Global Milk Mineral Concentrate Market Size and Forecast (2025–2033), Growth Trends, Share, and Industry Analysis Report Coverage: By Calcium Content (Less than 20%, 20% to 25%, 26% to 30%, Others), By Granularity (Standard Powder (>10 microns), Micronized Powder (<10 microns)), By Application (Infant Formula, Functional Food, Beverages, Sports Nutrition, Dietary Supplements, Others), and Geography

2026-01-02

Consumer Products

Jaya Bundele (Research Analyst)

Description

Milk Mineral Concentrate Market Overview

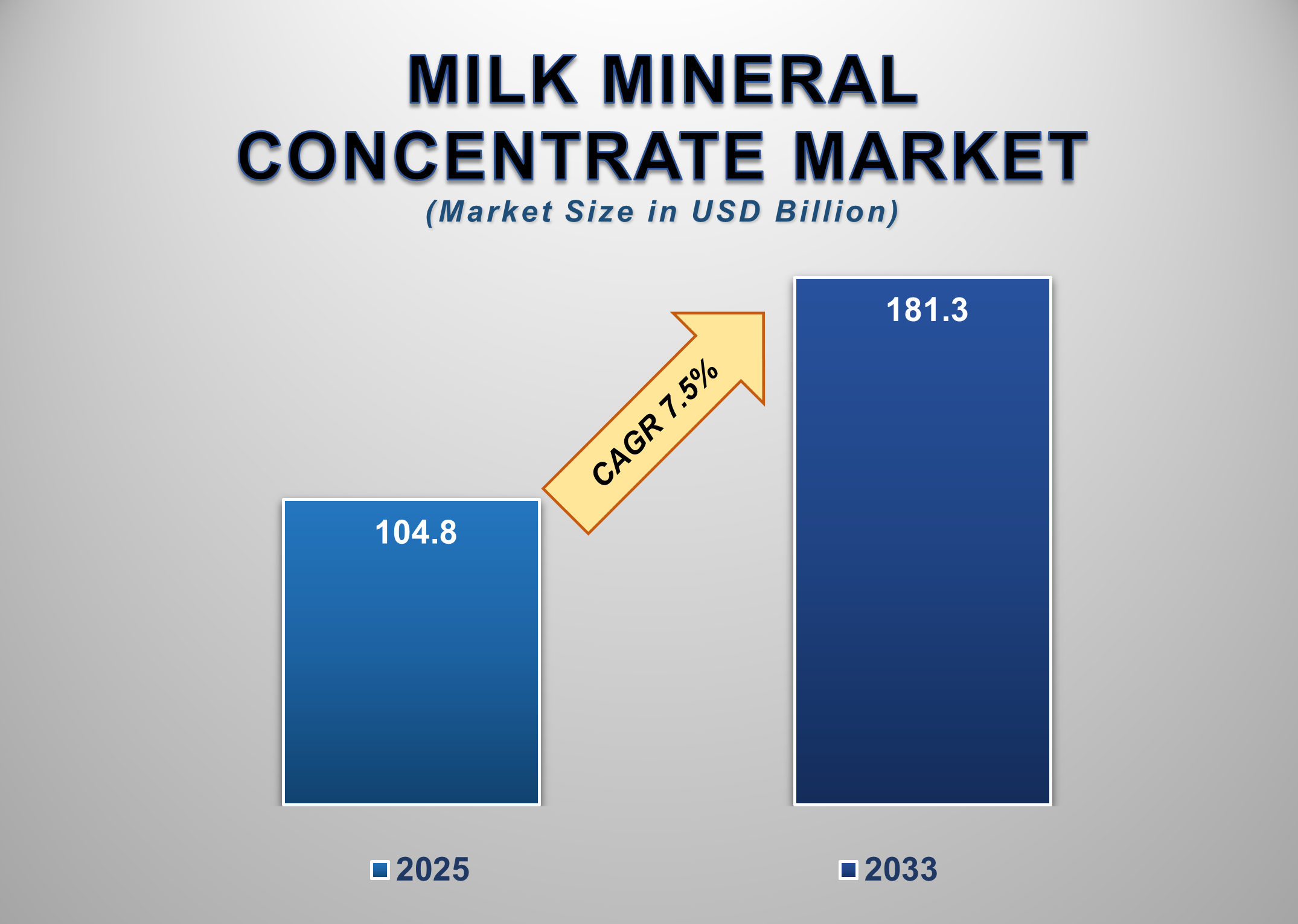

The Global Milk Mineral Concentrate Market is projected to grow from USD 104.8 billion in 2025 to USD 181.3 billion by 2033, registering a CAGR of 7.5% during the forecast period. Milk mineral concentrates, derived from milk permeate or whey streams, provide a highly bioavailable source of calcium, phosphorus, magnesium, and other essential minerals, making them increasingly valuable in the nutrition, food, and beverage sectors.

Growing consumer interest in bone

health, clean-label nutrition, and functional ingredients is driving widespread

industry adoption. The expanding demand for infant formula, sports nutrition,

and dietary supplements is elevating the market’s growth trajectory, as

manufacturers seek premium mineral sources aligned with safety, purity, and

regulatory compliance. The shift toward micronized powders is further improving

ingredient solubility and functionality in beverages and ready-to-mix

formulations.

Milk Mineral Concentrate

Market Drivers and Opportunities

Rising Demand for Nutrient-Dense Products Is Driving the Milk

Mineral Concentrate Market Growth

The global push toward nutrient-dense and functional foods

continues to be a major driver of the Milk Mineral Concentrate Market.

Consumers are increasingly prioritizing health and wellness, resulting in

heightened demand for products that support bone strength, muscle development,

metabolic functions, and overall wellness. Milk mineral concentrates,

containing bioavailable forms of calcium, phosphorus, and trace minerals, offer

superior absorption compared to synthetic alternatives. This advantage positions

them strongly in the evolving clean-label and natural ingredient landscape. The

growing elderly population, especially in Western markets, further accelerates

demand for mineral-enriched foods and supplements aimed at preventing

osteoporosis and age-related nutritional deficiencies. On the other hand,

manufacturers increasingly prefer milk-derived mineral blends because they

align with natural and minimally processed product claims. Rising fortification

trends across bakery, confectionery, beverage, and dairy products are expanding

commercial applications. As food brands reformulate products to meet stricter

nutritional standards, milk mineral concentrates are emerging as a preferred

functional ingredient that delivers health benefits without altering taste or

texture, strengthening market demand globally.

Expanding Applications in Infant Nutrition and Sports

Nutrition Are Supporting Market Growth

The rapid growth of the infant nutrition and sports nutrition

industries is creating strong momentum for the Milk Mineral Concentrate Market.

Infant formula manufacturers rely heavily on high-purity mineral ingredients to

replicate the nutritional composition of human milk, making milk mineral

concentrates a critical input for calcium and phosphorus fortification.

Increased birth rates in certain developing markets, along with higher demand

for premium and specialty formulas, are accelerating the ingredient’s adoption.

Additionally, micronized milk mineral powders improve dispersion and stability

in ready-to-feed formulations, further benefitting manufacturers. In parallel,

the sports nutrition market is witnessing unprecedented growth, driven by

rising fitness culture, professional sports participation, and increased

consumption of protein powders and recovery drinks. Athletes and active

consumers demand highly bioavailable minerals essential for bone strength,

muscle contraction, and electrolyte balance. Milk mineral concentrates meet

these needs effectively, offering natural mineral profiles that complement

protein-rich formulations. As sports nutrition continues to diversify into

mainstream consumer categories, the integration of milk-derived minerals is

expected to strengthen, creating sustained demand across global markets.

Emerging Opportunities in Clean-Label Beverages and

Functional Food Innovations

The growing clean-label

movement represents a major opportunity for the Milk Mineral Concentrate

Market. Consumers globally are shifting toward recognizable, simple, and

naturally sourced ingredients, prompting manufacturers to replace synthetic

mineral additives with dairy-derived alternatives. Milk mineral concentrates

are ideally positioned to meet this demand due to their natural origin,

superior bioavailability, and compatibility with clean-label claims. The

beverage industry is particularly poised for significant adoption, as companies

introduce mineral-enriched water, dairy-based drinks, and plant-based beverage

blends fortified with natural minerals. Next-generation product innovations,

including protein shakes, meal replacements, and functional hydration products,

are incorporating milk minerals to enhance nutritional density. Additionally,

advances in microencapsulation and particle-size reduction technologies are

enabling new product formats with improved solubility and sensory profiles. As

functional beverages continue to gain traction globally, the industry presents

a high-growth opportunity for suppliers of milk mineral concentrates. Beyond

beverages, applications in bakery, cereals, snacks, and fortified foods are

broadening, strengthening the ingredient’s outlook across multiple emerging

markets.

Milk Mineral Concentrate

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 104.8 Billion |

|

Market Forecast in 2033 |

USD 181.3 Billion |

|

CAGR % 2025-2033 |

7.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Calcium

Content, By Granularity, By Application |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Milk Mineral Concentrate

Market Report Segmentation Analysis

The global Milk Mineral Concentrate Market is segmented by Calcium

Content, by Granularity, by Application, and by Region.

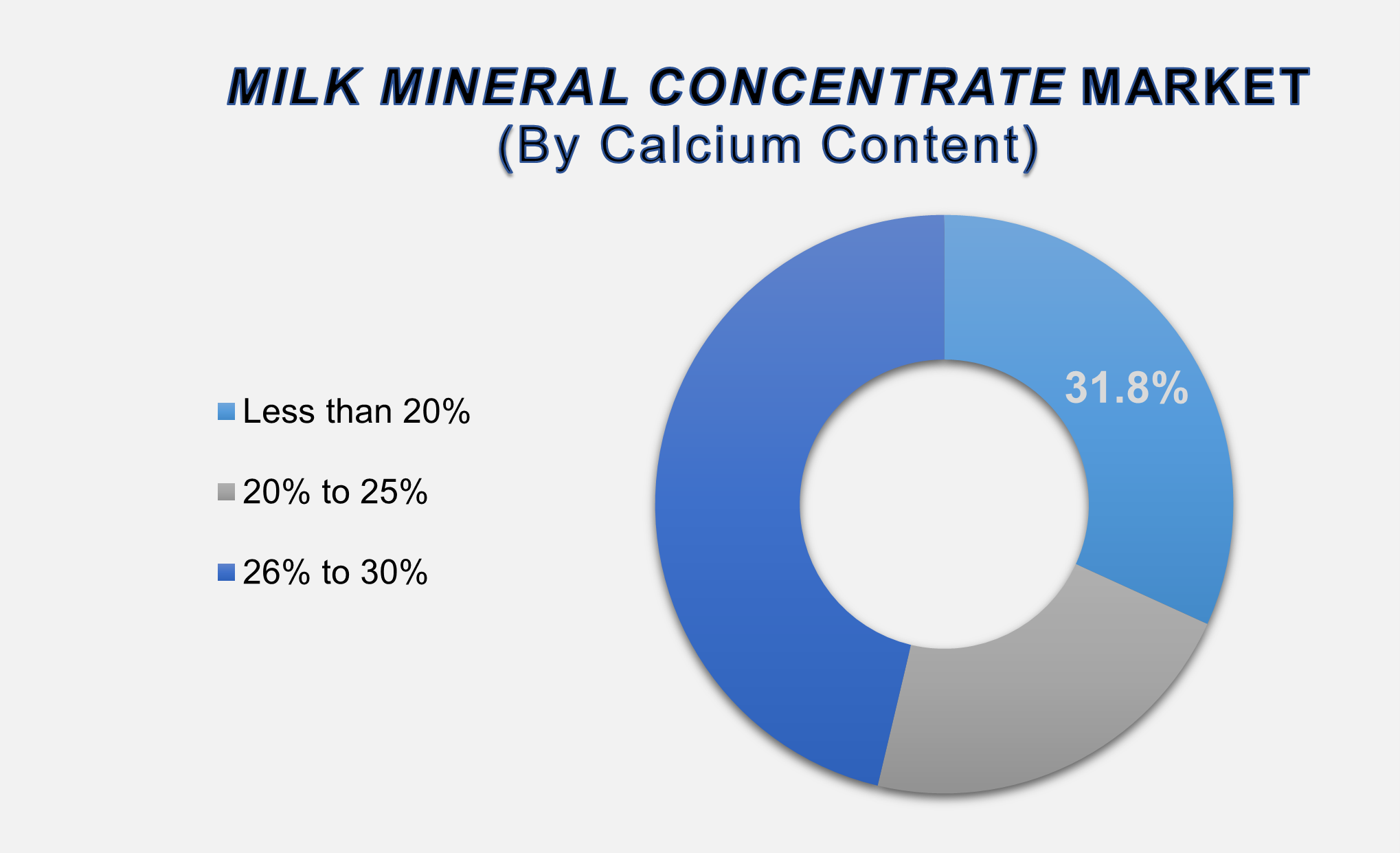

The less than 20% segment

accounted for the largest market share in the global milk mineral concentrate

market.

This dominance is attributed to the segment’s widespread use across infant formula, beverages, and functional food applications, where lower calcium concentrations support balanced mineral profiles and improved product stability. Formulators benefit from the segment’s versatility, as it provides an optimal ratio of calcium to phosphorus that closely mirrors natural milk composition, ensuring high bioavailability for consumers across all age groups. The segment is also preferred for products targeting general wellness, fortification, and dietary supplementation without altering the sensory properties of the end product. As demand for fortified beverages and dairy alternatives increases, the less than 20% calcium segment continues to gain prominence. Meanwhile, other segments, such as the 20%–25% and 26%–30% categories, are also expanding, supported by specialized applications in sports nutrition and therapeutic nutritional products. With evolving consumer preferences and regulatory approvals, the calcium content-based segmentation will remain crucial in shaping product innovation across global markets.

The Standard Powder

(>10 microns) segment accounted for the largest market share in the global

milk mineral concentrate market.

Standard powders remain the

preferred format for major applications such as bakery, dairy foods, cereals,

and infant formula, owing to their ease of handling, good dispersibility, and

cost efficiency. The segment benefits from broad product compatibility and

strong demand from large-scale food manufacturers who rely on stable,

consistent mineral sources for mass production. On the other hand, micronized

powder (<10 microns) is gaining momentum, driven by its superior solubility

and suitability for beverages, instant mixes, and sports nutrition

formulations. Micronized materials offer improved texture, reduced grittiness,

and enhanced bioavailability, making them ideal for premium functional food and

beverage products. As consumer preferences shift toward smooth,

ready-to-consume nutritional solutions, the micronized category is expected to

grow at a faster pace. The interplay between cost-efficiency and performance

benefits is shaping the growth dynamics within the granularity-based

segmentation.

The Infant Formula

segment accounted for the largest market share in the global milk mineral

concentrate market.

The rising demand for

nutritionally advanced infant formula products is driving strong adoption of

milk mineral concentrates, which serve as a critical source of calcium,

phosphorus, and trace minerals essential for infant development. Infant formula

manufacturers prioritize high-purity, safe, and bioavailable mineral inputs,

positioning milk-derived concentrates as the gold standard in this category.

Growing birth rates in the Asia Pacific, increasing adoption of premium

products, and rising awareness of infant nutrition are accelerating demand

within this segment. Additionally, functional food and sports nutrition

applications are expanding rapidly, supported by trends toward active

lifestyles and clean-label nutrition. Dietary supplements and beverages integrating

milk minerals are also witnessing growth, particularly in North America and

Europe. As product innovation expands in functional foods and drinks, milk

mineral concentrates will play a larger role across all application categories,

reinforcing their importance in the global nutrition ecosystem.

The following segments are

part of an in-depth analysis of the global Milk Mineral Concentrate market:

|

Market Segments |

|

|

By Calcium

Content |

●

Less than 20% ●

20% to 25% ●

26% to 30% |

|

By Granularity |

●

Standard Powder

(>10 microns) ●

Micronized Powder

(<10 microns) |

|

By Application |

●

Infant Formula ●

Functional Food ●

Beverages ●

Sports Nutrition ●

Dietary Supplements ●

Others |

Milk Mineral Concentrate

Market Share Analysis by Region

North America is

anticipated to hold the biggest portion of the Milk Mineral Concentrate Market

globally throughout the forecast period.

North America dominates the

global Milk Mineral Concentrate Market, accounting for 39.1% of the total share

in 2025, driven by high consumption of fortified foods, advanced dairy

processing capabilities, and strong regulatory support for nutritional enhancement.

The region benefits from robust demand across infant formula, sports nutrition,

and dietary supplements, supported by a large health-conscious population and

high household spending on premium nutrition products. Extensive R&D

investments from leading dairy companies in the U.S. and Canada further

contribute to innovation in milk mineral extraction and formulation

technologies. Europe also represents a significant market, with established

dairy cooperatives, strong functional food consumption, and growing interest in

clean-label products.

However, the Asia Pacific is

projected to record the highest CAGR during the forecast period. The region’s

growth is fueled by expanding infant formula markets in China, India, and

Southeast Asia, coupled with rising purchasing power and increasing adoption of

fortified foods. The shift toward active lifestyles and higher demand for

sports nutrition are reinforcing this trend. Latin America and the Middle East

& Africa are emerging markets, showing positive adoption as food

fortification initiatives expand across developing economies.

Milk Mineral Concentrate

Market Competition Landscape Analysis

The competitive landscape of the

Milk Mineral Concentrate Market is characterized by strong participation from

global dairy ingredient manufacturers, nutrition companies, and specialty

mineral processors. Key players are focusing on improving extraction technologies,

enhancing product purity, and expanding their micronized powder capabilities to

meet evolving industry needs.

Global Milk Mineral

Concentrate Market Recent Developments News:

- In June 2022,

Sachsenmilch Leppersdorf GmbH agreed

with FrieslandCampina DOMO to acquire five dairy brands and three

production facilities, expanding its product portfolio and manufacturing

capabilities in the European dairy market.

- In March 2022,

Arla Foods Ingredients launched two new organic products for early

life nutrition, reinforcing its commitment to the organic segment and

strengthening its market position in specialized infant and toddler

nutrition.

The Global Milk Mineral Concentrate Market Is Dominated by a Few Large Companies, such as

●

Armor Protéines

●

Arla Foods Ingredients

●

Glanbia

●

Hilmar Ingredients

●

Sachsenmilch

Leppersdorf

●

Erie Foods

International

●

Fonterra

●

Milk Specialties

Global

●

Ingredia

●

Kerry Group

●

FrieslandCampina

●

Saputo

●

Lactalis

●

Dairy Farmers of

America

●

Agropur

●

Valio

●

Südzucker

●

Meggle

●

Hoogwegt

●

Milk Powder Solutions

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Milk Mineral

Concentrate Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Milk Mineral Concentrate Market Scope and Market Estimation

1.2.1.Global Milk Mineral

Concentrate Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Milk Mineral

Concentrate Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Calcium Content of Global Milk

Mineral Concentrate Market

1.3.2.Granularity of Global Milk

Mineral Concentrate Market

1.3.3.Application of Global Milk

Mineral Concentrate Market

1.3.4.Region of Global Milk

Mineral Concentrate Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Milk Mineral Concentrate Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Milk Mineral Concentrate Market Estimates

& Forecast Trend Analysis, by Calcium Content

4.1.

Global

Milk Mineral Concentrate Market Revenue (US$ Bn) Estimates and Forecasts, by Calcium

Content, 2020 - 2033

4.1.1.Less than 20%

4.1.2.20% to 25%

4.1.3.26% to 30%

5. Global

Milk Mineral Concentrate Market Estimates

& Forecast Trend Analysis, by Granularity

5.1.

Global

Milk Mineral Concentrate Market Revenue (US$ Bn) Estimates and Forecasts, by Granularity,

2020 - 2033

5.1.1.Standard Powder (>10

microns)

5.1.2.Micronized Powder (<10

microns)

6. Global

Milk Mineral Concentrate Market Estimates

& Forecast Trend Analysis, by Application

6.1.

Global

Milk Mineral Concentrate Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

6.1.1.Infant Formula

6.1.2.Functional Food

6.1.3.Beverages

6.1.4.Sports Nutrition

6.1.5.Dietary Supplements

6.1.6.Others

7. Global

Milk Mineral Concentrate Market Estimates

& Forecast Trend Analysis, by Region

7.1.

Global

Milk Mineral Concentrate Market Revenue (US$ Bn) Estimates and Forecasts, by Region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Milk

Mineral Concentrate Market: Estimates

& Forecast Trend Analysis

8.1.

North

America Milk Mineral Concentrate Market Assessments & Key Findings

8.1.1.North America Milk Mineral

Concentrate Market Introduction

8.1.2.North America Milk Mineral

Concentrate Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Calcium

Content

8.1.2.2. By Granularity

8.1.2.3. By Application

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Milk

Mineral Concentrate Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Milk Mineral Concentrate Market Assessments & Key Findings

9.1.1.Europe Milk Mineral

Concentrate Market Introduction

9.1.2.Europe Milk Mineral

Concentrate Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Calcium

Content

9.1.2.2. By Granularity

9.1.2.3. By Application

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Milk

Mineral Concentrate Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Milk Mineral Concentrate Market Introduction

10.1.2.

Asia

Pacific Milk Mineral Concentrate Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Calcium

Content

10.1.2.2. By Granularity

10.1.2.3. By Application

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Milk

Mineral Concentrate Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Milk Mineral Concentrate Market

Introduction

11.1.2.

Middle East & Africa Milk Mineral Concentrate Market Size

Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Calcium

Content

11.1.2.2. By Granularity

11.1.2.3. By Application

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Milk Mineral Concentrate Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Milk Mineral Concentrate Market Introduction

12.1.2.

Latin

America Milk Mineral Concentrate Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Calcium

Content

12.1.2.2. By Granularity

12.1.2.3. By Application

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Milk Mineral Concentrate Market Product Mapping

14.2.

Global

Milk Mineral Concentrate Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Milk Mineral Concentrate Market Tier Structure Analysis

14.4.

Global

Milk Mineral Concentrate Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

Armor Protéines

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Arla

Foods Ingredients

15.3. Glanbia

15.4. Hilmar

Ingredients

15.5. Sachsenmilch

Leppersdorf

15.6. Erie

Foods International

15.7. Fonterra

15.8. Milk

Specialties Global

15.9. Ingredia

15.10. Kerry

Group

15.11. FrieslandCampina

15.12. Saputo

15.13. Lactalis

15.14. Dairy

Farmers of America

15.15. Agropur

15.16. Valio

15.17. Südzucker

15.18. Meggle

15.19. Hoogwegt

15.20. Milk

Powder Solutions

15.21. Others

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables