Non-stick Cookware Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Material Type (Teflon Coated, Anodized Aluminum Coated, Ceramic Coated, Enameled Iron Coated, Others), By End-use (Residential, Commercial), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-commerce Stores, Others), and Geography

2026-01-02

Consumer Products

Jaya Bundele (Research Analyst)

Description

Non-stick Cookware Market Overview

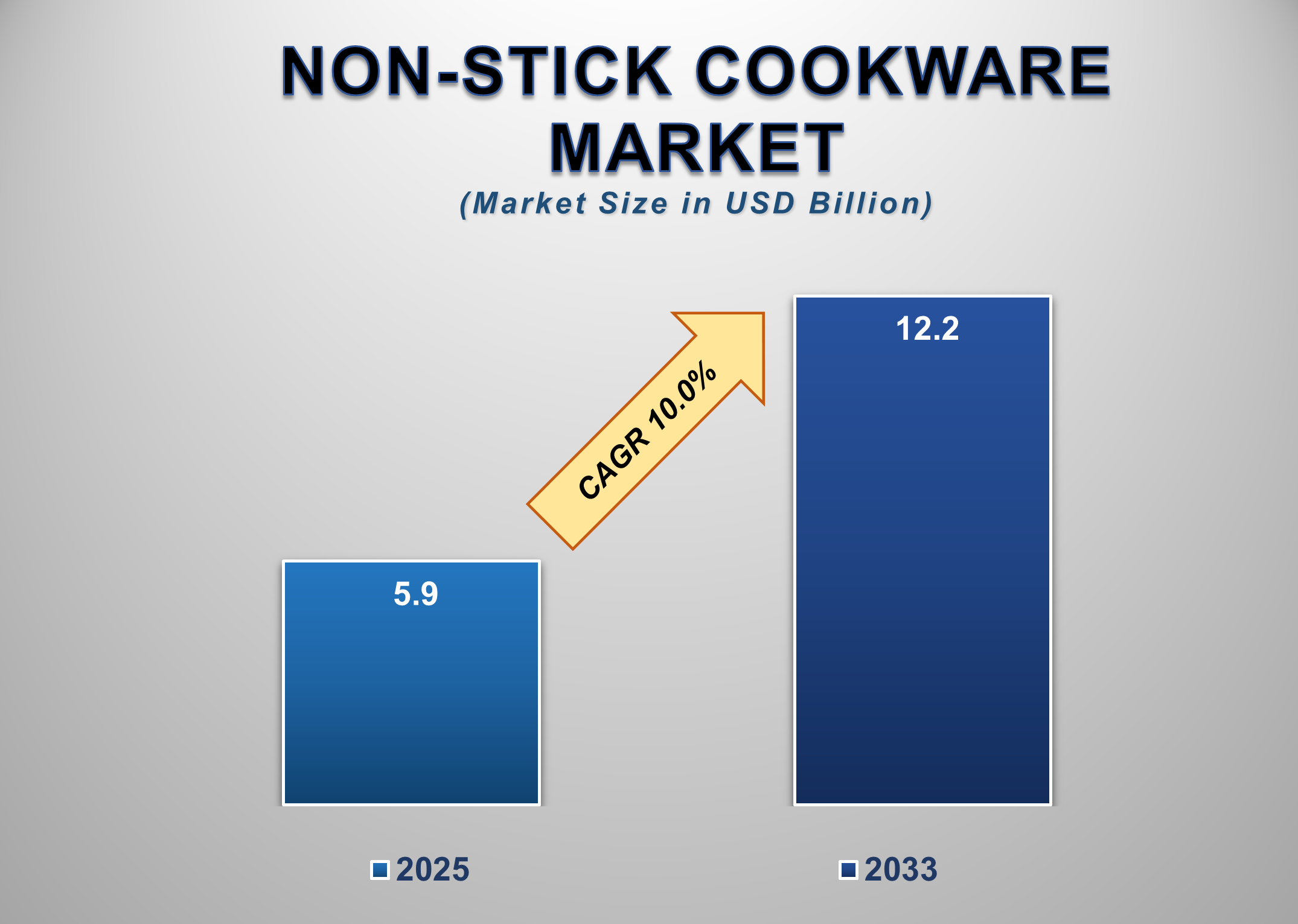

The Global Non-stick Cookware Market is projected to expand from USD 5.9 billion in 2025 to USD 12.2 billion by 2033, registering a robust CAGR of 10.0%. The market's growth is driven by rising consumer preference for convenient, easy-to-clean cookware and a shift toward healthier, low-oil cooking practices. Non-stick surfaces ranging from conventional PTFE (Teflon) to ceramic, anodized aluminum, and hybrid formulations continue to gain traction due to their ability to reduce cooking time, prevent food adhesion, and improve the overall cooking experience. Increasing household formation, expanding urban middle-class populations, and greater emphasis on kitchen aesthetics are further boosting product adoption across residential kitchens.

In addition, the market benefits

from a flourishing e-commerce ecosystem, enabling brands to expand visibility

and offer bundled cookware sets at competitive prices. Manufacturers are also

investing in advanced coatings that enhance durability, scratch resistance, and

heat distribution, addressing past concerns related to surface degradation and

chemical safety.

Non-stick Cookware Market Drivers and Opportunities Rising Demand for Convenient, Low-Oil Cooking Solutions Is Driving Global Market Growth

Growing health consciousness remains a pivotal factor accelerating

demand for non-stick cookware worldwide. Consumers today are actively reducing

oil consumption, supporting cookware surfaces that require minimal or no

cooking fats. Traditional stainless-steel cookware is less preferred for daily

frying or sautéing due to sticking issues, which non-stick materials

effectively overcome. This preference aligns with the surge in lifestyle

diseases, such as obesity and high cholesterol, prompting consumers to shift to

healthier cooking habits. The convenience offered by non-stick surfaces also

boosts adoption as they reduce cooking time, simplify cleaning, and minimize

food residue buildup. These benefits make such cookware particularly attractive

to working professionals and nuclear families seeking fast meal preparation.

Additionally, innovations in coating technology such as long-lasting ceramic

finishes, titanium reinforcement, and multi-layer PTFE further boost market

attractiveness by improving durability and heat retention. The integration of

non-stick surfaces into bakeware, induction cookware, and multifunctional

products broadens consumer applicability. Retail expansion, attractive pricing,

and easy access through e-commerce platforms amplify availability across

geographies. The increasing trend of home cooking and kitchen décor

modernization also influences consumers to upgrade to premium cookware sets,

thereby strengthening global demand.

Expansion of Residential Kitchens and Home Cooking Culture Is

Fueling Market Adoption

A significant shift in global culinary behavior marked by the

growing popularity of home cooking, food experimentation, and modern kitchen

aesthetics continues to propel the non-stick cookware market forward. The

COVID-era transformation in cooking habits persists, with consumers

increasingly investing in high-performance cookware that enhances cooking

results and aligns with contemporary kitchen designs. Rising residential

construction, increased modular kitchen installation, and growing household

disposable incomes further encourage the adoption of premium cookware

sets.Social media and digital food influencers have also played a

transformative role by popularizing home cooking trends, driving consumers

toward cookware that ensures professional-like results. The rise in multi-piece

cookware sets, color-coordinated kitchenware, and ergonomic designs aligns with

consumer demand for functionality paired with style. Residential users prefer

non-stick cookware for its versatility, enabling easy preparation of diverse

cuisines from Asian stir-fries to Western breakfasts without requiring

specialized skills.

Manufacturers are capitalizing on this trend by offering visually

appealing, scratch-resistant ceramic-coated pans, induction-ready cookware, and

lightweight aluminum products for everyday cooking. As a result, the

residential segment remains the largest end-use category and a core contributor

to sustained market expansion through 2033.

Growing Shift Toward Eco-friendly and Non-toxic Coating

Technologies Is Creating Significant Opportunities

Increasing consumer awareness about chemical safety in cookware

has created substantial growth opportunities for eco-friendly, non-toxic, and

PFAS-free non-stick solutions. Traditional PTFE-based Teflon coatings have

faced scrutiny due to concerns over overheating and chemical release, prompting

buyers to explore safer alternatives. Ceramic coatings, water-based sol-gel

technologies, and diamond- or titanium-reinforced non-stick surfaces are

rapidly gaining traction as viable, sustainable options.

Manufacturers now emphasize durability, scratch resistance,

metal-utensil tolerance, and high-temperature stability, features previously

considered limitations of non-toxic coatings. This shift aligns strongly with

environmental regulations and growing preference for recyclable and ethically

sourced materials. Additionally, consumer demand for premium cookware in

eco-conscious markets, particularly Europe and North America, opens avenues for

product differentiation and brand expansion. Companies focusing on sustainable

packaging, minimal-emission production processes, and recyclable base materials

such as anodized aluminum and enameled iron are gaining a competitive edge. As

PFAS restrictions tighten globally, brands offering certified toxic-free, safe

alternatives stand to capture significant market share. This trend defines a

major long-term opportunity that will reshape product innovation across the

nonstick cookware industry.

Non-stick Cookware Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 5.9 Billion |

|

Market Forecast in 2033 |

USD 12.2 Billion |

|

CAGR % 2025-2033 |

10.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Material Type,

By End-use, By Distribution Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Non-stick Cookware Market

Report Segmentation Analysis

The Global Non-stick Cookware

Market is segmented by Material Type, End-use, Distribution Channel, and

Geography.

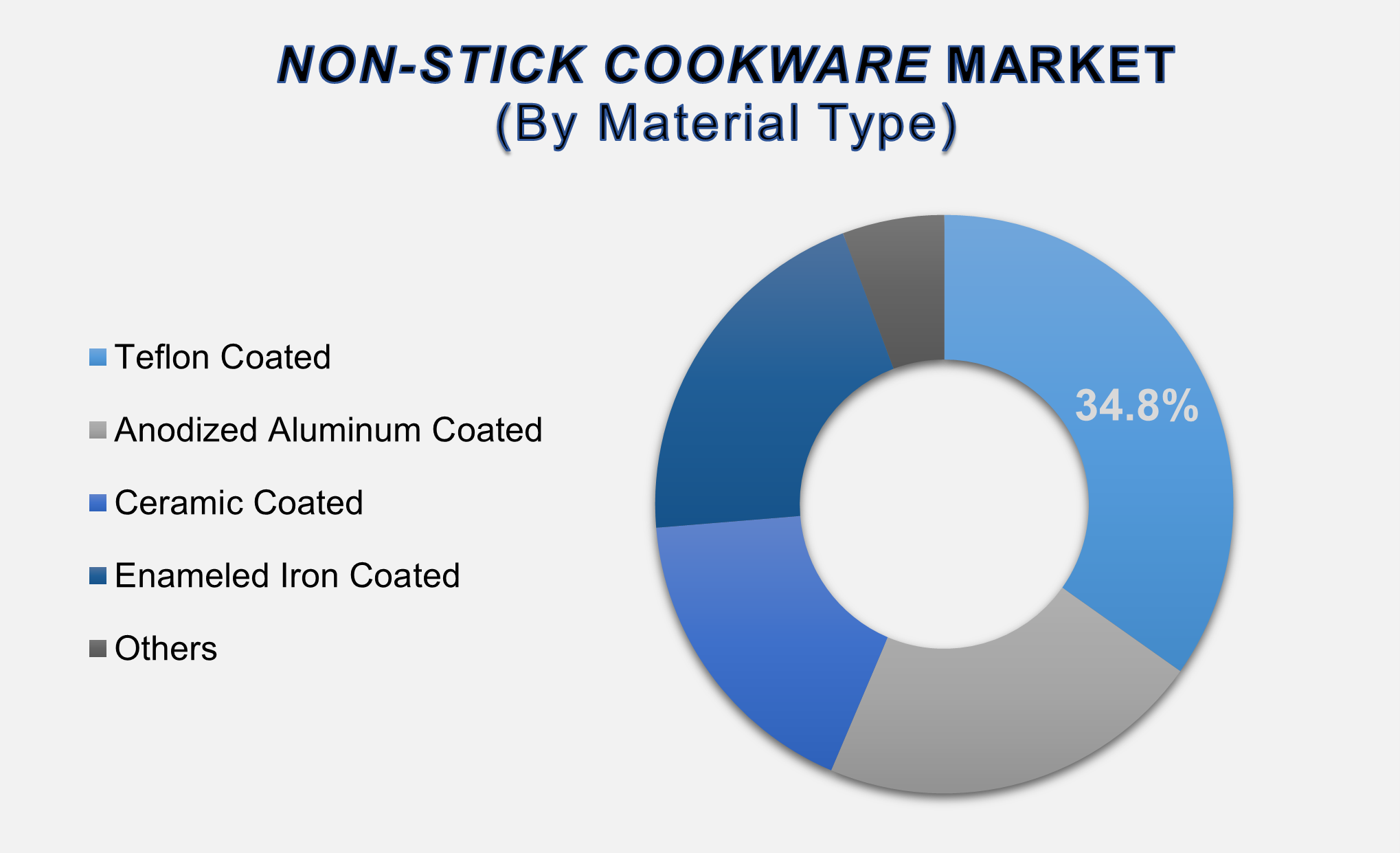

The Teflon-coated segment

accounted for the largest market share in the global Non-stick Cookware market.

This dominance is driven by the wide availability, cost-effectiveness, and strong non-stick performance offered by PTFE-based (Teflon) coatings. These products are highly preferred for everyday cooking due to their smooth surface, heat efficiency, and compatibility with a variety of stovetops. Manufacturers continue to invest in multi-layer reinforced PTFE coatings that enhance durability and scratch resistance while maintaining affordability for mass-market consumers. Although ceramic and anodized aluminum alternatives are gaining attention for their eco-friendly appeal, Teflon-coated cookware remains the most accessible option, particularly in developing regions where price sensitivity is high. The segment also benefits from strong retail penetration in supermarkets, hypermarkets, and online platforms. With ongoing innovations aimed at improving temperature resistance and extending product lifespan, Teflon-coated cookware is expected to maintain a considerable share throughout the forecast period.

The residential segment

accounted for the largest market share in the global Non-stick Cookware market.

Residential

consumers represent the core demand base, driven by rising household formation,

urbanization, and the popularity of home cooking. Non-stick cookware is

preferred in homes due to its convenience, low maintenance, and suitability for

daily meal preparation across diverse cuisines. Additionally, increasing

adoption of modular kitchens encourages consumers to invest in premium cookware

sets that complement modern interior aesthetics. E-commerce expansion has

further boosted product accessibility, enabling consumers to explore a wide

assortment of designs, colors, and material options. Residential demand is also

fueled by rising health awareness, with users opting for cookware that requires

minimal oil while ensuring superior heat distribution. Continuous product

innovation, such as ceramic-coated pans and

induction-compatible materials, further

enhances adoption. The shift toward healthier and more efficient cooking

practices ensures that the residential segment remains the primary growth

driver through 2033.

The Supermarkets &

Hypermarkets segment accounted for the largest market share in the global

Non-stick Cookware market.

These

retail formats offer consumers the advantage of physically evaluating cookware

quality, weight, coating texture, and brand comparisons before purchase,

an important factor for cookware selection.

Attractive pricing, seasonal promotions, and bundled deals further support

strong sales of non-stick pans, pots, and cookware sets through offline retail.

Major brands maintain a strong presence in supermarkets and hypermarkets due to

consistent footfall and broad visibility. These stores often feature dedicated

kitchenware aisles and curated product displays, which appeal to both

first-time buyers and repeat customers. Despite the rapid rise of e-commerce,

offline retail remains dominant in many regions, particularly in emerging

markets where consumers prefer hands-on product assessment. The continued

expansion of large-format retail chains across Asia, the Middle East, and

Europe is expected to sustain growth in this segment.

The following segments are

part of an in-depth analysis of the global Non-stick Cookware market:

|

Market Segments |

|

|

By Material

Type |

●

Teflon Coated ●

Anodized Aluminum

Coated ●

Ceramic Coated ●

Enameled Iron Coated ●

Others |

|

By End-use |

●

Residential ●

Commercial |

|

By

Distribution Channel |

●

Supermarkets &

Hypermarkets ●

Specialty Stores ●

E-commerce Stores ●

Others |

Non-stick Cookware Market

Share Analysis by Region

The North America region

is projected to hold the largest share of the global Non-stick Cookware market

over the forecast period

North

America remains the largest regional market, accounting for 39.3% of the global

non-stick cookware revenue in 2025. High consumer spending on kitchenware,

strong brand presence, and a well-established retail network underpin market

leadership. Consumers in the U.S. and Canada show a strong preference for premium, durable cookware, particularly anodized aluminum and ceramic-coated

products. Well-informed shoppers, coupled with high adoption of modular

kitchens and modern cookware sets, further contribute to regional dominance.

Asia-Pacific,

however, is projected to record the highest CAGR through 2033. Rising

disposable incomes, expanding urban populations, and the rapid growth of

residential construction significantly boost cookware adoption. Increasing

Western culinary influence and the rise of food delivery and cloud kitchens

further amplify market expansion. Countries such as China, India, Japan, and

Indonesia are becoming key manufacturing as well as consumption hubs.

Collectively, APAC's economic progress, coupled with high consumer replacement

cycles, positions it as the fastest-evolving regional market.

Non-stick Cookware Market

Competition Landscape Analysis

The Non-stick Cookware Market is

moderately fragmented, with global brands competing alongside regional

manufacturers offering cost-effective alternatives. Companies focus on advanced

coating technologies, heat-resistant materials, and induction-compatible

designs to enhance product differentiation. Sustainability-driven innovation,

especially PFAS-free coatings, is emerging as a major competitive driver among

premium brands. Strategic partnerships with retailers, influencer-led

marketing, and online channel expansion are key approaches adopted to

strengthen market penetration. Mergers, acquisitions, and product line

diversification remain prevalent as companies seek to broaden their consumer

reach across both developed and emerging markets.

Global Non-stick Cookware

Market Recent Developments News:

- In

November 2022, TTK

Prestige Ltd. launched a new range of hard-anodized non-stick cookware in

India, featuring its ‘DURASTONE’ six-layer coating. The collection

includes frying pans, tawas, casseroles, kadais, and tea pans, designed

for enhanced durability and performance.

- In April 2022,

Meyer Corporation introduced the Meyer Accent collection in the U.S.

market, featuring 16 hard-anodized aluminum non-stick and stainless steel

utensils. The launch expanded Meyer’s portfolio of premium, durable

kitchenware solutions.

The Global Non-stick Cookware Market Is Dominated by a Few Large Companies, such as

●

Tefal

●

Circulon

●

Scanpan

●

All-Clad

●

Calphalon

●

Woll

●

GreenPan

●

Anolon

●

Farberware

●

Cuisinart

●

Rachael Ray

●

Tramontina

●

Berndes

●

Bialetti

●

Meyer Corporation

●

Gibson

●

Nordic Ware

●

KitchenAid

●

Lagostina

●

Maxcook

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Non-stick Cookware

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Non-stick Cookware Market Scope and Market Estimation

1.2.1.Global Non-stick Cookware

Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Non-stick Cookware

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Material Type of Global Non-stick

Cookware Market

1.3.2.End-use of Global Non-stick

Cookware Market

1.3.3.Distribution Channel of

Global Non-stick Cookware Market

1.3.4.Region of Global Non-stick

Cookware Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Non-stick Cookware Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Non-stick Cookware Market Estimates

& Historical Trend Analysis (2020 - 2024)

4.

Global Non-stick Cookware

Market Estimates & Forecast Trend

Analysis, by Material Type

4.1.

Global

Non-stick Cookware Market Revenue (US$ Bn) Estimates and Forecasts, by Material

Type, 2020 - 2033

4.1.1.Teflon Coated

4.1.2.Anodized Aluminum Coated

4.1.3.Ceramic Coated

4.1.4.Enameled Iron Coated

4.1.5.Others

5.

Global Non-stick Cookware

Market Estimates & Forecast Trend

Analysis, by End-use

5.1.

Global

Non-stick Cookware Market Revenue (US$ Bn) Estimates and Forecasts, by End-use,

2020 - 2033

5.1.1.Residential

5.1.2.Commercial

6.

Global Non-stick Cookware

Market Estimates & Forecast Trend

Analysis, by Distribution Channel

6.1.

Global

Non-stick Cookware Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel, 2020 - 2033

6.1.1.Supermarkets &

Hypermarkets

6.1.2.Specialty Stores

6.1.3.E-commerce Stores

6.1.4.Others

7. Global

Non-stick Cookware Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Non-stick Cookware Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

1.1.1.North America

1.1.2.Europe

1.1.3.Asia Pacific

1.1.4.Middle East & Africa

1.1.5.Latin America

8. North America Non-stick

Cookware Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Non-stick Cookware Market Assessments & Key Findings

8.1.1.North America Non-stick

Cookware Market Introduction

8.1.2.North America Non-stick

Cookware Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Material

Type

8.1.2.2. By End-use

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1.

The

U.S.

8.1.2.4.2.

Canada

9. Europe Non-stick

Cookware Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Non-stick Cookware Market Assessments & Key Findings

9.1.1.Europe Non-stick Cookware

Market Introduction

9.1.2.Europe Non-stick Cookware

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Material

Type

9.1.2.2. By End-use

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1. Germany

9.1.2.4.2. Italy

9.1.2.4.3. U.K.

9.1.2.4.4. France

9.1.2.4.5. Spain

9.1.2.4.6. Switzerland

9.1.2.4.7.

Rest of Europe

10. Asia Pacific Non-stick

Cookware Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Non-stick Cookware Market Introduction

10.1.2.

Asia

Pacific Non-stick Cookware Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Material

Type

10.1.2.2. By End-use

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6.

Rest

of Asia Pacific

11. Middle East & Africa Non-stick

Cookware Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Non-stick Cookware Market

Introduction

11.1.2.

Middle East & Africa Non-stick Cookware Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Material

Type

11.1.2.2. By End-use

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. South

Africa

11.1.2.4.2. UAE

11.1.2.4.3. Saudi

Arabia

11.1.2.4.4.

Rest of MEA

12. Latin America

Non-stick Cookware Market: Estimates

& Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Non-stick Cookware Market Introduction

12.1.2.

Latin

America Non-stick Cookware Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Material

Type

12.1.2.2. By End-use

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Mexico

12.1.2.4.3. Argentina

12.1.2.4.4.

Rest of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Non-stick Cookware Market Product Mapping

14.2.

Global

Non-stick Cookware Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Non-stick Cookware Market Tier Structure Analysis

14.4.

Global

Non-stick Cookware Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1. Tefal

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all

the players mentioned below

15.2. Circulon

15.3. Scanpan

15.4. All-Clad

15.5. Calphalon

15.6. Woll

15.7. GreenPan

15.8. Anolon

15.9. Farberware

15.10. Cuisinart

15.11. Rachael Ray

15.12. Tramontina

15.13. Berndes

15.14. Bialetti

15.15. Meyer

Corporation

15.16. Gibson

15.17. Nordic Ware

15.18. KitchenAid

15.19. Lagostina

15.20. Maxcook

15.21. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables