Pet Clothing Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Apparel, Footwear, Accessories), By Pet Type (Dogs, Cats, Others), By Material (Cotton, Wool & Knits, Synthetic, Others), By Distribution Channel (Specialty Stores, Online Retail, Hypermarkets/Supermarkets) And Geography

2025-12-17

Consumer Products

Jaya Bundele (Research Analyst)

Description

Pet Clothing

Market Overview

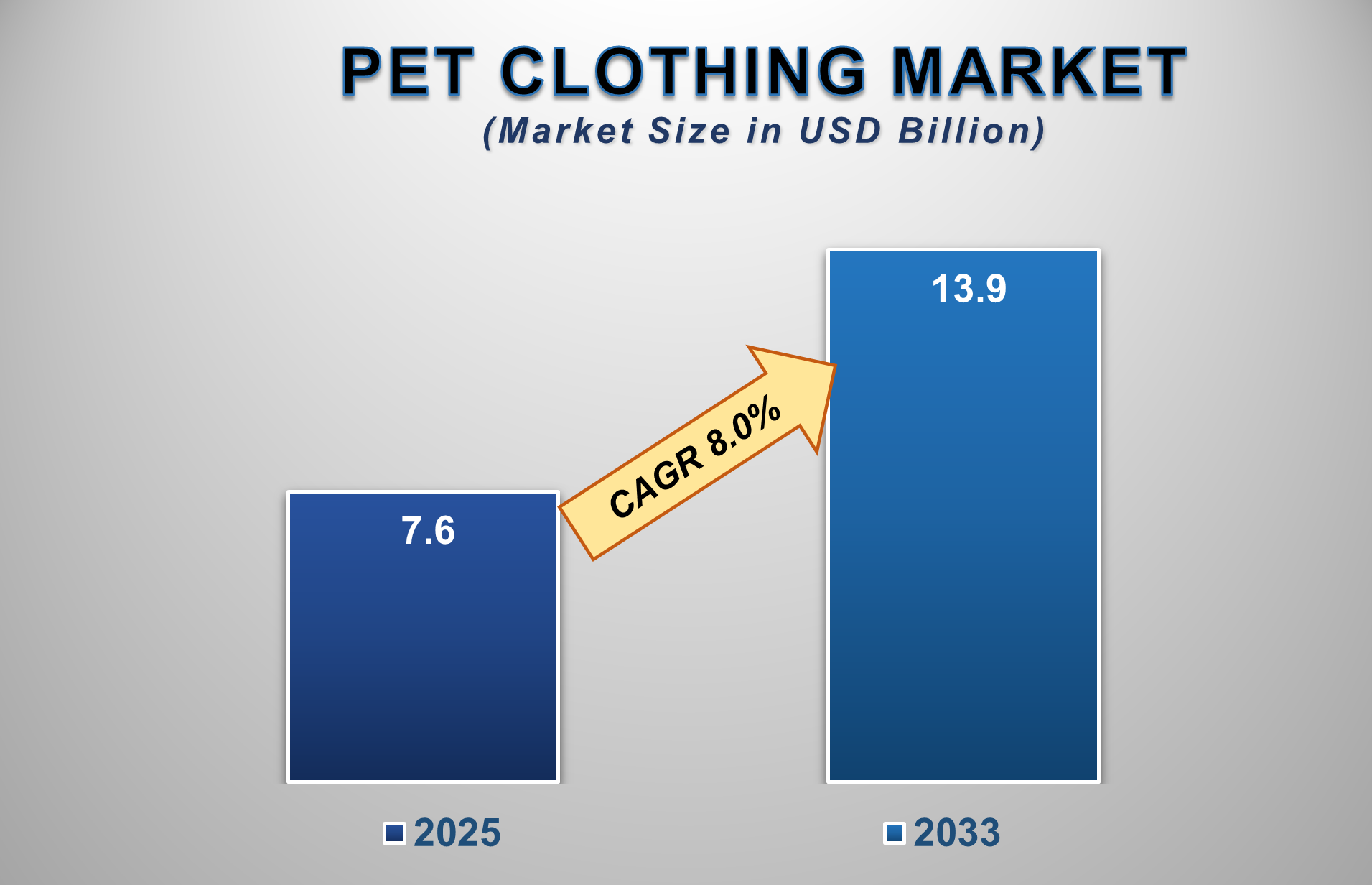

The Pet Clothing Market is poised for robust growth from 2025 to 2033, driven by the escalating trend of pet humanization, rising disposable income, and the growing perception of pets as family members. The market is projected to be valued at approximately USD 7.6 billion in 2025 and is forecasted to reach nearly USD 13.9 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.0% during this period.

Pet clothing encompasses a wide range of

products designed for companion animals, including functional apparel like

sweaters and raincoats, fashion-forward outfits, protective footwear, and

accessories such as hats and bandanas. The market's expansion is fueled by the

increasing number of pet owners who are willing to spend on premium products

for their pets' comfort, style, and well-being. Factors such as the growing

awareness of pet health (e.g., the need for protection from harsh weather,

allergens, and UV rays) and the influence of social media, where "pet

influencers" showcase trendy outfits, are significantly contributing to

market growth. North America currently holds the largest market share,

supported by high pet ownership rates and strong purchasing power, while the

Asia-Pacific region is expected to witness the fastest growth, fueled by

urbanization, westernization of pet care trends, and a burgeoning middle class.

Pet Clothing Market Drivers and Opportunities

The "Pet Humanization" Trend is the Primary Market

Driver

The "Pet Humanization" trend is the

dominant force propelling the global pet clothing market. This cultural shift,

where pets are increasingly viewed as sentient family members rather than mere

animals, has fundamentally altered consumer spending patterns. Owners now

project their own desires for comfort, style, and identity onto their pets,

driving demand for products that go beyond basic utility. This emotional

connection translates into a willingness to purchase seasonal fashion

collections, premium branded outfits, and functional apparel that mirrors human

clothing trends. The desire to provide the "best" for a beloved pet,

coupled with the social validation of sharing a well-dressed pet on platforms

like Instagram, creates a powerful and sustained demand for diverse and

innovative pet clothing.

A prime example of a company capitalizing on

this trend is Canada Pooch. The brand has built its entire identity

around solving pet problems with stylish, high-quality solutions that resonate

with discerning owners. Their products, such as the "Cedar Swirl

Snood" or the "Parka & Snow Boots" set, are marketed not

just as functional items for weather protection but as essential, fashionable gear for the modern, cared-for

pet. By focusing on design aesthetics, durable materials, and a brand voice

that understands the deep bond between owners and their dogs, Canada Pooch

effectively taps into the core of the pet humanization trend, positioning its

clothing as a natural extension of a loving owner's care.

Rising Disposable Income and Premiumization are Driving

Market Evolution

Increasing household disposable income,

particularly in developing economies, allows pet owners to allocate more funds

to non-essential and luxury pet products. This has led to the premiumization of

the market, with brands offering high-quality materials, designer

collaborations, and customized clothing options. The demand for durable,

comfortable, and aesthetically pleasing apparel is pushing manufacturers to

innovate in terms of design, fabric technology, and functionality, moving

beyond basic sweaters to a diverse portfolio of fashion-led and

performance-oriented products.

E-commerce Expansion and Niche Product Development Present

Significant Opportunities

The explosive growth of e-commerce presents a

massive opportunity for the pet clothing market. Online platforms offer a vast

selection, competitive pricing, and the convenience of home delivery, which is

particularly appealing for busy pet owners. Social media platforms like

Instagram and TikTok serve as powerful marketing tools, creating viral trends

and driving sales. Simultaneously, there is a significant opportunity in

developing niche products, such as clothing for specific dog breeds,

therapeutic wear for pets with allergies or anxiety (e.g., thunder shirts),

eco-friendly and sustainable clothing lines, and smart clothing integrated with

GPS or health monitoring sensors.

Pet Clothing Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 7.6 Billion |

|

Market Forecast in 2033 |

USD 13.9 Billion |

|

CAGR % 2025-2033 |

8.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Pet Type ●

By Material ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Pet Clothing Market Report Segmentation Analysis

The global Pet Clothing Market

industry analysis is segmented by Product Type, by Pet Type, by Material, by

Distribution Channel, and by Region.

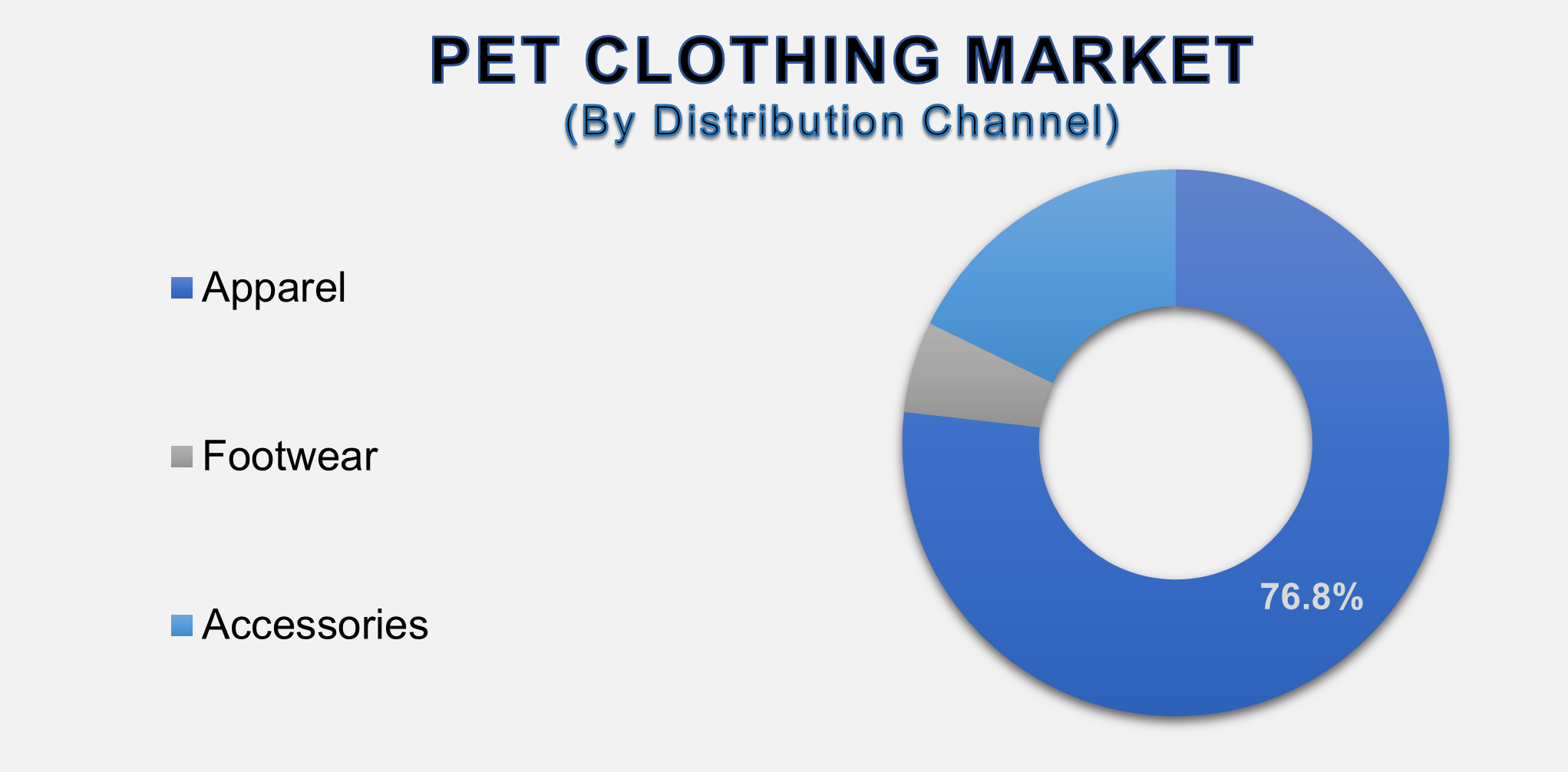

The Apparel segment is anticipated to command a dominant market share in 2025.

The

Product Type segment is categorized into Apparel, Footwear, and Accessories.

The Apparel segment commands a dominant market share, as it constitutes the

core category of pet clothing. This includes a wide variety of items such as

sweaters, jackets, dresses, t-shirts, and costumes. The high volume and repeat

purchase nature of apparel, driven by seasonal changes and fashion trends, solidifies its position as the largest revenue-generating segment.

While footwear and accessories are growing, they are often considered

complementary purchases to the main apparel item.

The Online Retail segment

is projected to be the key distribution channel.

The

Distribution Channel segment is divided into Specialty Stores, Online Retail,

and Hypermarkets/Supermarkets. The Online Retail segment is the dominant and

fastest-growing channel. The convenience of browsing extensive collections,

accessing customer reviews, and the ability to find unique or customized items

not available in brick-and-mortar stores make

online platforms the preferred shopping destination for pet owners. The visual

nature of pet clothing is also highly conducive to social media marketing and

influencer-driven sales, which are primarily channeled through online retail.

The Dogs segment is

projected to exhibit the strongest growth.

The Pet

Type segment includes Dogs, Cats, and Others. The Dogs segment exhibits the

strongest and most dominant growth. Dogs are the most common pets globally and

are more frequently dressed in clothing due to their size, varied breeds, and

higher tolerance for wearing apparel compared to cats. The vast array of dog

breeds also creates a diverse market for breed-specific clothing, functional

wear for outdoor activities, and a wide range of fashion items, making this

segment the primary driver of the market.

The following segments are

part of an in-depth analysis of the global Pet Clothing Market:

|

Market

Segments |

|

|

By Product

Type |

●

Apparel ●

Footwear ●

Accessories |

|

By Pet Type |

●

Dogs ●

Cats ●

Others |

|

By Material |

●

Cotton ●

Wool & Knits ●

Synthetic ●

Others |

|

By Distribution Channel |

●

Specialty Stores ●

Online Retail ●

Hypermarkets/Supermarkets

Online Pharmacies |

Pet Clothing Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Pet Clothing Market globally

throughout the forecast period.

North

America's dominance is attributed to its high rate of pet ownership, strong

consumer purchasing power, and the deeply entrenched trend of pet humanization.

The region has a mature retail landscape, including major pet specialty chains

and a robust e-commerce ecosystem, which makes premium pet clothing highly

accessible. High awareness of pet fashion trends and a culture of celebrating

pets with seasonal outfits and costumes further solidify North America's

position as the largest regional market.

In

addition, the Asia-Pacific region is expected

to be the fastest-growing market, driven by rapid urbanization, a growing

affinity for pet ownership, and the increasing influence of Western lifestyles.

The expanding middle class in countries like China and India, with rising

disposable incomes, is beginning to spend significantly on pet care and luxury

products. The proliferation of online shopping platforms and the power of

social media in setting trends are key accelerators of market growth in the

region.

Pet Clothing Market Competition Landscape

Analysis

The global pet clothing market

is highly fragmented and competitive, featuring a mix of specialized pet

apparel brands, large pet product corporations, and fast-fashion retailers

extending their lines to pets. The market includes everything from luxury designer

labels to affordable mass-market options. Competition is based on design

innovation, brand identity, material quality, pricing, and marketing reach. Key

strategies include celebrity endorsements, collaborations with fashion

designers, leveraging social media influencers, expanding product portfolios to

include sustainable options, and strengthening online and offline distribution

networks.

Global Pet Clothing

Market Recent Developments News:

- In March 2025, The Pet Fashion Group launched a new sustainable

collection made entirely from recycled ocean plastics, responding to

growing consumer demand for eco-friendly pet products.

- In January 2025, a collaboration between a major high-street fashion

brand and a popular pet influencer resulted in a limited-edition clothing

line that sold out online within hours.

- In November 2024, Ruffwear, a leader in performance dog gear,

introduced a new line of all-weather jackets with integrated LED safety

lights for nighttime visibility.

- In August 2024, Chewy.com expanded its private-label pet apparel

line, focusing on breed-specific fits and veterinarian-approved materials

for sensitive skin.

The Global Pet Clothing

Market Is Dominated by a Few Large Companies, such as

●

PetSmart Inc.

●

Petco Animal Supplies,

Inc.

●

LupinePet

●

Hurtta LLC

●

Mungo & Maud

●

Foggy Mountain Dog

Coats

●

Ralph Lauren

Corporation

●

Canada Pooch

●

Ruby Rufus

●

Weatherbeeta

●

Ultra Paws

●

Chilly Dogs

●

Equafleece Ltd.

●

RC Pet Products

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Pet Clothing Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Pet Clothing Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Mn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Pet Clothing Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Pet

Clothing Market

1.3.2.Pet Type of Global Pet

Clothing Market

1.3.3.Material of Global Pet

Clothing Market

1.3.4.Distribution Channel of Global

Pet Clothing Market

1.3.5.Region of Global Pet

Clothing Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Mn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Technological

Advancements

2.6.

Regulatory

Scenario by Region

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Pet Clothing Market Estimates

& Historical Trend Analysis (2020 – 2024)

4. Global

Pet Clothing Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Pet Clothing Market Revenue (US$ Mn) Estimates and Forecasts, by Product Type, 2020

- 2033

4.1.1.Apparel

4.1.2.Footwear

4.1.3.Accessories

5. Global

Pet Clothing Market Estimates

& Forecast Trend Analysis, by Pet Type

5.1.

Global

Pet Clothing Market Revenue (US$ Mn) Estimates and Forecasts, by Pet Type, 2020

- 2033

5.1.1.Dogs

5.1.2.Cats

5.1.3.Others

6. Global

Pet Clothing Market Estimates

& Forecast Trend Analysis, by Material

6.1.

Global

Pet Clothing Market Revenue (US$ Mn) Estimates and Forecasts, by Material 2020

- 2033

6.1.1.Cotton

6.1.2.Wool & Knits

6.1.3.Synthetic

6.1.4.Others

7. Global

Pet Clothing Market Estimates

& Forecast Trend Analysis, by Distribution Channel

7.1.

Global

Pet Clothing Market Revenue (US$ Mn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

7.1.1.Specialty Stores

7.1.2.Online Retail

7.1.3.Hypermarkets/Supermarkets

8. Global

Pet Clothing Market Estimates

& Forecast Trend Analysis, by region

8.1.

Global

Pet Clothing Market Revenue (US$ Mn) Estimates and Forecasts, by region, 2020 -

2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Pet

Clothing Market: Estimates &

Forecast Trend Analysis

9.1.

North

America Pet Clothing Market Assessments & Key Findings

9.1.1.North America Pet Clothing

Market Introduction

9.1.2.North America Pet Clothing

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Pet Type

9.1.2.3. By Material

9.1.2.4. By Distribution

Channel

9.1.2.5.

By

Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Pet

Clothing Market: Estimates &

Forecast Trend Analysis

10.1.

Europe

Pet Clothing Market Assessments & Key Findings

10.1.1.

Europe

Pet Clothing Market Introduction

10.1.2.

Europe

Pet Clothing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Pet Type

10.1.2.3. By Material

10.1.2.4. By

Distribution Channel

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Pet

Clothing Market: Estimates &

Forecast Trend Analysis

11.1.

Asia

Pacific Market Assessments & Key Findings

11.1.1.

Asia

Pacific Pet Clothing Market Introduction

11.1.2.

Asia

Pacific Pet Clothing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Pet Type

11.1.2.3. By Material

11.1.2.4. By

Distribution Channel

11.1.2.5.

By

Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Pet

Clothing Market: Estimates &

Forecast Trend Analysis

12.1.

Middle

East & Africa Market Assessments & Key Findings

12.1.1.

Middle East & Africa Pet Clothing Market Introduction

12.1.2.

Middle East & Africa Pet Clothing Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Pet Type

12.1.2.3. By Material

12.1.2.4. By

Distribution Channel

12.1.2.5.

By

Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Pet Clothing Market: Estimates &

Forecast Trend Analysis

13.1.

Latin

America Market Assessments & Key Findings

13.1.1.

Latin

America Pet Clothing Market Introduction

13.1.2.

Latin

America Pet Clothing Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1. By Product

Type

13.1.2.2. By Pet Type

13.1.2.3. By Material

13.1.2.4. By

Distribution Channel

13.1.2.5.

By

Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14. Country Wise Market:

Introduction

15.

Competition

Landscape

15.1.

Global

Pet Clothing Market Product Mapping

15.2.

Global

Pet Clothing Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

15.3.

Global

Pet Clothing Market Tier Structure Analysis

15.4.

Global

Pet Clothing Market Concentration & Company Market Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

PetSmart Inc.

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2. Petco Animal

Supplies, Inc.

16.3. LupinePet

16.4. Hurtta LLC

16.5. Mungo &

Maud

16.6. Foggy

Mountain Dog Coats

16.7. Ralph Lauren

Corporation

16.8. Canada Pooch

16.9. Ruby Rufus

16.10. Weatherbeeta

16.11. Ultra Paws

16.12. Chilly Dogs

16.13. Equafleece

Ltd.

16.14. RC Pet

Products

16.15. Other

Prominent Players

17. Research

Methodology

17.1.

External

Transportations / Databases

17.2.

Internal

Proprietary Database

17.3.

Primary

Research

17.4.

Secondary

Research

17.5.

Assumptions

17.6.

Limitations

17.7.

Report

FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables