Medical Spa Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Service Type (Injection-Based Treatments, Skin Rejuvenation & Resurfacing, Body Contouring & Fat Reduction, Hair Removal, Anti-Aging & Regenerative Medicine, Others), By Age Group (Below 30, 30–50, Above 50), By Facility Type (Single-Owner/Solo Practices, Franchised Spas, Medical Group & Hospital-Affiliated Spas), By Distribution Channel (Direct Sales/In-clinic, Online Booking Platforms, Third-Party Aggregators), and Geography

2025-12-19

Healthcare

Swetal (Research Analyst)

Description

Medical Spa

Market Overview

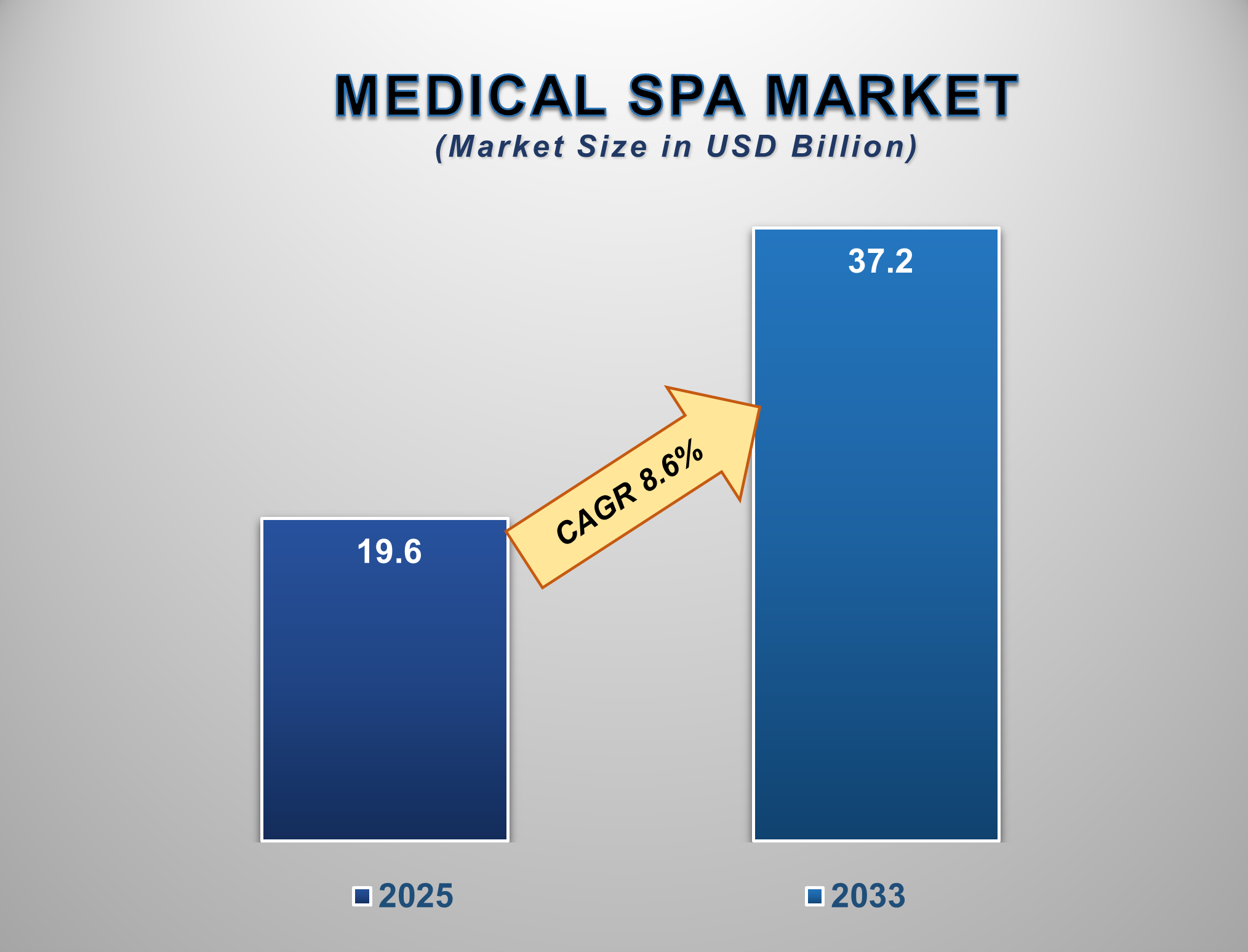

The Medica Spa Market is poised for robust growth between 2025 and 2033, fueled by rising consumer demand for minimally invasive aesthetic procedures, increasing disposable income, and growing awareness of appearance enhancement and wellness. The market is expected to be valued at USD 19.6 billion in 2025 and is projected to reach USD 37.2 billion by 2033, registering a CAGR of 8.6% during the forecast period.

Medical spas integrate clinical medical treatments with

traditional spa services, offering procedures such as Botox, dermal fillers,

laser hair removal, chemical peels, microdermabrasion, and non-surgical body

sculpting under medical supervision. These facilities bridge the gap between

dermatology clinics and luxury spas, providing a safe, results-driven

environment for cosmetic and wellness services. Advancements in energy-based

devices, injectable technologies, and personalized treatment protocols have expanded

the range of services and improved outcomes, attracting a diverse clientele.

The market is driven by a cultural shift towards proactive aging management,

social media influence, and the destigmatization of aesthetic treatments. North

America leads in revenue due to high adoption rates and advanced healthcare

infrastructure, while Asia-Pacific is witnessing explosive growth driven by

medical tourism, rising beauty consciousness, and expanding middle-class

populations.

Medical Spa Market Drivers and Opportunities

Rising Demand for

Non-Invasive and Minimally Invasive Aesthetic Procedures Is the Primary Market

Driver

The global surge in preference for non-surgical cosmetic

treatments is the most influential driver of medical spa growth. Consumers increasingly seek procedures with

minimal downtime, lower risk, and natural-looking results compared to

traditional surgery. Treatments like neuromodulator injections (Botox),

hyaluronic acid fillers, laser skin resurfacing, and non-invasive fat reduction

(e.g., CoolSculpting, ultrasound cavitation) are highly popular due to their

effectiveness and convenience. The aging global population, particularly baby

boomers and Generation X, is actively investing in anti-aging solutions to

maintain a youthful appearance.

Additionally, younger demographics (millennials and Gen Z)

are engaging in preventative treatments earlier in life. The growing influence

of social media, celebrity endorsements, and visual platforms like Instagram

and TikTok has normalized aesthetic enhancements, making them more accessible

and desirable. The medical oversight offered by medical spas assures safety and efficacy, further boosting

consumer confidence and driving market expansion.

Increasing Disposable Income and Expanding Middle-Class

Population in Emerging Economies Are Accelerating Market Adoption

Rising per capita income, especially in developing regions,

has made aesthetic treatments more affordable and accessible. As disposable

incomes grow, consumers are more willing to spend on premium wellness and

beauty services that were previously considered luxuries. The expanding

middle-class population in countries such as China, India, Brazil, and Mexico

is demonstrating heightened interest in personal grooming, appearance

enhancement, and self-care.

Medical spas are capitalizing on this trend by offering tiered

pricing, package deals, and membership models to attract a broader clientele.

Furthermore, the medical tourism industry is fueling cross-border travel for

high-quality, cost-effective aesthetic procedures, particularly in destinations

like Thailand, South Korea, Turkey, and Mexico. The combination of economic

growth, increased beauty consciousness, and the availability of advanced

technologies at competitive prices is creating a sustainable demand pipeline

for medical spa services worldwide.

Technological Advancements and Integration of AI and

Personalized Medicine Present Significant Opportunities

Continuous innovation in aesthetic devices and treatment

protocols is a major opportunity for market differentiation. The advent of

AI-driven skin analysis tools, personalized treatment planning software, and

advanced energy-based devices (e.g., fractional lasers, RF microneedling, HIFU)

allow for more precise, effective, and

tailored outcomes. The integration of regenerative medicine—such as

platelet-rich plasma (PRP) therapy, stem cell treatments, and exosome

therapy—into medical spa offerings is attracting

clients seeking holistic anti-aging and rejuvenation solutions. Additionally,

the rise of telemedicine and virtual consultations enables medical spas to expand their reach, provide follow-up care, and

engage with clients remotely.

Sustainability and eco-conscious practices are also

emerging as differentiators, with spas adopting green technologies, organic

products, and waste-reduction initiatives to appeal to environmentally aware

consumers. Franchising and partnership models with hospitals, dermatology

clinics, and wellness centers offer scalable growth avenues, especially in

underserved regions. For investors and operators, opportunities lie in

developing integrated wellness ecosystems, incorporating nutraceuticals and

holistic health services, and leveraging data analytics to enhance customer

retention and treatment outcomes.

Medical Spa Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 19.6 Billion |

|

Market Forecast in 2033 |

USD 37.2 Billion |

|

CAGR % 2025-2033 |

8.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Service Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Service Type ●

By Age Group ●

By Facility Type ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Medical Spa Market Report Segmentation Analysis

The

global Medica Spa Market is segmented by Service Type, End-user, Age Group,

Facility Type, Distribution Channel, and Region.

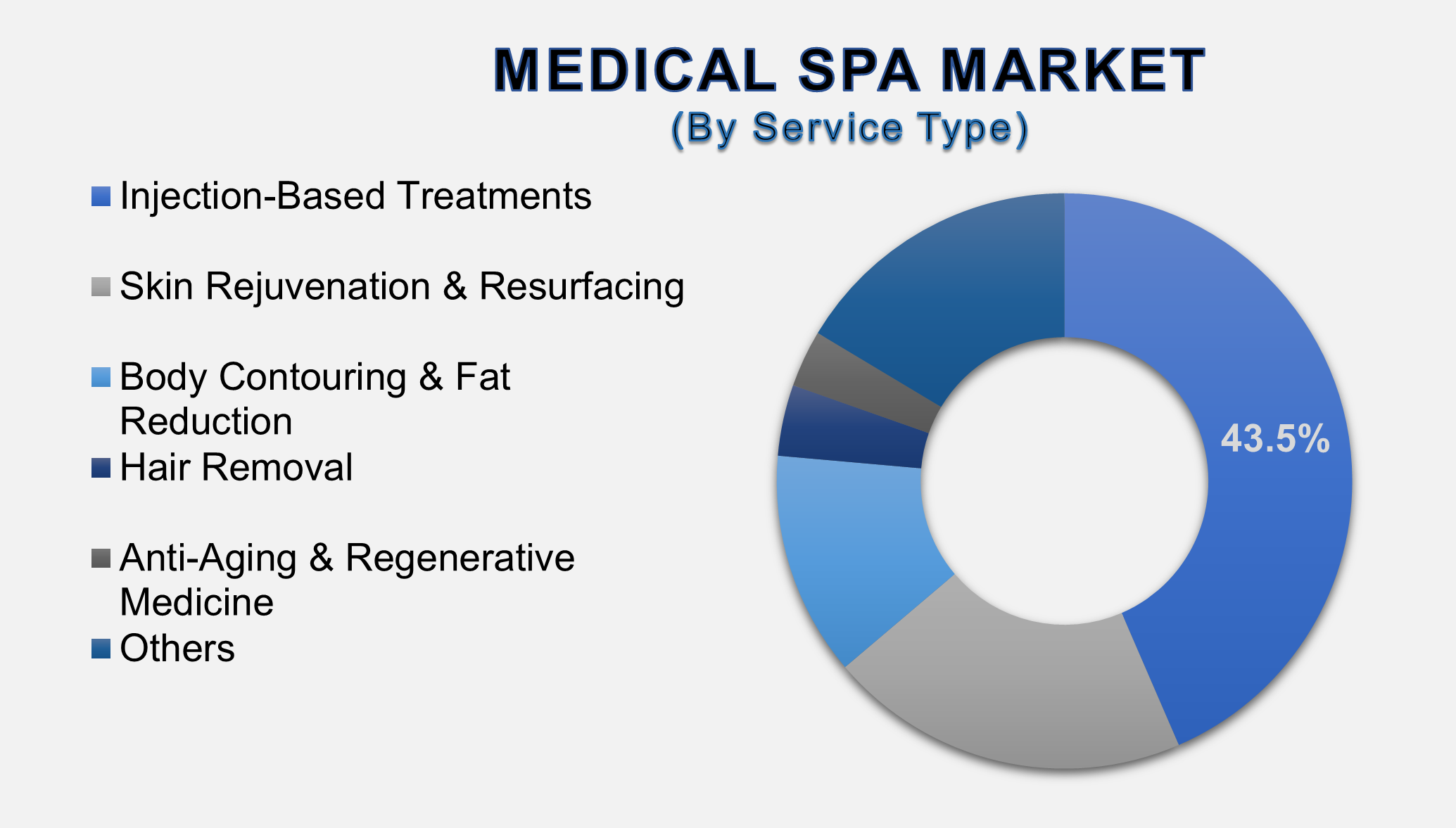

Injection-Based

Treatments Are Anticipated to Command the Largest Market Share in 2025

Injection-based treatments, including neuromodulators (e.g., Botox, Dysport) and dermal fillers, dominate the Service Type segment due to their high popularity, quick procedure time, and immediate, noticeable results. Their market leadership is anchored in widespread use for addressing wrinkles, volume loss, and facial contouring with minimal recovery. Continuous innovation in product formulations—such as longer-lasting fillers, bio-stimulatory agents, and targeted micro-injectables—has expanded their applications and improved safety profiles. The growing acceptance among both female and male clients, coupled with increased training and certification for practitioners, has made these procedures more accessible. Rising demand for preventative “tweakments” among younger adults and the recurring nature of treatments (requiring maintenance every 6–12 months) ensure consistent revenue streams. The strong presence of established pharmaceutical brands (Allergan, Galderma) and medical spa partnerships further solidifies injection-based treatments as the leading service category globally.

The Female Segment Holds

the Largest Share by End-user

Females

represent the primary end-user segment, accounting for the majority of medical spa clients. This dominance stems from historically higher

engagement in cosmetic procedures, greater sensitivity to aging signs, and

stronger influence from beauty and wellness marketing. Women are more likely to

seek a comprehensive range of services, from

injectables and laser treatments to body contouring and skin rejuvenation, often combining multiple procedures for enhanced results.

Societal pressures, media representation, and the desire for self-confidence

continue to drive female participation. However, the male segment is growing

rapidly, fueled by increasing grooming consciousness, workplace

competitiveness, and the rise of “brotox” and male-specific aesthetic packages.

Despite this, females remain the core demographic due to higher lifetime

spending, earlier adoption of treatments, and greater openness to discussing

aesthetic enhancements, ensuring their continued leadership in the market.

Direct Sales/In-clinic

Channels Lead the Distribution Channel Segment

Direct

sales or in-clinic consultations dominate the Distribution Channel segment, as medical spa services require personalized assessments, treatment

planning, and clinical oversight. Clients prefer face-to-face interactions with

medical professionals (doctors, nurse practitioners, and aestheticians) to evaluate their needs, discuss

expectations, and ensure safety. The consultative nature of aesthetic

treatments builds trust and allows for upselling and cross-selling of

complementary services or products.

In-clinic

sales also include retail skincare lines, post-treatment care products, and

package memberships that enhance customer loyalty and recurring revenue. While

online booking platforms and third-party aggregators (e.g., Groupon, Treatwell)

are gaining traction for discovery and appointment scheduling, the final

decision and treatment delivery remain firmly rooted in the physical clinic.

The integration of digital tools for virtual consultations and follow-ups

complements rather than replaces the direct channel, reinforcing its central

role in the medical spa ecosystem.

The following segments are

part of an in-depth analysis of the global Medical Spa Market:

|

Market

Segments |

|

|

By Service

Type |

●

Injection-Based

Treatments ●

Skin Rejuvenation

& Resurfacing ●

Body Contouring

& Fat Reduction ●

Hair Removal ●

Anti-Aging &

Regenerative Medicine ●

Others |

|

By Age Group |

●

Below 30 ●

30–50 ●

Above 50 |

|

By Distribution Channel |

●

Direct

Sales/In-clinic ●

Online Booking

Platforms ●

Third-Party

Aggregators |

|

By Facility Type |

●

Single-Owner/Solo

Practices ●

Franchised Spas ●

Medical Group &

Hospital-Affiliated Spas |

Medical Spa

Market Share Analysis by Region

North America is

anticipated to hold the largest portion of the Medical Spa Market globally

throughout the forecast period.

North

America’s leadership is driven by high consumer spending power, advanced

medical aesthetics technology, strong regulatory frameworks, and widespread

cultural acceptance of cosmetic enhancements. The United States represents the

largest contributor, supported by a dense network of medical spas, prominent key players, and aggressive marketing. The

region benefits from a well-established healthcare infrastructure, extensive

insurance coverage for certain medically necessary procedures, and high

awareness of anti-aging solutions. Canada is also experiencing steady growth

due to increasing demand for non-invasive treatments and rising medical

tourism. The presence of leading device manufacturers, pharmaceutical

companies, and training academies in North America fosters continuous

innovation and practitioner expertise. While Asia-Pacific is the

fastest-growing region—fueled by South Korea’s advanced beauty industry and

China’s expanding middle class—North America maintains its dominance due to

maturity, high procedure volumes, and premium service pricing.

Medical Spa Market Competition Landscape Analysis

The global market is

fragmented, with a mix of large corporate chains, hospital-affiliated centers,

franchise networks, and independent boutique spas. Competition centers on

service quality, technological advancement, practitioner credentials, clinic

ambiance, and customer experience. Leading players invest in state-of-the-art

devices, staff training, and loyalty programs to retain clients. Strategic

collaborations with dermatologists, plastic surgeons, and wellness brands are

common to expand service portfolios. Digital marketing, social media

engagement, and online reputation management are critical for client

acquisition. Mergers and acquisitions are frequent as larger entities seek to

consolidate regional markets and expand geographic presence.

Global Medical Spa Market Recent Developments News:

- In February 2025, Allergan Aesthetics launched a new digital

consultation platform integrating AI skin analysis for personalized

treatment plans in partner medical

spas.

- In November 2024, The HydraFacial Company expanded its flagship

device offerings to include regenerative boosters, targeting medical spa partnerships in Europe and

Asia.

- In September 2024, Scientis partnered with leading U.S. medical spa chains to introduce its

next-generation hyaluronic acid filler with an

improved longevity and safety profile.

- In June 2024, LaserAway announced the acquisition of five independent

medical spas in Texas, strengthening

its footprint in the southern United States.

The Global Medical Spa Market Is Dominated by a

Few Large Companies, such as

●

Allergan Aesthetics

(AbbVie Inc.)

●

Galderma Laboratories,

L.P.

●

Cynosure, LLC

(Hologic, Inc.)

●

Lumenis Ltd.

●

Sciton, Inc.

●

Cutera, Inc.

●

Solta Medical (Bausch

Health Companies Inc.)

●

Alma Lasers Ltd.

●

El.En. S.p.A.

●

Candela Corporation

●

Syneron Medical Ltd.

●

Lutronic Corporation

●

Venus Concept Inc.

●

Merz Pharma GmbH &

Co. KGaA

●

Revance Therapeutics,

Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Medical Spa Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Medical Spa Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Medical Spa Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Service Type of Global Medical

Spa Market

1.3.2.Age Group of Global Medical

Spa Market

1.3.3.Faculty Type of Global Medical

Spa Market

1.3.4.Distribution Channel of Global

Medical Spa Market

1.3.5.Region of Global Medical

Spa Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Medical Spa Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Medical Spa Market Estimates

& Forecast Trend Analysis, by Service Type

4.1.

Global

Medical Spa Market Revenue (US$ Bn) Estimates and Forecasts, by Service Type,

2020 - 2033

4.1.1.Injection-Based Treatments

4.1.2.Skin Rejuvenation &

Resurfacing

4.1.3.Body Contouring & Fat

Reduction

4.1.4.Hair Removal

4.1.5.Anti-Aging &

Regenerative Medicine

4.1.6.Others

5. Global

Medical Spa Market Estimates

& Forecast Trend Analysis, by Age Group

5.1.

Global

Medical Spa Market Revenue (US$ Bn) Estimates and Forecasts, by Age Group, 2020

- 2033

5.1.1.Below 30

5.1.2.30–50

5.1.3.Above 50

6. Global

Medical Spa Market Estimates

& Forecast Trend Analysis, by Facility Type

6.1.

Global

Medical Spa Market Revenue (US$ Bn) Estimates and Forecasts, by Facility Type

2020 - 2033

6.1.1.Single-Owner/Solo

Practices

6.1.2.Franchised Spas

6.1.3.Medical Group &

Hospital-Affiliated Spas

7. Global

Medical Spa Market Estimates

& Forecast Trend Analysis, by Distribution Channel

7.1.

Global

Medical Spa Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

7.1.1.Direct Sales/In-clinic

7.1.2.Online Booking Platforms

7.1.3.Third-Party Aggregators

8. Global

Medical Spa Market Estimates

& Forecast Trend Analysis, by region

8.1.

Global

Medical Spa Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Medical

Spa Market: Estimates & Forecast

Trend Analysis

9.1.

North

America Medical Spa Market Assessments & Key Findings

9.1.1.North America Medical Spa

Market Introduction

9.1.2.North America Medical Spa

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Service

Type

9.1.2.2. By Age Group

9.1.2.3. By Distribution

Channel

9.1.2.4. By Facility

Type

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Medical

Spa Market: Estimates & Forecast

Trend Analysis

10.1.

Europe

Medical Spa Market Assessments & Key Findings

10.1.1.

Europe

Medical Spa Market Introduction

10.1.2.

Europe

Medical Spa Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Service

Type

10.1.2.2. By Age Group

10.1.2.3. By Distribution

Channel

10.1.2.4. By Facility

Type

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Medical

Spa Market: Estimates & Forecast

Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Medical Spa Market Introduction

11.1.2.

Asia

Pacific Medical Spa Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Service

Type

11.1.2.2. By Age Group

11.1.2.3. By Distribution

Channel

11.1.2.4. By Facility

Type

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Medical

Spa Market: Estimates & Forecast

Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Medical Spa Market Introduction

12.1.2.

Middle East & Africa Medical Spa Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Service

Type

12.1.2.2. By Age Group

12.1.2.3. By Distribution

Channel

12.1.2.4. By End User

12.1.2.5.

By

Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Medical Spa Market: Estimates &

Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Medical Spa Market Introduction

13.1.2.

Latin

America Medical Spa Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1. By Service

Type

13.1.2.2. By Age Group

13.1.2.3. By Distribution

Channel

13.1.2.4. By Facility

Type

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Medical Spa Market Product Mapping

15.2.

Global

Medical Spa Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

15.3.

Global

Medical Spa Market Tier Structure Analysis

15.4.

Global

Medical Spa Market Concentration & Company Market Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

Allergan Aesthetics (AbbVie Inc.)

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2. Galderma

Laboratories, L.P.

16.3. Cynosure, LLC

(Hologic, Inc.)

16.4. Lumenis Ltd.

16.5. Sciton, Inc.

16.6. Cutera, Inc.

16.7. Solta Medical

(Bausch Health Companies Inc.)

16.8. Alma Lasers

Ltd. (Sisram Medical Ltd)

16.9. El.En. S.p.A.

16.10. Candela

Corporation

16.11. Syneron

Medical Ltd.

16.12. Lutronic

Corporation

16.13. Venus Concept

Inc.

16.14. Merz Pharma

GmbH & Co. KGaA

16.15. Revance

Therapeutics, Inc.

16.16. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables