Organic Electronics Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Material (Semiconductor, Conductive, Dielectric, Substrate and others); By Application (Flexible Displays, Organic Photovoltaics (OPV), Lighting (OLED), Printed Batteries, Sensors, Radio-Frequency Identification (RFID) Tags and others); By End-User (Consumer Electronics, Automotive, Healthcare, Retail & Packaging, Aerospace & Défense and others) and Geography

2025-10-27

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Organic Electronics Market Overview

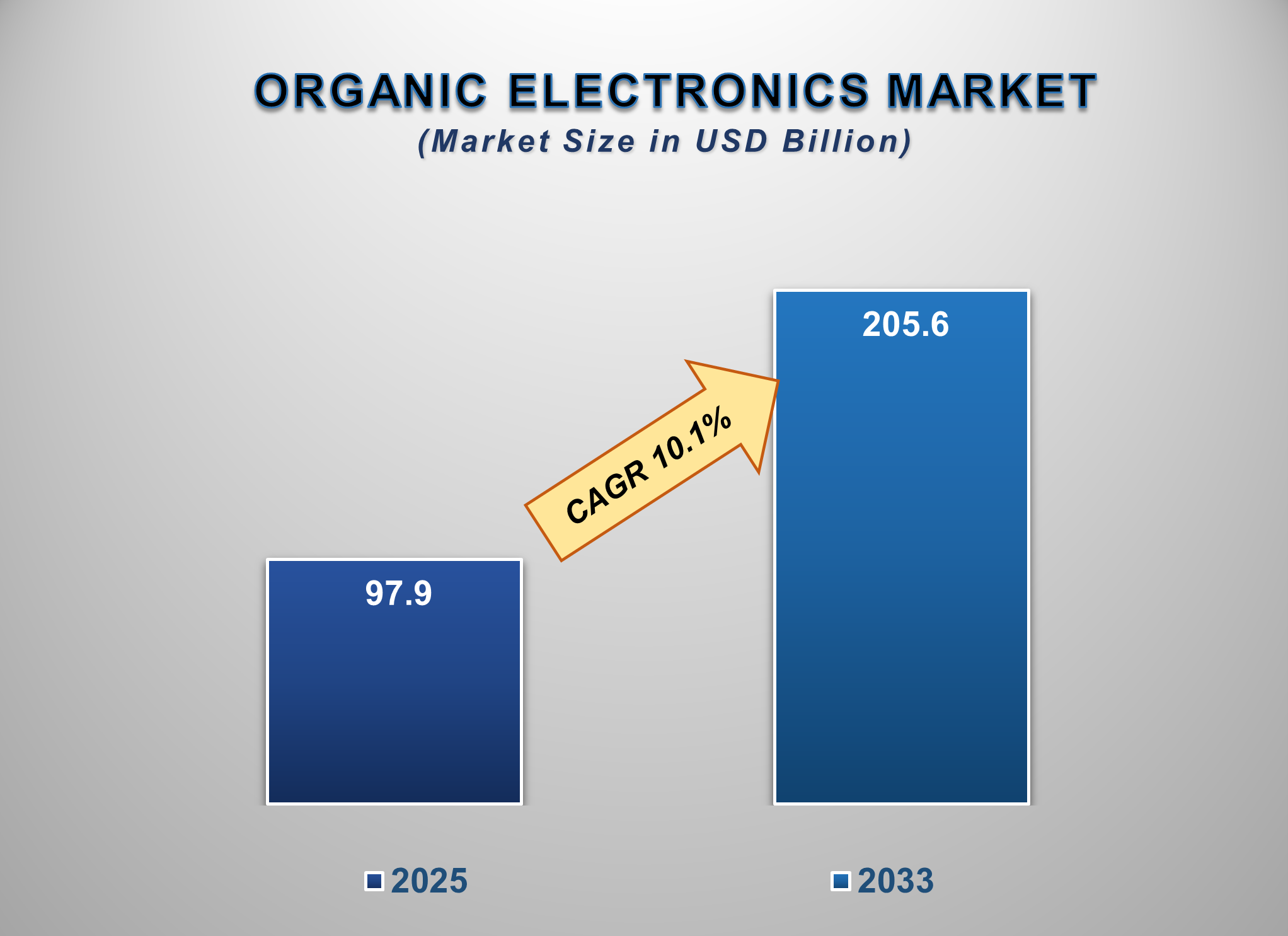

The organic electronics market size is projected to witness remarkable growth from 2025 to 2033, propelled by the escalating demand for flexible, lightweight, and energy-efficient electronic devices, alongside significant advancements in material science and printing technologies. Valued at approximately USD 97.9 billion in 2025, the market is expected to surge to USD 205.6 billion by 2033, reflecting a robust compound annual growth rate (CAGR) of 10.1% over the forecast period.

The organic electronics market is

experiencing a transformative phase, driven by the paradigm shift from rigid

silicon-based electronics to versatile, solution-processable organic materials.

The unique properties of organic semiconductors, including mechanical

flexibility, semi-transparency, and low-temperature manufacturing, are

unlocking novel applications across diverse industries. Key growth areas

include flexible OLED displays for smartphones and televisions, large-area

organic photovoltaics (OPV) for building-integrated applications, and

ultra-thin, conformal lighting solutions.

The market is further benefiting

from the rapid expansion of the Internet of Things (IoT) ecosystem, which

demands low-cost, printable sensors and RFID tags. Continuous R&D

investments are leading to improvements in the efficiency, stability, and lifetime

of organic electronic components, thereby broadening their commercial

viability. North America and Asia-Pacific are pivotal markets, with the latter

dominating production and consumption due to the strong presence of consumer

electronics manufacturers. The competitive landscape is characterized by

collaborations between chemical companies, display manufacturers, and research

institutions to accelerate innovation and commercialization.

Organic Electronics

Market Drivers and Opportunities

Proliferation of Flexible and Foldable Display Technology

The

insatiable consumer demand for innovative form factors in electronic devices is

a primary driver for the organic electronics market. Organic Light-Emitting

Diodes (OLEDs) are at the heart of the flexible and foldable display

revolution, enabling screens that can bend, roll, and fold. Major smartphone

and television manufacturers are heavily investing in this technology to

differentiate their products and capture market share. The superior performance

of OLEDs, including high contrast ratios, wide viewing angles, and faster

response times compared to traditional LCDs, is cementing their position as the

premium display technology. This trend is creating a sustained and high-volume

demand for organic semiconductors and conductive materials.

Push for Sustainable and Energy-Efficient Solutions

The

global emphasis on sustainability and energy conservation is significantly

driving the adoption of organic electronics. Organic Photovoltaics (OPV) offer

the potential for lightweight, semi-transparent, and customizable solar cells

that can be integrated into windows, facades, and vehicles, enabling on-site

power generation. Similarly, OLED lighting is recognized for its high energy

efficiency and superior quality of light, contributing to reduced energy

consumption. Government initiatives and regulations promoting green

technologies, coupled with growing corporate sustainability goals, are

providing a strong impetus for the development and deployment of these organic

electronic applications.

Opportunity for the

Organic Electronics Market

Expansion in Printed Electronics and Emerging IoT

Applications

A

significant opportunity lies in the low-cost, high-volume production

capabilities of printed electronics. Techniques like inkjet printing and

roll-to-roll processing allow for the fabrication of electronic components on

flexible substrates at a fraction of the cost of conventional silicon-based

methods. This opens up massive opportunities in the manufacturing of disposable

and ubiquitous electronics, particularly for the IoT market. The demand for

low-cost, printed sensors for health monitoring, smart packaging, and

environmental sensing, along with RFID tags for asset tracking and retail, is

expected to explode. Companies that can master the scalability and reliability

of printed organic electronics are poised to capture a substantial share of

this burgeoning market.

Organic Electronics

Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 97.9 Billion |

|

Market Forecast in 2033 |

USD 205.6 Billion |

|

CAGR % 2025-2033 |

10.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production, growth factors and more |

|

Segments Covered |

●

By Material ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

U.K. 4)

Germany 5)

France 6)

Italy 7)

Spain 8)

Netherland 9)

China 10)

India 11)

Japan 12)

South Korea 13)

Australia 14)

Mexico 15)

Brazil 16)

Argentina 17)

Saudi Arabia 18)

UAE 19)

Egypt 20) South Africa |

Organic Electronics

Market Report Segmentation Analysis

The global Organic Electronics

Market industry analysis is segmented by Material, by Application, by End-user,

and by region.

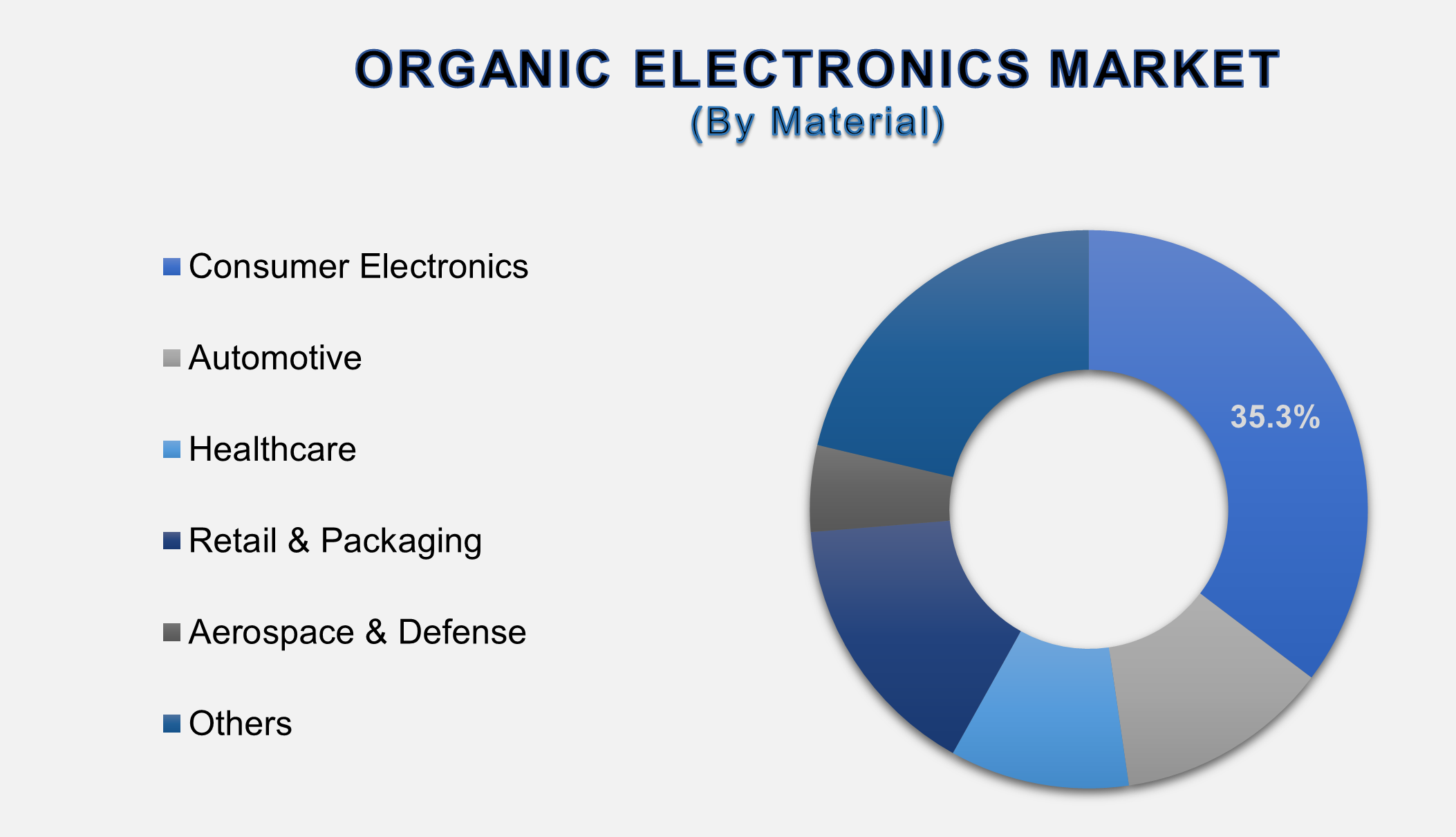

The Dominance of the Semiconductor Material Segment

The semiconductor material segment is the foundational pillar and revenue leader of the organic electronics market because these materials are the active "brain" of every device. Unlike other components like substrates or dielectrics, organic semiconductors possess the unique electronic properties that enable critical functions: they emit light in OLEDs, absorb light and generate charge in OPVs, and switch electrical currents in transistors. Their dominance is secured by two key factors. First, their performance directly dictates the efficiency, brightness, and longevity of the end product, making them the primary focus of intense R&D.

Material suppliers continuously

innovate molecular structures to enhance charge carrier mobility and

environmental stability, creating high-value, proprietary compounds. Second,

they are indispensable across all high-growth applications, from flexible

displays to printable sensors. As these applications proliferate, the demand

for advanced, specialized semiconductor materials surges, ensuring this

segment's continued profitability and major market share.

The Commanding Share of the Flexible Displays Application

Segment

The

Flexible Displays application segment commands a major market share because it

represents the most commercially successful and visible realization of organic

electronics to date. This dominance is driven by the ubiquitous adoption of

Organic Light-Emitting Diode (OLED) technology in high-value consumer products

like premium smartphones, televisions, and the rapidly growing category of

foldable devices. Organic electronics are uniquely suited for this role, as

they can be fabricated on flexible plastic substrates, enabling vivid,

ultra-thin, and unbreakable screens that are impossible with rigid

silicon-based LCDs.

The

consumer electronics industry's relentless drive for design differentiation and

enhanced user experience creates a powerful, sustained demand pull.

Furthermore, the substantial revenue generated from flagship devices with OLED

displays fuels a virtuous cycle of reinvestment into R&D, leading to

further improvements in display performance, production yields, and cost

reduction, thereby cementing the segment's leadership.

The Leadership of the Consumer Electronics End-User Segment

The

Consumer Electronics end-user segment is the largest and most influential

market for organic electronics, acting as the primary engine for its growth.

This dominance is a direct consequence of the sector's massive scale, fast

innovation cycles, and intense competition. Organic electronics, particularly

OLED displays and lighting, have become key differentiators in flagship

products, including smartphones, televisions, laptops, and wearables.

Manufacturers integrate these technologies to offer superior value

propositions: stunning visuals, slimmer form factors, energy efficiency, and,

crucially, the ability to create flexible and foldable devices.

The

sector's high production volumes ensure consistent, large-scale demand for

organic electronic components. Unlike specialized industries like aerospace or

healthcare, consumer electronics operate on a

global scale with shorter product lifecycles, which accelerates the adoption of

new technologies and continuously drives the market forward, making it the

undisputed leader among end-user segments.

The following segments are part of an in-depth analysis of the global

organic electronics market:

|

Market Segments |

|

|

By Material |

●

Semiconductor ●

Conductive Material ●

Dielectric ●

Substrate ●

Others |

|

By Application

|

●

Flexible Displays ●

Organic

Photovoltaics (OPV) ●

Lighting (OLED) ●

Printed Batteries ●

Sensors ●

Radio-Frequency

Identification (RFID) Tags ●

Others |

|

By End-user |

●

Consumer Electronics ●

Automotive ●

Healthcare ●

Retail &

Packaging ●

Aerospace &

Defense ●

Others |

Organic Electronics

Market Share Analysis by Region

The Asia-Pacific region is expected to

dominate the Global Organic Electronics Market during the forecast period.

Asia-Pacific is anticipated to be the undisputed leader in the global Organic Electronics Market. This dominance is anchored by the region's concentration of world-leading consumer electronics manufacturers (e.g., in South Korea, Japan, and China), massive electronics production capacity, and strong government support for advanced materials and display industries. Countries like China and South Korea are home to the largest OLED panel fabrication plants and are making significant investments in next-generation display and energy technologies. The presence of a robust supply chain, from material suppliers to end-device assemblers, creates a highly synergistic ecosystem that secures Asia-Pacific's leading position.

Global

Organic Electronics Market Recent Developments News:

- In January 2025, LG Display announced the

development of a stretchable OLED display prototype with a 20% elongation

capability, targeting future wearable and automotive applications.

- In February 2025, BASF SE and a leading Japanese

electronics firm unveiled a new class of high-performance,

solution-processable organic semiconductors designed to increase the

efficiency of printed OPV cells by 15%.

- In March 2025, Samsung Electronics Co., Ltd. began

mass production of its third-generation under-panel camera technology for

smartphones, utilizing advanced OLED materials to achieve a truly

full-screen display.

- In April 2025, Heliatek GmbH secured a major funding round to scale up its production of organic solar films for integration into commercial building facades across Europe.

The Global Organic Electronics Market is dominated by a few large companies, such as

●

Samsung Electronics

Co., Ltd.

●

LG Display Co., Ltd.

●

Universal Display

Corporation

●

AUO Corporation

●

BASF SE

●

Merck KGaA

●

Sony Corporation

●

Konica Minolta, Inc.

●

OSRAM GmbH

●

Covestro AG

●

Novaled GmbH (Part of

Samsung)

●

Heliatek GmbH

●

Cymbet Corporation

●

Thin Film Electronics

ASA

● Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

- Global Organic Electronics Market Introduction and Market Overview

- Objectives of the Study

- Global Organic Electronics Market Scope and Market Estimation

- Global Organic Electronics Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Organic Electronics Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Material of Global Organic Electronics Market

- Application of Global Organic Electronics Market

- End-user of Global Organic Electronics Market

- Region of Global Organic Electronics Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Organic Electronics Market

- Key Materials/Brand Analysis

- Pricing Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Organic Electronics Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Organic Electronics Market Estimates & Forecast Trend Analysis, by Material

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020 - 2033

- Semiconductor

- Conductive Material

- Dielectric

- Substrate

- Others

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020 - 2033

- Global Organic Electronics Market Estimates & Forecast Trend Analysis, by Application

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Flexible Displays

- Organic Photovoltaics (OPV)

- Lighting (OLED)

- Printed Batteries

- Sensors

- Radio-Frequency Identification (RFID) Tags

- Others

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Organic Electronics Market Estimates & Forecast Trend Analysis, by End-user

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Consumer Electronics

- Automotive

- Healthcare

- Retail & Packaging

- Aerospace & Defense

- Others

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Global Organic Electronics Market Estimates & Forecast Trend Analysis, by region

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Organic Electronics Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020 - 2033

- North America Organic Electronics Market: Estimates & Forecast Trend Analysis

- North America Organic Electronics Market Assessments & Key Findings

- North America Organic Electronics Market Introduction

- North America Organic Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- North America Organic Electronics Market Assessments & Key Findings

- Europe Organic Electronics Market: Estimates & Forecast Trend Analysis

- Europe Organic Electronics Market Assessments & Key Findings

- Europe Organic Electronics Market Introduction

- Europe Organic Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Application

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Netherland

- Rest of Europe

- Europe Organic Electronics Market Assessments & Key Findings

- Asia Pacific Organic Electronics Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Organic Electronics Market Introduction

- Asia Pacific Organic Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Organic Electronics Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Organic Electronics Market Introduction

- Middle East & Africa Organic Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Application

- By End-user

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Organic Electronics Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Organic Electronics Market Introduction

- Latin America Organic Electronics Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Material

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Organic Electronics Market Material Mapping

- Global Organic Electronics Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Organic Electronics Market Tier Structure Analysis

- Global Organic Electronics Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Samsung Electronics Co., Ltd.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Material Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Samsung Electronics Co., Ltd.

* Similar details would be provided for all the players mentioned below

- LG Display Co., Ltd.

- Universal Display Corporation

- AUO Corporation

- BASF SE

- Merck KGaA

- Sony Corporation

- Konica Minolta, Inc.

- OSRAM GmbH

- Covestro AG

- Novaled GmbH (Part of Samsung)

- Heliatek GmbH

- Cymbet Corporation

- Thin Film Electronics ASA

- Other Prominent Players

- Research Methodology

- External Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables