Orthopedic Devices Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Product (Joint Replacement/Orthopedic Implants, Spinal Implants, Dental, Trauma Implants, Sports Medicine, Body Reconstruction & Repair, Body Monitoring & Evaluation, Body Support & Recovery, Orthobiologics, Others); By End-user (Hospitals, Outpatient Facilities, Ambulatory Surgical Centers); And Geography

2025-08-20

Healthcare

Swetal (Research Analyst)

Description

Global Orthopedic Devices Market Overview

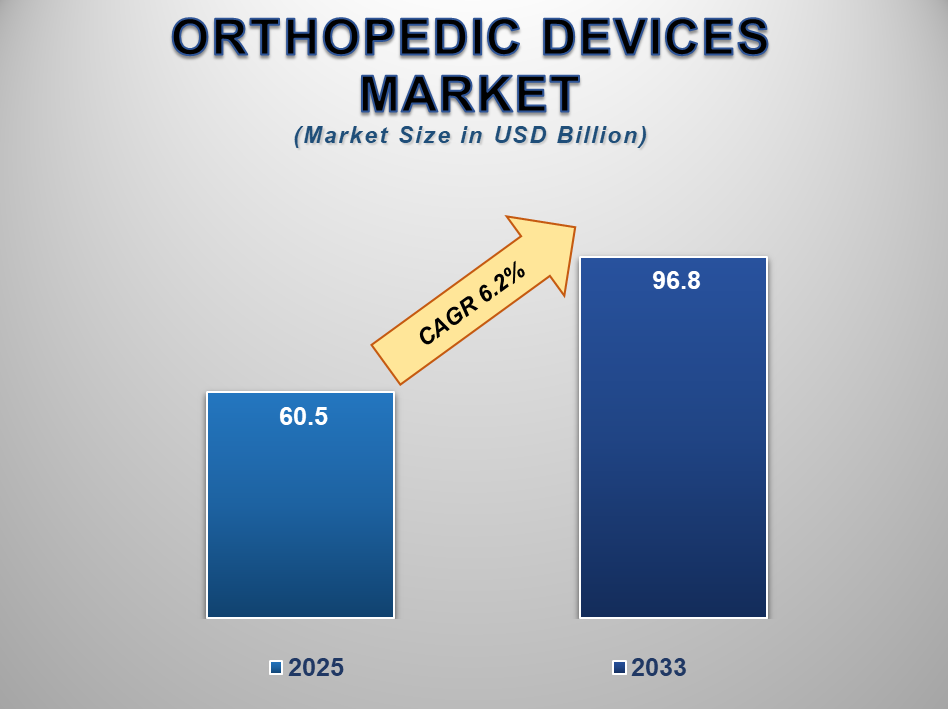

The global Orthopedic Devices Market was valued at USD 60.5 billion in 2025 and is projected to reach USD 96.8 billion by 2033, expanding at a CAGR of 6.2% during the forecast period. The market is driven by the growing incidence of musculoskeletal disorders, osteoarthritis, trauma injuries, and an aging population globally. Technological advancements in orthopedic implants and the rising demand for minimally invasive surgeries are also contributing to market expansion.

Joint replacement procedures,

such as knee, hip, and shoulder arthroplasties, are witnessing a surge due to

improved implant materials, 3D printing technologies, and robotic-assisted

surgical techniques. Orthobiologics such as stem cell therapy and bone

morphogenetic proteins (BMPs) are gaining traction in orthopedic care owing to

their regenerative potential. Additionally, rising sports participation and

road traffic injuries are leading to increased adoption of trauma and sports

medicine devices. Healthcare infrastructure improvements, especially in

emerging economies, and growing investments in ambulatory surgical centers

(ASCs) further support market growth. With shifting patient preferences toward

outpatient orthopedic procedures and post-operative recovery solutions, device

innovation and efficiency are becoming key competitive differentiators. As

global demand for motion-preserving, durable, and biocompatible implants

increases, the orthopedic devices market is poised for sustainable expansion.

Orthopedic Devices Market

Drivers and Opportunities

The growing geriatric population and the rising incidence of

orthopedic disorders are major drivers of market growth

The aging global population is

significantly contributing to the rising demand for orthopedic devices.

According to the WHO, the number of people aged 60 and older is expected to

reach over 2 billion by 2050. With aging comes an increased prevalence of

degenerative joint diseases such as osteoarthritis, osteoporosis, and other

musculoskeletal disorders that require surgical intervention and orthopedic

support. Additionally, sedentary lifestyles, obesity, and physical inactivity

are exacerbating orthopedic conditions across all age groups. Orthopedic

implants, such as hip and knee replacements, are increasingly being used to

restore mobility and improve quality of life. The demand for pain management

and joint reconstruction procedures has surged, especially in developed markets

with access to advanced healthcare infrastructure.

Moreover, spinal implants and

trauma fixation devices are in high demand due to a growing number of road

traffic accidents and workplace injuries. Governments and healthcare providers

are also focusing on value-based orthopedic care to reduce long-term disability

and hospital readmissions. These trends are expected to continue driving the

growth of the orthopedic devices market, especially in regions with rapidly

aging populations and rising lifestyle-related orthopedic ailments.

Increase in trauma cases and sports injuries drives demand

for orthopedic implants

The rising number of trauma cases

and sports-related injuries is another major factor propelling the orthopedic

devices market. With growing urbanization, mobility, and engagement in athletic

activities, the prevalence of fractures, dislocations, and ligament tears is

increasing globally. Young adults and athletes often require surgical

correction using devices such as screws, plates, pins, and arthroscopic tools,

particularly for knee, shoulder, and ankle injuries. Furthermore, road

accidents and workplace injuries are contributing significantly to the global

trauma burden, particularly in low- and middle-income countries. The demand for

trauma implants is also supported by enhanced emergency care infrastructure and

expanding insurance coverage in both developed and developing regions.

Orthopedic trauma care is now more accessible due to better hospital

facilities, rising surgical awareness, and improved implant availability. As

sports medicine and trauma recovery continue to advance with minimally invasive

approaches, the segment is expected to experience continued high demand

throughout the forecast period.

Opportunity for the Orthopedic Devices Market

Technological innovations in orthopedic implants and

procedures offer strong market opportunities

The orthopedic devices market is

poised for rapid transformation owing to advances in implant technology and

minimally invasive surgical techniques. Next-generation implants made from

biocompatible materials such as titanium alloys, PEEK, and ceramics are

enabling faster recovery, longer implant lifespan, and fewer complications. In

parallel, the growing adoption of robotic-assisted surgery, navigation systems,

and artificial intelligence in orthopedic operating rooms is enhancing surgical

precision and improving patient outcomes. Additionally, the advent of 3D

printing is enabling custom-fit implants tailored to the patient’s anatomy,

while smart implants equipped with sensors allow real-time monitoring of

implant performance post-surgery. These innovations are not only reducing the

burden on healthcare systems but also enhancing patient satisfaction and

outcomes. The growing demand for outpatient and day-care surgeries is pushing

manufacturers to develop portable and efficient tools that integrate with digital

platforms. Collectively, these advancements are unlocking new opportunities for

manufacturers to differentiate and scale their offerings across diverse

clinical settings and geographies.

Orthopedic Devices Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 60.5 Billion |

|

Market Forecast in 2033 |

USD 96.8 Billion |

|

CAGR % 2025-2033 |

6.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors, and more |

|

Segments Covered |

●

By Product ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Orthopedic Devices Market Report Segmentation Analysis

The global Orthopedic Devices

Market industry analysis is segmented by Product, by End-user, and by region.

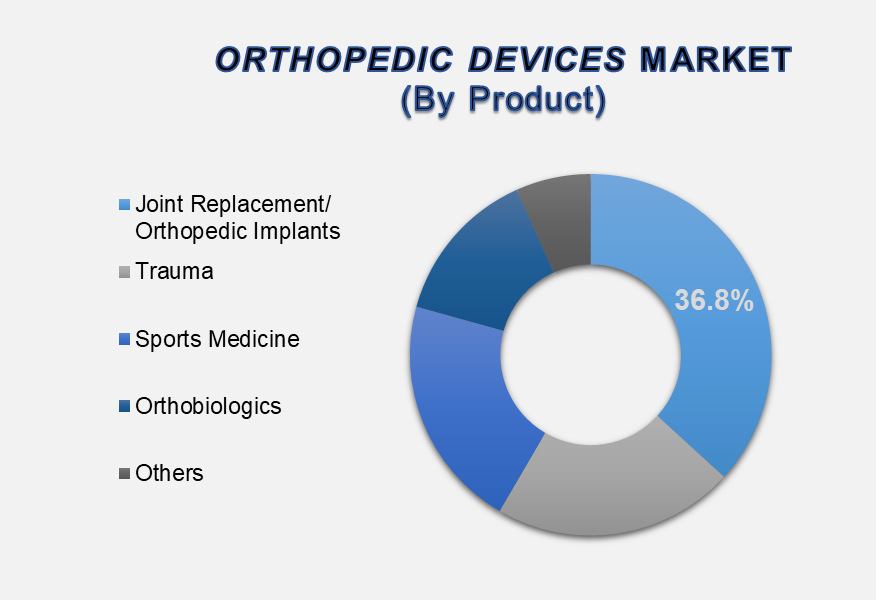

The Joint Replacement/Orthopedic Implants segment accounted

for the largest market share in the global Orthopedic Devices market

By Product, the market is segmented into Joint Replacement/Orthopedic Implants, Spinal Implants, Dental Implants, Trauma Implants, Accessories, Instruments, Sports Medicine, Body Reconstruction & Repair, Orthobiologics, and Others. The Joint Replacement/Orthopedic Implants segment accounted for 36.8% of the global market in 2024. This segment’s growth is driven by increasing hip and knee arthroplasty procedures among aging populations and patients with arthritis. Improved implant materials, robotic assistance, and better surgical techniques are making joint replacements more successful and accessible. Innovations in personalized and cementless implants are further fueling adoption, especially in high-volume surgical centers globally.

The Hospitals segment accounted for the largest market share

in the global Orthopedic Devices market

By End-user, the market is

segmented into Hospitals, Outpatient Facilities, and Ambulatory Surgical

Centers. The Hospitals segment held the largest market share in 2024, driven by

high volumes of complex orthopedic surgeries performed in these settings. Hospitals

offer comprehensive surgical care with advanced imaging, rehabilitation, and

trauma management capabilities. They also have access to robotic platforms and

navigation-assisted tools, enabling better precision during joint and spinal

procedures. Their strong reimbursement networks and partnerships with major

orthopedic device firms make them a critical distribution and innovation hub in

the orthopedic ecosystem.

The following segments are part

of an in-depth analysis of the global Orthopedic Devices Market:

|

Market Segments |

|

|

By Product |

●

Joint Replacement/

Orthopedic Implants o Lower Extremity Implants ▪

Knee Implants ▪

Hip Implants ▪

Foot & Ankle

Implants o Spinal Implants ▪

Dental ▪

Dental Implants o Craniomaxillofacial Implants ▪

Upper Extremity

Implants ▪

Elbow Implants ▪

Hand & Wrist

Implants o Shoulder Implants ●

Trauma o

Implants o

Accessories o

Instruments ●

Sports Medicine o

Body Reconstruction

& Repair o

Accessories o

Body Monitoring

& Evaluation o

Body Support &

Recovery ●

Orthobiologics o Viscosupplementation o Demineralized Bone Matrix o Synthetic Bone Substitutes o Bone Morphogenetic Protein (BMP) o Stem Cell Therapy o Allograft ●

Others |

|

By End-User |

●

Hospitals ●

Outpatient

Facilities ●

Ambulatory surgical

centers |

Orthopedic Devices Market

Share Analysis by Region

The North America region is projected to hold the largest

share of the global Orthopedic Devices market over the forecast period.

North America dominated the

global orthopedic devices market in 2024, accounting for a significant share of

45.7%. This dominance is largely attributed to the region’s advanced healthcare

infrastructure, high prevalence of arthritis and trauma-related conditions, and

rapid adoption of innovative surgical technologies. The U.S. market is

bolstered by favorable reimbursement frameworks, skilled orthopedic surgeons,

and strong collaborations between hospitals and device manufacturers. Key

players such as Johnson & Johnson, Stryker, and Zimmer Biomet are

headquartered in the region and contribute to early access to cutting-edge

products such as robotic surgery platforms, 3D-printed implants, and smart

prosthetics.

Furthermore, the Asia Pacific

region is anticipated to witness the highest CAGR during the forecast period,

driven by a large aging population, increasing lifestyle-related orthopedic

issues, and improved healthcare access. Countries like China, India, and Japan

are making significant investments in orthopedic infrastructure, medical

education, and trauma care. Growing awareness, expanding middle-class

populations, and increased insurance penetration are accelerating surgical

procedure volumes across the region. Medical tourism in APAC is also attracting

international patients seeking cost-effective orthopedic interventions. With

ongoing investment and innovation, the Asia Pacific is expected to become a key

growth engine in the global orthopedic devices market.

Orthopedic Devices Market Competition Landscape Analysis

The global

orthopedic devices market is dominated by players such as Johnson &

Johnson, Stryker, Zimmer Biomet, Smith & Nephew, Medtronic, and DJO Global.

These companies focus on joint reconstruction, trauma, and spine segments.

Emerging firms like NuVasive, Arthrex, and Globus Medical are gaining ground

with innovations in navigation systems and biologics. Strategic collaborations,

acquisitions, and a push into minimally invasive and AI-powered orthopedic

solutions define the competitive landscape.

Global Orthopedic Devices

Market Recent Developments News:

- In January

2025 - Stryker (US) finalized an agreement to divest its spinal implant

business to Viscogliosi Brothers, LLC (US), with the assets transferring

to a newly formed entity called VB Spine, LLC.

- In December 2024 - Zimmer Biomet (US) obtained FDA

510(k) clearance for its OsseoFit Stemless Shoulder System, a

comprehensive shoulder replacement solution.

- In December 2024 - Zimmer Biomet (US) received FDA

clearance for its Persona Solution PPS Femur, a knee component designed

for patients requiring cement-free or metal-sensitive implant options.

- In July 2024 - Smith+Nephew (UK) entered a strategic collaboration

with Healthcare Outcomes Performance Company (US) to enhance surgical

solutions through advanced digital analytics capabilities for healthcare

providers and ASCs.

The Global Orthopedic

Devices Market is dominated by a few large companies, such as

●

Johnson & Johnson

●

Stryker

●

Zimmer Biomet

●

Medtronic

●

Smith & Nephew

●

DJO Global

●

NuVasive

●

Globus Medical

●

Wright Medical Group

●

Arthrex

●

CONMED

●

Össur

●

B. Braun

●

Aesculap

●

Corin Group

●

MicroPort Scientific

●

Exactech

●

Orthofix

●

RTI Surgical

●

SeaSpine

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Orthopedic Devices Market Introduction and Market Overview

- Objectives of the Study

- Global Orthopedic Devices Market Scope and Market Estimation

- Global Orthopedic Devices Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Orthopedic Devices Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Product of Global Orthopedic Devices Market

- End-user of Global Orthopedic Devices Market

- Region of Global Orthopedic Devices Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Orthopedic Devices Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Orthopedic Devices Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Orthopedic Devices Market Estimates & Forecast Trend Analysis, by Product

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Joint Replacement/ Orthopedic Implants

- Lower Extremity Implants

- Knee Implants

- Hip Implants

- Foot & Ankle Implants

- Spinal Implants

- Dental

- Dental Implants

- Craniomaxillofacial Implants

- Upper Extremity Implants

- Elbow Implants

- Hand & Wrist Implants

- Shoulder Implants

- Trauma

- Implants

- Accessories (Plates, Screws, Nails, Pins, Wires)

- Instruments

- Sports Medicine

- Body Reconstruction & Repair

- Accessories

- Body Monitoring & Evaluation

- Body Support & Recovery

- Orthobiologics

- Viscosupplementation

- Demineralized Bone Matrix

- Synthetic Bone Substitutes

- Bone Morphogenetic Protein (BMP)

- Stem Cell Therapy

- Allograft

- Others

- Lower Extremity Implants

- Joint Replacement/ Orthopedic Implants

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2020 - 2033

- Global Orthopedic Devices Market Estimates & Forecast Trend Analysis, by End-user

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Hospitals

- Outpatient Facilities

- Ambulatory surgical centers

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2020 - 2033

- Global Orthopedic Devices Market Estimates & Forecast Trend Analysis, by Region

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Orthopedic Devices Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Orthopedic Devices Market: Estimates & Forecast Trend Analysis

- North America Orthopedic Devices Market Assessments & Key Findings

- North America Orthopedic Devices Market Introduction

- North America Orthopedic Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By End-user

- By Country

- The U.S.

- Canada

- North America Orthopedic Devices Market Assessments & Key Findings

- Europe Orthopedic Devices Market: Estimates & Forecast Trend Analysis

- Europe Orthopedic Devices Market Assessments & Key Findings

- Europe Orthopedic Devices Market Introduction

- Europe Orthopedic Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Orthopedic Devices Market Assessments & Key Findings

- Asia Pacific Orthopedic Devices Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Orthopedic Devices Market Introduction

- Asia Pacific Orthopedic Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Orthopedic Devices Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Orthopedic Devices Market Introduction

- Middle East & Africa Orthopedic Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By End-user

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Orthopedic Devices Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Orthopedic Devices Market Introduction

- Latin America Orthopedic Devices Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Product

- By End-user

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Orthopedic Devices Market Product Mapping

- Global Orthopedic Devices Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Orthopedic Devices Market Tier Structure Analysis

- Global Orthopedic Devices Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Johnson & Johnson

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Johnson & Johnson

* Similar details would be provided for all the players mentioned below

- Stryker

- Zimmer Biomet

- Medtronic

- Smith & Nephew

- DJO Global

- NuVasive

- Globus Medical

- Wright Medical Group

- Arthrex

- CONMED

- Össur

- Braun

- Aesculap

- Corin Group

- MicroPort Scientific

- Exactech

- Orthofix

- RTI Surgical

- SeaSpine

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables