Medical Tourism Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Healthcare Services (Medical Treatment, Cardiac Procedures, Oncology Procedures, Orthopedic & Spine Procedures, Dental Procedures, Wellness Treatment, Cosmetic Procedures, Rejuvenation Procedures, Alternative Treatment, Others), By Service Provider (Public, Private), and Geography

2026-02-17

Travel & Hospitality

Ekta Chaurasia (Team Lead)

Description

Medical Tourism Market Overview

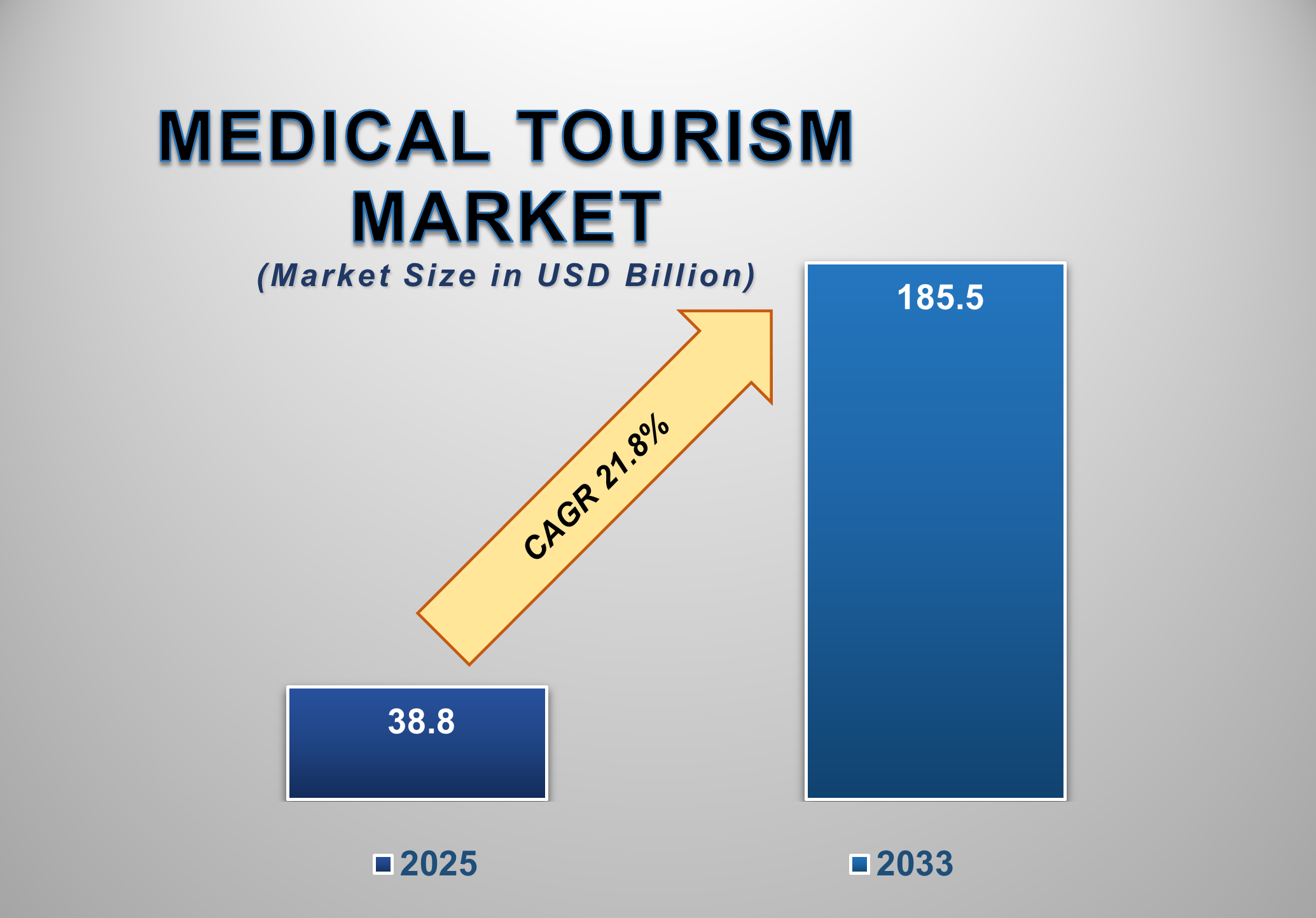

The global Medical Tourism Market is undergoing rapid transformation and expansion, driven by widening cost differentials in healthcare services, growing cross-border mobility, and increasing patient willingness to seek high-quality medical care outside their home countries. Valued at USD 38.8 billion in 2025, the market is projected to reach USD 185.5 billion by 2033, registering a remarkable CAGR of 21.8% during the forecast period. Medical tourism encompasses a broad range of healthcare services, including complex medical treatments, elective surgeries, wellness therapies, and cosmetic and rejuvenation procedures.

Patients increasingly travel

internationally to access advanced medical treatments at significantly lower

costs, often combined with shorter waiting times and access to internationally

accredited hospitals. The market benefits from advancements in medical

technology, teleconsultation, digital health records, and coordinated patient

facilitation services, which simplify cross-border treatment journeys. Private

healthcare providers, in particular, have emerged as major beneficiaries,

offering bundled treatment packages that combine medical procedures,

accommodation, post-operative care, and travel assistance.

Medical Tourism Market

Drivers and Opportunities

Rising Healthcare Costs

and Long Waiting Times in Developed Economies Are Driving Medical Tourism

Growth

Escalating healthcare costs and prolonged waiting periods in

developed economies are among the most significant drivers fueling growth in

the global medical tourism market. In regions such as North America and parts

of Europe, patients face high out-of-pocket expenses, limited insurance

coverage for elective procedures, and extended wait times for surgeries such as

orthopedic, cardiac, and diagnostic interventions. These challenges are

prompting patients to seek treatment in countries offering comparable or

superior care at substantially lower costs. Medical tourism destinations in the

Asia Pacific and parts of the Middle East offer savings of 40–80% on major

procedures, even after accounting for travel and accommodation expenses. For

example, cardiac surgeries, orthopedic replacements, and oncology treatments

are available at a fraction of the cost charged in the United States or Western

Europe. Shorter waiting times further enhance the appeal, particularly for

patients requiring timely intervention.

In addition, international accreditation standards such as JCI and

ISO certifications have strengthened patient confidence in overseas healthcare

providers. Hospitals actively market their expertise, outcomes, and cost

advantages to international patients, reinforcing cross-border demand. As

healthcare affordability challenges persist in developed economies, medical

tourism is expected to remain a compelling alternative for millions of patients

worldwide.

Improving Healthcare Infrastructure and Government Support in

Destination Countries Is Accelerating Market Expansion

Significant investments in healthcare infrastructure and proactive

government support in key destination countries are accelerating the expansion

of the medical tourism market. Governments across the Asia Pacific and the

Middle East are actively positioning medical tourism as a strategic economic

sector, offering policy incentives, streamlined medical visas, and

international marketing initiatives. Countries such as India, Thailand,

Malaysia, and Turkey have invested heavily in state-of-the-art hospitals, advanced

diagnostic equipment, and specialized treatment centers. These facilities are

staffed by internationally trained physicians and surgeons, many of whom have

practiced in the U.S. or Europe. The presence of multilingual staff and

dedicated international patient departments further enhances the treatment

experience.

Public-private collaboration is also strengthening market growth.

While private healthcare providers dominate medical tourism flows, public

hospitals in certain regions are increasingly participating through specialized

departments and partnerships. As destination countries continue to enhance

healthcare quality, transparency, and patient facilitation services,

international patient volumes are expected to rise steadily.

Growth of Specialized Treatments and Wellness Tourism Is

Creating Significant Market Opportunities

The expanding demand for specialized medical treatments and

integrated wellness tourism is creating substantial growth opportunities in the

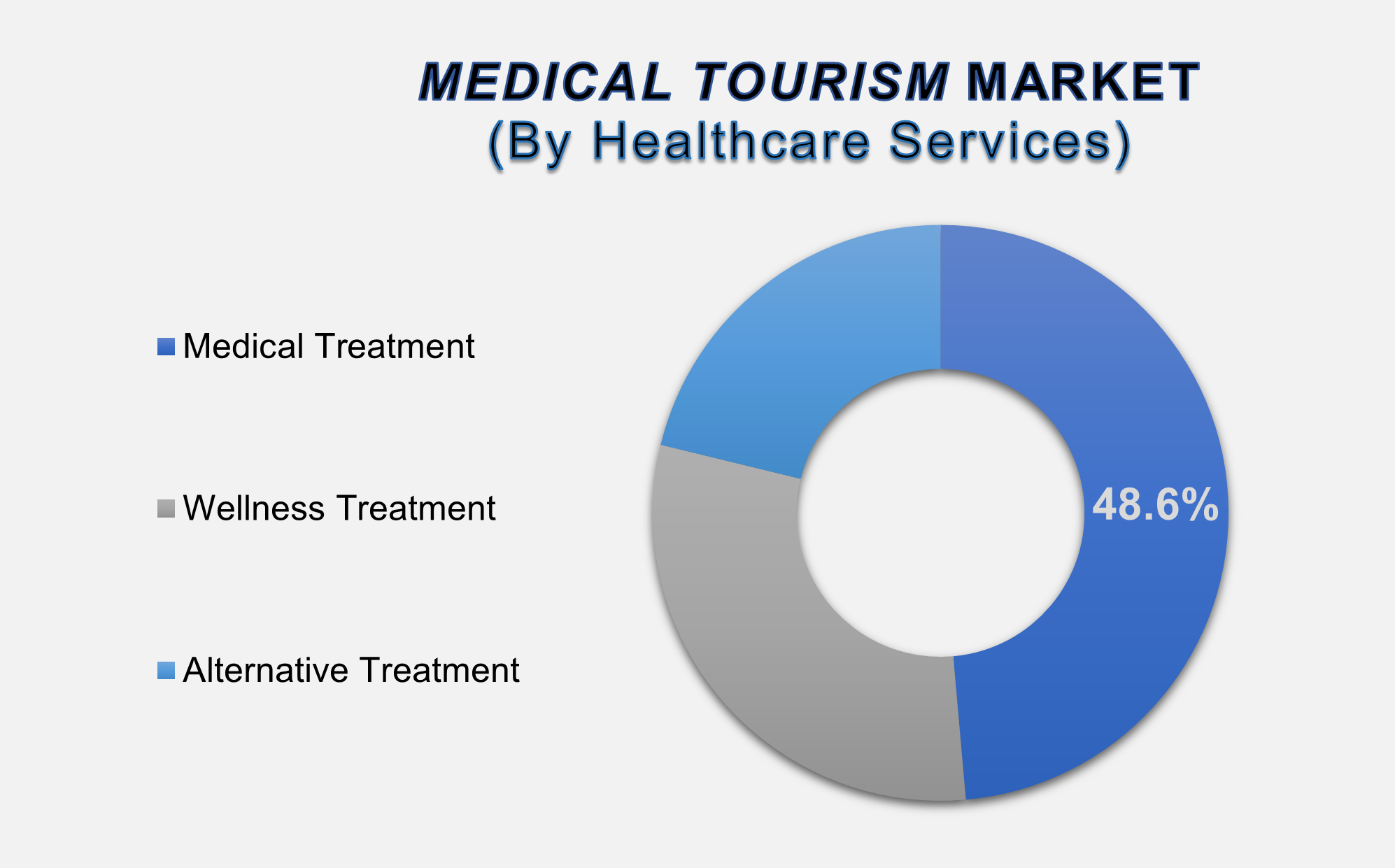

global medical tourism market. Medical treatment services account for 48.6% of

the market, reflecting strong demand for core healthcare services such as

cardiac, orthopedic, oncology, and neurological procedures. In parallel,

wellness, cosmetic, rejuvenation, and alternative treatments are gaining

popularity among international travelers seeking preventive and lifestyle-oriented

care. Procedures such as cosmetic surgery, dental treatments, fertility

services, and regenerative therapies are increasingly bundled with wellness

programs and post-treatment recovery packages.

This convergence of medical and wellness tourism enables providers to diversify revenue streams and attract a broader patient base. Emerging treatments, personalized medicine, and integrative healthcare models are expected to further expand market scope. As global populations age and health awareness rises, demand for both curative and preventive medical tourism services is expected to grow substantially

Medical Tourism Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 38.8 Billion |

|

Market Forecast in 2035 |

USD 185.5 Billion |

|

CAGR % 2025-2035 |

21.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

● Healthcare Services, Service Provider |

|

Regional Scope |

● North America, ● Europe, ● APAC, ● Latin America ● Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Medical Tourism Market

Report Segmentation Analysis

The Global Medical Tourism Market

Industry Analysis Is Segmented by Healthcare Services, by Service Provider, and

by Region.

The

Medical Treatment Segment Accounted for the Largest

Market Share in the Global Medical Tourism Market

The medical treatment segment accounted for the largest market share, contributing 48.6% of the global medical tourism market. This dominance is driven by high demand for essential and life-saving procedures, including cardiac surgeries, oncology treatments, orthopedic and spine interventions, and complex diagnostics. Patients primarily travel abroad to access cost-effective yet high-quality medical treatment that may be unavailable or unaffordable in their home countries. Advanced clinical expertise, modern infrastructure, and internationally accredited hospitals reinforce the leadership of this segment. As chronic disease prevalence rises globally, medical treatment services are expected to remain the cornerstone of medical tourism demand.

Private

Service Provider Segment Dominated the Global Medical Tourism Market

The

private service provider segment dominated the global medical tourism market,

driven by flexible pricing, advanced facilities, and strong international

patient support systems. Private hospitals actively invest in technology,

specialized departments, and patient-centric services tailored for

international visitors. These providers offer end-to-end treatment packages,

multilingual support, and coordinated care pathways, making them highly

attractive to medical tourists. While public hospitals play a supporting role

in certain regions, private healthcare providers continue to lead in attracting

international patient flows and generating revenue.

The following segments are

part of an in-depth analysis of the global Medical Tourism market:

|

Market Segments |

|

|

By Healthcare

Services |

●

Medical Treatment o

Cardiac Procedures o

Oncology Procedures o

Orthopedic &

Spine Procedures o

Dental Procedures o

Others ●

Wellness Treatment o

Cosmetic Procedures o

Rejuvenation

Procedures o

Others ●

Alternative

Treatment |

|

By Service

Provider |

●

Public ●

Private |

Medical Tourism Market

Share Analysis by Region

Asia Pacific is

anticipated to hold the biggest portion of the Medical Tourism Market globally

throughout the forecast period.

Asia Pacific dominated the global

medical tourism market, accounting for 45.6% of the total market share. The

region’s leadership is driven by cost competitiveness, high-quality healthcare

infrastructure, and strong government support. Countries such as India,

Thailand, Malaysia, and South Korea serve as major hubs, offering advanced

medical procedures at significantly lower costs. The availability of

internationally accredited hospitals, skilled medical professionals, and

integrated tourism infrastructure further strengthens regional dominance.

North America is expected to

register the highest CAGR during the forecast period, driven by increasing

outbound medical tourism, demand for specialized treatments, and rising

healthcare costs. Patients from the U.S.and Canada increasingly seek overseas treatment

for elective and high-cost procedures, accelerating outbound medical travel and

contributing to global market growth.

Medical Tourism Market

Competition Landscape Analysis

The global medical tourism market

is highly competitive and fragmented, with participation from multinational

hospital groups, specialty care centers, and integrated healthcare networks.

Market players compete based on treatment quality, international accreditation,

pricing transparency, and patient experience. Strategic partnerships,

international marketing, and service diversification are key competitive

strategies.

Global Medical Tourism

Market Recent Developments News:

- In October 2024 – KPJ Healthcare and Malaysia

International Healthcare co-organized the

Malaysia International Healthcare Megatrends 2024 event at the Kuala

Lumpur Convention Centre, showcasing the latest advancements in medical

technology and healthcare solutions.

- In October 2024 – Apollo Hospitals Group reached a

significant milestone by completing 500 robotic cardiac care procedures,

marking a major advancement in its precision cardiology services.

- In September 2024 – Bumrungrad International

Hospital in Thailand opened a new wellness center to cater to the growing

demand for wellness treatments, strengthening its brand and expanding its

service offerings.

- In August 2024 – Bangkok Chain Hospital Public

Company Limited opened the new "Kasetsart Aree Radiotherapy

Specialist Clinic," a comprehensive cancer treatment center in

Bangkok aimed at enhancing patient care and treatment outcomes.

The Global Medical Tourism Market

Is Dominated by a Few Large Companies, such as

●

Bumrungrad

International Hospital

●

Apollo Hospitals

Enterprise

●

Bangkok Hospital

●

Anadolu Medical Center

●

Fortis Healthcare

●

Prince Court Medical

Centre

●

Asklepios Kliniken

●

Shouldice Hospital

●

Samitivej Hospital

●

Gleneagles Hospital

●

Raffles Medical Group

●

KPJ Healthcare Berhad

●

Clemenceau Medical

Center

●

Asian Heart Institute

●

Burjeel Hospital

●

Christus Muguerza

●

Hospital Clínic de

Barcelona

●

UZ Leuven

●

Johns Hopkins Medicine

International

●

Mayo Clinic

● Others

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Medical Tourism

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Medical Tourism Market Scope and Market Estimation

1.2.1.Global Medical Tourism Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Medical Tourism

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Healthcare Services of

Global Medical Tourism Market

1.3.2.Service Provider of Global

Medical Tourism Market

1.3.3.Region of Global Medical

Tourism Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Medical Tourism Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Healthcare Services

4.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Healthcare

Services, 2020 - 2033

4.1.1.Medical Treatment

4.1.1.1.

Cardiac

Procedures

4.1.1.2.

Oncology

Procedures

4.1.1.3.

Orthopedic

& Spine Procedures

4.1.1.4.

Dental

Procedures

4.1.1.5.

Others

4.1.2.Wellness Treatment

4.1.2.1.

Cosmetic

Procedures

4.1.2.2.

Rejuvenation

Procedures

4.1.2.3.

Others

4.1.3.Alternative Treatment

5. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Service Provider

5.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Service

Provider, 2020 - 2033

5.1.1.Public

5.1.2.Private

6. Global

Medical Tourism Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Medical Tourism Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Medical

Tourism Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Medical Tourism Market Assessments & Key Findings

7.1.1.North America Medical

Tourism Market Introduction

7.1.2.North America Medical

Tourism Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Healthcare

Services

7.1.2.2. By Service

Provider

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Medical

Tourism Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Medical Tourism Market Assessments & Key Findings

8.1.1.Europe Medical Tourism

Market Introduction

8.1.2.Europe Medical Tourism

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Healthcare

Services

8.1.2.2. By Service

Provider

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Medical

Tourism Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Medical

Tourism Market Introduction

9.1.2.Asia Pacific Medical

Tourism Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Healthcare

Services

9.1.2.2. By Service

Provider

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Medical

Tourism Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Medical Tourism Market Introduction

10.1.2.

Middle East & Africa Medical Tourism Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Healthcare

Services

10.1.2.2. By Service

Provider

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Medical Tourism Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Medical Tourism Market Introduction

11.1.2.

Latin

America Medical Tourism Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Healthcare

Services

11.1.2.2. By Service

Provider

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Medical Tourism Market Product Mapping

13.2.

Global

Medical Tourism Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

13.3.

Global

Medical Tourism Market Tier Structure Analysis

13.4.

Global

Medical Tourism Market Concentration & Company Market Shares (%) Analysis,

2024

14.

Company

Profiles

14.1.

Bumrungrad International Hospital

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Apollo

Hospitals Enterprise

14.3. Bangkok

Hospital

14.4. Anadolu

Medical Center

14.5. Fortis

Healthcare

14.6. Prince

Court Medical Centre

14.7. Asklepios

Kliniken

14.8. Shouldice

Hospital

14.9. Samitivej

Hospital

14.10. Gleneagles

Hospital

14.11. Raffles

Medical Group

14.12. KPJ

Healthcare Berhad

14.13. Clemenceau

Medical Center

14.14. Asian

Heart Institute

14.15. Burjeel

Hospital

14.16. Christus

Muguerza

14.17. Hospital

Clínic de Barcelona

14.18. UZ

Leuven

14.19. Johns

Hopkins Medicine International

14.20. Mayo

Clinic

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables