Packaging Testing Services Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Testing Type (Physical, Mechanical, Chemical, and Microbiological), By Material (Plastic, Glass, Metal, Paper & Paperboard, and Others), By End-Use Industry (Food & Beverage, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Chemicals, and Others) And Geography

2025-12-12

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Packaging

Testing Services Market Overview

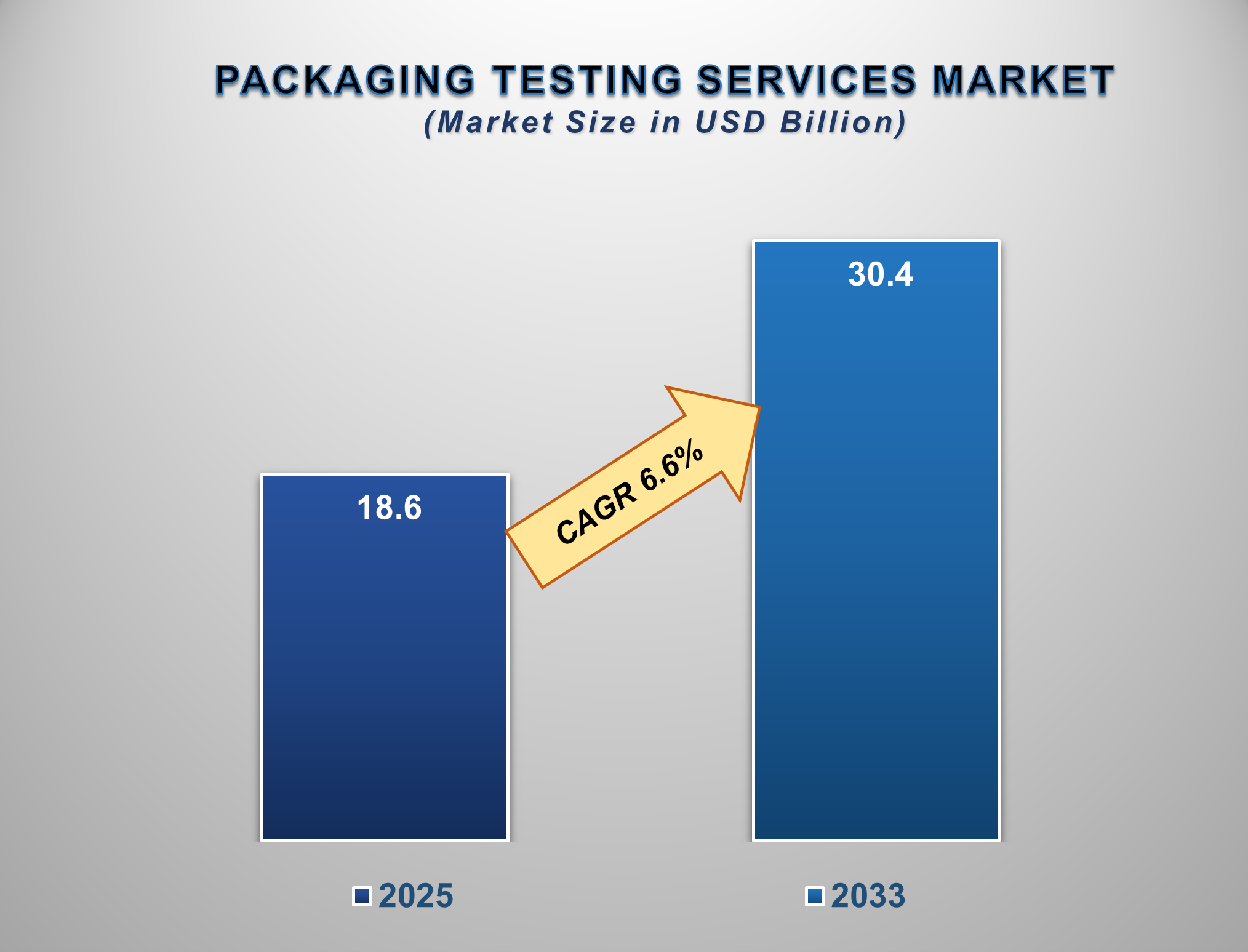

The Packaging Testing Services Market is positioned for robust growth from 2025 to 2033, fueled by stringent regulatory standards, rising consumer awareness about product safety, and the global expansion of packaged goods. The market is projected to be valued at approximately USD 18.6 billion in 2025 and is forecasted to reach nearly USD 30.4 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.6% during this period.

Packaging testing services are essential for

evaluating the performance, durability, safety, and compliance of packaging

materials and finished packages. These services ensure that products are

protected throughout the supply chain, maintain their integrity, and are safe

for the end-consumer. The market's expansion is underpinned by factors such as

the increasing complexity of global supply chains, the growing demand for

sustainable packaging, and strict regulations in the pharmaceutical and food

& beverage industries. Technological advancements in testing equipment,

such as the integration of automation and data analytics, are enhancing testing

accuracy and efficiency. North America and Europe are mature markets with a

strong focus on regulatory compliance, while the Asia-Pacific region is

expected to witness the fastest growth, driven by rapid industrialization, a

booming e-commerce sector, and rising quality standards.

Packaging Testing Services Market Drivers and

Opportunities

Stringent Regulatory Compliance and Focus on Product Safety

Are the Primary Market Drivers

The implementation of strict global and regional

regulations governing packaging safety, particularly in the food, beverage, and

pharmaceutical sectors, is the most significant driver for the packaging

testing services market. Agencies like the FDA (U.S.), EMA (Europe), and others

mandate rigorous testing for migration of substances, material composition, and

child-resistant features. Concurrently, rising consumer awareness about product

contamination and quality is pressuring brands to invest in independent

verification of their packaging's safety and integrity. This dual pressure from

regulators and consumers creates a non-discretionary and sustained demand for

comprehensive testing services to avoid costly recalls, legal liabilities, and

brand damage.

Growth of E-commerce and Sustainable Packaging Is Driving

Market Evolution

The explosive growth of the e-commerce industry

has created a critical need for packaging that can withstand the rigors of the

logistics environment. This has led to a surge in demand for mechanical and

physical testing services, such as vibration, shock, and compression testing,

to ensure products arrive undamaged. Simultaneously, the global shift towards

sustainable packaging materials like bioplastics, recycled paper, and novel

composites requires extensive testing to validate their performance, barrier properties,

and safety compared to traditional materials. This trend is pushing testing

laboratories to develop new protocols and capabilities to handle innovative,

eco-friendly packaging solutions.

Expansion in Emerging Economies and Outsourcing Trends

Present Significant Opportunities

The rapid growth of manufacturing, especially in

the food, pharmaceutical, and consumer goods sectors in Asia-Pacific, Latin

America, and the Middle East, presents a major growth frontier. As local

companies aim to export to regulated markets and multinationals set up

production facilities, the demand for internationally accredited testing

services skyrockets. This offers a massive opportunity for global testing

service providers to expand their footprint. Furthermore, the increasing trend

of outsourcing testing functions to specialized third-party laboratories,

rather than maintaining in-house capabilities, is a key strategic opportunity.

This allows manufacturers to access expert knowledge, state-of-the-art

equipment, and accredited services in a cost-effective manner.

Packaging Testing Services Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 18.6 Billion |

|

Market Forecast in 2033 |

USD 30.4 Billion |

|

CAGR % 2025-2033 |

6.6% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Testing Type ●

By Material ●

By End-user

Industry |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Packaging Testing Services Market Report

Segmentation Analysis

The global Packaging Testing

Services Market industry analysis is segmented by Testing Type, by Material, by

End-Use Industry, and by Region.

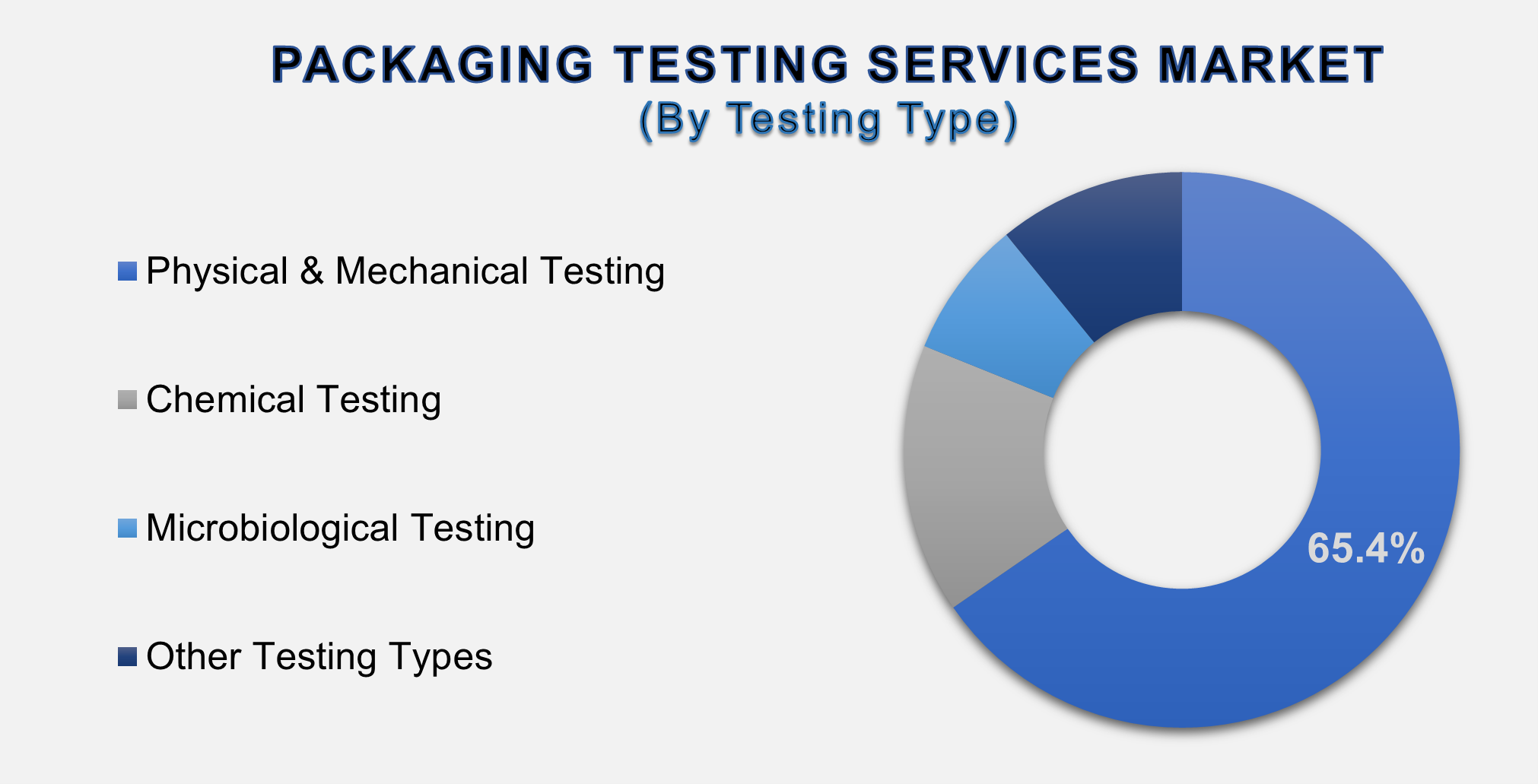

The Physical &

Mechanical Testing segment is anticipated to command a dominant market share in

2025.

The Testing Type segment is categorized into Physical, Mechanical, Chemical, and Microbiological. The Physical & Mechanical Testing segment commands a dominant market share, as it forms the foundation of package integrity and performance. These tests are crucial across all industries to ensure packaging can protect its contents from real-world stresses. Key tests include compression strength (for stacking in warehouses), drop/impact resistance (for handling and shipping), vibration testing (for transport), and tear resistance. The growth of e-commerce and complex global supply chains has made these tests indispensable for minimizing in-transit damage and associated financial losses.

The Healthcare &

Pharmaceuticals segment is projected to be the fastest-growing.

The

End-Use Industry segment is divided into Food & Beverage, Healthcare &

Pharmaceuticals, Personal Care & Cosmetics, Chemicals, and Others. The

Healthcare & Pharmaceuticals segment is projected to be the fastest-growing

end-user due to the exceptionally high stakes of product safety and stringent

regulatory oversight. Packaging for drugs, medical devices, and vaccines must

undergo rigorous testing for sterility, container closure integrity,

drug-package interaction (leachables & extractables), and stability. The

rapid development of biologics, complex injectables, and the need for

ultra-cold chain packaging for certain pharmaceuticals are driving demand for

highly specialized and sensitive testing services to ensure patient safety and

regulatory approval.

The Plastic material

segment is projected to exhibit strong growth.

The

Material segment includes Plastic, Glass, Metal, Paper & Paperboard, and

Others. The Plastic segment exhibits strong growth and remains a major focus

for testing services due to its ubiquitous use and the dual challenges of

ensuring its safety and evolving towards sustainability. While its dominance is

challenged by environmental concerns, it remains a primary packaging material.

This drives demand for tests on recyclability, recycled content validation, and

migration of substances from complex multi-layer plastics. Furthermore, the

development and testing of new bioplastics and compostable polymers require

extensive analysis to verify their performance and safety, ensuring this

segment remains a key revenue generator for testing laboratories.

The following segments are

part of an in-depth analysis of the global Packaging Testing Services Market:

|

Market

Segments |

|

|

By Testing

Type |

●

Physical &

Mechanical Testing ●

Chemical Testing ●

Microbiological

Testing ●

Other Testing Types |

|

By Material |

●

Plastic ●

Glass ●

Metal ●

Paper &

Paperboard ●

Others |

|

By End-user Industry |

●

Food & Beverage ●

Healthcare &

Pharmaceuticals ●

Personal Care &

Cosmetics ●

Chemicals ●

Others |

Packaging Testing Services Market Share Analysis

by Region

The North America region

is anticipated to hold the largest portion of the Packaging Testing Services

Market globally throughout the forecast period.

North

America's dominance is attributed to its mature and highly regulated consumer

markets, particularly in the food and pharmaceutical sectors. The presence of

major global brands, a strong culture of litigation and product liability, and

strict enforcement by agencies like the FDA and EPA creates a mandatory and high-value demand for accredited testing

services. The region also has a high concentration of leading testing service

providers and a robust logistics and e-commerce sector that relies heavily on

package performance validation.

In

addition, the Asia-Pacific region is

anticipated to be the fastest-growing region, driven by its position as the

global manufacturing hub. The rapid expansion of its domestic middle class with

higher quality expectations, coupled with increasing exports to regulated Western

markets, is compelling manufacturers to invest in quality assurance.

Governments in countries like China and India are also strengthening their own

regulatory frameworks for product and packaging safety, further propelling the

need for professional testing services and attracting significant investment

from international testing firms.

Packaging Testing Services Market Competition

Landscape Analysis

The global packaging testing

services market is fragmented and competitive, featuring a mix of large

multinational testing, inspection, and certification (TIC) corporations and

specialized regional players. Competition is based on accreditation, technical

expertise, global network, turnaround time, and price. Key strategies include

geographic expansion into high-growth markets, acquisitions of smaller

specialized labs to broaden service portfolios, and heavy investment in new

testing methodologies for sustainable and advanced materials. Building

long-term partnerships with major fast-moving consumer goods (FMCG) and

pharmaceutical companies is also a critical success factor.

Global Packaging Testing Services Market Recent

Developments News:

- In January 2025, SGS SA opened a new state-of-the-art packaging

testing facility in India, focusing on e-commerce durability and

pharmaceutical integrity testing.

- In November 2024, Eurofins Scientific acquired a specialized

laboratory in the United States to strengthen its capabilities in

extractables and leachables (E&L) testing for pharmaceutical

packaging.

- In August 2024, Intertek Group plc launched a new digital platform

that provides clients with real-time tracking and analytics for their

packaging testing projects.

- In May 2024, Bureau Veritas introduced a new suite of testing

services specifically designed to validate the composability and

recyclability claims of sustainable packaging materials.

The Global Packaging Testing Services Market Is

Dominated by a Few Large Companies, such as

●

SGS SA

●

Bureau Veritas SA

●

Intertek Group plc

●

Eurofins Scientific SE

●

TUV SUD AG

●

ALS Limited

●

Mérieux NutriSciences

●

Microbac Laboratories,

Inc.

●

CRYOPAK (An ADP

Company)

●

National Technical

Systems (NTS)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Packaging Testing

Services Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Packaging Testing Services Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Mn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Packaging Testing

Services Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Testing Type of Global Packaging

Testing Services Market

1.3.2.Material of Global Packaging

Testing Services Market

1.3.3.End-user Industry of Global

Packaging Testing Services Market

1.3.4.Region of Global Packaging

Testing Services Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Mn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Regulatory

Scenario by Region

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Packaging Testing Services Market

Estimates & Historical Trend Analysis (2020 - 2024)

4. Global

Packaging Testing Services Market

Estimates & Forecast Trend Analysis, by Testing

Type

4.1.

Global

Packaging Testing Services Market Revenue (US$ Mn) Estimates and Forecasts, by Testing

Type, 2020 - 2033

4.1.1.Physical & Mechanical

Testing

4.1.2.Chemical Testing

4.1.3.Microbiological Testing

4.1.4.Other Testing Types

5. Global

Packaging Testing Services Market

Estimates & Forecast Trend Analysis, by Material

5.1.

Global

Packaging Testing Services Market Revenue (US$ Mn) Estimates and Forecasts, by Material,

2020 - 2033

5.1.1.Plastic

5.1.2.Glass

5.1.3.Metal

5.1.4.Paper & Paperboard

5.1.5.Others

6. Global

Packaging Testing Services Market

Estimates & Forecast Trend Analysis, by End-user

Industry

6.1.

Global

Packaging Testing Services Market Revenue (US$ Mn) Estimates and Forecasts, by End-user

Industry 2020 - 2033

6.1.1.Food & Beverage

6.1.2.Healthcare &

Pharmaceuticals

6.1.3.Personal Care &

Cosmetics

6.1.4.Chemicals

6.1.5.Others

7. Global

Packaging Testing Services Market

Estimates & Forecast Trend Analysis, by region

7.1.

Global

Packaging Testing Services Market Revenue (US$ Mn) Estimates and Forecasts, by region,

2020 - 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Packaging

Testing Services Market: Estimates

& Forecast Trend Analysis

8.1.

North

America Packaging Testing Services Market Assessments & Key Findings

8.1.1.North America Packaging

Testing Services Market Introduction

8.1.2.North America Packaging

Testing Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Testing

Type

8.1.2.2. By Material

8.1.2.3. By End-user

Industry

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Packaging

Testing Services Market: Estimates

& Forecast Trend Analysis

9.1.

Europe

Packaging Testing Services Market Assessments & Key Findings

9.1.1.Europe Packaging Testing

Services Market Introduction

9.1.2.Europe Packaging Testing

Services Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Testing

Type

9.1.2.2. By Material

9.1.2.3. By End-user

Industry

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Packaging

Testing Services Market: Estimates

& Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Packaging Testing Services Market Introduction

10.1.2.

Asia

Pacific Packaging Testing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

10.1.2.1. By Testing

Type

10.1.2.2. By Material

10.1.2.3. By End-user

Industry

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Packaging

Testing Services Market: Estimates

& Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Packaging Testing Services Market

Introduction

11.1.2.

Middle East & Africa Packaging Testing Services Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Testing

Type

11.1.2.2. By Material

11.1.2.3. By End-user

Industry

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Packaging Testing Services Market:

Estimates & Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Packaging Testing Services Market Introduction

12.1.2.

Latin

America Packaging Testing Services Market Size Estimates and Forecast (US$ Billion)

(2020 - 2033)

12.1.2.1. By Testing

Type

12.1.2.2. By Material

12.1.2.3. By End-user

Industry

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Packaging Testing Services Market Product Mapping

14.2.

Global

Packaging Testing Services Market Concentration Analysis, by Leading Players /

Innovators / Emerging Players / New Entrants

14.3.

Global

Packaging Testing Services Market Tier Structure Analysis

14.4.

Global

Packaging Testing Services Market Concentration & Company Market Shares (%)

Analysis, 2024

15.

Company

Profiles

15.1.

GE Healthcare

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Siemens

Healthineers

15.3. Philips

15.4. Canon Medical

Systems Corporation

15.5. Fujifilm

Holdings Corporation

15.6. Hitachi, Ltd.

15.7. Medtronic plc

15.8. Nihon Kohden

Corporation

15.9. Elekta AB

15.10. Brainlab AG

15.11. Shimadzu

Corporation

15.12. MinFound

Medical Systems Co., Ltd.

15.13. NeuroLogica

Corp (Samsung)

15.14. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables