Medical Implant Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage; Product Type (Orthopedic Implants, Cardiovascular Implants, Dental Implants, Neurological Implants, Ophthalmic Implants, Others), Material Type (Metal, Polymer, Ceramic, Composite), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Geography

2026-03-11

Healthcare

Swetal (Research Analyst)

Description

Medical Implant Market Overview

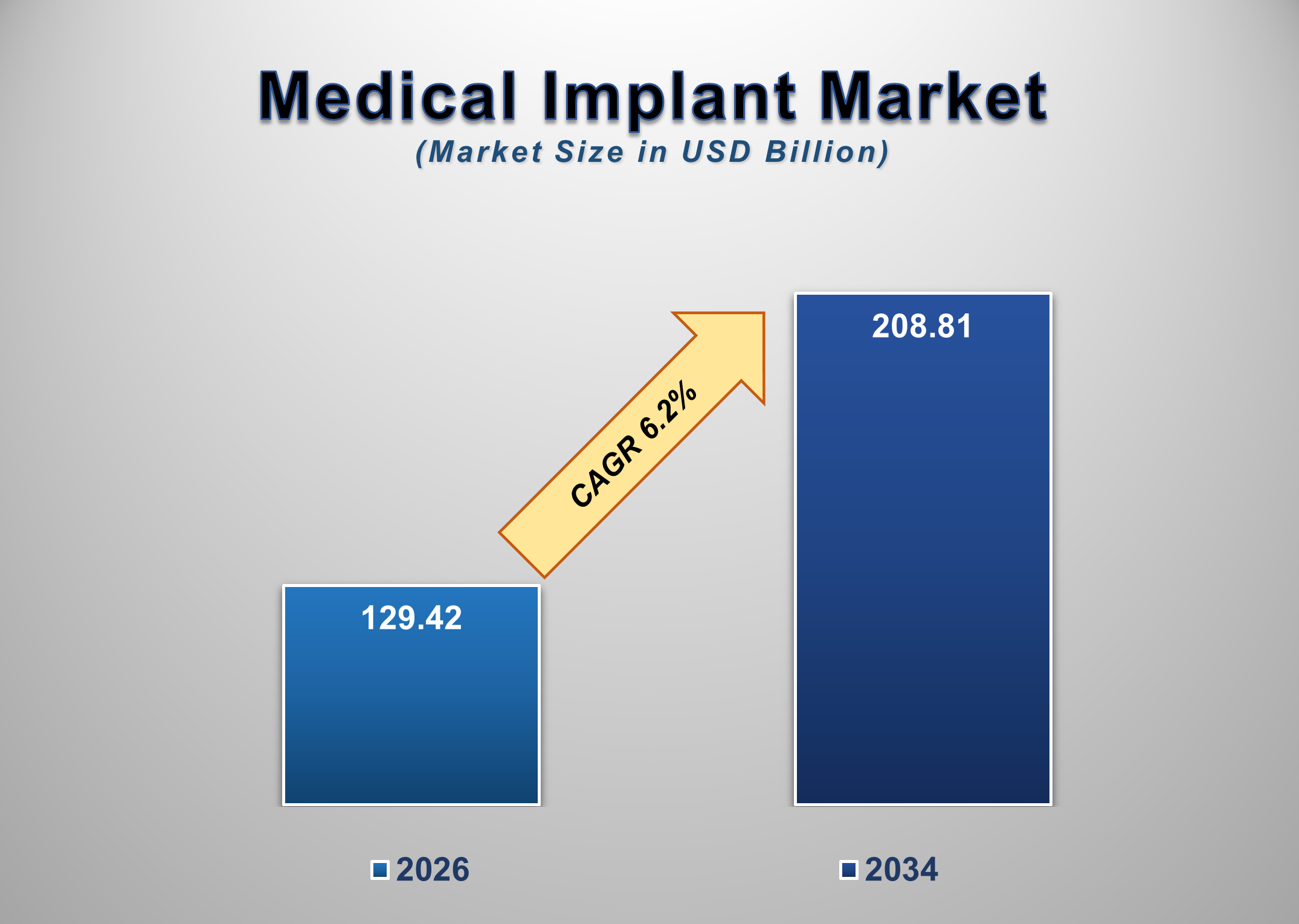

The global medical implant market is witnessing robust growth driven by the rising prevalence of chronic diseases, the expanding geriatric population, increasing surgical procedures, and rapid advancements in biomaterials and implant technologies. Valued at USD 129.42 billion in 2026, the market is projected to reach USD 208.81 billion by 2034, growing at a healthy CAGR of 6.2% during the forecast period.

Medical implants are devices or materials inserted into the human body to replace, support, or enhance biological structures. These include orthopedic implants (such as joint replacements and spinal fixation devices), cardiovascular implants (such as pacemakers, stents, and heart valves), dental implants, neurological implants (such as neurostimulators), ophthalmic implants (including intraocular lenses), and other specialized devices.

The increase in orthopedic conditions like osteoarthritis and osteoporosis, combined with the growing number of cardiovascular diseases worldwide, is significantly fuelling implant demand. Technological advancements such as 3D-printed implants, coated surfaces for enhanced biocompatibility, and smart implants with embedded sensor technologies are reshaping treatment paradigms and improving patient outcomes.

Growing awareness about minimally invasive surgical techniques, expanding reimbursement coverage, and increasing healthcare expenditure in emerging economies further support market growth. While high costs of advanced implantable systems and regulatory challenges remain barriers in certain regions, ongoing innovation and broader accessibility are strengthening adoption rates globally.

Medical Implant Market Drivers and Opportunities

Increasing Prevalence of Chronic Degenerative Diseases and Aging Population

The rising incidence of chronic conditions such as osteoarthritis, rheumatoid arthritis, osteoporosis, and degenerative spinal disorders significantly fuels demand for orthopedic implants. Globally, the geriatric population aged 65 years and above is expanding rapidly, increasing the burden of joint replacement surgeries, spinal fusion procedures, and fracture management.

Similarly, cardiovascular diseases remain a leading cause of mortality worldwide, prompting extensive use of cardiovascular implants like pacemakers, stents, and heart valves. Implantable cardiac defibrillators (ICDs) and left ventricular assist devices (LVADs) are increasingly used to treat life-threatening arrhythmias and heart failure, respectively.

Technological improvements in implant design, durability, and material biocompatibility have expanded the range of patient candidates eligible for implant-based therapies, directly boosting procedural volumes and market demand.

Advancements in Biomaterials, Smart Implants, and Minimally Invasive Techniques

Technological developments in biomaterials — such as titanium alloys, porous metals, bioresorbable polymers, and ceramic composites — have significantly improved long-term implant performance and patient outcomes. These materials offer superior strength, biocompatibility, and reduced risk of rejection or infection.

Smart implants equipped with embedded sensors and connectivity features are emerging, enabling real-time monitoring of physiological parameters and proactive healthcare management. These innovations are especially valuable in orthopedic joint replacements and cardiovascular monitoring.

Furthermore, the expansion of minimally invasive surgical procedures, such as robotic-assisted joint replacements and catheter-based cardiovascular interventions, is driving implant adoption by reducing hospitalization times, lowering complication risks, and improving recovery rates. Surgeons increasingly prefer implant options optimized for minimally invasive workflows.

Expansion of Reimbursement Coverage and Emerging Market Penetration

A major growth opportunity lies in the expansion of insurance and government reimbursement policies covering implant-related procedures. Countries in the Asia-Pacific and Latin America are expanding reimbursement frameworks, making implant surgeries more affordable. This shift, coupled with improving healthcare infrastructure, enables broader access to advanced implant technologies.

Emerging markets like China, India, Brazil, and Mexico are witnessing rising healthcare expenditure, increasing surgical capacities in tertiary care centers, and the adoption of advanced implant systems through strategic partnerships between global manufacturers and local healthcare providers. As clinical outcomes data accumulates and the cost-effectiveness of implant procedures improves, these emerging markets are expected to capture incremental demand over the forecast period.

Market Scope

Medical Implant Market Report Segmentation Analysis

The global medical implant market analysis is segmented by product type, material type, end user, and region. The orthopedic implants segment dominated the market in 2025 and is projected to continue commanding a significant share throughout the forecast period.

Orthopedic implants, including hip and knee joint replacements, spinal fixation systems, and trauma devices, remain the largest revenue contributors due to increasing prevalence of musculoskeletal disorders, aging demographics, and expanding adoption of joint reconstruction surgeries. Technological improvements in modular implant designs and surface coatings for improved osseointegration have increased product lifespans, reducing revision surgery rates and enhancing surgeon confidence.

Application Segment Analysis

The hospital segment holds the highest share of the end-user segment over the forecast period.

Hospitals are the primary procurers of medical implants due to established surgical infrastructure, availability of specialized surgeon networks, and comprehensive post-operative care facilities. High procedure volumes for joint replacements, cardiovascular implantations, and dental surgeries contribute to the dominant share. Ambulatory surgical centers and specialty clinics are gradually increasing adoption as minimally invasive procedures become more standardized and insurance coverage expands.

Medical Implant Market Share Analysis by Region

North America is projected to hold the largest share of the global medical implant market over the forecast period.

The region’s dominance is attributed to advanced healthcare infrastructure, high surgical procedure volumes, strong insurance reimbursement policies, and robust clinical trial activities. The United States leads due to high per-capita healthcare expenditure, widespread adoption of advanced implants, and growing orthopedic and cardiovascular procedure volumes. Europe maintains a significant share with a strong presence of major implant manufacturers and well-established healthcare systems. Asia-Pacific is expected to exhibit the fastest growth rate, driven by expanding surgical capacities, healthcare investments, and increasing access to advanced technologies in China and India.

Medical Implant Market Recent Developments News

In March 2025, Zimmer Biomet Holdings launched a new generation of 3D-printed spinal implants designed to improve osseointegration and reduce recovery times.

In July 2025, Medtronic plc received FDA approval for an advanced neurostimulator platform with adaptive stimulation capabilities for chronic pain management.

In October 2025, Stryker Corporation expanded its orthopedic implant manufacturing capacity in India, targeting rapid deployment across South Asian markets.

Competitive Landscape

The Global Medical Implant Market is dominated by a few large companies, such as:

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Medtronic plc

Johnson & Johnson (DePuy Synthes)

Smith+Nephew plc

B. Braun Melsungen AG

DENTSPLY SIRONA, Inc.

Globus Medical, Inc.

NuVasive, Inc.

Boston Scientific Corporation

Abbott Laboratories

Orthofix International N.V.

Conformis, Inc.

EssilorLuxottica (Ophthalmic Implants)

Carl Zeiss Meditec AG

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

Medical Implant Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables