Medical Face Shield Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product (Full Face Shields, Half Face Shields), By Material (Polycarbonate, Acetate, PET, Others), By End-user (Hospitals & Clinics, Diagnostic Laboratories, Ambulatory Surgical Centers, Others), And Geography

2026-01-14

Healthcare

Swetal (Research Analyst)

Description

Medical Face

Shield Market Overview

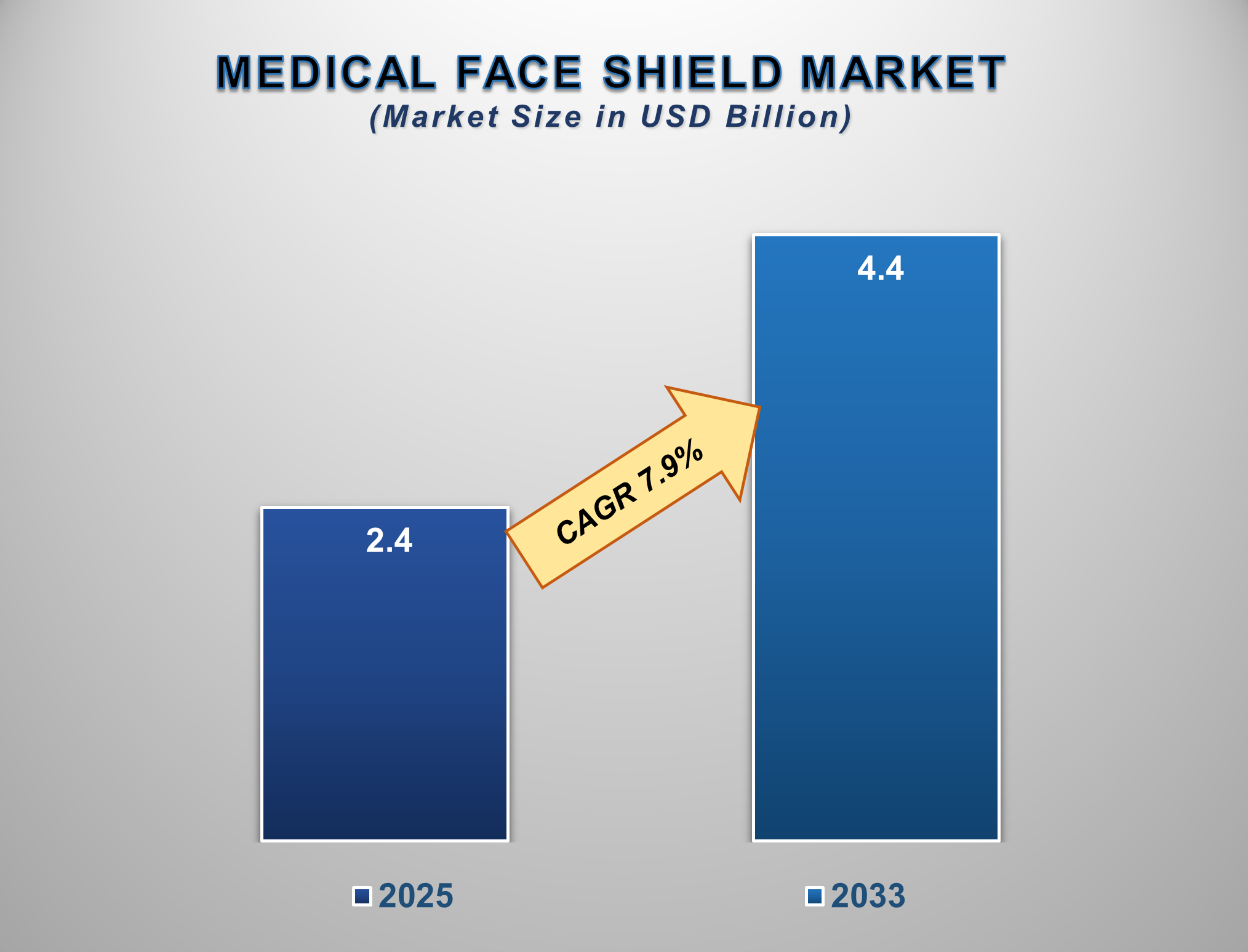

The Medical Face Shield Market is expected to witness steady growth from 2025 to 2033, driven by increasing awareness of infection prevention, rising healthcare worker safety concerns, and sustained demand for personal protective equipment (PPE) across healthcare settings. The market is estimated to be valued at approximately USD 2.4 billion in 2025 and is projected to reach around USD 4.4 billion by 2033, expanding at a CAGR of 7.9% during the forecast period.

Medical face shields are protective devices designed to

safeguard the face, eyes, nose, and mouth from exposure to infectious droplets,

splashes, and aerosols. Their use has become a standard infection control

practice in hospitals, diagnostic laboratories, and outpatient facilities,

particularly during surgical procedures, sample handling, and patient

interactions. Although demand surged significantly during the global pandemic period,

ongoing concerns related to healthcare-associated infections (HAIs) and

occupational safety are sustaining long-term adoption.

Healthcare systems worldwide are strengthening infection

prevention protocols, leading to routine usage of face shields alongside masks

and other PPE. Advancements in shield design,

such as anti-fog coatings, lightweight materials, reusable designs, and

enhanced comfort, are improving compliance

among healthcare professionals. North America and Europe represent established

markets due to strict safety regulations and high PPE standards, while

Asia-Pacific is expected to witness the fastest growth driven by expanding

healthcare infrastructure, rising healthcare expenditure, and increasing

preparedness for infectious disease outbreaks.

Medical Face Shield Market Drivers and

Opportunities

Rising Emphasis on Infection Control and Healthcare Worker

Safety Drives Market Growth

The growing focus on infection prevention and

occupational safety is a key driver of the medical face shield market.

Healthcare workers are routinely exposed to blood, body fluids, respiratory

droplets, and aerosols, particularly during surgical procedures, emergency

care, and diagnostic testing. Face shields provide an additional layer of

protection beyond masks, reducing the risk of cross-contamination and infection

transmission. Increasing awareness of HAIs and strict hospital safety protocols

has made face shields a standard component of

PPE kits. The rise in surgical volumes, emergency department visits, and

diagnostic procedures further supports sustained demand for medical-grade face

shields across healthcare facilities.

Regulatory Guidelines and Institutional Procurement Support

Adoption

Government agencies and healthcare regulatory

bodies across major markets have established guidelines recommending or

mandating the use of face shields in high-risk clinical environments. Hospitals

and healthcare systems are increasingly investing in bulk procurement of PPE to

ensure uninterrupted supply and compliance with safety standards. Accreditation

requirements and workplace safety regulations reinforce routine usage,

particularly in operating rooms, intensive care units, and laboratories. This institutionalized

procurement approach provides stable demand and encourages manufacturers to

develop standardized, certified products tailored to healthcare needs.

Product Innovation and Growth in Emerging Markets Create

Opportunities

Technological innovation and expanding

healthcare access in emerging economies present significant growth

opportunities. Manufacturers are focusing on ergonomic designs, reusable and

sterilizable shields, anti-scratch and anti-fog coatings, and sustainable

materials to meet evolving user preferences. The rapid expansion of hospitals,

ambulatory surgical centers, and diagnostic laboratories in Asia-Pacific, Latin

America, and the Middle East is increasing PPE consumption. Additionally,

rising investments in public health preparedness and stockpiling of essential

medical supplies are creating long-term opportunities for medical face shield

manufacturers.

Medical Face Shield Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.4 Billion |

|

Market Forecast in 2033 |

USD 4.4 Billion |

|

CAGR % 2025-2033 |

7.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors, and more |

|

Segments Covered |

●

By Product ●

By Material ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Medical Face Shield Market Report Segmentation

Analysis

The global

Medical Face Shield Market industry analysis is segmented by Product, by

Material, by End-user and by Region.

The Full Face Shield Segment Is Expected to Witness the

Fastest Growth

The full face shield segment is anticipated to grow at the

fastest pace due to its comprehensive coverage and higher level of protection

compared to partial designs. Full face shields protect the eyes, nose, mouth,

and facial skin from splashes, droplets, and aerosols, making them ideal for

high-risk medical procedures. Their widespread adoption in surgical settings,

emergency departments, and diagnostic laboratories is driven by enhanced safety

and regulatory recommendations. Improvements in lightweight materials,

ventilation, and comfort are further encouraging usage among healthcare

professionals who require extended wear during long shifts.

Polycarbonate Material Segment Is Anticipated to Hold the

Largest Market Share

Polycarbonate-based face shields are expected to hold the

largest market share due to their superior impact resistance, optical clarity,

and durability. These materials offer excellent protection while maintaining

clear visibility, which is critical during medical procedures. Polycarbonate

shields are also compatible with anti-fog and anti-scratch coatings, enhancing

usability. Their reusability and resistance to repeated disinfection make them

cost-effective for hospitals and clinics, supporting widespread adoption across

healthcare facilities.

Hospitals & Clinics Are Expected to Remain the Largest

End-user Segment

Hospitals and clinics are projected to remain the largest

end-user segment owing to high patient volumes and continuous exposure risks

for healthcare workers. These facilities require face shields for surgeries,

emergency care, inpatient treatment, and routine examinations. Strict infection

control policies and institutional PPE procurement programs further drive

demand. The presence of skilled medical staff and compliance with safety

regulations ensure consistent and large-scale usage of medical face shields in

hospital and clinical environments worldwide.

The

following segments are part of an in-depth analysis of the global Medical Face

Shield Market:

|

Market

Segments |

|

|

By

Product |

●

Full Face Shields ●

Half Face Shields |

|

By Material |

●

Polycarbonate ●

Acetate ●

PET ●

Others |

|

By End-user |

●

Hospitals &

Clinics ●

Diagnostic

Laboratories ●

Ambulatory Surgical

Centers ●

Others |

Medical Face Shield Market Share Analysis by

Region

North America Is Expected

to Dominate the Global Medical Face Shield Market

North America

dominates the global medical face shield market primarily due to strict

occupational safety regulations, high infection control awareness, and

well-established healthcare infrastructure, with the United States accounting

for the largest share. For example, agencies such as the U.S. Occupational

Safety and Health Administration (OSHA) and the Centers for Disease Control and

Prevention (CDC) mandate the use of appropriate personal protective equipment

(PPE), including face shields, during high-risk medical procedures involving

exposure to blood, bodily fluids, or airborne pathogens. As a result, hospitals

routinely procure face shields in bulk through long-term contracts with

suppliers such as 3M, Cardinal Health, and Medline Industries, ensuring

consistent demand.

Large

hospital networks and group purchasing organizations (GPOs) in the U.S. further

strengthen market dominance by standardizing PPE usage across facilities. For

instance, integrated delivery networks often require face shields for emergency

departments, surgical units, and intensive care units as part of mandatory

infection control protocols. In contrast, Europe follows closely, supported by

universal healthcare systems and regulatory bodies such as the European Centre

for Disease Prevention and Control (ECDC), which promotes PPE compliance across

member states. Meanwhile, Asia-Pacific is expected to grow fastest, driven by

hospital expansion in countries like India and China, increased medical tourism

in Thailand and Malaysia, and rising government investments in healthcare

preparedness and worker safety.

Medical Face Shield Market Competition Landscape

Analysis

The global medical face shield market is

moderately fragmented, with international PPE manufacturers and regional

players competing on product quality, certifications, pricing, and distribution

reach. Key strategies include product innovation, capacity expansion, and

partnerships with healthcare institutions and government agencies.

Global Medical Face Shield Market Recent Developments News:

o February 2025: 3M Company

introduced an advanced reusable medical face shield with enhanced anti-fog

coating for surgical applications.

o November 2024: Honeywell

International expanded its medical PPE production capacity to support rising

healthcare demand.

o September 2024: Alpha Pro

Tech launched lightweight, recyclable face shields targeting hospital and

laboratory use.

The Global Medical Face Shield Market Is

Dominated by a Few Large Companies, such as

●

3M Company

●

Honeywell

International Inc.

●

Alpha Pro Tech, Ltd.

●

Ansell Limited

●

DuPont de Nemours,

Inc.

●

Medline Industries, LP

●

Cardinal Health, Inc.

●

MSA Safety

Incorporated

●

Lakeland Industries,

Inc.

●

Kimberly-Clark

Corporation

●

Uvex Safety Group

●

Paul Boyé Technologies

●

Drägerwerk AG &

Co. KGaA

●

Gateway Safety, Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

..........

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables