Pharmaceutical Packaging Market Size and Forecast (2026 – 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Product Type (Primary Packaging, Secondary Packaging, and Tertiary Packaging); By Material (Plastics & Polymers, Glass, Paper & Paperboard, Aluminum Foil, and Others); By Drug Delivery Mode (Oral Drugs, Injectable Drugs, Topical Drugs, and Others); By End-use (Pharmaceutical Manufacturing Companies, Contract Packaging Organizations, and Research Laboratories) and Geography

2026-04-02

Healthcare

Swetal (Research Analyst)

Description

Pharmaceutical Packaging Market Overview

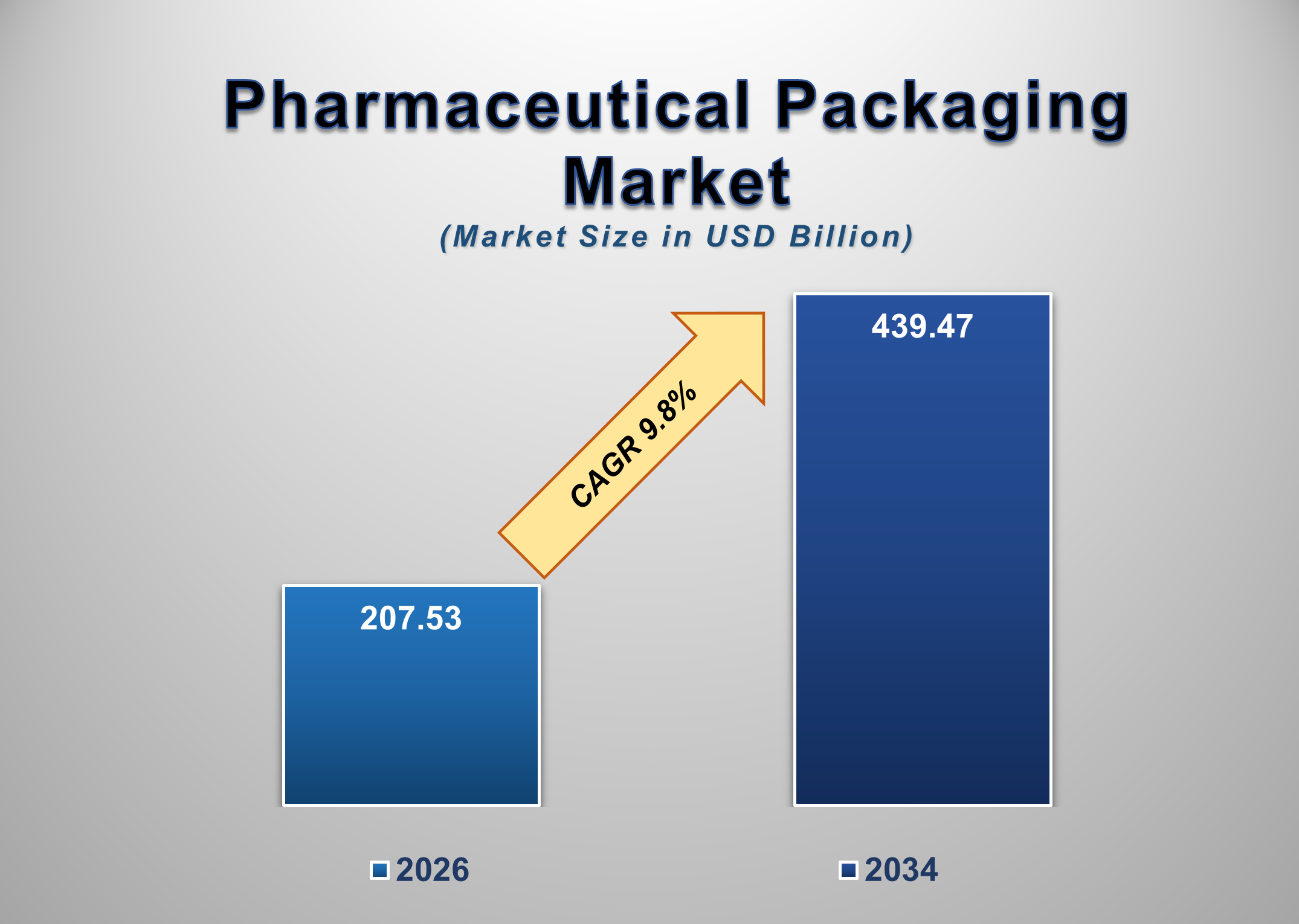

The global Pharmaceutical Packaging Market is witnessing substantial growth due to the increasing demand for safe, reliable, and efficient packaging solutions in the pharmaceutical industry. The market is estimated to reach USD 207.53 billion in 2026 and is projected to grow to USD 439.47 billion by 2034, registering a compound annual growth rate (CAGR) of 9.8% during the forecast period. Rising pharmaceutical production, increasing demand for biologics and specialty drugs, and stringent regulatory requirements regarding drug safety and packaging standards are among the key factors supporting the growth of the pharmaceutical packaging industry.

Pharmaceutical packaging plays a critical role in ensuring the safety, stability, and integrity of medicinal products throughout their lifecycle. Packaging systems protect pharmaceutical products from environmental factors such as moisture, oxygen, contamination, and physical damage. They also provide essential information related to drug dosage, expiration dates, and handling instructions, which helps healthcare professionals and patients use medications safely and effectively.

The pharmaceutical industry relies on multiple layers of packaging, including primary packaging that directly contacts the drug product, secondary packaging used for labeling and product identification, and tertiary packaging designed for transportation and bulk handling. These packaging solutions must comply with strict regulatory standards established by healthcare authorities to ensure patient safety and maintain product quality.

In recent years, pharmaceutical packaging technologies have evolved significantly to address the increasing complexity of modern medicines. Advanced packaging solutions such as tamper-evident packaging, child-resistant containers, and smart packaging systems are becoming widely adopted across the pharmaceutical sector. Additionally, the rapid growth of biologic drugs, vaccines, and injectable medications is increasing demand for specialized packaging formats such as vials, ampoules, and prefilled syringes. As global pharmaceutical production continues to expand, the demand for innovative packaging solutions is expected to grow steadily.

Pharmaceutical Packaging Market Drivers and Opportunities

Expanding Pharmaceutical Manufacturing Industry Drives Market Growth

One of the primary drivers of the pharmaceutical packaging market is the continuous expansion of global pharmaceutical manufacturing activities. The increasing prevalence of chronic diseases, growing aging populations, and rising healthcare expenditures have significantly increased the demand for pharmaceutical products worldwide. As pharmaceutical companies scale up production to meet rising healthcare needs, the requirement for high-quality packaging solutions has also increased.

Pharmaceutical packaging serves multiple functions beyond product containment. It ensures drug stability, prevents contamination, and facilitates safe transportation from manufacturing facilities to healthcare providers and patients. As pharmaceutical companies develop new drug formulations and advanced therapeutic products, packaging technologies must evolve to meet specialized storage and handling requirements.

Furthermore, the growth of generic drug manufacturing is contributing to increased demand for pharmaceutical packaging materials. Generic drug manufacturers require cost-effective yet reliable packaging solutions that comply with regulatory standards while maintaining product quality. As global demand for pharmaceutical products continues to rise, packaging manufacturers are expanding their production capabilities to meet industry requirements.

Stringent Regulatory Standards Increase Demand for Advanced Packaging Solutions

Another major factor driving the pharmaceutical packaging market is the implementation of strict regulatory guidelines governing drug packaging and labeling. Healthcare authorities such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other regulatory bodies worldwide enforce rigorous packaging standards to ensure drug safety and prevent counterfeit pharmaceutical products from entering the supply chain.

Pharmaceutical packaging must meet specific requirements related to tamper resistance, child safety, product identification, and traceability. As a result, pharmaceutical companies are increasingly adopting advanced packaging technologies that enhance product security and compliance with regulatory regulations.

Tamper-evident packaging systems, serialization technologies, and track-and-trace solutions are becoming widely implemented to combat counterfeit drugs and improve supply chain transparency. These technologies allow manufacturers and regulatory authorities to monitor the movement of pharmaceutical products throughout the distribution network, thereby ensuring product authenticity and patient safety.

Emergence of Smart and Sustainable Packaging Technologies Creates Opportunities

Technological innovations in packaging materials and design are creating significant growth opportunities within the pharmaceutical packaging market. The emergence of smart packaging solutions is enabling pharmaceutical companies to integrate digital technologies into traditional packaging systems. Smart packaging features such as temperature sensors, RFID tags, and digital tracking systems allow pharmaceutical companies to monitor product conditions during storage and transportation.

These technologies are particularly important for temperature-sensitive drugs such as biologics and vaccines that require strict cold chain management. Smart packaging solutions can provide real-time monitoring of environmental conditions, ensuring that pharmaceutical products remain within safe storage limits throughout the distribution process.

In addition to technological advancements, sustainability is becoming a major focus within the pharmaceutical packaging industry. Packaging manufacturers are increasingly developing eco-friendly packaging materials that reduce environmental impact while maintaining product safety and durability. Recyclable materials, biodegradable packaging solutions, and reduced packaging waste are becoming important priorities for pharmaceutical companies seeking to improve environmental sustainability.

Pharmaceutical Packaging Market Scope

Pharmaceutical Packaging Market Report Segmentation Analysis

The global pharmaceutical packaging market industry analysis is segmented based on product type, packaging material, drug delivery mode, end-use industry, and geographical region.

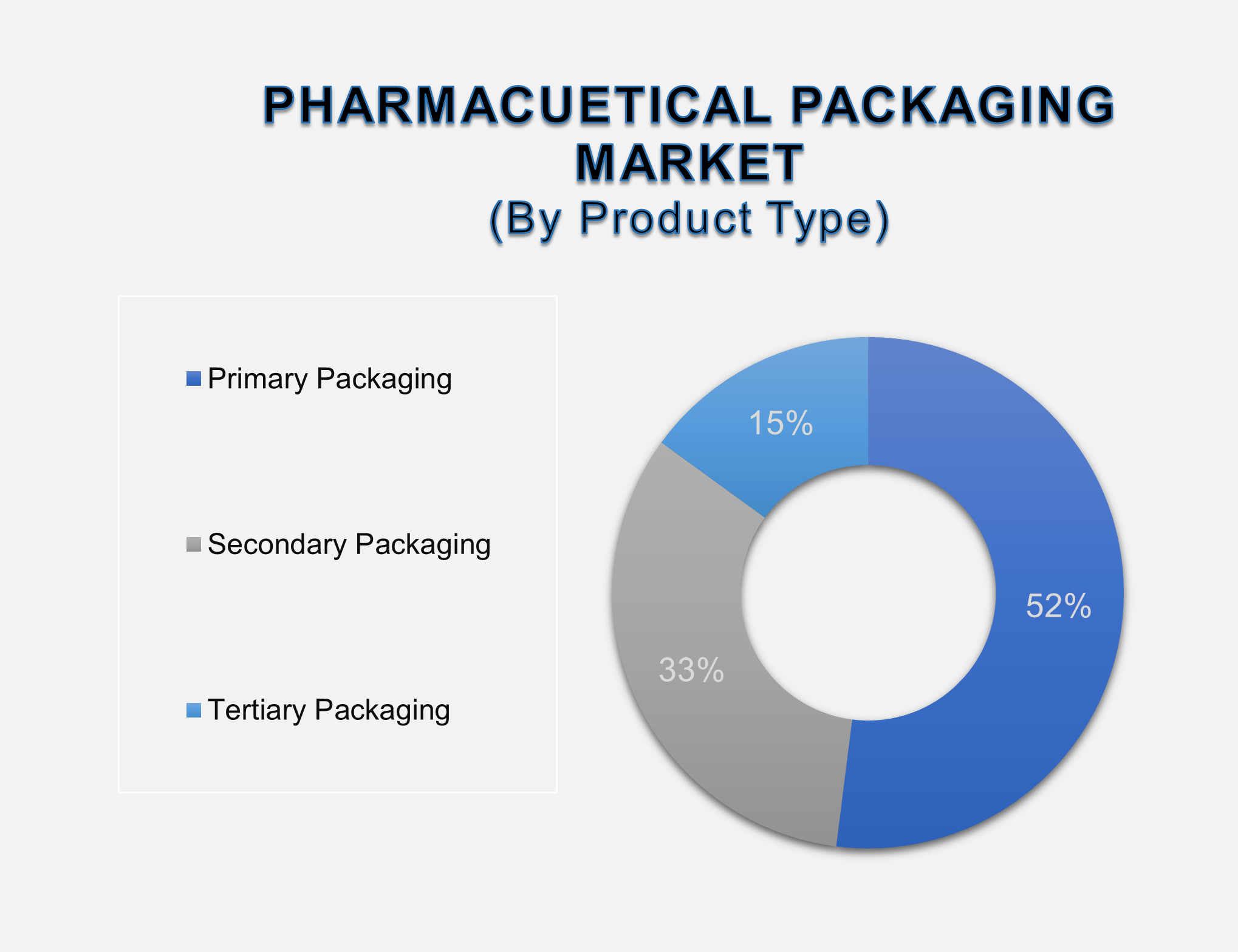

Primary Packaging Segment Holds Major Market Share

Based on product type, the market is segmented into primary packaging, secondary packaging, and tertiary packaging. Among these, primary packaging holds a significant share of the market because it directly contacts the pharmaceutical product and plays a crucial role in maintaining drug stability and safety.

Primary packaging solutions include blister packs, bottles, vials, ampoules, and prefilled syringes. These packaging formats are widely used across pharmaceutical manufacturing operations to protect drug products from contamination and environmental exposure.

Plastics and Polymers Segment Dominates Material Market

Based on material type, the market is categorized into plastics & polymers, glass, paper & paperboard, aluminum foil, and others. Plastics and polymers represent the dominant material segment due to their versatility, durability, and cost-effectiveness.

Plastic packaging materials are widely used in pharmaceutical packaging because they provide lightweight and durable solutions suitable for large-scale manufacturing and transportation. Plastic bottles, blister packaging, and plastic containers are commonly used for oral drug formulations and over-the-counter medications.

Pharmaceutical Manufacturing Companies Lead End-Use Markets

Based on end-use, the pharmaceutical packaging market is segmented into pharmaceutical manufacturing companies, contract packaging organizations, and research laboratories. Pharmaceutical manufacturing companies account for the largest share because they require large volumes of packaging materials for commercial drug production.

Pharmaceutical companies collaborate with packaging suppliers to develop packaging systems that comply with regulatory standards while ensuring product safety and efficient distribution.

Pharmaceutical Packaging Market Share Analysis by Region

North America currently holds a significant share of the global pharmaceutical packaging market due to the presence of major pharmaceutical manufacturers and advanced healthcare infrastructure. The United States represents a major hub for pharmaceutical innovation and drug production, which drives demand for advanced packaging technologies.

Europe also represents a strong market for pharmaceutical packaging solutions due to strict regulatory standards and well-established pharmaceutical industries in countries such as Germany, Switzerland, and the United Kingdom.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Rapid expansion of pharmaceutical manufacturing activities in countries such as China and India, along with increasing healthcare investments, is contributing to rising demand for pharmaceutical packaging solutions across the region.

Global Pharmaceutical Packaging Market: Recent Developments News

● In February 2025, Amcor announced new recyclable pharmaceutical packaging solutions designed to reduce environmental impact.

● In October 2024, Gerresheimer expanded its production facilities for pharmaceutical glass packaging to support increasing demand for injectable drug containers.

● In June 2024, Berry Global launched innovative pharmaceutical plastic packaging products designed to improve product safety and sustainability.

Competitive Landscape

Major companies operating in the global Pharmaceutical Packaging Market include:

● Amcor plc

● Gerresheimer AG

● Berry Global Inc.

● West Pharmaceutical Services Inc.

● AptarGroup Inc.

● Schott AG

● Becton Dickinson and Company

● CCL Industries

● Catalent Inc.

● Nipro Corporation

● SGD Pharma

● WestRock Company

● Sonoco Products Company

● Constantia Flexibles

● Uflex Limited

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

Global Pharmaceutical Packaging Market Introduction and Market Overview

Objectives of the Study

Global Pharmaceutical Packaging Market Scope and Market Estimation

Global Pharmaceutical Packaging Market Size (US$ Bn), CAGR (%), Forecast (2025 - 2033)

Global Pharmaceutical Packaging Market Revenue Share (%) and Y-o-Y Growth (2020 - 2033)

Market Segmentation

Product Type of Global Pharmaceutical Packaging Market

Material of Global Pharmaceutical Packaging Market

Drug Delivery Mode of Global Pharmaceutical Packaging Market

End Use of Global Pharmaceutical Packaging Market

Region of Global Pharmaceutical Packaging Market

Competition Coverage List of Market Participants

Market Definition: Pharmaceutical Packaging Market

Executive Summary

Demand Side Trends

Key Market Trends

Market Revenue (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

Demand and Opportunity Assessment

Key Developments

Overview of Tariff, Regulatory Landscape and Standards

Market Entry Strategies

Market Dynamics

Drivers

Limitations

Opportunities

Impact Analysis

Porter’s Five Forces Analysis

PEST Analysis

Global Pharmaceutical Packaging Market Historical Analysis (2020 - 2024)

Global Pharmaceutical Packaging Market Forecast Analysis (2025 - 2033), by Product Type

Revenue Estimates & Forecast (US$ Bn), 2020 - 2033

Primary Packaging

Secondary Packaging

Tertiary Packaging

Global Pharmaceutical Packaging Market Forecast Analysis, by Material

Revenue Estimates & Forecast (US$ Bn), 2020 - 2033

Plastics & Polymers

Glass

Paper & Paperboard

Aluminum Foil

Others

Global Pharmaceutical Packaging Market Forecast Analysis, by Drug Delivery Mode

Revenue Estimates & Forecast (US$ Bn), 2020 - 2033

Oral Drugs

Injectable Drugs

Topical Drugs

Others

Global Pharmaceutical Packaging Market Forecast Analysis, by End Use

Revenue Estimates & Forecast (US$ Bn), 2020 - 2033

Pharmaceutical Manufacturing Companies

Contract Packaging Organizations

Research Laboratories

Global Pharmaceutical Packaging Market Forecast Analysis, by Region

Revenue Estimates & Forecast (US$ Bn), 2020 - 2033

North America

Europe

Asia Pacific

Middle East & Africa

Latin America

North America Pharmaceutical Packaging Market Analysis

Market Overview

Market Size Forecast (2020 - 2033)

By Product Type

By Material

By Drug Delivery Mode

By End Use

By Country

U.S.

Canada

Europe Pharmaceutical Packaging Market Analysis

Market Overview

Market Size Forecast (2020 - 2033)

By Product Type

By Material

By Drug Delivery Mode

By End Use

By Country

Germany

U.K.

France

Italy

Spain

Switzerland

Rest of Europe

Asia Pacific Pharmaceutical Packaging Market Analysis

Market Overview

Market Size Forecast (2020 - 2033)

By Product Type

By Material

By Drug Delivery Mode

By End Use

By Country

China

India

Japan

South Korea

Australia

Rest of Asia Pacific

Middle East & Africa Pharmaceutical Packaging Market Analysis

Market Overview

Market Size Forecast (2020 - 2033)

By Product Type

By Material

By Drug Delivery Mode

By End Use

By Country

UAE

Saudi Arabia

South Africa

Rest of MEA

Latin America Pharmaceutical Packaging Market Analysis

Market Overview

Market Size Forecast (2020 - 2033)

By Product Type

By Material

By Drug Delivery Mode

By End Use

By Country

Brazil

Mexico

Argentina

Rest of LATAM

Country Wise Market Analysis

Competitive Landscape

Product Mapping

Market Share Analysis (2024)

Tier Structure Analysis

Competitive Benchmarking

Company Profiles

Amcor plc

Company Overview

Financial Performance

Product Portfolio

SWOT Analysis

Recent Developments

Gerresheimer AG

Berry Global Inc.

West Pharmaceutical Services Inc.

AptarGroup Inc.

Schott AG

Becton Dickinson and Company

CCL Industries

Catalent Inc.

Nipro Corporation

SGD Pharma

WestRock Company

Sonoco Products Company

Constantia Flexibles

Uflex Limited

Others

Research Methodology

Primary Research

Secondary Research

Data Triangulation

Market Estimation

Assumptions

Limitations

FAQs

Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables