers healthcare providers

with data-driven insights, improves patient outcomes, and enhances operational

efficiency. The shift from episodic care to continuous, connected health

management is driving the widespread adoption of advanced medical electronics

across the care continuum.

The Expansion of Home-Based Healthcare and

the Emergence of Personalized Medicine Present Significant Opportunities

The strategic development of devices for

decentralized care and the tailoring of medical treatment are creating significant growth frontiers for the medical

electronics market. Key opportunities lie in the booming segment of home-use

medical devices, driven by patient preference for comfort and the need to

reduce healthcare costs. This includes connected glucose monitors, smart

inhalers, wearable ECG patches, and portable dialysis machines. Furthermore,

the rise of personalized medicine, which uses diagnostic data to tailor

therapies to individual patients, is fueling demand for advanced genomic

sequencing instruments, point-of-care testing devices, and minimally invasive

surgical robots that allow for precision interventions. For manufacturers,

investing in user-centric design for home-care devices, developing

sophisticated sensors for new biomarkers, and creating interoperable systems

that integrate into larger digital health platforms are key strategies to

capture untapped market potential.

Medical Electronics

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 96.8 Billion |

|

Market Forecast in 2033 |

USD 196.0 Billion |

|

CAGR % 2025-2033 |

9.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Product ●

By Component ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Medical Electronics

Market Report Segmentation Analysis

The global Medical Electronics

Market industry analysis is segmented by Product, by Component, by End-User,

and by Region.

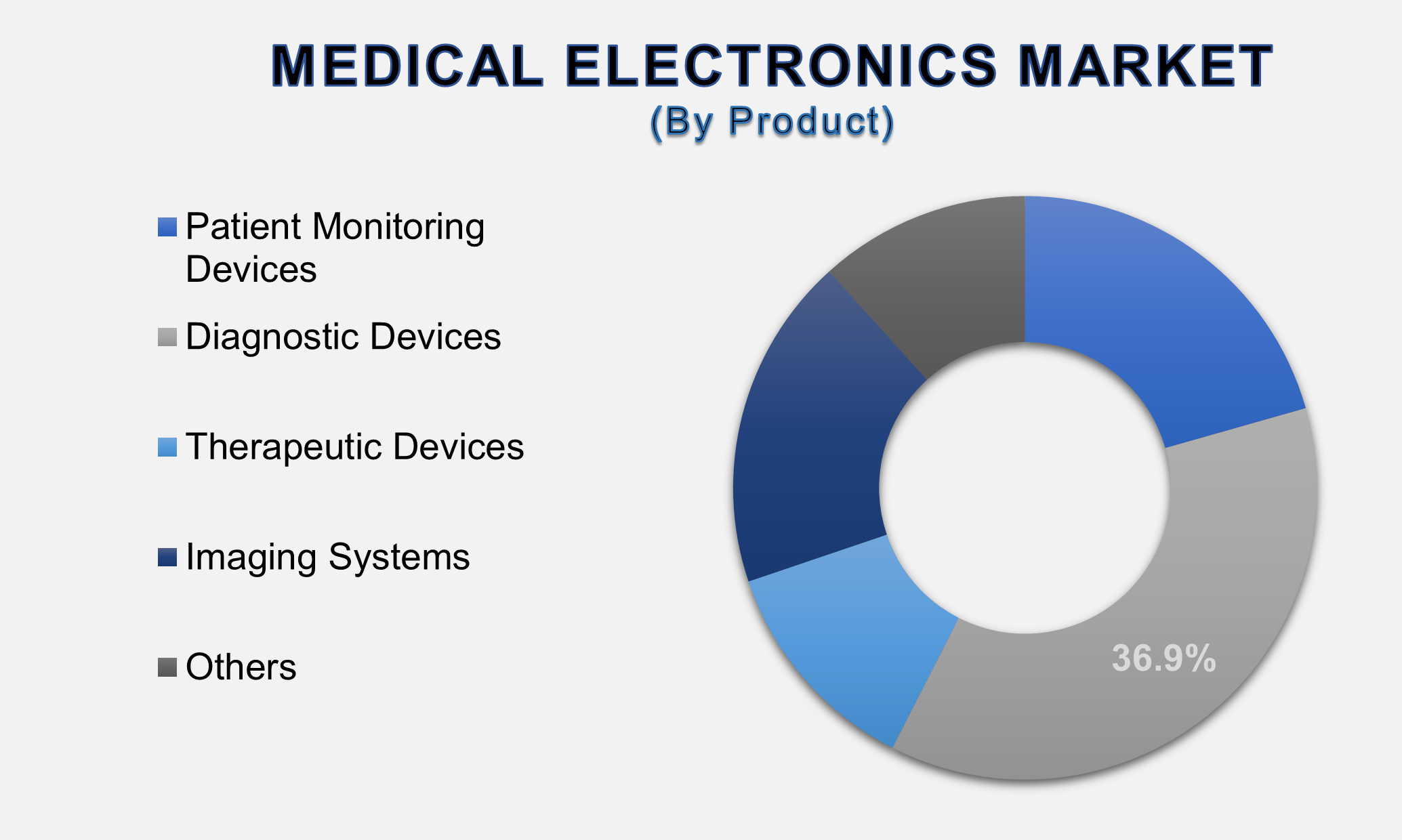

The Diagnostic Devices

product segment is anticipated to command the largest market share in 2025

The Product segment is categorized

into Patient Monitoring Devices, Diagnostic Devices, Therapeutic Devices, and

Imaging Systems. The dominance of the diagnostic devices segment is attributed

to the fundamental role of diagnostics in all aspects of healthcare, from

initial disease detection to treatment monitoring. This segment includes a wide

range of electronic equipment, such as ECG

machines, EEG systems, blood gas analyzers, and point-of-care testing devices.

The high and consistent volume of diagnostic procedures performed globally,

coupled with the continuous technological advancements that improve accuracy

and speed (e.g., digital PCR, next-generation sequencing), sustains this

segment's leadership. The critical need for accurate and early diagnosis to

enable effective treatment and control healthcare costs ensures that diagnostic

devices remain the cornerstone of the medical electronics market.

The Sensors component segment is projected to

grow at a significant CAGR.

The Component segment includes Sensors,

Batteries, Microprocessors/MCU, Displays, and ASICs/FPGAs. The sensor

segment's projected significant growth is a direct result of its function as the critical interface between the patient and

the medical device. Sensors are the enabling technology for virtually every

modern medical electronic device, converting physiological parameters (e.g.,

heart rate, blood pressure, oxygen saturation, glucose level) into electronic

signals. The proliferation of wearable monitors, implantable devices, and smart

home-care systems is driving demand for smaller, more accurate, lower-power,

and more specialized sensors. Innovations in MEMS (Micro-Electro-Mechanical

Systems) technology, biosensors, and flexible electronics are creating new

sensing capabilities, making this component the fastest-growing and most

innovation-intensive part of the market.

The Home Care Settings end-user segment is

projected to witness the highest growth rate.

The End-User segment is divided into Hospitals,

Diagnostic Centers, Ambulatory Surgical Centers, and Home Care Settings. The

Home Care Settings segment's position as the fastest-growing channel is firmly

rooted in the powerful trend of healthcare decentralization. Driven by an aging

population, the prevalence of chronic diseases, and pressure to reduce

hospitalization costs, there is a massive shift towards managing health at

home. This is enabled by a new generation of user-friendly, connected medical electronics,

such as remote patient monitoring kits, smart pill dispensers, and wearable

vital signs monitors. The convenience for patients, the ability to generate

continuous real-world health data, and the overall reduction in healthcare

expenditure are powerful forces propelling the explosive growth of medical

electronics in the home care environment.

The following segments are part of an in-depth analysis of

the global Medical Electronics Market:

|

Market

Segments |

|

|

By Product |

●

Patient Monitoring

Devices ●

Diagnostic Devices ●

Therapeutic Devices ●

Imaging Systems ●

Others |

|

By Component |

●

Sensors ●

Batteries ●

Microprocessors/MCU ●

Displays ●

ASICs/FPGAs |

|

By End-user |

●

Hospitals ●

Diagnostic Centers ●

Ambulatory Surgical

Centers ●

Home Care Settings |

Medical Electronics

Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Medical Electronics Market

globally throughout the forecast period.

North America's dominance is attributed to its

high healthcare expenditure, strong presence of leading medical device and

electronics manufacturers, and a robust regulatory framework that both ensures

safety and fosters innovation. The region has a high adoption rate for advanced

medical technologies, supportive reimbursement policies for many electronic

medical devices, and a well-established healthcare infrastructure. The presence

of major technology firms entering the digital health space further accelerates

regional growth. High awareness levels among both clinicians and patients about

the benefits of advanced medical electronics solidify North America's leading

position.

The United States, in particular, is the world's

largest single market for medical electronics, driven by factors such as the

high cost of healthcare, which incentivizes efficiency-saving technologies, a

significant burden of chronic diseases, and substantial R&D investment from

both private and public sectors. Regulatory pathways through the FDA, while

rigorous, provide a clear framework for commercialization. The strong venture

capital ecosystem also fuels innovation and the growth of startups in the medtech

space, ensuring a continuous pipeline of new electronic medical devices.

Medical Electronics

Market Competition Landscape Analysis

The global medical electronics

market is highly competitive and innovation-driven, featuring a mix of

established medical device OEMs (Original Equipment Manufacturers), specialized

electronic component suppliers, and emerging technology companies. Competition

is intense and centers on technological leadership, product reliability and

miniaturization, regulatory compliance, and deep clinical relationships. Key

strategies include heavy investment in R&D for next-generation products,

strategic mergers and acquisitions to acquire new technologies or expand market

reach, and partnerships with software companies to enhance device connectivity

and data analytics capabilities. The market also sees increasing competition

from consumer electronics companies moving into the health and wellness

monitoring space.

Global Medical

Electronics Market Recent Developments News:

- In January 2025, Medtronic plc received FDA

approval for its next-generation insertable cardiac monitor with an

AI-powered algorithm for improved atrial fibrillation detection.

- In November 2024, Siemens Healthineers launched a

new mobile C-arm system with enhanced image processing and a lower radiation dose, targeting growing

ambulatory surgical centers.

- In September 2024, Texas Instruments introduced a

new family of ultra-low-power system-on-chips (SoCs) specifically designed

for miniaturized, long-lasting wearable medical patches.

- In July 2024, Philips and Roche announced a strategic collaboration

to develop integrated solutions that connect Philips' patient monitoring

platforms with Roche's diagnostic insights to support clinical

decision-making in the ICU.

The Global Medical

Electronics Market Is Dominated by a Few Large Companies, such as

●

Medtronic plc

●

Siemens Healthineers

AG

●

Philips N.V.

●

GE Healthcare

●

Abbott Laboratories

●

Texas Instruments

Incorporated

●

Analog Devices, Inc.

●

STMicroelectronics

N.V.

●

NXP Semiconductors

N.V.

●

Renesas Electronics

Corporation

●

Microchip Technology

Inc.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Medical Electronics

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Medical Electronics Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Medical Electronics

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product of Global Medical

Electronics Market

1.3.2.Component of Global Medical

Electronics Market

1.3.3.End-user of Global Medical

Electronics Market

1.3.4.Region of Global Medical

Electronics Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Key

Developments

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Medical Electronics Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Medical Electronics Market Estimates

& Forecast Trend Analysis, by Product

4.1.

Global

Medical Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Product,

2020 - 2033

4.1.1.Patient Monitoring Devices

4.1.2.Diagnostic Devices

4.1.3.Therapeutic Devices

4.1.4.Imaging Systems

4.1.5.Others

5. Global

Medical Electronics Market Estimates

& Forecast Trend Analysis, by Component

5.1.

Global

Medical Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Component,

2020 - 2033

5.1.1.Sensors

5.1.2.Batteries

5.1.3.Microprocessors/MCU

5.1.4.Displays

5.1.5.ASICs/FPGAs

6. Global

Medical Electronics Market Estimates

& Forecast Trend Analysis, by End-user

6.1.

Global

Medical Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

2020 - 2033

6.1.1.Hospitals

6.1.2.Diagnostic Centers

6.1.3.Ambulatory Surgical

Centers

6.1.4.Home Care Settings

7. Global

Medical Electronics Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Medical Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Medical

Electronics Market: Estimates &

Forecast Trend Analysis

8.1. North America Medical

Electronics Market Assessments & Key Findings

8.1.1.North America Medical

Electronics Market Introduction

8.1.2.North America Medical

Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Product

8.1.2.2.

By Component

8.1.2.3.

By End-user

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Medical

Electronics Market: Estimates &

Forecast Trend Analysis

9.1. Europe Medical Electronics

Market Assessments & Key Findings

9.1.1.Europe Medical Electronics

Market Introduction

9.1.2.Europe Medical Electronics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Product

9.1.2.2.

By Component

9.1.2.3.

By End-user

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Medical

Electronics Market: Estimates &

Forecast Trend Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Medical Electronics Market Introduction

10.1.2.

Asia

Pacific Medical Electronics Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Product

10.1.2.2.

By Component

10.1.2.3.

By End-user

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Medical

Electronics Market: Estimates &

Forecast Trend Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Medical Electronics Market Introduction

11.1.2. Middle

East & Africa

Medical Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Product

11.1.2.2.

By Component

11.1.2.3.

By End-user

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Medical Electronics Market: Estimates

& Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Medical

Electronics Market Introduction

12.1.2. Latin America Medical

Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Product

12.1.2.2.

By Component

12.1.2.3.

By End-user

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Medical Electronics

Market Product Mapping

14.2. Global Medical Electronics

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Medical Electronics

Market Tier Structure Analysis

14.4. Global Medical Electronics

Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Medtronic plc

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Siemens Healthineers AG

15.3.

Philips N.V.

15.4.

GE Healthcare

15.5.

Abbott Laboratories

15.6.

Texas Instruments Incorporated

15.7.

Analog Devices, Inc.

15.8.

STMicroelectronics N.V.

15.9.

NXP Semiconductors N.V.

15.10.

Renesas Electronics Corporation

15.11.

Microchip Technology Inc.

15.12.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables