Pharmacovigilance Market Size and Forecast (2020 - 2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Service Provider (In-House, Contract Outsourcing), By Product Life Cycle (Pre-Clinical, Phase I, Phase II, Phase III, Phase IV), By Type (Spontaneous Reporting, Intensified ADR Reporting, Targeted Spontaneous Reporting, Cohort Event Monitoring, EHR Mining), By End-User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Companies, CROs) And Geography

2025-11-20

Healthcare

Swetal (Research Analyst)

Description

Pharmacovigilance Market Overview

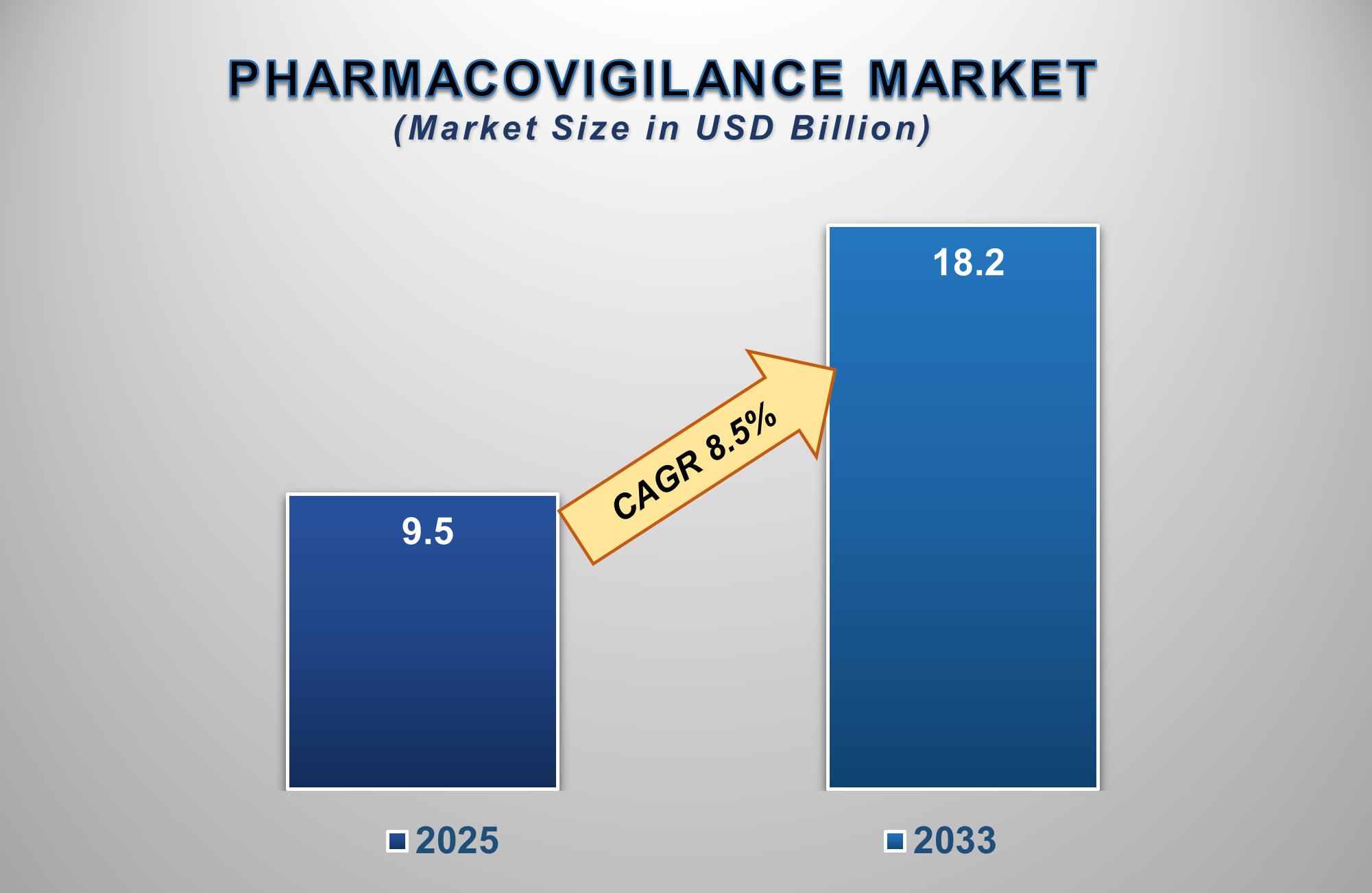

The Pharmacovigilance (PV) Market is positioned for a period of sustained and critical growth from 2025 to 2033, driven by the escalating complexity of drug development, a global increase in pharmaceutical consumption, and stringent regulatory mandates for drug safety monitoring. The market is projected to be valued at approximately USD 9.5 billion in 2025 and is forecasted to reach nearly USD 18.2 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 8.6% during this period.

Pharmacovigilance encompasses the science and activities relating to the detection, assessment, understanding, and prevention of adverse effects or any other drug-related problems. The market's robust expansion is primarily fueled by the rising number of new drug approvals, including complex biologics and specialty therapies, which require intensive, long-term safety monitoring. The growing adoption of outsourcing by pharmaceutical and biotechnology companies to specialized Contract Research Organizations (CROs) is a significant contributor, as it offers cost-efficiency and access to expert resources. Furthermore, technological advancements, particularly the integration of Artificial Intelligence (AI) and machine learning for signal detection and the analysis of real-world data (RWD), are reshaping the market landscape. North America currently holds the largest market share due to its well-established regulatory framework and high R&D expenditure, while the Asia-Pacific region is expected to witness the fastest growth, driven by expanding clinical trial activities and evolving regulatory standards.

Pharmacovigilance

Market Drivers and Opportunities

The Rising Burden of Adverse Drug Reactions

and Stringent Global Regulations is the Primary Market Driver

The increasing global focus on patient safety

and the significant clinical and economic burden of Adverse Drug Reactions

(ADRs) are the most powerful forces propelling the pharmacovigilance market.

Regulatory bodies like the FDA (U.S.), EMA (Europe), and others have

implemented rigorous and continuously evolving post-marketing surveillance

requirements. The mandate for Risk Evaluation and Mitigation Strategies (REMS),

Periodic Benefit-Risk Evaluation Reports (PBRERs), and stringent

pharmacovigilance inspections compels life sciences companies to invest heavily

in robust PV systems. The high cost of drug recalls and litigation related to

safety issues further incentivizes proactive investment in comprehensive

pharmacovigilance practices. This regulatory environment ensures that

pharmacovigilance is not an optional function but a critical, integral

component of the entire drug lifecycle, providing a solid foundation for

sustained market expansion.

The Increasing Complexity of Therapeutics and

Outsourcing Trends is Driving Adoption

The pharmaceutical pipeline is increasingly

dominated by complex molecules, including biologics, biosimilars, cell and gene

therapies, and orphan drugs. These advanced therapies often have novel

mechanisms of action and unknown long-term safety profiles, necessitating more

sophisticated and specialized pharmacovigilance expertise. Concurrently, a

paradigm shift towards outsourcing PV activities to CROs is a powerful

catalyst. Pharmaceutical companies are leveraging the expertise, technological

infrastructure, and geographic reach of CROs to manage costs, increase

operational flexibility, and navigate diverse international regulatory

landscapes. This allows sponsors to focus on core R&D while ensuring

compliance. The convergence of complex drug development and the strategic

outsourcing model is driving the adoption of advanced pharmacovigilance

services across the industry.

The Advent of Advanced Analytics and Digital

Health Technologies Presents Significant

Opportunities

The strategic integration of advanced

technologies and the explosion of digital health data are creating significant

growth frontiers for the pharmacovigilance market. The application of AI,

machine learning, and Natural Language Processing (NLP) allows for the

automated processing of vast datasets from sources like electronic health

records (EHRs), social media, and literature, enabling faster and more accurate

signal detection. Furthermore, the rise of wearable devices and mobile health

applications provide a continuous stream of

real-world data, offering unprecedented insights into drug safety in a

patient's natural environment. For PV service providers, developing expertise

in these advanced analytics and forging partnerships with health tech companies

are key strategies. Leveraging these technologies enables a shift from a

reactive to a proactive, predictive safety model, representing a massive

opportunity to enhance drug safety and create significant value for the

industry.

Pharmacovigilance Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 9.5 Billion |

|

Market Forecast in 2033 |

USD 18.2 Billion |

|

CAGR % 2025-2033 |

8.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Service

Provider ●

By Product Life

Cycle ●

By Type ●

By End-user |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Pharmacovigilance Market

Report Segmentation Analysis

The global Pharmacovigilance

Market industry analysis is segmented by Service Provider, by Product Life

Cycle, by Type, by End-User, and by region.

The Contract Outsourcing

service provider segment is anticipated to command the largest market share in

2025

The dominance of the contract outsourcing segment

is intrinsic to its role as the primary strategic partner for pharmaceutical

and biotech companies seeking operational efficiency and specialized expertise.

Outsourcing to CROs allows sponsors to convert fixed internal costs into

variable costs, providing significant financial flexibility. This model grants

access to a global talent pool of PV professionals and advanced technological

platforms without the need for substantial capital investment. Furthermore,

CROs offer scalability to manage fluctuating workloads, particularly during

peak periods such as drug launches or in response to safety alerts. The ability

of CROs to navigate complex, multi-regional regulatory requirements makes them

an indispensable partner for companies with global ambitions. This combination

of cost-effectiveness, scalability, and specialized expertise solidifies the

segment's largest market share.

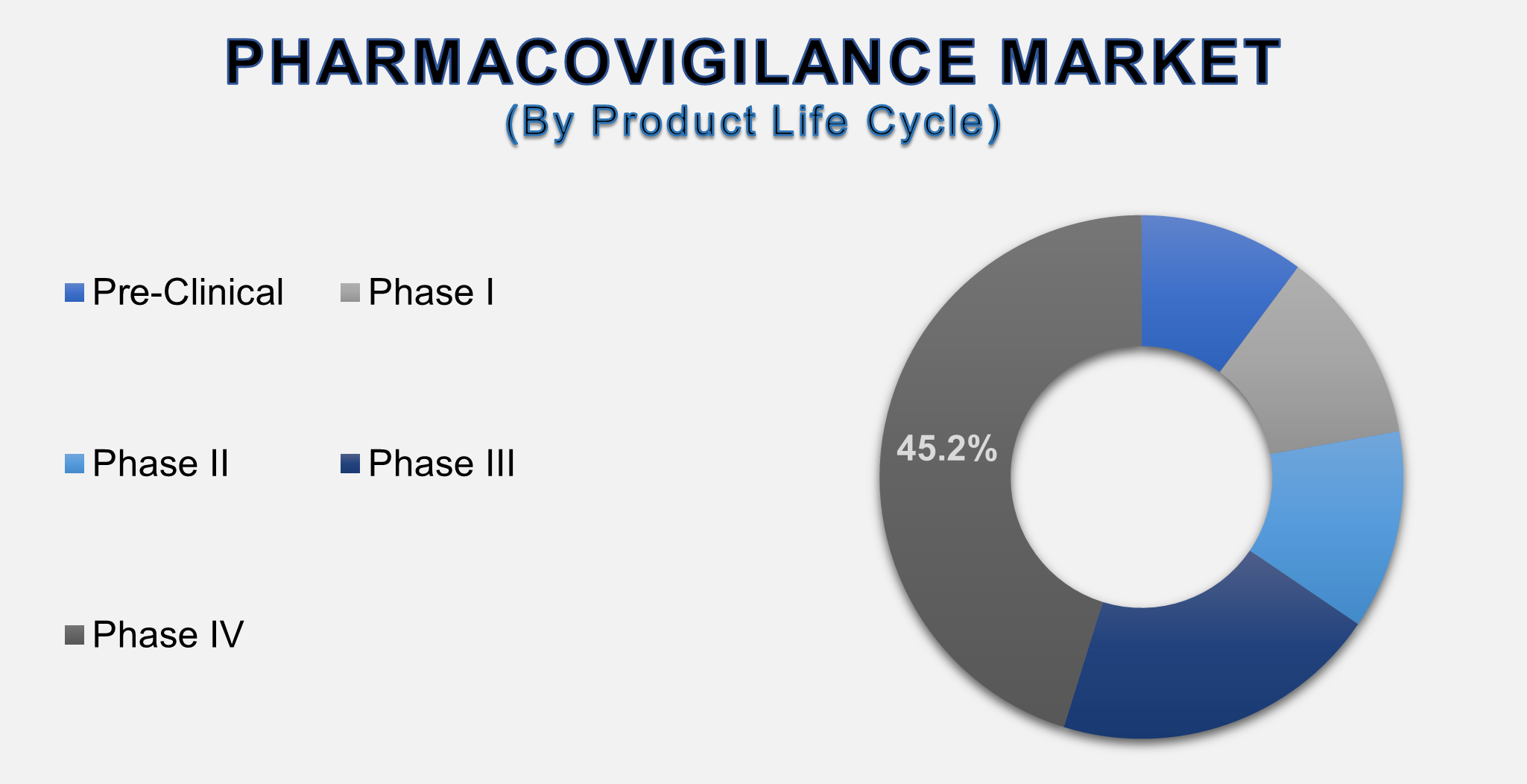

The Phase IV (Post-Marketing Surveillance)

product life cycle segment is projected to grow at a significant CAGR.

The Phase IV segment's projected significant

growth is a direct result of regulatory mandates and the critical need to

monitor drug safety in large, diverse patient populations over the long term.

While pre-approval phases are crucial, the real-world safety profile of a drug

is fully revealed only after it is marketed to a much larger and less

controlled population. Regulatory authorities require continuous monitoring and

reporting of adverse events throughout a drug's market life. The rise of

risk-management plans and the increasing number of drugs receiving accelerated

approval—which often comes with strict post-marketing study requirements—are key

drivers. As the volume of marketed drugs, especially complex therapies,

continues to grow, the demand for robust and continuous Phase IV

pharmacovigilance services is accelerating, fueling this segment's rapid

expansion.

The Spontaneous Reporting type segment is

projected to witness the highest growth rate.

Spontaneous Reporting's position as the

fastest-growing segment is firmly rooted in its status as the cornerstone of

most national pharmacovigilance systems. It is the most common and fundamental

method for detecting new, rare, or serious adverse drug reactions. The growth

of this segment is being amplified by digital transformation. The proliferation

of easy-to-use, online reporting portals for healthcare professionals and

patients, along with mobile health applications, has significantly lowered the

barrier to reporting. Increased global awareness campaigns about the importance

of reporting ADRs, led by regulatory bodies and patient advocacy groups, are

also contributing to a higher volume of spontaneous reports. As digital access

and health literacy improve worldwide, the volume and strategic value of data

from spontaneous reports are expected to grow exponentially.

The following segments are part of an in-depth analysis of

the global Pharmacovigilance Market:

|

Market

Segments |

|

|

By Service

Provider |

●

In-House ●

Contract Outsourcing |

|

By Product

Life Cycle |

●

Preclinical ●

Phase I ●

Phase II ●

Phase III ●

Phase IV |

|

By Type |

●

Spontaneous

Reporting ●

Intensified ADR

Reporting ●

Targeted Spontaneous

Reporting ●

Cohort Event

Monitoring ●

EHR Mining |

|

By End-user |

●

Pharmaceutical

Companies ●

Biotechnology

Companies ●

Medical Device

Companies ●

CROs |

Pharmacovigilance Market

Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Pharmacovigilance Market

globally throughout the forecast period.

North America's dominance is attributed to the

presence of a stringent regulatory authority (the FDA), the highest global

concentration of pharmaceutical and biotechnology companies, and substantial

R&D investment. The region's early and widespread adoption of advanced

technologies, such as AI and cloud-based solutions for drug safety, further

solidifies its lead. The well-established healthcare infrastructure, high

healthcare expenditure, and a mature culture of post-marketing surveillance and

compliance contribute significantly to North America's leading position. The

complex regulatory environment necessitates sophisticated pharmacovigilance

systems, driving consistent and high-value market demand.

It is estimated that over 2 million individual

case safety reports (ICSRs) are processed annually in the United States alone.

This high volume is driven by mandatory reporting requirements for

manufacturers and the active participation of healthcare providers. The vast

majority of new molecular entities approved each year come with post-marketing

commitments or requirements, ensuring a continuous pipeline of work for PV

systems. The growing focus on patient-reported outcomes and the integration of

real-world evidence into regulatory decision-making are further intensifying

the demand for advanced pharmacovigilance capabilities in the region.

Pharmacovigilance Market

Competition Landscape Analysis

The global pharmacovigilance

market is competitive and features a mix of large, global CROs, specialized PV

service providers, and IT firms offering safety software solutions. Competition

is centered on technological capability, regulatory expertise, global

operational footprint, and the ability to offer integrated, end-to-end

services. Key strategies include mergers and acquisitions to gain scale and

expertise, heavy investment in AI and automation platforms, and forming

strategic partnerships with technology companies. The market also sees

competition from niche players offering region-specific or

therapy-area-specific services.

Global Pharmacovigilance

Market Recent Developments News:

- In January 2025, IQVIA Holdings Inc. launched a new

AI-powered safety analytics platform designed to accelerate signal

detection and management for its clients. IQVIA's launch represents a

strategic move to leverage artificial intelligence in enhancing drug

safety monitoring. This platform uses advanced algorithms to sift through

massive volumes of disparate data from clinical trials, spontaneous

reports, and medical literature to identify potential safety signals

(adverse drug reactions) faster and more accurately than traditional

manual methods.

- In November 2024, LabCorp (Covance) announced a

strategic partnership with a leading health tech company to integrate

real-world data from wearables into its pharmacovigilance services. This partnership signifies a

major evolution in pharmacovigilance, shifting from passive reporting to

active, continuous monitoring. By integrating data from wearable devices

such as heart rate, activity levels, and sleep patterns into its safety

services, LabCorp can access a rich stream of real-world evidence (RWE).

- In September 2024, ICON plc completed the

acquisition of a specialized pharmacovigilance consultancy to bolster its

expertise in cell and gene therapy safety monitoring.

- In July 2024, Oracle Health Sciences updated its Argus Safety

platform with enhanced automation features for processing high volumes of

ICSRs. Oracle's enhancements to its industry-standard Argus platform

likely include features for automated data entry, triage, and coding,

which reduce manual effort and minimize human error.

The Global

Pharmacovigilance Market Is Dominated by a Few Large Companies, such as

●

IQVIA Holdings Inc.

●

LabCorp (Covance)

●

ICON plc

●

Parexel International

Corporation

●

Accenture PLC

●

Cognizant

●

IBM Corporation

●

Oracle Corporation

●

ArisGlobal LLC

●

BioClinica, Inc. (a

CLARIO company)

●

CAPTION Health

●

FMD K&L

● Other Prominent Players

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1. Global Pharmacovigilance

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Pharmacovigilance Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Pharmacovigilance

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Service Provider of Global

Pharmacovigilance Market

1.3.2.Product Life Cycle of

Global Pharmacovigilance Market

1.3.3.Type of Global Pharmacovigilance

Market

1.3.4.End-user of Global Pharmacovigilance

Market

1.3.5.Region of Global Pharmacovigilance

Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Pricing

Analysis

2.6.

Technological

Advancements

2.7.

Key

Developments

2.8.

Market

Entry Strategies

2.9.

Market

Dynamics

2.9.1.Drivers

2.9.2.Limitations

2.9.3.Opportunities

2.9.4.Impact Analysis of Drivers

and Restraints

2.10.

Porter’s

Five Forces Analysis

2.11.

PEST

Analysis

3. Global

Pharmacovigilance Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Pharmacovigilance Market Estimates

& Forecast Trend Analysis, by Service Provider

4.1.

Global

Pharmacovigilance Market Revenue (US$ Bn) Estimates and Forecasts, by Service

Provider, 2020 - 2033

4.1.1.In-House

4.1.2.Contract Outsourcing

5. Global

Pharmacovigilance Market Estimates

& Forecast Trend Analysis, by Product Life Cycle

5.1.

Global

Pharmacovigilance Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Life Cycle, 2020 - 2033

5.1.1.Pre-Clinical

5.1.2.Phase I

5.1.3.Phase II

5.1.4.Phase III

5.1.5.Phase IV

6. Global

Pharmacovigilance Market Estimates

& Forecast Trend Analysis, by Type

6.1.

Global

Pharmacovigilance Market Revenue (US$ Bn) Estimates and Forecasts, by Type 2020

- 2033

6.1.1.Spontaneous Reporting

6.1.2.Intensified ADR Reporting

6.1.3.Targeted Spontaneous

Reporting

6.1.4.Cohort Event Monitoring

6.1.5.EHR Mining

7. Global

Pharmacovigilance Market Estimates

& Forecast Trend Analysis, by End-user

7.1.

Global

Pharmacovigilance Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2020 - 2033

7.1.1.Pharmaceutical Companies

7.1.2.Biotechnology Companies

7.1.3.Medical Device Companies

7.1.4.CROs

8. Global

Pharmacovigilance Market Estimates

& Forecast Trend Analysis, by region

8.1.

Global

Pharmacovigilance Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

8.1.1.North America

8.1.2.Europe

8.1.3.Asia Pacific

8.1.4.Middle East & Africa

8.1.5.Latin America

9. North America Pharmacovigilance

Market: Estimates & Forecast Trend

Analysis

9.1. North America Pharmacovigilance

Market Assessments & Key Findings

9.1.1.North America Pharmacovigilance

Market Introduction

9.1.2.North America Pharmacovigilance

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1.

By Service Provider

9.1.2.2.

By Product Life Cycle

9.1.2.3.

By Type

9.1.2.4.

By End-user

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Pharmacovigilance

Market: Estimates & Forecast Trend

Analysis

10.1. Europe Pharmacovigilance

Market Assessments & Key Findings

10.1.1. Europe Pharmacovigilance

Market Introduction

10.1.2. Europe Pharmacovigilance

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1.

By Service Provider

10.1.2.2.

By Product Life Cycle

10.1.2.3.

By Type

10.1.2.4.

By End-user

10.1.2.5. By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Pharmacovigilance

Market: Estimates & Forecast Trend

Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Pharmacovigilance Market Introduction

11.1.2.

Asia

Pacific Pharmacovigilance Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

11.1.2.1.

By Service Provider

11.1.2.2.

By Product Life Cycle

11.1.2.3.

By Type

11.1.2.4.

By End-user

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Pharmacovigilance

Market: Estimates & Forecast Trend

Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Pharmacovigilance Market Introduction

12.1.2. Middle

East & Africa

Pharmacovigilance Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

12.1.2.1.

By Service Provider

12.1.2.2.

By Product Life Cycle

12.1.2.3.

By Type

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. UAE

12.1.2.5.2. Saudi

Arabia

12.1.2.5.3. South

Africa

12.1.2.5.4. Rest

of MEA

13. Latin America

Pharmacovigilance Market: Estimates

& Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Pharmacovigilance

Market Introduction

13.1.2. Latin America Pharmacovigilance

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

13.1.2.1.

By Service Provider

13.1.2.2.

By Product Life Cycle

13.1.2.3.

By Type

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Argentina

13.1.2.5.3. Mexico

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Pharmacovigilance

Market Product Mapping

15.2. Global Pharmacovigilance

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

15.3. Global Pharmacovigilance

Market Tier Structure Analysis

15.4. Global Pharmacovigilance

Market Concentration & Company Market Shares (%) Analysis, 2024

16.

Company

Profiles

16.1.

IQVIA Holdings Inc.

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

16.2.

LabCorp (Covance)

16.3.

ICON plc

16.4.

Parexel International Corporation

16.5.

Accenture PLC

16.6.

Cognizant

16.7.

IBM Corporation

16.8.

Oracle Corporation

16.9.

ArisGlobal LLC

16.10.

BioClinica, Inc. (a CLARIO company)

16.11.

CAPTION Health

16.12.

FMD K&L

16.13.

Other Prominent Players

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables