Pharmaceutical Manufacturing Market Size and Forecast (2025 – 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Molecule Type (Biologics & Biosimilars, Monoclonal Antibodies, Vaccines, Cell & Gene Therapy, Others, Conventional Drugs); By Formulation (Tablets, Capsules, Injectables, Sprays, Suspensions, Powders, Other Formulations); By Route of Administration (Oral, Topical, Parenteral, Inhalations, Other Routes of Administration); By Therapy Area (Cardiovascular Diseases, Pain, Diabetes, Cancer, Respiratory Diseases, Other Diseases); By Prescription (Prescription Medicines, Over-the-counter Medicines); and Geography

2025-08-20

Healthcare

Swetal (Research Analyst)

Description

Pharmaceutical Manufacturing Market Overview

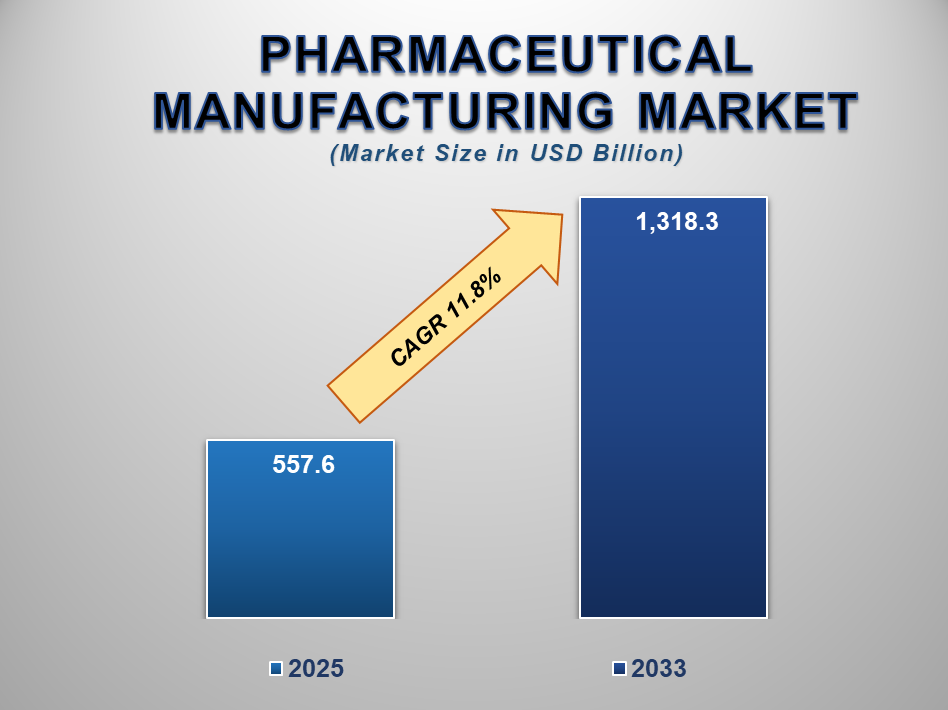

The global Pharmaceutical Manufacturing market size is projected to grow from USD 557.6 Billion in 2025 to USD 1,318.3 Billion by 2033, registering a strong CAGR of 11.8% over the forecast period. This rapid expansion is driven by technological innovation, increasing demand for biologics, biosimilars, and personalized medicine, and the continued prevalence of chronic diseases and infectious disorders globally.

Pharmaceutical manufacturing

includes the industrial-scale production of medications, from small-molecule

drugs to large complex biologics. Advances in bioprocessing, automation, and

continuous manufacturing have revolutionized how pharmaceuticals are developed

and produced. Additionally, digital transformation, AI, and data analytics are

streamlining R&D, improving batch consistency, and enhancing supply chain

agility. As regulatory authorities emphasize GMP compliance and fast-track

approvals, pharmaceutical companies are increasingly investing in flexible,

scalable, and quality-centric manufacturing systems. The market is also being

influenced by the expanding landscape of specialty drugs, growth in biosimilars

due to patent expirations, and increasing outsourcing of manufacturing services

by pharmaceutical firms to CMOs/CDMOs. With rising healthcare expenditure,

aging populations, and growing demand for novel treatments, pharmaceutical

manufacturing is poised to remain a critical enabler of global healthcare

systems.

Pharmaceutical

Manufacturing Market Drivers and Opportunities

The rising prevalence of chronic diseases and drug innovation

is anticipated to lift the Pharmaceutical Manufacturing market during the

forecast period

One of the key growth drivers for

the pharmaceutical manufacturing market is the rising global burden of chronic

diseases such as cancer, cardiovascular diseases, diabetes, and respiratory

conditions. These health challenges have led to a surge in demand for novel

therapies, including specialty drugs and biologics. Pharmaceutical companies

are under pressure to accelerate time-to-market while maintaining quality and

compliance, thus driving investments in advanced manufacturing infrastructure.

Additionally, the expansion of drug pipelines focused on autoimmune,

neurological, and rare diseases is increasing the complexity and scale of

pharmaceutical production. Targeted therapies, including monoclonal antibodies,

gene therapies, and immune-oncology drugs, require specialized manufacturing

environments. As research becomes more sophisticated, pharmaceutical

manufacturing must also evolve to support flexible, modular production systems.

This has created significant demand for single-use technologies, bioreactors,

smart automation, and continuous processing systems. These advancements are not

only improving yield and product quality but also enhancing operational

efficiency and scalability across the pharmaceutical value chain.

Technological innovation and automation in manufacturing

processes are anticipated to lift the Pharmaceutical Manufacturing market

during the forecast period

The pharmaceutical manufacturing

landscape is experiencing a wave of technological innovation, including smart

manufacturing, digital twins, AI-driven process analytics, and real-time

monitoring. These technologies allow for predictive maintenance, continuous

validation, and enhanced traceability, all while maintaining rigorous

regulatory compliance. Automation is minimizing human error, boosting output,

and facilitating precision in complex formulations and biologics processing.

Continuous manufacturing is becoming a preferred method over traditional batch

processing, enabling 24/7 production and minimizing downtime. In parallel,

machine learning and advanced robotics are being deployed in sterile

environments to ensure accuracy and safety. Additionally, innovations in

lyophilization, nanoparticle formulation, and 3D printing of dosage forms are

expanding the frontiers of pharmaceutical production. As manufacturers adopt

Industry 4.0 frameworks, they gain the ability to scale up rapidly, respond to

fluctuating demand, and reduce costs. This technological leap is proving

especially critical in vaccine production, oncology drug development, and

personalized therapies.

Opportunity for the Pharmaceutical Manufacturing Market

Rising outsourcing of manufacturing to CDMOs and expanding

biologics pipeline are poised to create significant opportunities in the

Pharmaceutical Manufacturing market

A major opportunity lies in the

increasing trend of outsourcing pharmaceutical manufacturing, Contract market, Development,

and Manufacturing Organizations (CDMOs). Faced with growing demand, cost

constraints, and a need to focus on core competencies like R&D and

commercialization, many pharmaceutical companies are partnering with CDMOs to

access state-of-the-art manufacturing capabilities without investing in large

capital projects. This model is particularly attractive for emerging biotech

firms and smaller pharma companies that lack in-house production

infrastructure. CDMOs offer end-to-end services including process development,

scale-up, regulatory support, and commercial manufacturing. As biologics and

biosimilars represent a growing share of the therapeutic landscape, CDMOs that

specialize in large molecule production are seeing increased demand. The

expansion of mRNA-based vaccines and cell & gene therapies further opens

doors for advanced CDMO capabilities. Geographically, countries like India,

South Korea, and Ireland are becoming major hubs for contract pharmaceutical

manufacturing due to skilled labor, cost advantages, and strong regulatory

environments. This trend is expected to significantly reshape global supply

chains and offer scalable opportunities for both established players and new

entrants.

Pharmaceutical Manufacturing Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 557.6 Billion |

|

Market Forecast in 2033 |

USD 1,318.3 Billion |

|

CAGR % 2025-2033 |

11.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

● By molecule type ●

By formulation ●

By route of administration ●

By therapy area ● By prescription |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Pharmaceutical Manufacturing Market Report Segmentation

Analysis

The global pharmaceutical

manufacturing market industry analysis is segmented by molecule type, by

formulation, by route of administration, by therapy area, by prescription type,

and by region.

The Biologics & Biosimilars segment accounted for the

largest market share in the global Pharmaceutical Manufacturing market

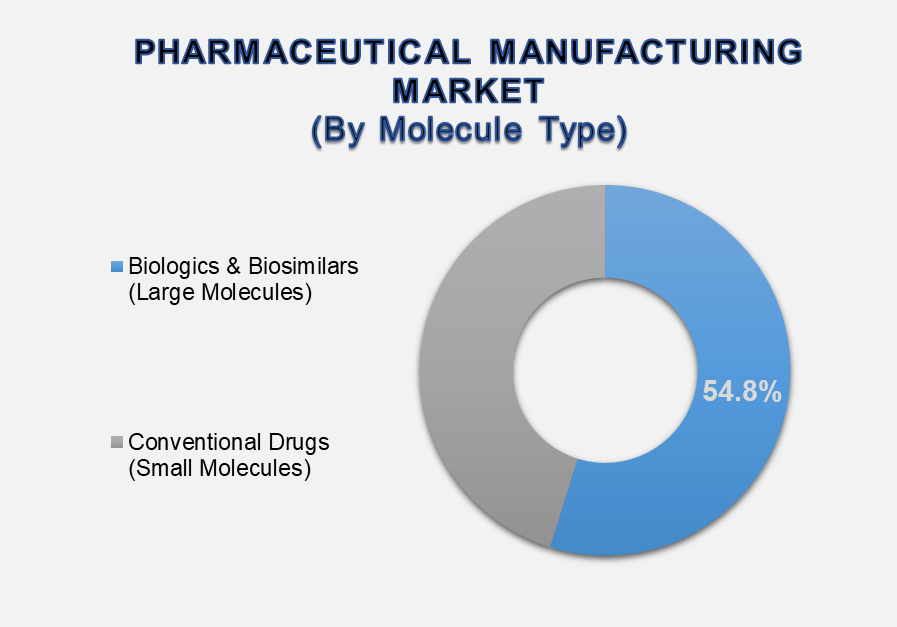

By Molecule Type, the market is segmented into Biologics & Biosimilars (Large Molecules) and Conventional Drugs (Small Molecules). In 2024, Biologics & Biosimilars held the dominant share at 54.8% owing to the rapid development of complex biologics such as monoclonal antibodies, cell & gene therapies, and recombinant proteins. These large-molecule drugs are used to treat various chronic and life-threatening conditions, including cancer, autoimmune disorders, and infectious diseases. As patents for originator biologics expire, the market for biosimilars is also growing rapidly, particularly in cost-sensitive regions.

The Tablets segment led the market in 2024 and is expected to

maintain dominance through the forecast period

By Formulation, Tablets accounted

for the largest share due to their stability, cost-effectiveness, ease of

administration, and wide application across therapy areas. However, there is

growing demand for advanced formulations like nanoparticle-based tablets,

controlled-release systems, and fixed-dose combinations.

The Oral segment dominated in 2024 and continues to be the

preferred route of administration

By Route of Administration, Oral

remains the most preferred route owing to patient convenience and compatibility

with a wide range of formulations. It is followed by parenteral routes,

especially for biologics, where injectable formats are crucial for drugs

requiring systemic delivery.

The following segments are part

of an in-depth analysis of the global Pharmaceutical Manufacturing Market:

|

Market Segments |

|

|

By Molecule Type |

●

Biologics &

Biosimilars (Large Molecules) o

Monoclonal

Antibodies o

Vaccines o

Cell & Gene

Therapy o

Others ●

Conventional Drugs

(Small Molecules) |

|

By Formulation |

●

Tablets ●

Capsules ●

Injectable ●

Sprays ●

Suspensions ●

Powders ●

Other Formulations |

|

By Route Of Administration |

●

Oral ●

Topical ●

Parenteral ●

Inhalations ●

Other Routes Of

Administration |

|

By Therapy Area |

●

Cardiovascular

Diseases (CVDs) ●

Pain ●

Diabetes ●

Cancer ●

Respiratory Diseases ●

Other Diseases |

|

By Prescription |

●

Prescription

Medicines ●

Over-The-Counter

(OTC) Medicines |

Pharmaceutical

Manufacturing Market Share Analysis by Region

Asia Pacific is projected to dominate the global

Pharmaceutical Manufacturing market over the forecast period

Asia Pacific is expected to

account for the largest share of the global pharmaceutical manufacturing market

over the forecast period. This dominance is attributed to the region’s

expanding pharmaceutical industry, availability of cost-efficient manufacturing

infrastructure, and favorable government policies. Countries such as China,

India, South Korea, and Singapore are becoming major pharmaceutical

manufacturing hubs due to their skilled labor pool, compliance with

international standards (e.g., US FDA, EMA), and strong investments in

industrial clusters. India, for instance, is the world’s largest supplier of

generic drugs and vaccines and is rapidly expanding its API and biosimilar

manufacturing capabilities. China continues to lead in active pharmaceutical

ingredient (API) production, with significant investments in biologics

manufacturing facilities. Public-private partnerships, production-linked

incentive (PLI) schemes, and foreign direct investments are further enhancing

capacity in the region. Additionally, domestic consumption is rising sharply

due to growing healthcare access, aging populations, and increasing chronic

disease prevalence.

North America remains a vital

market driven by advanced infrastructure, a strong R&D ecosystem, and early

adoption of innovative manufacturing technologies. The United States is a key

hub for biologics, mRNA therapeutics, and personalized medicine production.

High pharmaceutical spending, favorable regulatory pathways, and the presence

of leading global pharma giants support regional growth. Canada also

contributes with a strong CDMO network and government incentives for

pharmaceutical innovation and scale-up.

Pharmaceutical Manufacturing Market Competition Landscape

Analysis

The global

Pharmaceutical Manufacturing market is highly competitive and fragmented,

comprising large pharmaceutical firms with in-house manufacturing capabilities,

as well as specialized CDMOs serving different molecule classes and formulation

types. Companies are investing in expanding biologics and cell therapy

capacity, digitizing facilities, and forming strategic alliances to accelerate

speed-to-market.

Global Pharmaceutical

Manufacturing Market Recent Developments News:

- In May 2025 – Genentech announced a USD 700 million

investment to build a 700,000 sq. ft. drug manufacturing facility in Holly

Springs, North Carolina, creating 400 manufacturing and 1,500 construction

jobs to support its metabolic medicines portfolio.

- In May 2025 – Gilead Sciences committed USD 32

billion toward U.S. manufacturing and R&D expansion through 2030,

projected to generate USD 43 billion in economic impact and create 3,000+

jobs by 2028.

- In April 2025 – Roche unveiled a USD 50 billion,

5-year U.S. investment plan for pharmaceuticals and diagnostics, including

new R&D and manufacturing sites across 8 states, with 12,000+ new

jobs.

- In April 2025 – Novartis pledged USD 23 billion over 5 years to

expand U.S. operations, adding 10 facilities (including 7 new sites) for

API, biologics, and radioligand therapy production.

The Global Pharmaceutical

Manufacturing Market is dominated by a few large companies, such as

●

Pfizer

●

Novartis

●

Roche (Genentech)

●

Johnson & Johnson

(Janssen)

●

Merck & Co. (MSD)

●

GlaxoSmithKline (GSK)

●

Sanofi

●

AstraZeneca

●

Bristol Myers Squibb

(BMS)

●

Eli Lilly

●

AbbVie

●

Takeda Pharmaceutical

●

Gilead Sciences

●

Amgen

●

Moderna

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

- Global Pharmaceutical Manufacturing Market Introduction and Market Overview

- Objectives of the Study

- Global Pharmaceutical Manufacturing Market Scope and Market Estimation

- Global Pharmaceutical Manufacturing Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Pharmaceutical Manufacturing Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Molecule Type of Global Pharmaceutical Manufacturing Market

- Formulation of Global Pharmaceutical Manufacturing Market

- Route of Administration of Global Pharmaceutical Manufacturing Market

- Therapy Area of Global Pharmaceutical Manufacturing Market

- Prescription of Global Pharmaceutical Manufacturing Market

- Region of Global Pharmaceutical Manufacturing Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Pharmaceutical Manufacturing Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Pharmaceutical Manufacturing Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Molecule Type

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Molecule Type, 2021 - 2033

- Biologics & Biosimilars (Large Molecules)

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapy

- Others

- Conventional Drugs (Small Molecules)

- Biologics & Biosimilars (Large Molecules)

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Molecule Type, 2021 - 2033

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Formulation

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Formulation, 2021 - 2033

- Tablets

- Capsules

- Injectable

- Sprays

- Suspensions

- Powders

- Other Formulations

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Formulation, 2021 - 2033

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Route of Administration

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Route of Administration, 2021 - 2033

- Oral

- Topical

- Parenteral

- Inhalations

- Other Routes of Administration

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Route of Administration, 2021 - 2033

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Therapy Area

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Therapy Area, 2021 - 2033

- Cardiovascular Diseases (CVDs)

- Pain

- Diabetes

- Cancer

- Respiratory Diseases

- Other Diseases

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Therapy Area, 2021 - 2033

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Prescription

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Prescription, 2021 - 2033

- Prescription Medicines

- Over-the-counter (OTC) Medicines

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Prescription, 2021 - 2033

- Global Pharmaceutical Manufacturing Market Estimates & Forecast Trend Analysis, by Region

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Pharmaceutical Manufacturing Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2021 - 2033

- North America Pharmaceutical Manufacturing Market: Estimates & Forecast Trend Analysis

- North America Pharmaceutical Manufacturing Market Assessments & Key Findings

- North America Pharmaceutical Manufacturing Market Introduction

- North America Pharmaceutical Manufacturing Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Molecule Type

- By Formulation

- By Route of Administration

- By Therapy Area

- By Prescription

- By Country

- The U.S.

- Canada

- North America Pharmaceutical Manufacturing Market Assessments & Key Findings

- Europe Pharmaceutical Manufacturing Market: Estimates & Forecast Trend Analysis

- Europe Pharmaceutical Manufacturing Market Assessments & Key Findings

- Europe Pharmaceutical Manufacturing Market Introduction

- Europe Pharmaceutical Manufacturing Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Molecule Type

- By Formulation

- By Route of Administration

- By Therapy Area

- By Prescription

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Pharmaceutical Manufacturing Market Assessments & Key Findings

- Asia Pacific Pharmaceutical Manufacturing Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Pharmaceutical Manufacturing Market Introduction

- Asia Pacific Pharmaceutical Manufacturing Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Molecule Type

- By Formulation

- By Route of Administration

- By Therapy Area

- By Prescription

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Pharmaceutical Manufacturing Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Pharmaceutical Manufacturing Market Introduction

- Middle East & Africa Pharmaceutical Manufacturing Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Molecule Type

- By Formulation

- By Route of Administration

- By Therapy Area

- By Prescription

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Pharmaceutical Manufacturing Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Pharmaceutical Manufacturing Market Introduction

- Latin America Pharmaceutical Manufacturing Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Molecule Type

- By Formulation

- By Route of Administration

- By Therapy Area

- By Prescription

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Pharmaceutical Manufacturing Market Product Mapping

- Global Pharmaceutical Manufacturing Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Pharmaceutical Manufacturing Market Tier Structure Analysis

- Global Pharmaceutical Manufacturing Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Pfizer

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Pfizer

* Similar details would be provided for all the players mentioned below

- Novartis

- Roche (Genentech)

- Johnson & Johnson (Janssen)

- Merck & Co. (MSD)

- GlaxoSmithKline (GSK)

- Sanofi

- AstraZeneca

- Bristol Myers Squibb (BMS)

- Eli Lilly

- AbbVie

- Takeda Pharmaceutical

- Gilead Sciences

- Amgen

- Moderna

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables