Mobile Health (mHealth) Market Size and Forecast (2025 - 2035), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product Type (mHealth Apps, Wearable Devices and mHealth Services); By Platform (Android, iOS and Others); By Application (Chronic Disease Management, General Health and Wellness, Remote Patient Monitoring, Clinical Decision Support, Diagnostics and Treatment, Preventive Healthcare and Mental Health Support); By End-user (Patients/Consumers, Healthcare Providers, Payers (Insurance companies), Pharmaceutical Companies, Government/Public Health Agencies) and Geography

2025-08-20

Healthcare

Swetal (Research Analyst)

Description

Mobile

Health (mHealth) Market Overview

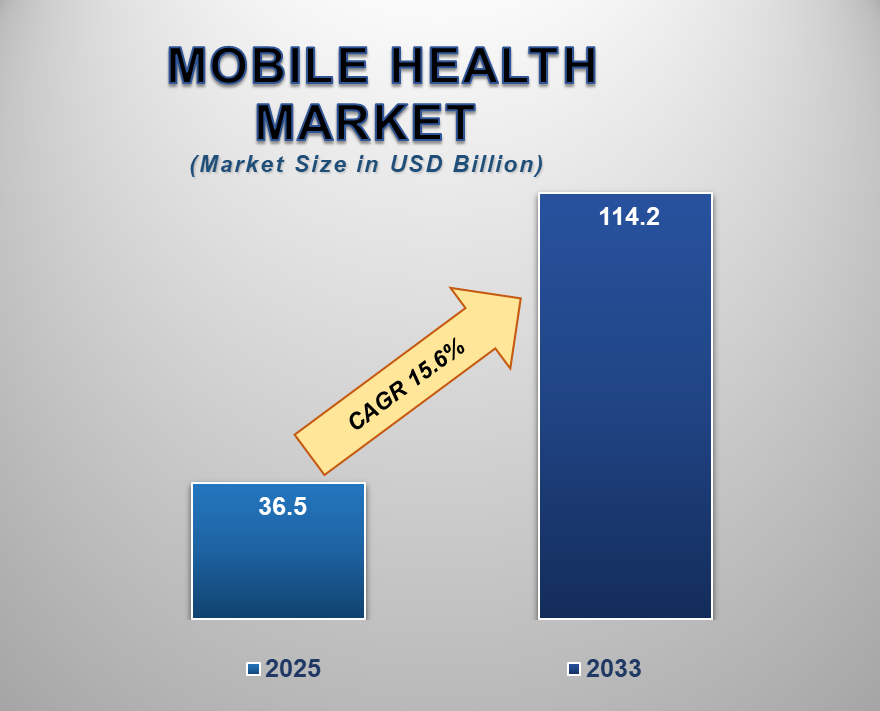

The Mobile Health (mHealth) Market size is anticipated to experience substantial growth from 2025 to 2035, fuelled by increasing internet and smartphone penetration and growing awareness of maintaining physical health and lifestyle improvement to further boost the adoption of mobile health market. With an estimated valuation of approximately USD 36.5 billion in 2025, the market is expected to reach USD 160.1 billion by 2035, registering a robust compound annual growth rate (CAGR) of 14.5% over the decade.

The Mobile Health (mHealth)

sector has emerged as the disruptive force within the healthcare sector,

powered by the mass adoption of smartphones, rising internet availability, and

the demand for affordable and personalized care. mHealth refers to the extensive

spectrum of digital health solutions such as mobile applications, wearable

technology, remote monitoring devices, and telemedicine services, facilitating

instant tracking, diagnosing, and treatment. It empowers both patients and

healthcare professionals by providing tools for managing long-term illnesses,

wellness monitoring, medication adherence, mental health care, and virtual

consultations.

The market has picked up rapidly

due to increased health consciousness, prominently in the post-COVID-19 period,

which has fueled the adoption of digital health platforms worldwide.

Governments and health organizations are increasingly backing mHealth through

regulatory frameworks as well as funding to alleviate the pressure from

conventional health infrastructure. Technological innovations like AI, big data

analytics, as well as the integration of IoT are further bolstering the

functionality of mHealth solutions, making them more accurate and easier to

use. Industry leaders like Apple, Google, Philips, and Teladoc are heavily

investing in innovation, broadening the market space. Even though the market is

growing at a fast pace, challenges like data privacy, regulatory issues, as

well as restricted accessibility to low-income locations plague the market.

However, with growing investments, strategic alliances, and growing emphasis on

preventive care, the mHealth market is likely to expand significantly during the

next few years. It has the potential to transform the delivery of health care

by making it proactive, economical, and patient-friendly. As of the mid-2020s,

the market is likely to serve as the cornerstone of contemporary digital health

ecosystems across the globe.

Mobile

Health (mHealth) Market Drivers and Opportunities

Growing

Smartphone and Internet Penetration are anticipated to lift the Mobile Health

(mHealth) Market during the forecast period

The prevalence of smartphones and

growing internet access has emerged as core drivers for the mHealth market.

Smartphones in both developed and developing countries provide an accessible

platform to access health apps, telemedicine, and wearable device integration.

With billions of active mobile users around the globe, healthcare services are

at one's fingertips, facilitating distant monitoring, virtual consultations,

and health monitoring. This ease of access empowers people to take proactive

control of their well-being, chronic care, and lifestyle behaviours. In

addition, mobile applications enable ongoing health data gathering and transfer

for better provider decision-making and preventive care. Convergence of health

care and mobility has a significant impact in rural or underserved communities

where access to conventional medical infrastructure is minimal. With growing

mobility, mHealth solutions are proving to be indispensable facilitators in the

delivery of timely, affordable, and patient-centric care to global populations.

Rising

Prevalence of Chronic Diseases Drives Global Mobile Health (mHealth) Market

The mounting worldwide burden of

long-term conditions like diabetes, hypertension, cardiovascular conditions,

and respiratory illnesses is one of the main drivers of the mHealth market. All

of these long-term conditions call for continuous monitoring, management of

lifestyle, and patient education—domains where mHealth capabilities shine.

Mobile health apps and wearable technologies provide immediate monitoring of

key signs, medication compliance reminders, and alerts for atypical results,

which contribute to early intervention and decreased hospitalizations. Health

systems are implementing mHealth in order to reduce treatment expenses, improve

outcomes for diseases, and engage patients. For example, diabetes management

apps are connected to continuous glucose monitors (CGMs), offering actionable

information to benefit both providers and patients. Further, as the elderly

populations expand, scalable solutions to care remotely are needed. mHealth

provides a low-cost, adaptable way to deal with such needs, making it a key

part of approaches to managing long-term conditions worldwide.

Opportunity

for the Mobile Health (mHealth) Market

Expansion

in Emerging Markets is a significant opportunity in the global Mobile Health

(mHealth) Market

Emerging economies represent a

tremendous growth opportunity for the mHealth market because they have large

populations, underdeveloped healthcare infrastructure, and rapidly expanding

mobile connectivity. In most low- and middle-income countries, access to health

facilities is restricted, particularly to rural and far-flung areas. mHealth

fills the gap by offering health services through mobile, remote diagnostics,

and telemedicine solutions with decreased in-person visit requirements.

Governments and NGOs are increasingly investing in digital health projects to

drive related outcomes, mitigate outbreaks, and promote maternal and childhood

health. Affordability and scalability of health platforms via mobile devices

enable them to fit within these environments. In addition, smartphone

availability in Sub-Saharan Africa, Southeast Asia, and countries in South

America is growing rapidly, opening the market even wider to mHealth takeoff.

With context-specific solutions to target language, local needs, and health

issues, there's an opportunity for early market leadership to be seized as well

as for driving health improvements in underserved segments.

Mobile

Health (mHealth) Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 36.5 Billion |

|

Market Forecast in 2035 |

USD 160.1 Billion |

|

CAGR % 2025-2035 |

14.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2035 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Product Type ●

By Platform ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Benelux 9)

Nordic Countries 10)

Russia 11)

China 12)

India 13)

Japan 14)

South Korea 15)

Australia 16)

Indonesia 17)

Thailand 18)

Mexico 19)

Brazil 20)

Argentina 21)

Saudi Arabia 22)

UAE 23)

Egypt 24)

South Africa 25) Nigeria |

Mobile

Health (mHealth) Market Report Segmentation Analysis

The global Mobile Health

(mHealth) Market industry analysis is segmented by Product Type, by Platform,

by application, by end-user, and by region.

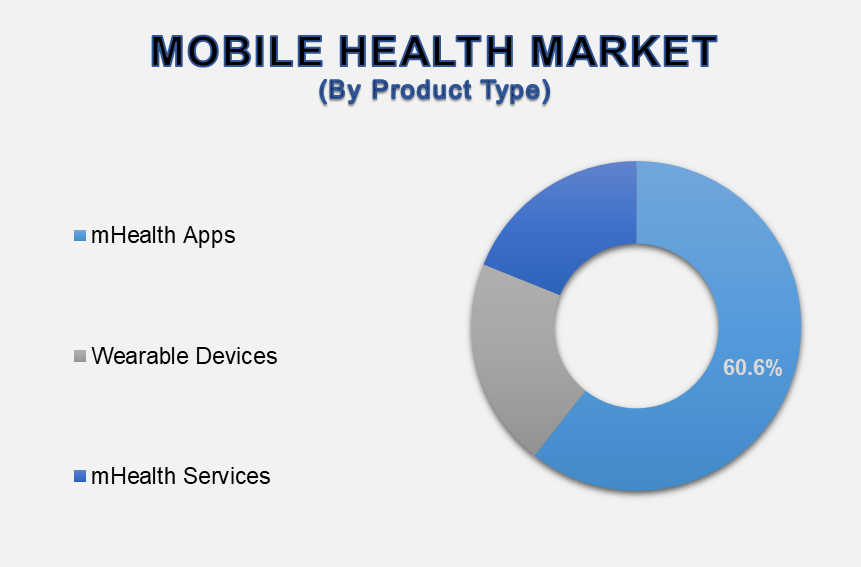

mHealth

App Product Type Segment Leading the Mobile Health (mHealth) Market

The mHealth product type segment is dominating the Mobile Health market because of its high diversity, scalability, and ease of use for its consumers. mHealth apps cater to a broad spectrum of health requirements—ranging from tracking fitness and well-being to managing chronic illnesses, mental health care, and teleconsultation. The popularity of mHealth apps stems from the ease of access and simple integration into one's daily life. One is now able to track physical exercise, sleep, diet, heart rate, and many others from the comfort of one's smartphone. mHealth apps are even favored by healthcare professionals, as they utilize the apps to monitor patient records, conduct remote consultations, and cope with care plans. Post-COVID-19, the demand for mHealth apps spiked as it exposed the necessity of telemedicine. Further, the integration of AI-powered tools in apps such as symptom checkers, tailored advice, and predictive analytics has made the apps more interactive and efficient.

Android

platforms hold a major share in the Mobile Health (mHealth) Market

A dominant share in the mHealth

market is attributed to Android platforms mainly due to its global reach,

affordability, and high market share—particularly in developing and emerging

nations. Android smartphones are more affordable and accessible to larger

segments of the population than iOS devices, thus they remain the platform of

choice for most mHealth app developers and users. This large user base compels

developers to focus mainly on Android compatibility while developing health

apps, from fitness tracking, telemedicine and management of chronic ailments.

Google Play Store also has an enormous collection of health-related apps,

following from its share of the market. Android's open nature supports

resilience to extensive customization at the platform level, which is extremely

beneficial in customizing mHealth solutions to fit particular languages,

locations, or health systems. Public health projects in nations from Asia,

through Africa, to South America tend to utilize Android-based apps to expand access

to healthcare to areas far from metropolitan centres.

Chronic

Disease Management Application Segment Dominating in Mobile Health (mHealth)

Market

The management of chronic disease

accounts for the largest share in the mHealth market due to the growing

prevalence of long-term conditions, including diabetes, hypertension,

cardiovascular ailments, and respiratory conditions. They require continuous monitoring,

proper medication compliance, and lifestyle management—tasks at which mHealth

solutions are uniquely positioned to assist. mHealth apps and wearable monitors

allow patients to monitor vital signs, record symptoms, take medication

reminders, and transmit health information to providers in real time. This

ongoing interaction facilitates early detection of complications and timelier

intervention, better outcomes for patients, and reduced healthcare spending.

Healthcare providers and payers are also finding the benefits of monitoring

remotely for long-term ailments, which reduces the frequency of hospital

utilization and increases care efficiency.

The following segments are part of an in-depth analysis of the global

Mobile Health (mHealth) Market:

|

Market Segments |

|

|

By Product Type

|

●

mHealth Apps o

Fitness &

Wellness Apps o

Disease Management

Apps o

Women's Health Apps o

Medication

Management Apps o

Mental Health Apps ●

Wearable Devices ●

mHealth Services o

Remote Monitoring o

Diagnostic Services o

Consultation

Services o

Healthcare Call

Centers |

|

By Platform

|

●

Android ●

iOS ●

Others |

|

By Application |

●

Chronic Disease

Management ●

General Health and

Wellness ●

Remote Patient

Monitoring ●

Clinical Decision

Support ●

Diagnostics and

Treatment ●

Preventive

Healthcare ●

Mental Health

Support |

|

By End-user |

●

Patients/Consumers ●

Healthcare Providers ●

Payers (Insurance

companies) ●

Pharmaceutical

Companies ●

Government/Public

Health Agencies |

Mobile

Health (mHealth) Market Share Analysis by Region

North

America is projected to hold the largest share of the global Mobile Health

(mHealth) Market over the forecast period.

North America is expected to have

the greatest share in the global mHealth market due to its well-developed

healthcare infrastructure, high smartphone and internet penetration rates, and

high adoption rates of digital health technologies. The rise in the adoption of

mHealth apps and wearable devices for tracking, management of chronic

illnesses, and e-visits has been seen in particular in the United States. Major

tech giants such as Apple, Google, and Amazon, along with healthcare giants

such as Teladoc Health and Medtronic, drive innovation and broader adoption of

the solutions in the field of mobile health. Favourable government initiatives

such as the large-scale implementation of electronic health records (EHR) and

reimbursement for telemedicine services also bolster the market. A

technologically advanced and health-conscious population with high disposable

income in North America is another reason for the boosting demand for

customized, anytime health solutions. COVID-19 has fueled the adoption of telemedicine

significantly in the region, making digital health a central aspect of the

delivery of care. Moreover, continued investment in AI, IoT, and data

protection is facilitating steady growth and trust in mHealth solutions.

Mobile

Health (mHealth) Market Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of Mobile Health products and services. Some of the key players are Apple Inc., Google (Alphabet Inc.), Samsung

Electronics, Fitbit (by Google), Garmin Ltd., Philips Healthcare, Medtronic,

and Others.

Global

Mobile Health (mHealth) Market Recent Developments News:

- In June 2024, H.I.G. Growth Partners, H.I.G.

Capital's specialist growth capital investment unit, is delighted to

announce the acquisition of Mobile Health Consumer, Inc. ("Mobile

Health" or the "Company"), a digital health, wellbeing, and

virtual care software as a service ("SaaS") platform. Mobile

Health is dedicated to lowering healthcare spend for employers and

boosting staff engagement, resulting in better health outcomes.

- In June 2024, Ryde Group Ltd, the preeminent

mobility and quick commerce technology platform, made an announcement of a partnership with Mobile-health Network

Solutions, Asia Pacific's very first US-listed

telehealth provider. Ryde and MaNaDr entered into a definitive partnership

deal to expand collaboration in the quick commerce and telehealth space.

The

Global Mobile Health (mHealth) Market is dominated by a few large companies,

such as

●

Apple Inc.

●

Google (Alphabet Inc.)

●

Samsung Electronics

●

Fitbit (by Google)

●

Garmin Ltd.

●

Philips Healthcare

●

Medtronic

●

Dexcom Inc.

●

Omron Healthcare

●

Teladoc Health

●

MyFitnessPal (Under

Armour)

●

Ada Health

●

Babylon Health

●

HealthTap

●

WellDoc Inc.

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Mobile Health (mHealth) Market Introduction and Market Overview

- Objectives of the Study

- Global Mobile Health (mHealth) Market Scope and Market Estimation

- Global Mobile Health (mHealth) Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2035)

- Global Mobile Health (mHealth) Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2035

- Market Segmentation

- Product Type of Global Mobile Health (mHealth) Market

- Platform of Global Mobile Health (mHealth) Market

- Application of Global Mobile Health (mHealth) Market

- End-user of Global Mobile Health (mHealth) Market

- Region of Global Mobile Health (mHealth) Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2035

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Mobile Health (mHealth) Market

- Impact of AI in (mHealth) Market

- Key Product/Brand Analysis

- Porter’s Five Forces Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of Substitutes

- Threat of New Entrants

- Competitive Rivalry

- PEST Analysis

- Political Factors

- Economic Factors

- Social Factors

- Product Type Factors

- Key Regulation

- Global Mobile Health (mHealth) Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Mobile Health (mHealth) Market Estimates & Forecast Trend Analysis, by Product Type

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- mHealth Apps

- Fitness & Wellness Apps

- Disease Management Apps

- Women's Health Apps

- Medication Management Apps

- Mental Health Apps

- Wearable Devices

- mHealth Services

- Remote Monitoring

- Diagnostic Services

- Consultation Services

- Healthcare Call Centers

- mHealth Apps

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2035

- Global Mobile Health (mHealth) Market Estimates & Forecast Trend Analysis, by Platform

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Platform, 2021 - 2035

- Android

- iOS

- Others

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Platform, 2021 - 2035

- Global Mobile Health (mHealth) Market Estimates & Forecast Trend Analysis, by Application

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2035

- Chronic Disease Management

- General Health and Wellness

- Remote Patient Monitoring

- Clinical Decision Support

- Diagnostics and Treatment

- Preventive Healthcare

- Mental Health Support

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2035

- Global Mobile Health (mHealth) Market Estimates & Forecast Trend Analysis, by End-user

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Patients/Consumers

- Healthcare Providers

- Payers (Insurance companies)

- Pharmaceutical Companies

- Government/Public Health Agencies

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2035

- Global Mobile Health (mHealth) Market Estimates & Forecast Trend Analysis, by region

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2035

- North America

- Eastern Europe

- Western Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Mobile Health (mHealth) Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2035

- North America Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- North America Mobile Health (mHealth) Market Assessments & Key Findings

- North America Mobile Health (mHealth) Market Introduction

- North America Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- Mexico

- North America Mobile Health (mHealth) Market Assessments & Key Findings

- Western Europe Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- Western Europe Mobile Health (mHealth) Market Assessments & Key Findings

- Western Europe Mobile Health (mHealth) Market Introduction

- Western Europe Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Benelux

- Nordics

- Rest of W. Europe

- Western Europe Mobile Health (mHealth) Market Assessments & Key Findings

- Eastern Europe Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- Eastern Europe Mobile Health (mHealth) Market Assessments & Key Findings

- Eastern Europe Mobile Health (mHealth) Market Introduction

- Eastern Europe Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- Russia

- Hungary

- Poland

- Balkan & Baltics

- Rest of E. Europe

- Eastern Europe Mobile Health (mHealth) Market Assessments & Key Findings

- Asia Pacific Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Mobile Health (mHealth) Market Introduction

- Asia Pacific Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Mobile Health (mHealth) Market Introduction

- Middle East & Africa Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- UAE

- Saudi Arabia

- Turkey

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Mobile Health (mHealth) Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Mobile Health (mHealth) Market Introduction

- Latin America Mobile Health (mHealth) Market Size Estimates and Forecast (US$ Billion) (2021 - 2035)

- By Product Type

- By Platform

- By Application

- By End-user

- By Country

- Brazil

- Argentina

- Colombia

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Mobile Health (mHealth) Market Product Mapping

- Global Mobile Health (mHealth) Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Mobile Health (mHealth) Market Tier Structure Analysis

- Global Mobile Health (mHealth) Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Apple Inc.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Apple Inc.

* Similar details would be provided for all the players mentioned below

- 3M Health Information Systems

- Google (Alphabet Inc.)

- Samsung Electronics

- Fitbit (by Google)

- Garmin Ltd.

- Philips Healthcare

- Medtronic

- Dexcom Inc.

- Omron Healthcare

- Teladoc Health

- MyFitnessPal (Under Armour)

- Ada Health

- Babylon Health

- HealthTap

- WellDoc Inc.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables