Motor Monitoring Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Offerings (Software, Hardware), By Process (On-premise, Cloud), By Deployment (Portable, Online), By End-use (Oil & Gas, Automotive & Transportation, Power Generation, Metals & Mining, Aerospace & Defense, Others), and Geography

2025-12-23

ICT

Ekta Chaurasia (Team Lead)

Description

Motor

Monitoring Market Overview

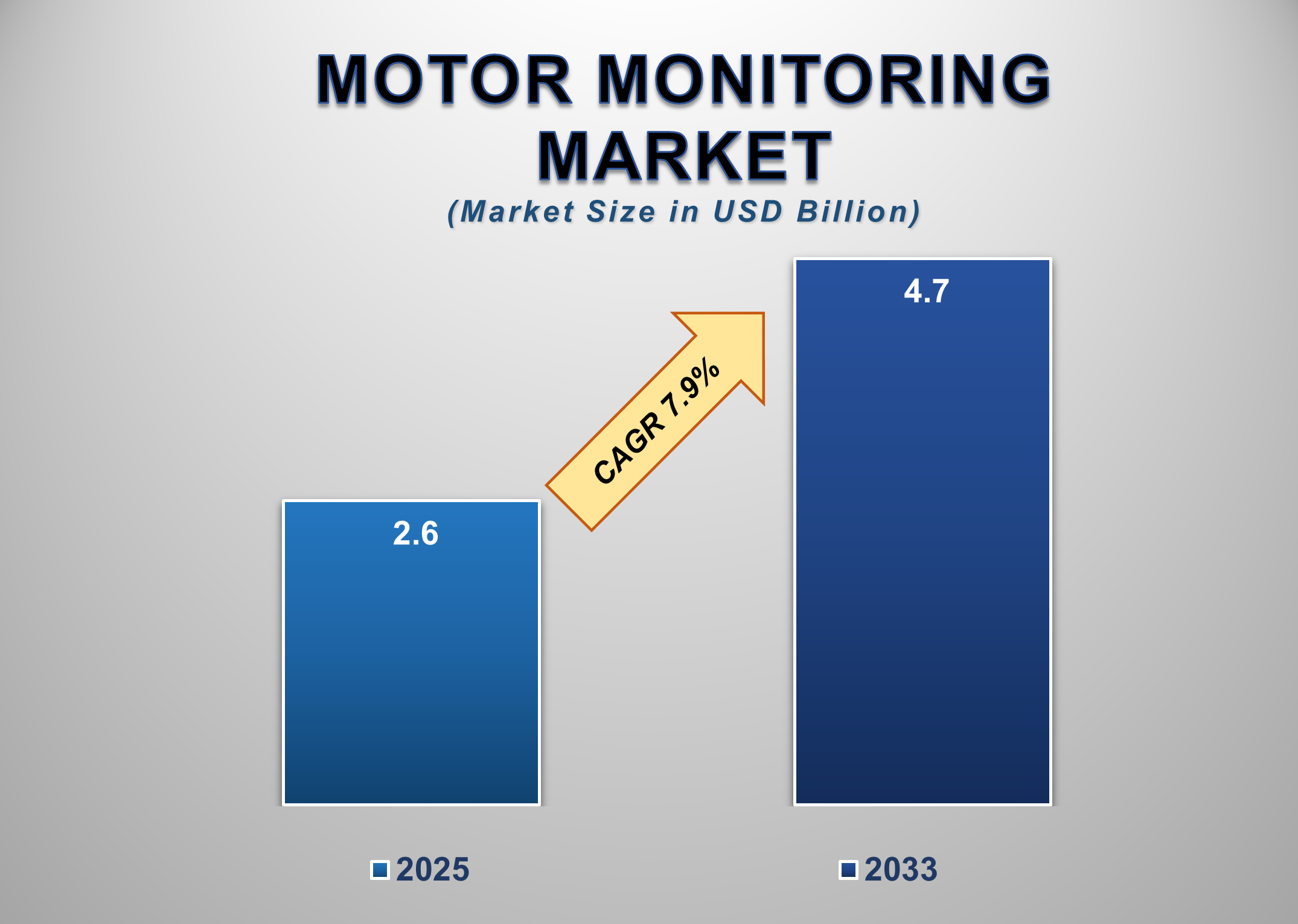

The Motor Monitoring Market is experiencing robust growth globally as industries intensify their focus on asset reliability, operational efficiency, and predictive maintenance. Estimated at USD 2.6 billion in 2025, the market is projected to reach USD 4.7 billion by 2033, registering a strong CAGR of 7.9%. Motor monitoring solutions, including condition monitoring hardware, diagnostic software, vibration analysis, temperature measurement, and advanced predictive analytics, play a vital role in preventing unexpected motor failures, reducing downtime, and optimizing maintenance costs across industrial sectors. Increasing automation, rising demand for uninterrupted operations, and the shift toward Industry 4.0 frameworks have made continuous equipment health assessment indispensable.

The market is being driven by

rapid technological enhancements such as IoT-enabled sensors, cloud-based

analytics, edge computing, and AI-driven failure prediction models. The growing

incidence of motor breakdowns and high replacement costs is pushing organizations

to adopt comprehensive monitoring strategies rather than traditional reactive

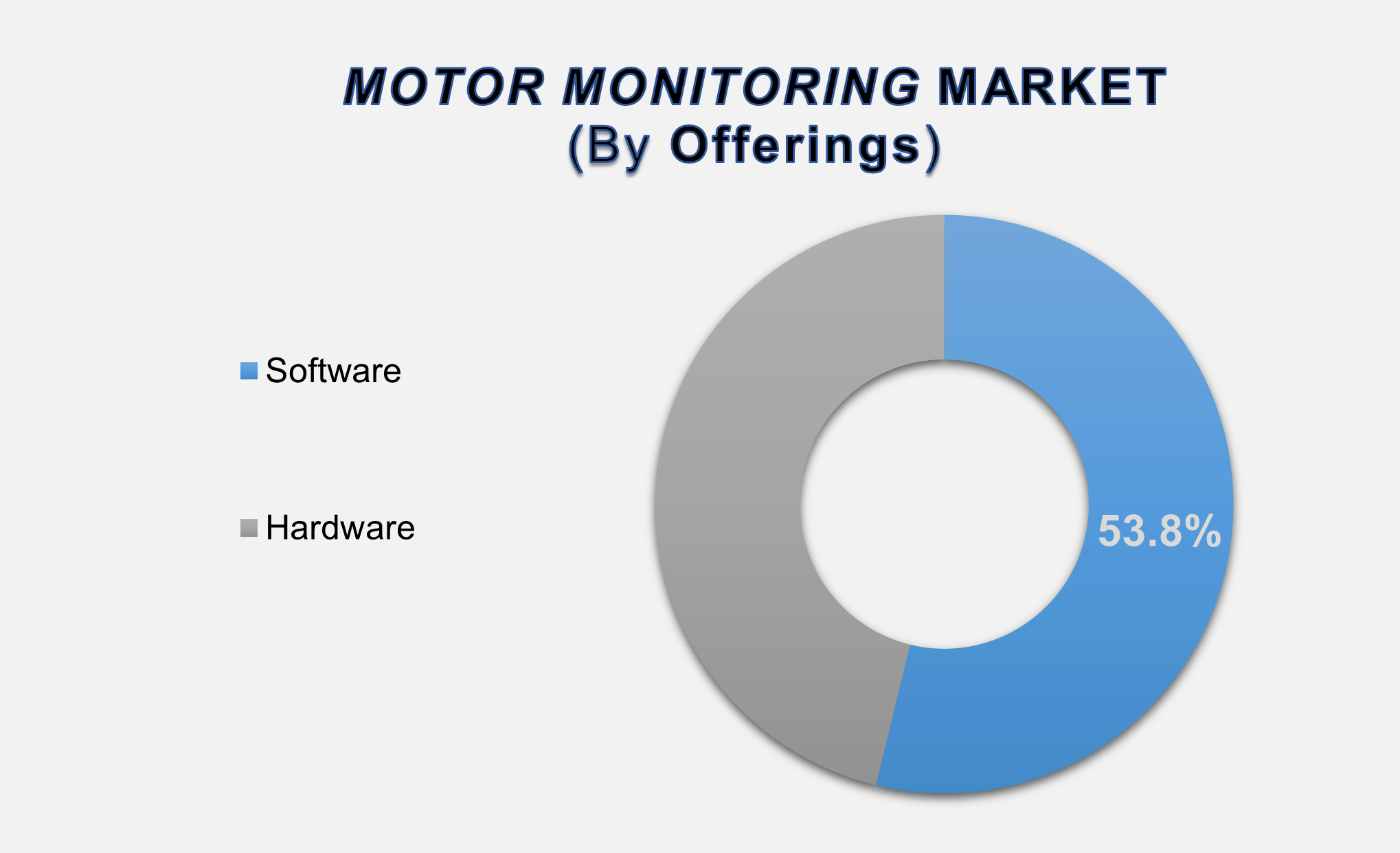

maintenance systems. Software leads the market with a 53.8% share, attributed

to intelligent diagnostics, real-time monitoring, and integration with

enterprise asset management systems.

Motor Monitoring Market Drivers and Opportunities

Growing Emphasis on

Predictive Maintenance and Equipment Reliability Is Driving Market Growth

Predictive maintenance has become

a central strategy for industries seeking to avoid unplanned shutdowns and

maximize equipment availability. Motors are among the most critical components

in the manufacturing, oil & gas, utilities, mining, and transportation

industries. Their failure can halt entire production processes, leading to

significant economic losses. Motor monitoring enables continuous surveillance

of health parameters such as vibration, current, voltage, temperature, and

insulation condition, facilitating early detection of anomalies. This

capability significantly reduces maintenance costs and extends equipment

lifespan, making it a crucial driver for the market.

Advancements in data analytics,

wireless communication, and AI algorithms have transformed motor monitoring

from basic condition checks to highly accurate predictive intelligence systems.

Software platforms now provide real-time insights, automated alerts, root-cause

diagnoses, and actionable recommendations. These capabilities help maintenance

teams transition from reactive or time-based servicing to predictive

maintenance cycles that optimize resources and prevent unexpected breakdowns.

Industries are also under pressure to increase uptime while reducing

operational risk, particularly in energy-intensive sectors like oil & gas

and power generation. Rising labor shortages further amplify the need for

automated monitoring systems that reduce manual inspections. As organizations

embrace digital transformation, the integration of motor monitoring with SCADA,

DCS, and cloud-based asset management systems continues to accelerate adoption

across global industries.

Industrial Automation and

Industry 4.0 Adoption Are Fueling Motor Monitoring Deployment Worldwide

The global push toward

automation, smart factories, and connected industrial ecosystems is

significantly boosting the adoption of motor monitoring solutions. Industry 4.0

technologies, such as IoT sensors, edge computing, machine learning, and

cyber-physical systems, enable continuous collection and interpretation of

motor performance data. These advancements allow facilities to create

interconnected networks of assets capable of self-diagnosing and communicating

operational status in real time. Manufacturing industries are increasingly

integrating motor monitoring into automated production lines to ensure higher

efficiency, precision, and reliability. Automated plants in the automotive,

semiconductor, packaging, and food processing sectors rely on complex

motor-driven machinery, making monitoring essential for uninterrupted

production. The rise of wireless solutions and compact sensors is enabling

easier retrofitting of legacy motors, allowing older facilities to participate

in digital transformation without complete system overhauls.

The

energy transition marked by increasing investments in renewable energy

generation, electrification, and modernization of power grids is also driving

motor monitoring adoption. Utilities depend on continuous motor operation for

pumps, compressors, fans, and turbines, making predictive insights invaluable.

As global industries prioritize operational excellence, safety, and

sustainability, motor monitoring is becoming a critical pillar of intelligent

industrial infrastructure.

Expanding Industrial Base

in Emerging Economies Is Creating Significant Global Opportunities

Emerging economies across

Asia-Pacific, Latin America, the Middle East, and Eastern Europe are rapidly

industrializing, presenting substantial growth opportunities for motor

monitoring providers. Countries such as India, China, Vietnam, Indonesia,

Brazil, and Mexico are seeing increasing investments in manufacturing, oil

& gas infrastructure, mining operations, and power generation. These

sectors extensively rely on motors to support production, pumping, and material

handling tasks, making monitoring indispensable for reliability and cost

optimization.

As factories modernize and adopt

automated production lines, the demand for predictive and condition monitoring

systems rises. Government-driven initiatives promoting industrial growth, such

as “Make in India,” China’s manufacturing upgrades, and Southeast Asia’s

export-led production expansion, are accelerating the deployment of motor

monitoring systems. The growing number of industrial parks, refineries,

chemical plants, and logistics centers further elevates potential demand.

Budget constraints often encourage industries in emerging markets to adopt

preventive strategies instead of costly equipment replacements, positioning

motor monitoring as a practical solution. Increasing availability of

cost-effective portable devices, cloud-based analytics, and subscription-based

software models is expected to further boost adoption. Collectively, these

trends create substantial long-term expansion opportunities for global and

regional motor monitoring solution providers.

Motor Monitoring Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.6 Billion |

|

Market Forecast in 2033 |

USD 4.7 Billion |

|

CAGR % 2025-2033 |

7.9% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Offerings, By

Process, By Deployment, By End-use |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Motor Monitoring Market

Report Segmentation Analysis

The global Motor Monitoring

Market industry analysis is segmented by Offerings, by Process, by Deployment,

by End-use, and by Region.

Software Segment

Accounted for the Largest Market Share in the Global Motor Monitoring Market

The software segment, contributing 53.8% of the global market, leads due to the increasing shift toward digital diagnostics, predictive maintenance analytics, and cloud-based monitoring platforms. Modern motor monitoring software integrates advanced algorithms capable of detecting anomalies, forecasting failures, analyzing trends, and generating automated maintenance alerts. This enables industries to transition from reactive or periodic maintenance models to predictive frameworks that significantly reduce downtime and operational costs. Software platforms also provide remote access capabilities, allowing engineers to monitor assets across multiple facilities from centralized dashboards. Compatibility with IoT sensors, enterprise asset management (EAM) systems, and SCADA interfaces further enhances software adoption. AI-driven insights, machine learning pattern recognition, and cloud-enabled data storage are making software-based monitoring essential for large-scale industrial operations. As industrial plants increasingly adopt digital transformation strategies and prioritize equipment reliability, the software segment will continue to dominate market share throughout the forecast period.

On-premise Segment Held

the Largest Share in the Global Motor Monitoring Market

The on-premise process segment

remains the preferred deployment mode across global industries, especially in

sectors with strict security, data privacy, and operational control

requirements. Industries such as oil & gas, power generation, aerospace &

defense, and heavy manufacturing rely heavily on sensitive operational data,

making locally hosted monitoring systems a trusted choice. On-premise solutions

offer real-time diagnostics without reliance on external networks, ensuring

performance stability and eliminating potential cybersecurity concerns

associated with cloud environments. Additionally, legacy industrial facilities

with existing wired infrastructure often find on-premise integration easier and

more cost-effective. These systems provide consistent performance for vibration

analysis, thermal diagnostics, and electrical monitoring while maintaining

compatibility with existing control room architectures. Although cloud-based

solutions are growing rapidly, the robustness, reliability, and data sovereignty

advantages of on-premise systems ensure continued dominance in large-scale

industrial applications.

Portable Segment

Accounted for the Largest Share in the Global Motor Monitoring Market

The portable deployment segment

leads the market due to its versatility, cost-efficiency, and extensive use in

periodic inspection routines across industries. Portable motor monitoring

devices such as handheld vibration analyzers, thermal imagers, data collectors,

and current analyzers allow maintenance teams to assess motor health across

multiple assets without requiring continuous installation. This makes portable

tools highly valuable in facilities with a wide range of motors operating in

different environments, such as manufacturing, mining, oil & gas, and

utilities.

Portable systems are especially

favored by small and mid-sized industries that require diagnostic capabilities

but lack resources for full-scale permanent monitoring infrastructure.

Technological advancements, including wireless communication, improved sensor

accuracy, and compatibility with cloud-based software, enhance the

effectiveness of portable solutions. Their flexibility, ease of use, and

suitability for varied industrial settings ensure they remain a dominant

deployment mode through the forecast period.

The following segments are

part of an in-depth analysis of the global Motor Monitoring Market:

|

Market

Segments |

|

|

by Offerings |

●

Software ●

Hardware |

|

by Process |

●

On-premise ●

Cloud |

|

by Deployment |

●

Portable ●

Online |

|

by End-use |

●

Oil and Gas ●

Automotive &

Transportation ●

Power Generation ●

Metals and Mining ●

Aerospace and

Defense ●

Others |

Motor Monitoring Market Share Analysis by Region

The North America region

is projected to hold the largest share of the global Motor Monitoring market

over the forecast period.

North America holds the largest

share in the global Motor Monitoring Market, accounting for 43.1% of total

revenue. The region’s strong industrial base, spanning oil & gas

operations, advanced manufacturing, power generation, and aerospace, drives high

adoption of monitoring solutions. Early implementation of predictive

maintenance strategies, strong regulatory standards for equipment safety, and

widespread use of automation technologies further contribute to market

leadership.

The presence of major technology

providers, advanced R&D ecosystems, and rapid adoption of AI- and

IoT-enabled solutions also support North America’s dominance. Frequent upgrades

to industrial infrastructure and high awareness of downtime-related costs

accelerate demand for sophisticated monitoring systems. Asia-Pacific is

expected to witness the highest CAGR, supported by rapid industrialization,

growing energy demand, large-scale manufacturing expansion, and increasing

emphasis on operational efficiency. Countries such as China, India, Japan, and

South Korea are heavily investing in smart factories, modern equipment

maintenance programs, and digital asset management systems.

Motor Monitoring Market

Competition Landscape Analysis

The Motor

Monitoring Market is moderately fragmented, with global technology leaders

competing alongside smaller specialized providers. Companies focus on expanding

their product portfolios with AI-driven predictive systems, cloud-integrated

platforms, and advanced sensor technologies. Strategic partnerships with

industrial automation providers, service companies, and OEMs are common as

vendors aim to deliver holistic monitoring solutions. Continuous R&D

investment, geographic expansion, and integration of cybersecurity capabilities

remain key competitive strategies.

Global Motor Monitoring Market Recent

Developments News:

- In October 2024, Siemens

introduced an innovative motor management system for industrial

switchboards, designed to enhance motor control, protection, and

operational efficiency in demanding industrial environments.

- In August 2024, ABB

strengthened its global environmental solutions portfolio with the

acquisition of FODISCH Group, a leader in continuous emission monitoring

systems. This strategic move enhances ABB’s ability to support industrial

clients in meeting regulatory requirements and sustainability goals.

The Global Motor Monitoring Market is dominated

by a few large companies, such as

●

General Electric

●

Siemens

●

ABB

●

Honeywell

●

Emerson Electric

●

Schneider Electric

●

Rockwell Automation

●

Banner Engineering

●

National Instruments

●

Parker Hannifin

●

Megger

●

Fluke Corporation

●

Acoem

●

Bruel & Kjaer

●

SKF

●

ifm electronic

●

Azima DLI

●

Dynapar

●

Petasense

●

Sensonics

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Motor Monitoring

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Motor Monitoring Market Scope and Market Estimation

1.2.1.Global Motor Monitoring

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Motor Monitoring

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Offerings of Global Motor

Monitoring Market

1.3.2.Process of Global Motor

Monitoring Market

1.3.3.Deployment of Global Motor

Monitoring Market

1.3.4.End-use of Global Motor

Monitoring Market

1.3.5.Region of Global Motor

Monitoring Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Motor Monitoring Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Motor Monitoring Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Motor Monitoring

Market Estimates & Forecast Trend

Analysis, by Offerings

4.1.

Global

Motor Monitoring Market Revenue (US$ Bn) Estimates and Forecasts, by Offerings,

2020 - 2033

4.1.1.Software

4.1.2.Hardware

5.

Global Motor Monitoring

Market Estimates & Forecast Trend

Analysis, by Process

5.1.

Global

Motor Monitoring Market Revenue (US$ Bn) Estimates and Forecasts, by Process, 2020

- 2033

5.1.1.On-premise

5.1.2.Cloud

6.

Global Motor Monitoring

Market Estimates & Forecast Trend

Analysis, by Deployment

6.1.

Global

Motor Monitoring Market Revenue (US$ Bn) Estimates and Forecasts, by Deployment,

2020 - 2033

6.1.1.Portable

6.1.2.Online

7.

Global Motor Monitoring

Market Estimates & Forecast Trend

Analysis, by End-use

7.1.

Global

Motor Monitoring Market Revenue (US$ Bn) Estimates and Forecasts, by End-use, 2020

- 2033

7.1.1.Oil and Gas

7.1.2.Automotive &

Transportation

7.1.3.Power Generation

7.1.4.Metals and Mining

7.1.5.Aerospace and Defense

7.1.6.Others

8. Global

Motor Monitoring Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Motor Monitoring Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

9. North America Motor

Monitoring Market: Estimates &

Forecast Trend Analysis

9.1.

North

America Motor Monitoring Market Assessments & Key Findings

9.1.1.North America Motor

Monitoring Market Introduction

9.1.2.North America Motor

Monitoring Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Offerings

9.1.2.2. By Process

9.1.2.3. By Deployment

9.1.2.4. By End-use

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Motor

Monitoring Market: Estimates &

Forecast Trend Analysis

10.1.

Europe

Motor Monitoring Market Assessments & Key Findings

10.1.1.

Europe

Motor Monitoring Market Introduction

10.1.2.

Europe

Motor Monitoring Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Offerings

10.1.2.2. By Process

10.1.2.3. By Deployment

10.1.2.4. By End-use

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Motor

Monitoring Market: Estimates &

Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Motor Monitoring Market Introduction

11.1.2.

Asia

Pacific Motor Monitoring Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1. By Offerings

11.1.2.2. By Process

11.1.2.3. By Deployment

11.1.2.4. By End-use

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Motor

Monitoring Market: Estimates &

Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Motor Monitoring Market Introduction

12.1.2.

Middle East & Africa Motor Monitoring Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Offerings

12.1.2.2. By Process

12.1.2.3. By Deployment

12.1.2.4. By End-use

12.1.2.5.

By

Country

12.1.2.5.1. South

Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi

Arabia

12.1.2.5.4. Rest

of MEA

13. Latin America

Motor Monitoring Market: Estimates

& Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Motor Monitoring Market Introduction

13.1.2.

Latin

America Motor Monitoring Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

13.1.2.1. By Offerings

13.1.2.2. By Process

13.1.2.3. By Deployment

13.1.2.4. By End-use

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Motor Monitoring Market Product Mapping

15.2.

Global

Motor Monitoring Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

15.3.

Global

Motor Monitoring Market Tier Structure Analysis

15.4.

Global

Motor Monitoring Market Concentration & Company Market Shares (%) Analysis,

2024

16.

Company

Profiles

16.1. General

Electric

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2. Siemens

16.3. ABB

16.4. Honeywell

16.5. Emerson

Electric

16.6. Schneider

Electric

16.7. Rockwell

Automation

16.8. Banner

Engineering

16.9. National

Instruments

16.10. Parker

Hannifin

16.11. Megger

16.12. Fluke

Corporation

16.13. Acoem

16.14. Bruel &

Kjaer

16.15. SKF

16.16. ifm

electronic

16.17. Azima DLI

16.18. Dynapar

16.19. Petasense

16.20. Sensonics

16.21. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables