Optoelectronics Market Size and Forecast (2020-2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Component (LEDs, Image Sensors, Laser Diodes, Optocouplers, Infrared Components), By Application (Lighting, Communication, Safety & Security, Measurement, Display), End-user (Consumer Electronics, Automotive, Telecommunications, Healthcare, Aerospace & Defense, and Others), and Geography

2025-12-05

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Optoelectronics Market Overview

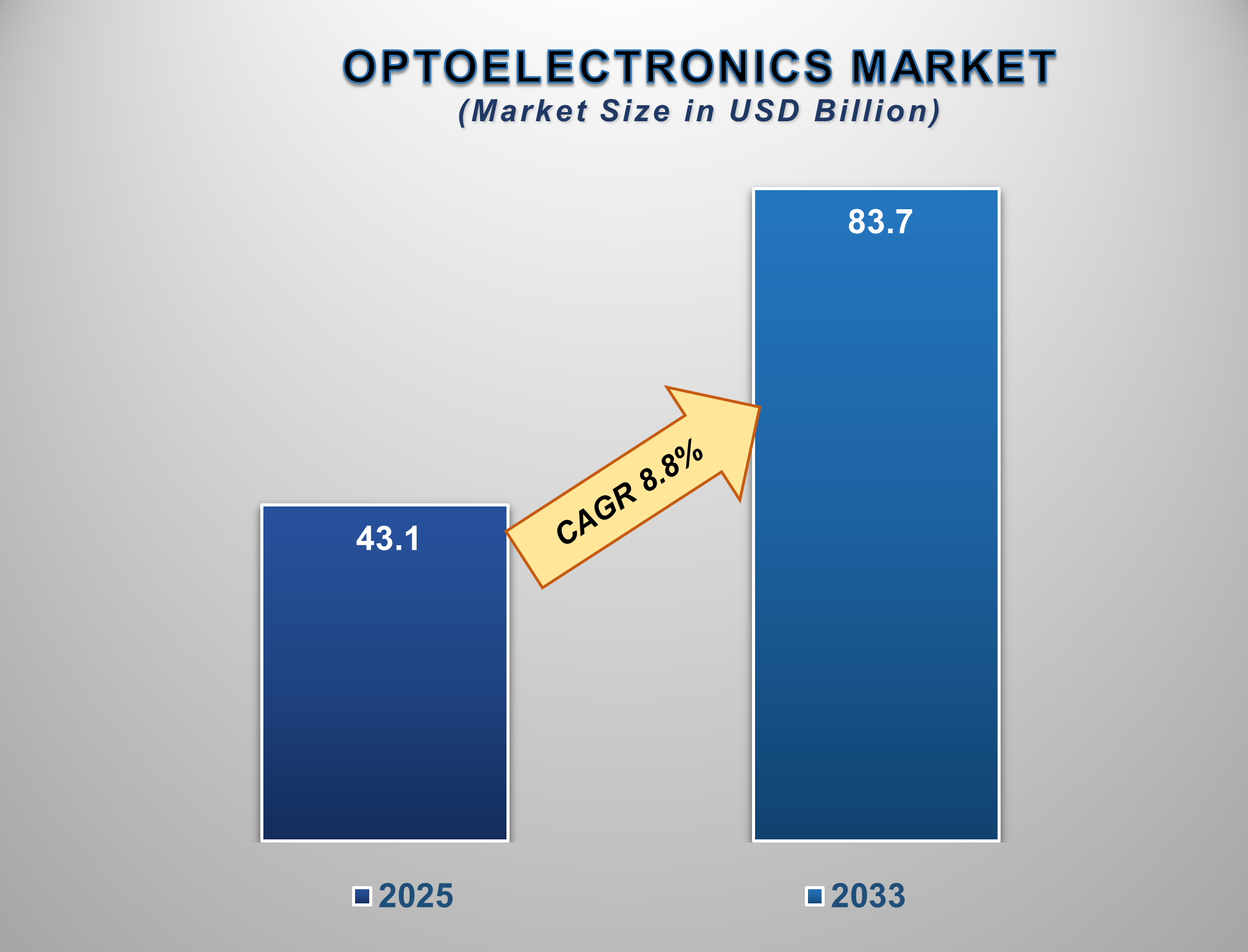

The Optoelectronics Market Size is poised for robust and sustained growth from 2025 to 2033, driven by the pervasive demand for energy-efficient lighting, the proliferation of sensing technologies, and the exponential growth in data communication. The market is projected to be valued at approximately USD 43.1 billion in 2025 and is forecasted to reach nearly USD 83.7 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.8% during this period.

Optoelectronics are devices that source, detect,

and control light, forming a critical bridge between electronics and photonics.

The market's expansion is underpinned by the global transition to solid-state

lighting, with Light Emitting Diodes (LEDs) dominating general illumination,

automotive lighting, and backlighting units. Furthermore, the surge in demand

for image sensors in smartphones, autonomous vehicles, and surveillance

systems, coupled with the critical role of laser diodes and infrared components

in data centers and fiber optic networks, are

key growth catalysts. The post-pandemic

emphasis on automation, smart homes, and digitalization across industries has

also accelerated adoption. The Asia-Pacific region currently leads the market

due to its massive electronics manufacturing base and high consumer demand,

while North America remains a key innovator, particularly in high-performance

applications for defense, healthcare, and

telecommunications.

Optoelectronics

Market Drivers and Opportunities

Energy Efficiency Mandates and Proliferation

of Sensing are the Primary Market Drivers

The global push for energy efficiency is the

most significant driver for the optoelectronics market, particularly for LEDs.

Government regulations phasing out incandescent bulbs and incentives for green

technologies have cemented the dominance of LED lighting. Simultaneously, the

proliferation of sensing across various industries is fueling demand. Image

sensors are essential for smartphone cameras, automotive ADAS (Advanced

Driver-Assistance Systems), and machine vision, while infrared sensors are critical

for night vision, biometric security, and temperature measurement. The

convergence of these two forces, efficient

light sources and advanced light detection, is

creating a self-reinforcing cycle of innovation and adoption.

Expansion of Data Communication and

Automotive Innovation is Fueling Market

Expansion

The insatiable global demand for high-speed data

is a major catalyst for the optoelectronics market. Laser diodes and

photodetectors are the backbone of fiber-optic communication networks that

underpin the internet, 5G infrastructure, and cloud computing. The growth of

data centers directly translates to increased demand for high-performance

optoelectronic components. In the automotive sector, the trend towards

electrification, autonomy, and enhanced safety is driving the adoption of

optoelectronics. LEDs for advanced lighting systems, LiDAR sensors for object

detection, and a multitude of in-cabin infrared sensors for driver monitoring

are creating a new, high-value market segment.

Advancements in Healthcare and the Emergence of AR/VR Present Significant Opportunities

The application of optoelectronics in medical

devices and the emergence of Augmented and Virtual Reality (AR/VR) are creating

significant growth frontiers. Key opportunities lie in the development of

miniaturized, high-resolution image sensors for endoscopy and other minimally

invasive surgical tools, as well as advanced laser systems for therapeutic and

diagnostic applications. In the consumer space, the AR/VR market relies

entirely on micro-displays, waveguides, and tracking sensors, presenting a massive

opportunity for component suppliers. For manufacturers, investing in R&D

for micro-LED displays, developing more powerful and efficient laser diodes for

LiDAR, and creating highly integrated sensor fusion modules are key strategies

to capture value in these high-growth, cutting-edge applications.

Optoelectronics Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 43.1 Billion |

|

Market Forecast in 2033 |

USD 83.7 Billion |

|

CAGR % 2025-2033 |

8.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Component ●

By Application ●

By End-user

Industry |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Optoelectronics Market

Report Segmentation Analysis

The global Optoelectronics Market

industry analysis is segmented by Component, by Application, end-user industry,

and by region.

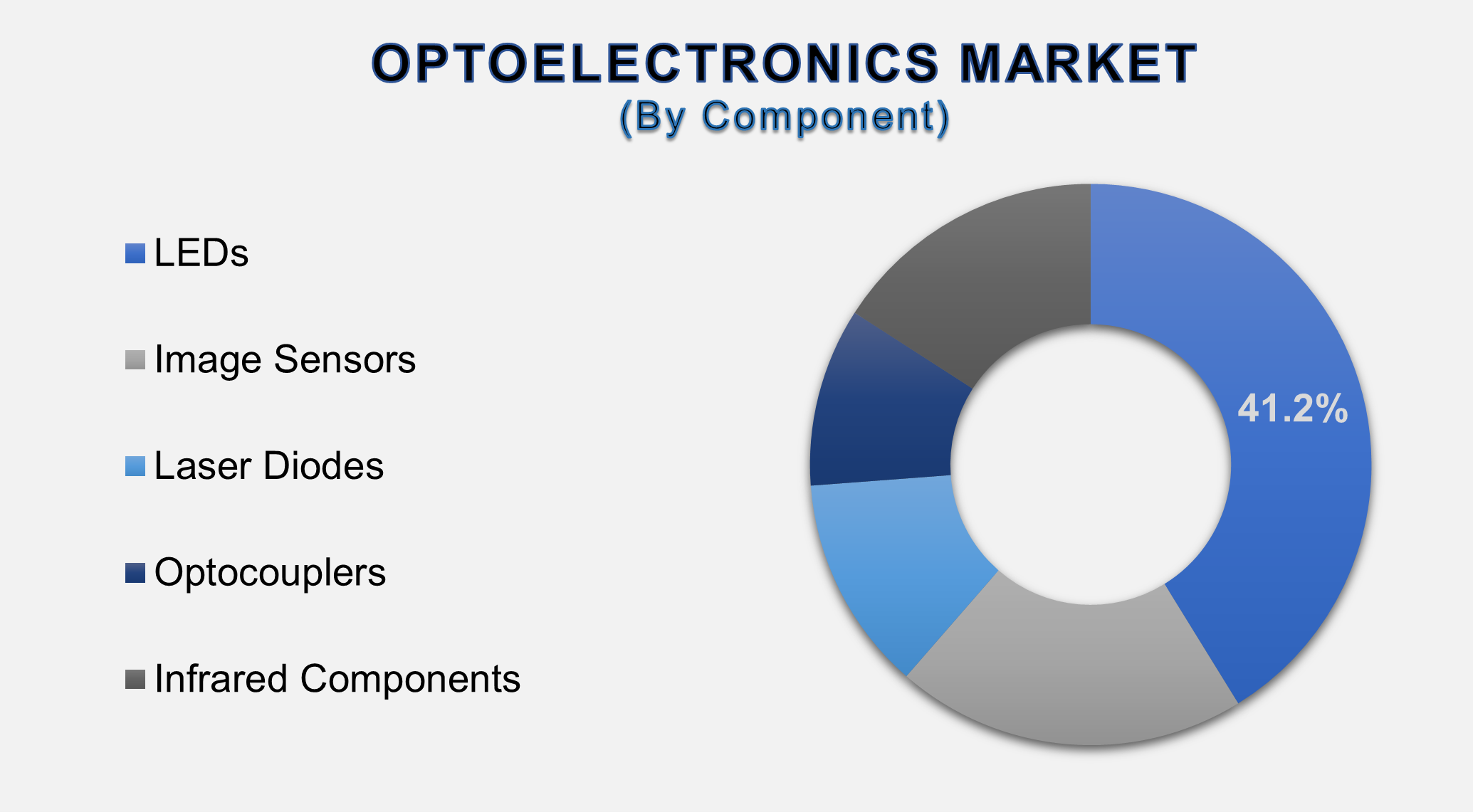

The LED component segment

is anticipated to command a significant market share in 2025.

The Component segment is categorized into LEDs, Image Sensors, Laser Diodes, Optocouplers, and Infrared Components. The LED segment dominates due to its ubiquitous application across lighting, automotive, signage, and consumer electronics. The long lifespan, declining costs, and superior energy efficiency of LEDs compared to traditional lighting have led to their massive adoption in general illumination. Beyond lighting, LEDs are critical for smartphone and TV displays, automotive headlights and taillights, and status indicators on countless electronic devices, ensuring this segment's continued revenue leadership.

The

Lighting application segment is projected to hold a substantial market share.

The

Application segment is divided into Lighting, Communication, Safety &

Security, Measurement, and Display. The Lighting segment's dominance is a

direct result of the global LED revolution. The retrofit market for existing

infrastructure and the integration of LEDs as the standard in all new

residential, commercial, and industrial buildings creates a massive, sustained

demand. While other segments like Communication are growing faster, the sheer

volume and scale of the lighting application secure its leading position in the

market. The increasing integration of smart and connected lighting systems is

further extending the growth trajectory of this segment.

The following segments are

part of an in-depth analysis of the global Optoelectronics Market:

|

Market

Segments |

|

|

By

Component |

●

LEDs ●

Image Sensors ●

Laser Diodes ●

Optocouplers ●

Infrared Components |

|

By

Application |

●

Lighting ●

Communication ●

Safety &

Security ●

Measurement ●

Display |

|

By End-user Industry |

●

Consumer Electronics ●

Automotive ●

Telecommunications ●

Healthcare ●

Aerospace &

Defence ●

Others |

Optoelectronics Market

Share Analysis by Region

The

Asia Pacific region is anticipated to hold the major share of the

Optoelectronics Market globally throughout the forecast period

Asia-Pacific's

dominance is fuelled by its position as the global hub for electronics

manufacturing, with countries like China, South Korea, Japan, and Taiwan

housing the world's leading semiconductor and consumer electronics companies.

The region has a massive consumer base with high demand for smartphones,

automobiles, and smart home devices, all of which are dense with optoelectronic

components. Strong government support for the semiconductor industry, a robust

supply chain, and the presence of key players like Sony (image sensors),

Samsung (LEDs), and LG Innotek solidify APAC's leading position. The rapid

industrialization and urbanization in emerging APAC economies further drive

demand for industrial and infrastructure-related optoelectronics.

China's

optoelectronics industry is currently defined by its aggressive push beyond

manufacturing dominance into cutting-edge innovation and strategic

self-sufficiency. Major players like BOE, CSOT, and Visionox are driving this

shift, with news heavily focused on three key areas. First, there's a

relentless pursuit of next-generation display technologies. Having conquered

the global LCD market, Chinese firms are now investing billions to master and

mass-produce advanced OLED, Mini-LED, and Micro LED panels, particularly for

high-growth applications like foldable smartphones and automotive displays.

Second,

the electric vehicle (EV) revolution is a massive catalyst for growth. The

sector's insatiable demand for large, interactive dashboard screens, advanced

LiDAR sensors for autonomous driving, and sophisticated LED lighting systems

has created a booming new market for optoelectronic components. Finally, the

geopolitical landscape, specifically US sanctions on advanced technology, has

accelerated China's "Xinchuang," or

domestic substitution policy. This national imperative to build a self-reliant

supply chain is a constant undercurrent in industry news, fueling investment in

homegrown semiconductor and photonics manufacturing to reduce foreign

dependence. Consequently, the narrative around Chinese optoelectronics has

evolved from one of sheer volume to one of strategic technological advancement

and supply chain security, positioning the sector at the heart of the country's

high-tech ambitions.

Optoelectronics Market

Competition Landscape Analysis

The global optoelectronics market

is highly competitive and fragmented, featuring a mix of large, diversified

electronics conglomerates and specialized component manufacturers. Competition

is intense and based on technological innovation, product performance, energy

efficiency, price, and reliability. Key strategies include heavy investment in

R&D to develop smaller, more efficient, and more powerful components;

strategic long-term contracts with major OEMs in the automotive and consumer

electronics sectors; and mergers & acquisitions to gain access to new

technologies or markets. The ability to provide integrated solutions and custom

components for specific high-growth applications is a critical differentiator

for leading players.

Global Optoelectronics

Market Recent Developments News:

- In

February 2025, Sony Semiconductor Solutions announced the development of a

new stacked CMOS image sensor with global shutter technology, targeting

high-speed industrial automation.

- In December 2024, ams OSRAM secured a major

contract to supply its Eviyos micro-LED pixel light modules for the

headlights of a new series of electric vehicles from a leading European

automaker.

- In October 2024, Coherent Corp. launched a new line

of high-power laser diodes designed for next-generation fiber laser pumps

and direct industrial processing applications.

- In August 2024, Nichia

Corporation reported a significant increase in sales of its laser diodes,

attributed to strong demand from the LiDAR and data center transceiver

markets.

The Global

Optoelectronics Market Is Dominated by a Few Large Companies, such as

●

Sony Corporation

●

Samsung Electronics

Co., Ltd.

●

ams OSRAM AG

●

Nichia Corporation

●

Sharp Corporation

●

Coherent Corp.

●

Broadcom Inc.

●

Vishay

Intertechnology, Inc.

●

TT Electronics PLC

●

Rohm Semiconductor

●

LG Innotek

●

Cree LED (an SGH

company)

●

Lumileds Holding B.V.

●

Everlight Electronics

Co., Ltd.

●

Stanley Electric Co.,

Ltd.

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

1. Global Optoelectronics

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Optoelectronics Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Optoelectronics

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Component of Global Optoelectronics

Market

1.3.2.Application of Global Optoelectronics

Market

1.3.3.End-user Industry of Global

Optoelectronics Market

1.3.4.Region of Global Optoelectronics

Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Pricing

Analysis

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Optoelectronics Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Optoelectronics Market Estimates

& Forecast Trend Analysis, by Component

4.1.

Global

Optoelectronics Market Revenue (US$ Bn) Estimates and Forecasts, by Component,

2020 - 2033

4.1.1.LEDs

4.1.2.Image Sensors

4.1.3.Laser Diodes

4.1.4.Optocouplers

4.1.5.Infrared Components

5. Global

Optoelectronics Market Estimates

& Forecast Trend Analysis, by Application

5.1.

Global

Optoelectronics Market Revenue (US$ Bn) Estimates and Forecasts, by Application,

2020 - 2033

5.1.1.Lighting

5.1.2.Communication

5.1.3.Safety & Security

5.1.4.Measurement

5.1.5.Display

6. Global

Optoelectronics Market Estimates

& Forecast Trend Analysis, by End-user Industry

6.1.

Global

Optoelectronics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user

Industry 2020 - 2033

6.1.1.Consumer Electronics

6.1.2.Automotive

6.1.3.Telecommunications

6.1.4.Healthcare

6.1.5.Aerospace & Defense

6.1.6.Others

7. Global

Optoelectronics Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Optoelectronics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Optoelectronics

Market: Estimates & Forecast Trend

Analysis

8.1. North America Optoelectronics

Market Assessments & Key Findings

8.1.1.North America Optoelectronics

Market Introduction

8.1.2.North America Optoelectronics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1.

By Component

8.1.2.2.

By Application

8.1.2.3.

By End-user Industry

8.1.2.4. By Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Optoelectronics

Market: Estimates & Forecast Trend

Analysis

9.1. Europe Optoelectronics

Market Assessments & Key Findings

9.1.1.Europe Optoelectronics

Market Introduction

9.1.2.Europe Optoelectronics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Component

9.1.2.2.

By Application

9.1.2.3.

By End-user Industry

9.1.2.4. By Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Optoelectronics

Market: Estimates & Forecast Trend

Analysis

10.1. Asia Pacific Market

Assessments & Key Findings

10.1.1.

Asia

Pacific Optoelectronics Market Introduction

10.1.2.

Asia

Pacific Optoelectronics Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1.

By Component

10.1.2.2.

By Application

10.1.2.3.

By End-user Industry

10.1.2.4. By Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Optoelectronics

Market: Estimates & Forecast Trend

Analysis

11.1. Middle East & Africa

Market Assessments & Key Findings

11.1.1. Middle

East & Africa

Optoelectronics Market Introduction

11.1.2. Middle

East & Africa

Optoelectronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1.

By Component

11.1.2.2.

By Application

11.1.2.3.

By End-user Industry

11.1.2.4. By Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Optoelectronics Market: Estimates &

Forecast Trend Analysis

12.1. Latin America Market

Assessments & Key Findings

12.1.1. Latin America Optoelectronics

Market Introduction

12.1.2. Latin America Optoelectronics

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Component

12.1.2.2.

By Application

12.1.2.3.

By End-user Industry

12.1.2.4. By Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13.

Country

Wise Market: Introduction

14.

Competition

Landscape

14.1. Global Optoelectronics

Market Product Mapping

14.2. Global Optoelectronics

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

14.3. Global Optoelectronics

Market Tier Structure Analysis

14.4. Global Optoelectronics

Market Concentration & Company Market Shares (%) Analysis, 2024

15.

Company

Profiles

15.1.

Sony Corporation

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2.

Samsung Electronics Co., Ltd.

15.3.

ams OSRAM AG

15.4.

Nichia Corporation

15.5.

Sharp Corporation

15.6.

Coherent Corp.

15.7.

Broadcom Inc.

15.8.

Vishay Intertechnology, Inc.

15.9.

TT Electronics PLC

15.10.

Rohm Semiconductor

15.11.

LG Innotek

15.12.

Cree LED (an SGH company)

15.13.

Lumileds Holding B.V.

15.14.

Everlight Electronics Co., Ltd.

15.15.

Stanley Electric Co., Ltd.

15.16.

Other Prominent Players

16. Research

Methodology

16.1. External Transportations /

Databases

16.2. Internal Proprietary

Database

16.3. Primary Research

16.4. Secondary Research

16.5. Assumptions

16.6. Limitations

16.7. Report FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables