Omega-3 in Animal Feed Market Size and Forecast (2020-2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Source (Fish Oil, Algae Oil, Flaxseed Oil, Others), By Livestock (Aquaculture, Pets, Poultry, Swine, Dairy & Ruminants, Others), And Geography

2025-12-17

Consumer Products

Jaya Bundele (Research Analyst)

Description

Omega-3 in

Animal Feed Market Overview

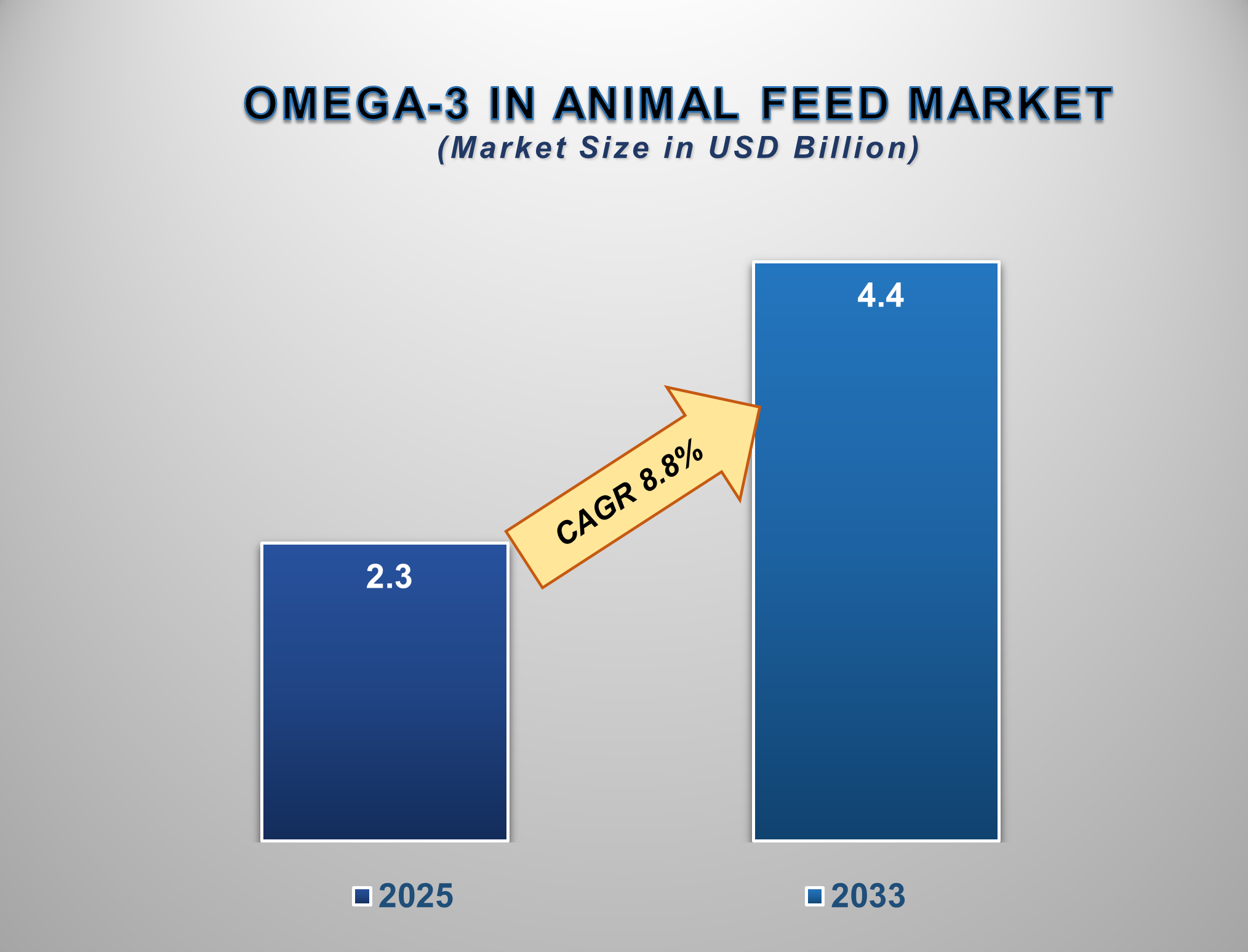

The Omega-3 in Animal Feed Market is poised for significant growth from 2025 to 2033, driven by the rising demand for enriched animal products, heightened awareness of animal health and welfare, and the proven benefits of omega-3s in improving livestock productivity. The market is projected to be valued at approximately USD 2.3 billion in 2025 and is forecasted to reach nearly USD 4.4 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.8% during this period.

Omega-3 fatty acids, primarily EPA

(eicosapentaenoic acid) and DHA (docosahexaenoic acid), are essential

polyunsaturated fats incorporated into animal feed to enhance the nutritional

profile of the end products (meat, milk, and

eggs) and to promote the health, growth, and immunity of the animals

themselves. The market's expansion is primarily fueled by the growing consumer

demand for functional foods, such as omega-3-enriched eggs and meat, which offer human health benefits. In the

rapidly expanding aquaculture sector, omega-3s are a critical component of fish

feed, essential for fish development and health. Furthermore, the pet

humanization trend is driving demand for premium pet foods with functional

ingredients that support skin, coat, joint, and cognitive health.

Sustainability concerns regarding traditional fish oil sources are accelerating

the adoption of alternative sources like algae and genetically modified canola

oil. The Asia-Pacific region holds the largest market share, propelled by its

massive aquaculture industry, while North America and Europe are expected to

see robust growth due to stringent animal welfare standards and high consumer

awareness.

Omega-3 in Animal Feed Market Drivers and

Opportunities

Rising Demand for Enriched Animal Products and Focus on

Livestock Health Are the Primary Market Drivers

The pivotal driver for omega-3 in the

animal feed market is the dual demand for value-added

animal products and enhanced livestock health management. Consumers are

increasingly seeking out functional foods—such as eggs, milk, and meat with

higher levels of omega-3s—due to the associated human health benefits,

including improved cardiovascular and cognitive function. This consumer pull

incentivizes producers to incorporate omega-3s into animal diets to

differentiate their products and command premium prices.

Simultaneously, within the farming industry,

there is a growing focus on improving animal health, welfare, and productivity

through advanced nutrition. Omega-3 fatty acids are proven to confer

significant benefits across livestock: they enhance reproductive performance,

boost immune function, reduce inflammation, and improve overall growth rates.

In aquaculture, they are indispensable for fish larval development, survival,

and fillet quality. For pets, they address specific health concerns like

arthritis, skin allergies, and cognitive decline in aging animals. This

convergence of consumer demand for nutritious food and producer need for

efficient, healthy livestock creates a powerful, sustained demand for omega-3-fortified feed, establishing a foundational growth pillar for the

entire market.

Sustainability Challenges and the Pet Humanization Trend are

Driving Market Evolution

The reliance on fish oil, the traditional source

of omega-3s for aquaculture and animal feed, faces significant sustainability

challenges due to fluctuating wild fish stocks and environmental pressures.

This is catalyzing a major shift towards alternative, sustainable sources.

Algae-derived DHA and EPA oils represent the most promising alternative, as

they are produced at the base of the marine food chain in controlled

fermenters, bypassing the ocean ecosystem entirely. Furthermore, the powerful

"pet humanization" trend, where owners treat pets as family members,

is fueling the demand for premium, health-focused pet food. Pet owners are

actively seeking out products with functional ingredients like omega-3s for

their proven benefits, making the pet segment one of the fastest-growing in the

market.

Innovation in Alternative Sources and Precision Livestock

Farming Presents Significant Opportunities

The need for sustainable and scalable omega-3

sources presents a substantial growth frontier. A key opportunity lies in the

commercialization and cost reduction of novel

sources like algae, krill, and genetically engineered oilseed crops (e.g.,

camelina, canola) that produce EPA and DHA. The integration of omega-3s into

the broader trend of precision livestock farming represents another significant

leap forward. Feed formulations can be tailored to specific animal life stages,

health statuses, and production goals (e.g., enhancing DHA levels in laying

hens for enriched eggs). For ingredient suppliers and feed manufacturers,

investing in R&D for sustainable and cost-effective omega-3 sources,

developing targeted solutions for specific livestock segments, and forming

partnerships with food producers to create branded, enriched products are key

strategies for capturing future market share.

Omega-3 in the Animal Feed Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.3 Billion |

|

Market Forecast in 2033 |

USD 4.4 Billion |

|

CAGR % 2025-2033 |

8.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Source ●

By Livestock |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Omega-3 in Animal Feed Market Report Segmentation

Analysis

The global Omega-3 in Animal Feed

Market industry analysis is segmented by Source, by Livestock, and by region.

Fish Oil Segment to Hold

Dominant Market Share in 2025

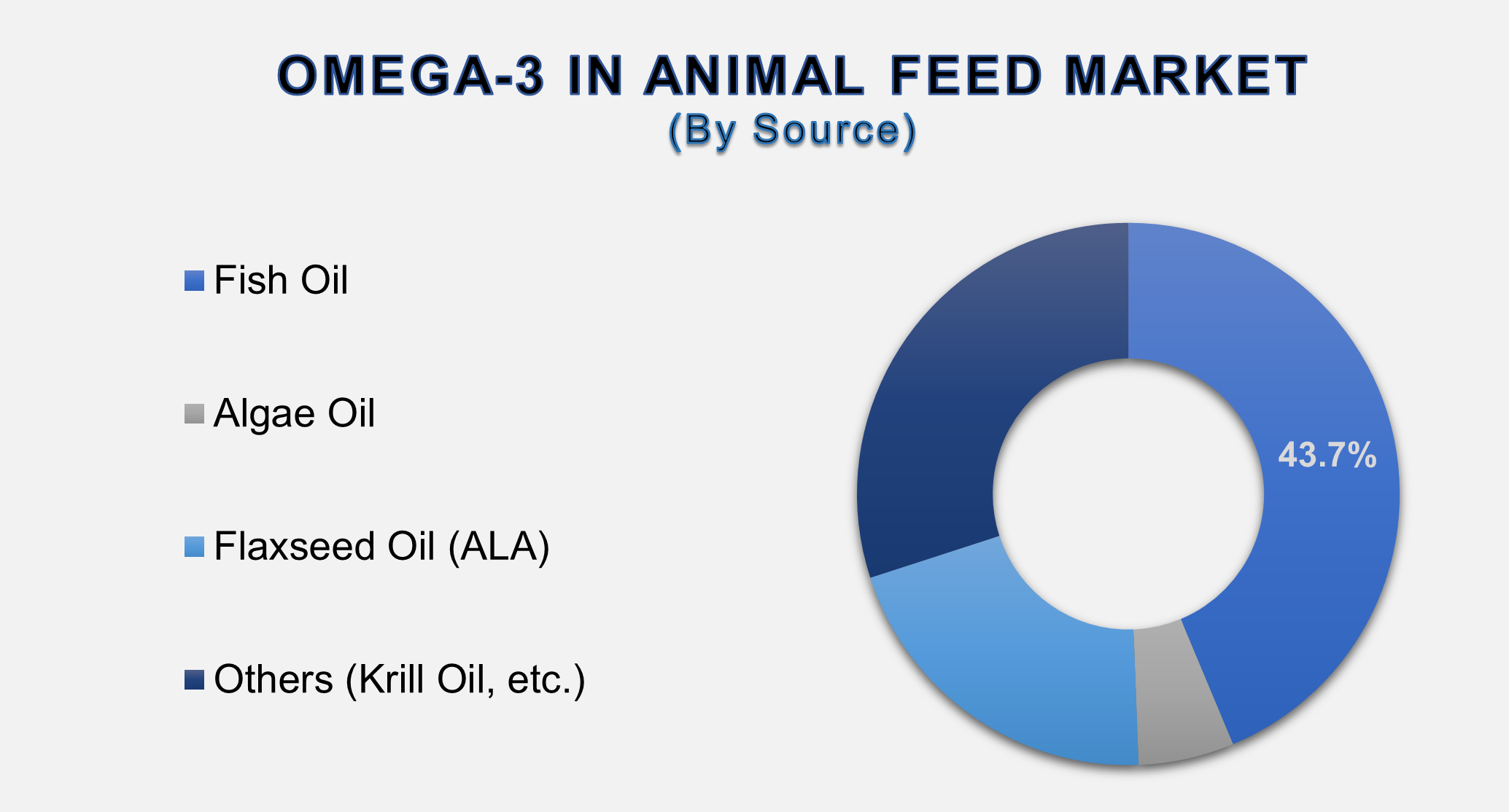

The Fish Oil segment is projected to command a dominant market share in 2025, remaining the cornerstone of the omega-3 feed ingredient industry, particularly in aquaculture. This dominance is rooted in its high concentration of the most bioavailable forms of EPA and DHA, which are essential for the health and development of farmed fish species like salmon and trout. The existing, well-established global supply chain and processing infrastructure for fish oil ensure its cost-effectiveness and widespread availability compared to newer alternatives. Despite growing sustainability concerns, its unparalleled efficiency in meeting the specific nutritional requirements of a massive and growing aquaculture sector secures its leading position in the short to medium term. However, its market share growth is expected to be tempered by the rapid ascent of alternative sources.

Aquaculture Segment as

the Largest Livestock Category for Omega-3 in Animal Feed Market

The

Aquaculture segment is projected to be the largest livestock category for

omega-3 consumption. This is an intrinsic requirement, not just a nutritional

enhancement. In the wild, fish obtain EPA and DHA by consuming algae or smaller

fish. In farmed settings, these essential fatty acids must be supplied through

the feed for proper growth, reproduction, bone development, and overall health.

The rapid global expansion of aquaculture to meet the world's growing demand

for seafood directly translates into increased consumption of omega-3

ingredients. As the most efficient and largest user of concentrated omega-3s,

the aquaculture industry's feed requirements form the bedrock of this market,

dwarfing the volumes used in other livestock sectors.

The following segments are

part of an in-depth analysis of the global Omega-3 in Animal Feed Market:

|

Market

Segments |

|

|

By Source |

●

Fish Oil ●

Algae Oil ●

Flaxseed Oil (ALA) ●

Others (Krill Oil,

etc.) |

|

By

Livestock |

●

Aquaculture ●

Pets ●

Poultry ●

Swine ●

Dairy &

Ruminants ●

Others |

Omega-3 in Animal Feed Market Share Analysis by

Region

The Asia Pacific region

is anticipated to hold the largest portion of the Omega-3 in the Animal Feed

Market globally throughout the forecast period.

Asia-Pacific's

dominance is directly attributed to its massive and rapidly growing aquaculture

industry, led by countries like China, India, and Vietnam. The region is the

world's largest producer and consumer of aquaculture products, creating an

immense, inherent demand for omega-3s in fish and shrimp feed. Rising

disposable incomes are also increasing the consumption of meat, eggs, and

dairy, prompting producers to use enhanced feed for better productivity and

product differentiation. Government initiatives supporting domestic aquaculture

and livestock production further solidify APAC's position as the largest

regional market.

China

is the single largest market within Asia-Pacific, driven by its unparalleled

scale in aquaculture and livestock production. The government's focus on food

security and self-sufficiency, coupled with a growing middle class demanding

higher-quality animal protein, fuels the demand for advanced animal nutrition,

including omega-3 fortified feed. The presence of large domestic feed

manufacturers and increasing investments in sustainable ingredient production

underscore the critical importance of the Chinese market.

Omega-3 in Animal Feed Market Competition

Landscape Analysis

The global omega-3 in animal

feed market is consolidated and features a mix of large, diversified

agribusinesses, specialized ingredient suppliers, and aquaculture nutrition

companies. Competition is based on product efficacy, sustainability

credentials, supply chain reliability, price, and technical support services.

Key strategies include vertical integration, securing sustainable raw material

sources (e.g., through fisheries partnerships or algae production), extensive

R&D to improve bioavailability and efficacy, and forming strategic

alliances with feed mills and large livestock producers.

Global Omega-3 in Animal

Feed Market Recent Developments News:

- In February 2025, DSM-Firmenich (now part of Firmenich) launched a

new, high-stability algae oil powder designed for inclusion in premixes

for poultry and swine feed.

- In November 2024, Cargill Incorporated expanded its partnership with

a biotechnology firm to scale up the use of algae-based omega-3s in its

salmon feed portfolios.

- In August 2024, BASF SE announced an investment to increase the

production capacity of its n-3 PUFA products for the animal nutrition

market.

- In May 2024, Veramaris (DSM-Evonik JV) reported a significant

increase in the use of its algal oil by major salmon farmers in Norway,

replacing marine-derived oils.

The Global Omega-3 in

Animal Feed Market Is Dominated by a Few Large Companies, such as

●

DSM-Firmenich

●

BASF SE

●

Cargill Incorporated

●

Archer Daniels Midland

Company (ADM)

●

Corbion N.V.

●

Veramaris (DSM &

Evonik JV)

●

Epax Norway AS

●

Olvea Group

●

Croda International

Plc

●

Omega Protein

Corporation (Part of Cooke Inc.)

●

GC Rieber Oils

●

Polaris

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Omega-3 in Animal

Feed Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Omega-3 in Animal Feed Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Mn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Omega-3 in Animal

Feed Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Source of Global Omega-3

in Animal Feed Market

1.3.2.Livestock of Global Omega-3

in Animal Feed Market

1.3.3.Region of Global Omega-3

in Animal Feed Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Mn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Regulatory

Scenario by Region

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Omega-3 in Animal Feed Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Omega-3 in Animal Feed Market Estimates

& Forecast Trend Analysis, by Source

4.1.

Global

Omega-3 in Animal Feed Market Revenue (US$ Mn) Estimates and Forecasts, by Source,

2020 - 2033

4.1.1.Fish Oil

4.1.2.Algae Oil

4.1.3.Flaxseed Oil (ALA)

4.1.4.Others (Krill Oil, etc.)

5. Global

Omega-3 in Animal Feed Market Estimates

& Forecast Trend Analysis, by Livestock

5.1.

Global

Omega-3 in Animal Feed Market Revenue (US$ Mn) Estimates and Forecasts, by Livestock

2020 - 2033

5.1.1.Aquaculture

5.1.2.Pets

5.1.3.Poultry

5.1.4.Swine

5.1.5.Dairy & Ruminants

5.1.6.Others

6. Global

Omega-3 in Animal Feed Market Estimates

& Forecast Trend Analysis, by region

6.1.

Global

Omega-3 in Animal Feed Market Revenue (US$ Mn) Estimates and Forecasts, by region,

2020 - 2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Omega-3

in Animal Feed Market: Estimates &

Forecast Trend Analysis

7.1.

North

America Omega-3 in Animal Feed Market Assessments & Key Findings

7.1.1.North America Omega-3 in

Animal Feed Market Introduction

7.1.2.North America Omega-3 in

Animal Feed Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Source

7.1.2.2. By Livestock

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Omega-3

in Animal Feed Market: Estimates &

Forecast Trend Analysis

8.1.

Europe

Omega-3 in Animal Feed Market Assessments & Key Findings

8.1.1.Europe Omega-3 in Animal

Feed Market Introduction

8.1.2.Europe Omega-3 in Animal

Feed Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Source

8.1.2.2. By Livestock

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

9. Asia Pacific Omega-3

in Animal Feed Market: Estimates &

Forecast Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Omega-3 in

Animal Feed Market Introduction

9.1.2.Asia Pacific Omega-3 in

Animal Feed Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Source

9.1.2.2. By Livestock

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Omega-3

in Animal Feed Market: Estimates &

Forecast Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Omega-3 in Animal Feed Market

Introduction

10.1.2.

Middle East & Africa Omega-3 in Animal Feed Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Source

10.1.2.2. By Livestock

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Omega-3 in Animal Feed Market:

Estimates & Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Omega-3 in Animal Feed Market Introduction

11.1.2.

Latin

America Omega-3 in Animal Feed Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

11.1.2.1. By Source

11.1.2.2. By Livestock

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Omega-3 in Animal Feed Market Product Mapping

13.2.

Global

Omega-3 in Animal Feed Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

13.3.

Global

Omega-3 in Animal Feed Market Tier Structure Analysis

13.4.

Global

Omega-3 in Animal Feed Market Concentration & Company Market Shares (%)

Analysis, 2024

14.

Company

Profiles

14.1.

DSM-Firmenich

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Product

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. BASF SE

14.3. Cargill

Incorporated

14.4. Archer

Daniels Midland Company (ADM)

14.5. Corbion N.V.

14.6. Veramaris

(DSM & Evonik JV)

14.7. Epax Norway

AS

14.8. Olvea Group

14.9. Croda

International Plc

14.10. Omega Protein

Corporation (Part of Cooke Inc.)

14.11. GC Rieber

Oils

14.12. Polaris

14.13. Other

Prominent Players

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables