Milk Packaging Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Material (Plastic, Paper & Paperboard, Glass, Metal), By Packaging Type (Pouches, Cartons, Bottles & Cans, Others), and Geography

2026-02-17

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Milk

Packaging Market Overview

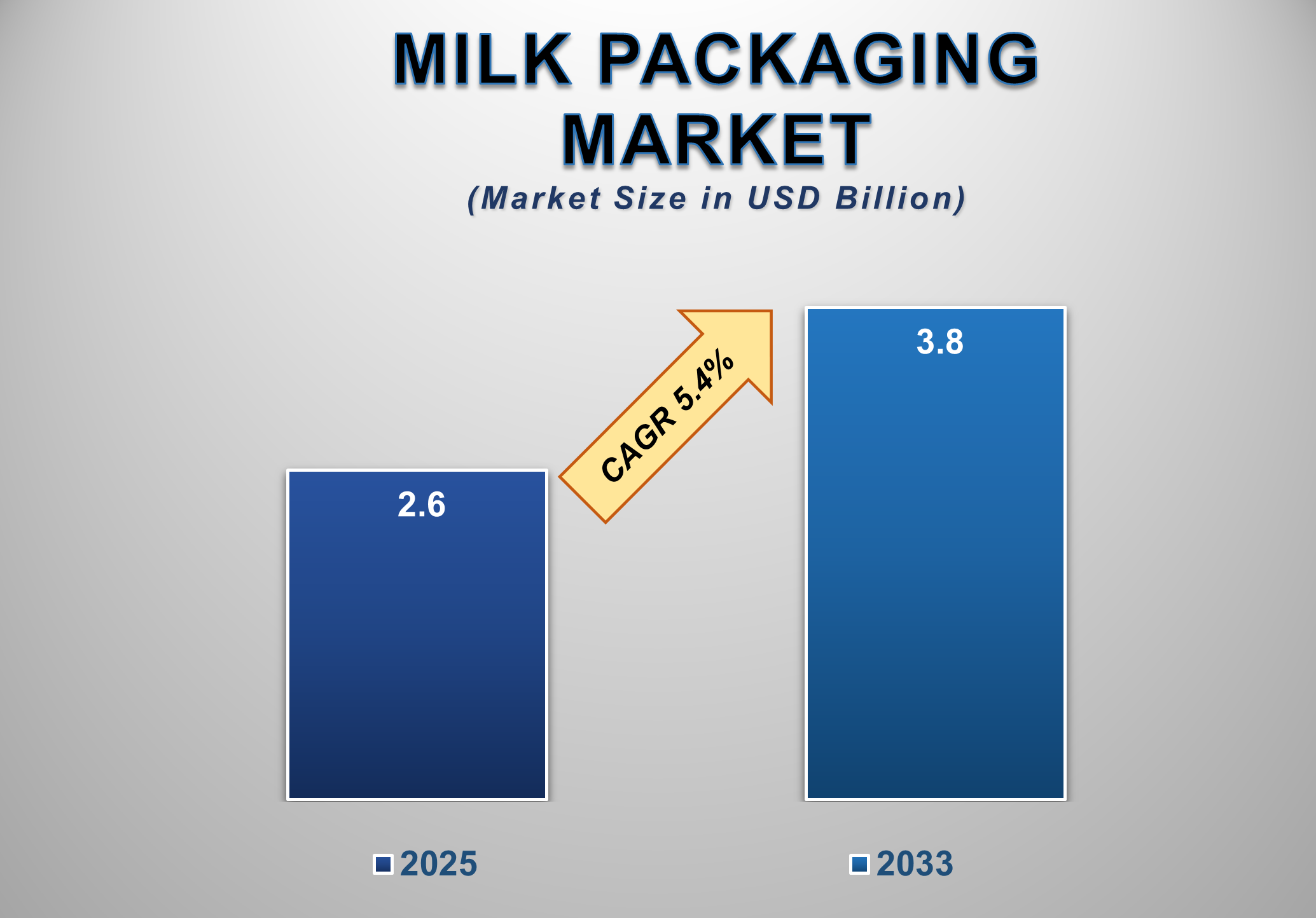

The global Milk Packaging Market plays a vital role in the dairy value chain by ensuring product safety, extending shelf life, preserving nutritional quality, and enabling efficient distribution of milk and milk-based beverages. Packaging solutions for milk must meet stringent requirements related to hygiene, barrier protection, durability, and sustainability, making innovation and material selection critical factors shaping the market. In 2025, the global milk packaging market is valued at USD 2.6 billion and is projected to reach USD 3.8 billion by 2033, growing at a CAGR of 5.4% during the forecast period.

Market growth is closely tied to

rising global milk consumption, increasing urbanization, and the expansion of

organized dairy processing and retail infrastructure. As consumers demand safe,

convenient, and affordable milk products, dairy producers are increasingly

adopting advanced packaging formats that enhance product shelf life and

facilitate cold-chain and ambient distribution. Single-serve and flexible

packaging formats are gaining popularity due to changing lifestyles and growing

demand for on-the-go consumption.

Milk Packaging Market Drivers and Opportunities

Rising Milk Consumption

and Expansion of the Organized Dairy Industry Are Driving Market Growth

The steady rise in global milk

consumption is a key driver of growth in the milk packaging market. Milk

remains a staple dietary product across most regions, consumed daily by

households and used extensively in foodservice and food processing applications.

Population growth, rising disposable income, and increasing awareness of the

nutritional benefits of milk, particularly its protein and calcium content, are

contributing to sustained demand. Simultaneously, the expansion of the

organized dairy industry is transforming milk packaging requirements.

Traditional loose milk distribution is gradually being replaced by packaged

milk, especially in developing economies, due to rising concerns around

hygiene, quality, and food safety. Organized dairy players are investing in

modern processing and packaging facilities to meet regulatory standards and

consumer expectations. Packaged milk ensures consistent quality, longer shelf

life, and improved traceability, making it more attractive to urban consumers.

As governments tighten food safety regulations and promote packaged dairy

consumption, demand for reliable and scalable milk packaging solutions is

expected to grow steadily throughout the forecast period.

Shift Toward Convenient

and Cost-Effective Packaging Formats Is Accelerating Adoption

Changing consumer lifestyles and

purchasing behavior are accelerating demand for convenient and cost-effective

milk packaging formats. Flexible packaging solutions, particularly pouches, are

gaining traction due to their low material usage, reduced transportation costs,

and ease of handling. These benefits are especially important in

price-sensitive and high-volume markets. Pouches enable dairy producers to

offer milk at affordable price points while maintaining acceptable shelf life

and product safety. Their lightweight nature also reduces carbon emissions

associated with transportation, aligning with sustainability goals.

Additionally, advancements in multilayer plastic films have improved barrier

properties, helping protect milk from contamination and spoilage. In developed

markets, convenience is driving demand for resealable cartons and bottles that

support longer storage and multiple usage occasions. As consumers seek

packaging that balances affordability, convenience, and sustainability,

manufacturers are diversifying packaging portfolios to cater to varied regional

and demographic preferences.

Sustainability

Initiatives and Material Innovation Are Creating Significant Opportunities

Sustainability has emerged as a major opportunity area within the milk packaging market. Growing environmental concerns and regulatory pressure to reduce plastic waste are pushing packaging manufacturers and dairy brands to invest in recyclable, renewable, and lightweight materials. Paper-based cartons, bio-based plastics, and mono-material structures are gaining increasing attention. In North America and Europe, consumer preference is shifting toward eco-friendly packaging, encouraging the adoption of paper & paperboard cartons and recyclable plastic bottles. Packaging companies are developing innovative solutions such as tethered caps, reduced plastic content designs, and recyclable multilayer structures to meet sustainability targets without compromising performance. Emerging economies also present opportunities as governments promote sustainable packaging practices and waste management infrastructure improves. As sustainability becomes a key differentiator for dairy brands, investments in material innovation and circular economy solutions are expected to create long-term growth opportunities in the milk packaging market.

Milk Packaging Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.6 Billion |

|

Market Forecast in 2033 |

USD 3.8 Billion |

|

CAGR % 2025-2033 |

5.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

Material,

Packaging Type |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Russia 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Saudi Arabia 17)

UAE 18)

South Africa

|

Milk Packaging Market

Report Segmentation Analysis

The Global Milk Packaging Market

Industry Analysis Is Segmented By Material, Packaging Type, And By Region.

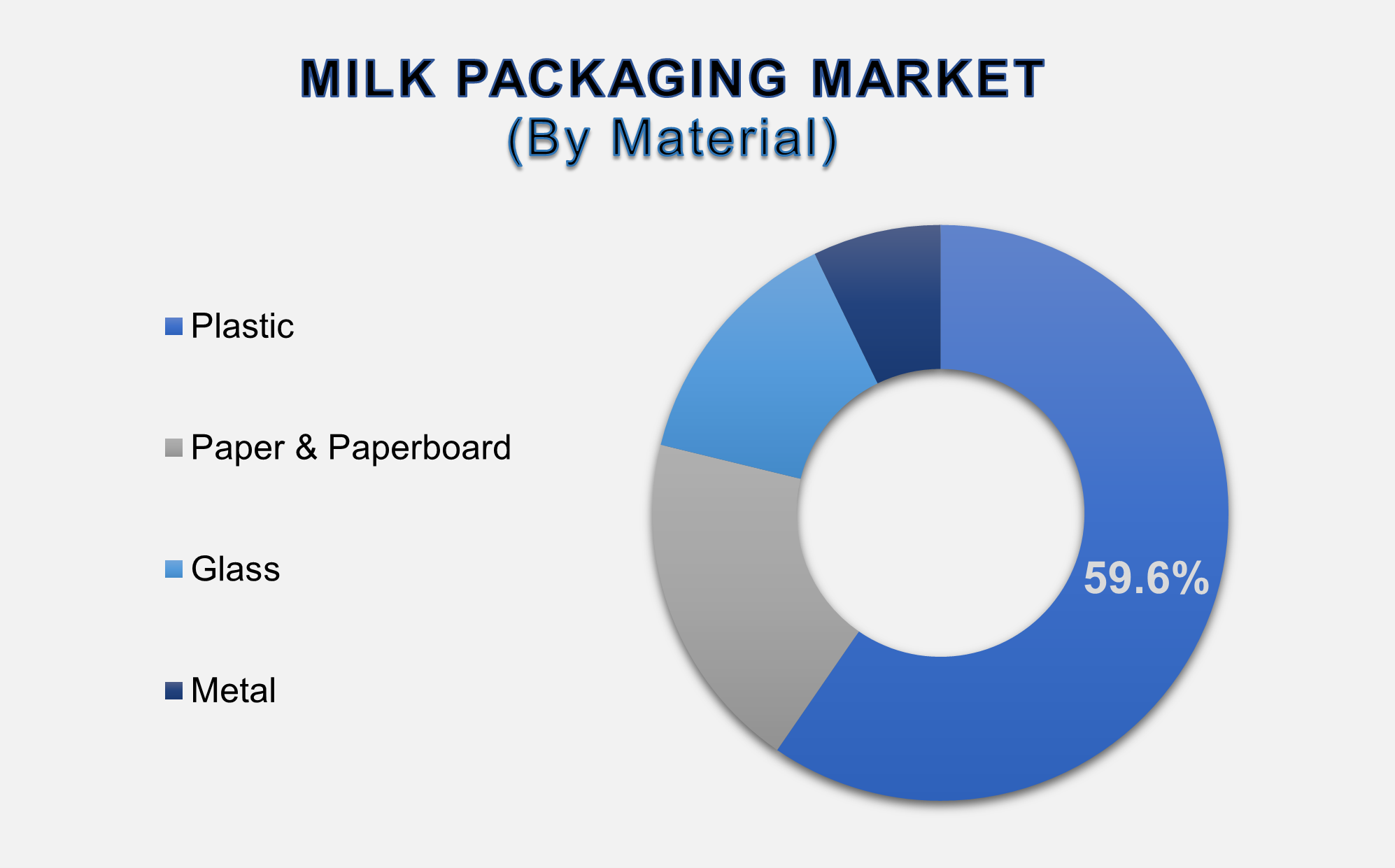

Plastic Segment Accounted

for the Largest Market Share in the Global Milk Packaging Market

The plastic segment accounted for

the largest share of the global milk packaging market, contributing 59.6% of

total revenue. Plastic materials such as polyethylene and polypropylene are

widely used in milk packaging due to their durability, lightweight properties,

and compatibility with flexible and rigid packaging formats. Plastic packaging

supports high-speed filling processes, reduces breakage risk, and lowers

transportation costs compared to glass and metal alternatives. Its dominance is

particularly strong in the Asia Pacific, where plastic pouches are the

preferred format for packaged milk distribution.

Despite increasing sustainability concerns, plastic remains indispensable due to its cost advantages and functional performance. Ongoing innovation in recyclable and bio-based plastics is expected to support the continued growth of this segment while addressing environmental challenges.

Pouches Segment Dominated

the Market by Packaging Type

The pouches segment dominates the

global milk packaging market, driven by widespread adoption in high-consumption

and price-sensitive regions. Pouches require less material than rigid packaging

formats, making them highly cost-effective for dairy producers and consumers

alike. Their lightweight design simplifies transportation and storage, reducing

logistics costs across the supply chain. Pouches are particularly popular in

Asia Pacific markets, where daily milk consumption volumes are high, and

affordability is a key purchasing factor. Advancements in film technology have

improved pouch durability and barrier performance, enhancing shelf life and

safety. As flexible packaging continues to evolve, pouches are expected to

maintain their leading position in the global milk packaging market.

The following segments are

part of an in-depth analysis of the global Milk Packaging market:

|

Market

Segments |

|

|

By Material |

●

Plastic ●

Paper &

Paperboard ●

Glass ●

Metal |

|

By Packaging

Type |

●

Pouches ●

Cartons ●

Bottles & Cans ●

Others |

Milk Packaging Market

Share Analysis By Region

Asia Pacific Is Projected

to Hold the Largest Share of The Global Milk Packaging Market Over the Forecast

Period.

Asia Pacific accounted for 43.9%

of the global milk packaging market, making it the largest regional

contributor. The region’s dominance is driven by high population density,

strong per capita milk consumption, and the extensive use of plastic pouch packaging

in countries such as India, China, and Southeast Asian nations. Rapid

urbanization and the expansion of organized dairy retail further support market

growth.

North America is expected to

register the highest CAGR during the forecast period, supported by increasing

demand for sustainable and premium milk packaging solutions. Consumers in the

region prefer cartons and bottles with enhanced convenience features, such as

resealable caps and extended shelf life. Regulatory emphasis on recyclable

packaging and strong innovation capabilities among packaging manufacturers are

accelerating market growth in North America.

Milk Packaging Market Competition Landscape

Analysis

The global milk packaging market

is moderately consolidated, with the presence of multinational packaging

companies and regional players. Competition is based on material innovation,

sustainability performance, cost efficiency, and long-term partnerships with

dairy producers. Leading players invest heavily in research and development to

offer advanced packaging solutions that meet evolving regulatory and consumer

requirements.

Global Milk Packaging Market Recent Developments

News:

●

In July 2024 – Tetra

Pak and Mengniu Group launched a limited-edition Milk Deluxe Pure Milk range in

Greater China, featuring 30 unique carton designs inspired by masterpieces by

Van Gogh and Monet. The products are packaged in Tetra Prisma Aseptic 250 Edge

cartons with DreamCap 26 closures, distributed through a partnership with Meet

You Museum in both online and physical stores.

●

In April 2024 – Nampak

Liquid Cartons, in collaboration with Woodlands Dairy, introduced South

Africa’s first tethered cap carton. The design is intended to reduce plastic

waste by keeping the cap attached to the carton throughout its lifecycle,

including the recycling process.

●

In January 2024 – Coop

and Emmi launched sustainable PET bottles for dairy products in Switzerland.

The packaging shift applies to select milk and cream products under Coop’s

private labels as well as several Emmi brand products, such as Emmi Energy Milk.

●

In August 2022 –

Delamere Dairy reintroduced its fresh goat's milk range in the U.K. in a new

SIG CombiDome packaging design. The format

combines the pouring convenience of a bottle with the environmental benefits of

the brick-shaped cartons previously used.

The Global Milk Packaging Market

is dominated by a few large companies, such as

●

Tetra Pak

●

SIG Combibloc

●

Elopak

●

Evergreen Packaging

●

Nippon Paper Industries

●

International Paper

●

Amcor

●

Mondi Group

●

Sealed Air

●

Ball Corporation

●

Berry Global

●

Sonoco

●

Huhtamaki

●

Liqui-Box

●

Krones

●

DS Smith

●

Graphic Packaging

●

Constantia Flexibles

●

IPI s.r.l.

●

Refresco

● Others

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Milk Packaging

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Milk Packaging Market Scope and Market Estimation

1.2.1.Global Milk Packaging Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Milk Packaging

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Material of Global Milk

Packaging Market

1.3.2.Packaging Type of Global Milk

Packaging Market

1.3.3.Region of Global Milk

Packaging Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Overview

of Tariff, Regulatory Landscape and Standards

2.7.

Market

Entry Strategies

2.8.

Market

Dynamics

2.8.1.Drivers

2.8.2.Limitations

2.8.3.Opportunities

2.8.4.Impact Analysis of Drivers

and Restraints

2.9.

Porter’s

Five Forces Analysis

2.10.

PEST

Analysis

3. Global

Milk Packaging Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Milk Packaging Market Estimates

& Forecast Trend Analysis, by Material

4.1.

Global

Milk Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020

- 2033

4.1.1.Plastic

4.1.2.Paper & Paperboard

4.1.3.Glass

4.1.4.Metal

5. Global

Milk Packaging Market Estimates

& Forecast Trend Analysis, by Packaging Type

5.1.

Global

Milk Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Packaging

Type, 2020 - 2033

5.1.1.Pouches

5.1.2.Cartons

5.1.3.Bottles & Cans

5.1.4.Others

6. Global

Milk Packaging Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Milk Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020

- 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Milk

Packaging Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Milk Packaging Market Assessments & Key Findings

7.1.1.North America Milk

Packaging Market Introduction

7.1.2.North America Milk

Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Material

7.1.2.2. By Packaging

Type

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Milk

Packaging Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Milk Packaging Market Assessments & Key Findings

8.1.1.Europe Milk Packaging

Market Introduction

8.1.2.Europe Milk Packaging

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Material

8.1.2.2. By Packaging

Type

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Milk

Packaging Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Milk

Packaging Market Introduction

9.1.2.Asia Pacific Milk

Packaging Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Material

9.1.2.2. By Packaging

Type

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Milk

Packaging Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Milk Packaging Market Introduction

10.1.2.

Middle East & Africa Milk Packaging Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Material

10.1.2.2. By Packaging

Type

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Milk Packaging Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Milk Packaging Market Introduction

11.1.2.

Latin

America Milk Packaging Market Size Estimates and Forecast (US$ Billion) (2020 -

2033)

11.1.2.1. By Material

11.1.2.2. By Packaging

Type

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Milk Packaging Market Product Mapping

13.2.

Global

Milk Packaging Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

13.3.

Global

Milk Packaging Market Tier Structure Analysis

13.4.

Global

Milk Packaging Market Concentration & Company Market Shares (%) Analysis,

2024

14.

Company

Profiles

14.1.

Tetra Pak

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. SIG

Combibloc

14.3. Elopak

14.4. Evergreen

Packaging

14.5. Nippon

Paper Industries

14.6. International

Paper

14.7. Amcor

14.8. Mondi

Group

14.9. Sealed

Air

14.10. Ball

Corporation

14.11. Berry

Global

14.12. Sonoco

14.13. Huhtamaki

14.14. Liqui-Box

14.15. Krones

14.16. DS Smith

14.17. Graphic

Packaging

14.18. Constantia

Flexibles

14.19. IPI

s.r.l.

14.20. Refresco

14.21. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables