Population Health Management Market Size and Forecast (2026–2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (Software, Services, Platforms); By Deployment Mode (Cloud-Based, On-Premises, Hybrid); By Function (Data Integration & Management, Patient Engagement, Care Coordination, Risk Stratification, Healthcare Analytics, Clinical Decision Support, Financial Management, Others); By End User (Healthcare Providers, Healthcare Payers, Government Healthcare Organizations, Employer Groups, Accountable Care Organizations, Others), and Geography

2026-06-23

Healthcare

Swetal (Research Analyst)

Description

Population Health Management Market

Overview

The global Population

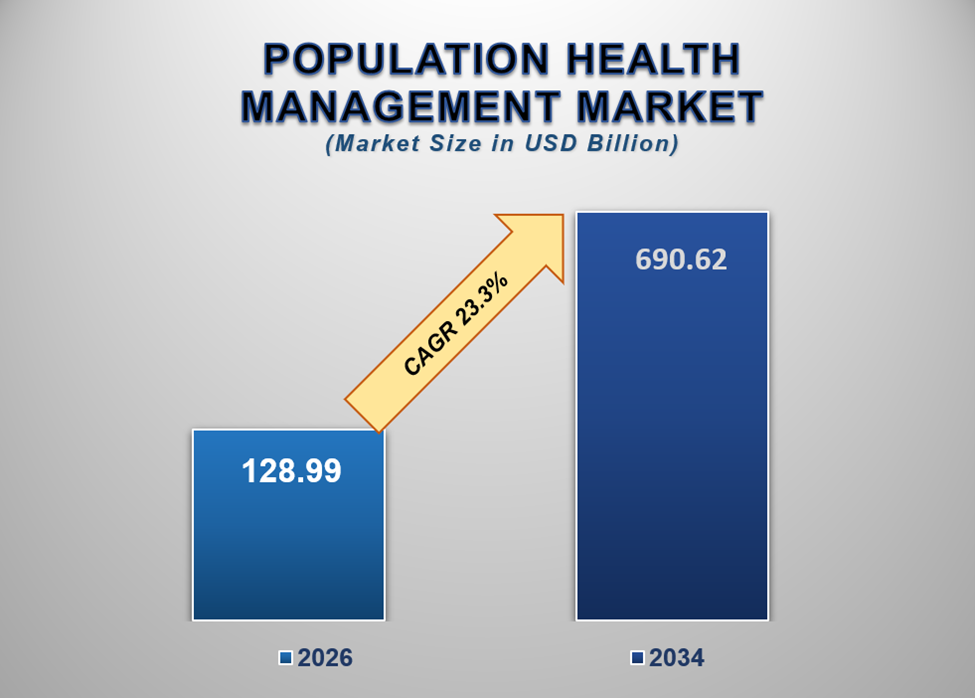

Health Management (PHM) Market was valued at USD 128.99 billion in 2026

and is projected to reach USD 690.62 billion by 2034, expanding at a

remarkable CAGR of 23.3% during the forecast period. The market is

experiencing substantial growth due to the increasing transition toward

value-based healthcare models, rising prevalence of chronic diseases, growing

adoption of healthcare analytics platforms, expanding use of electronic health

records, and increasing emphasis on improving patient outcomes while reducing

healthcare expenditures.

Population

Health Management has emerged as one of the most transformative approaches in

modern healthcare delivery. It focuses on improving the health outcomes of

specific populations by integrating clinical, financial, operational, and

behavioral health data to enable proactive care management, risk

identification, disease prevention, and healthcare resource optimization.

Traditionally,

healthcare systems have been structured around reactive treatment models that

focus primarily on managing illnesses after they occur. However, rising

healthcare costs, increasing chronic disease burdens, aging populations, and

growing pressure to improve care quality have accelerated the shift toward

preventive and value-based healthcare approaches. Population health management

solutions play a central role in supporting this transformation.

PHM platforms

aggregate and analyze data from diverse sources, including electronic health

records, insurance claims, pharmacy systems, laboratory databases, wearable

devices, remote monitoring platforms, and social determinants of health. These

integrated datasets enable healthcare organizations to gain comprehensive

insights into patient populations, identify high-risk individuals, and develop

targeted intervention strategies.

The increasing

prevalence of chronic conditions such as diabetes, cardiovascular diseases,

respiratory disorders, obesity, and cancer is creating substantial demand for

population health management solutions. These conditions require continuous

monitoring, coordinated care delivery, and long-term management strategies that

can be effectively supported through PHM platforms.

Healthcare

providers are increasingly adopting advanced analytics, predictive modeling,

artificial intelligence, and machine learning technologies to improve patient

stratification, disease prediction, care coordination, and treatment

optimization. These technologies enable healthcare organizations to move from

reactive care delivery toward predictive and preventive healthcare management.

Government

initiatives promoting healthcare digitization, interoperability, and

value-based reimbursement frameworks are further supporting market growth. Many

healthcare systems worldwide are implementing policies that incentivize

providers to improve patient outcomes while reducing unnecessary healthcare

utilization.

Additionally,

healthcare payers are increasingly utilizing PHM solutions to manage risk,

control costs, optimize reimbursement models, and improve member engagement.

The ability to identify high-cost patient populations and implement targeted

care interventions provides significant financial and clinical benefits.

As healthcare organizations continue prioritizing patient-centered care, preventive health strategies, and data-driven decision-making, the population health management market is expected to witness robust expansion throughout the forecast period.

Population Health Management Market

Drivers and Opportunities

Transition

Toward Value-Based Healthcare Models Is Driving Market Growth

One of the most

significant factors fueling the growth of the population health management

market is the global shift from fee-for-service healthcare models toward

value-based care systems.

Under

traditional healthcare reimbursement structures, providers are compensated

based on the volume of services delivered rather than patient outcomes. This

model often results in fragmented care delivery and rising healthcare

expenditures. Value-based care frameworks aim to align financial incentives

with quality outcomes, patient satisfaction, and cost efficiency.

Population

health management solutions provide the data integration, analytics, and care

coordination capabilities necessary to support value-based care initiatives.

Healthcare organizations utilize PHM platforms to monitor patient populations,

identify care gaps, track clinical outcomes, and implement targeted

intervention programs.

These solutions

enable providers to proactively manage patient health, reduce hospital

admissions, minimize readmissions, and improve overall care quality. As

healthcare systems increasingly adopt outcome-based reimbursement models,

demand for PHM technologies continues to accelerate.

Furthermore,

accountable care organizations, integrated delivery networks, and value-based

care providers rely heavily on population health management tools to achieve

performance objectives and maximize reimbursement opportunities.

The continued evolution of value-based healthcare frameworks is expected to remain a major driver of market expansion.

Rising Burden

of Chronic Diseases Is Accelerating Market Adoption

The increasing

prevalence of chronic diseases worldwide is another major factor contributing

to market growth.

Chronic

conditions account for a significant proportion of global healthcare

expenditures and often require long-term care management, frequent medical

interventions, and ongoing patient monitoring. Conditions such as diabetes,

hypertension, cardiovascular diseases, chronic respiratory disorders, obesity,

and mental health conditions place substantial pressure on healthcare systems.

Population

health management platforms enable healthcare organizations to identify at-risk

populations, monitor disease progression, coordinate multidisciplinary care,

and implement preventive interventions before complications occur.

Advanced

analytics capabilities allow providers to predict disease risks, optimize

treatment pathways, and allocate healthcare resources more efficiently. These

benefits contribute to improved patient outcomes while reducing overall

healthcare costs.

Additionally,

aging populations in many countries are increasing the prevalence of chronic

health conditions, further strengthening the need for comprehensive population

health management strategies.

As chronic disease burdens continue growing globally, healthcare organizations are expected to increase investments in PHM solutions.

Artificial

Intelligence and Predictive Healthcare Analytics Present Significant

Opportunities

Emerging

technologies are creating transformative opportunities within the population

health management market.

Artificial

intelligence and machine learning technologies are enabling healthcare

organizations to extract deeper insights from complex healthcare datasets.

These technologies support predictive risk modeling, disease forecasting,

patient stratification, treatment optimization, and personalized care planning.

Healthcare

providers increasingly utilize predictive analytics to identify patients who

may be at risk of hospitalization, disease progression, medication

non-adherence, or adverse clinical events. Early intervention strategies

supported by predictive analytics can significantly improve patient outcomes

while reducing healthcare costs.

The integration

of social determinants of health data into population health platforms also

presents substantial opportunities. Factors such as income levels, housing

conditions, education, transportation access, and community resources

significantly influence health outcomes. Incorporating these variables into

care planning enables more holistic and effective healthcare interventions.

Furthermore, the

growing adoption of remote patient monitoring, wearable health technologies,

digital therapeutics, and telehealth platforms is expanding the volume of

real-time patient data available for population health management.

As healthcare organizations increasingly embrace data-driven care delivery models, opportunities for advanced PHM solutions are expected to grow substantially.

Population Health Management Market

Scope

|

Report Attributes |

Description |

|

Market Size in 2026 |

USD 128.99 Billion |

|

Market Forecast in 2034 |

USD 690.62 Billion |

|

CAGR % 2026-2034 |

23.3% |

|

Base Year |

2025 |

|

Historic Data |

2021-2025 |

|

Forecast Period |

2026-2034 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production, Service Type, Growth

Factors and more |

|

Segments Covered |

∙ By Component |

|

Regional Scope |

● North America |

|

Country Scope |

U.S. |

Population

Health Management Market Report Segmentation Analysis

The global population health management market industry analysis is segmented by component, by deployment mode, by function, by end user, and by region.

Software

Segment Is Expected to Dominate the Market During the Forecast Period

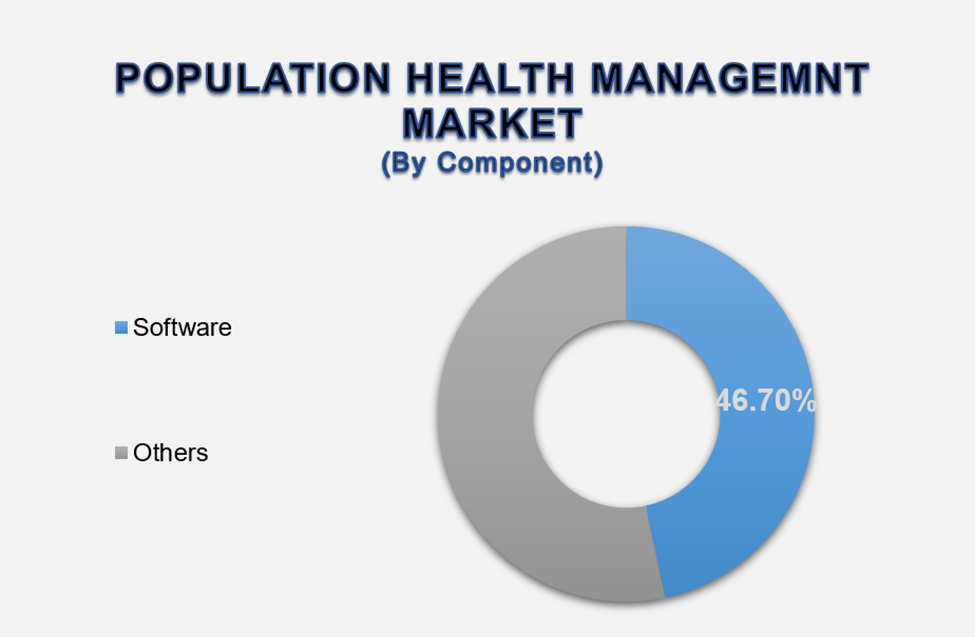

The software

segment accounted for approximately 46.7% of the global market, making

it the largest component category.

Software

solutions represent the core foundation of population health management

initiatives. These platforms integrate, organize, analyze, and visualize vast

volumes of healthcare data obtained from multiple clinical and administrative

sources.

Healthcare

organizations increasingly rely on software platforms to support patient risk

stratification, predictive analytics, care coordination, disease management,

quality reporting, and performance monitoring activities. Modern PHM software

solutions also incorporate artificial intelligence, machine learning, and

automation capabilities that improve decision-making efficiency.

The increasing

adoption of electronic health records and healthcare interoperability

frameworks is further driving demand for advanced population health management

software. Organizations seek integrated platforms capable of delivering

comprehensive insights across diverse patient populations.

Additionally,

software platforms enable healthcare providers to monitor clinical outcomes,

identify care gaps, and optimize resource allocation in real time. These

capabilities are essential for achieving value-based care objectives and

improving operational efficiency.

As healthcare organizations continue investing in digital transformation initiatives, software solutions are expected to maintain their dominant market position.

Cloud-Based

Segment Is Expected to Lead the Market by Deployment Mode

Cloud-based

deployment represents the largest segment within the population health

management market.

Healthcare

organizations increasingly prefer cloud-based PHM solutions because they offer

scalability, flexibility, remote accessibility, lower infrastructure costs, and

simplified implementation processes. Cloud environments also support seamless

integration of diverse healthcare datasets and enable real-time collaboration

among care teams.

The growing

adoption of telehealth services, remote patient monitoring systems, and

distributed healthcare networks is further supporting demand for cloud-based

deployment models.

Cloud platforms

facilitate advanced analytics, machine learning integration, and large-scale

data processing capabilities that are increasingly essential for population

health management initiatives.

Additionally,

cloud-based solutions enable organizations to rapidly scale operations as

patient populations and data volumes grow.

These advantages continue driving widespread adoption across healthcare providers, payers, and government organizations.

Healthcare

Analytics Segment Is Expected to Dominate the Market by Function

Healthcare

analytics represents the leading functional segment within the population

health management market.

Analytics

capabilities enable organizations to transform raw healthcare data into

actionable insights that support clinical, operational, and financial

decision-making. Through advanced analytics, providers can identify high-risk

patients, predict disease progression, evaluate treatment effectiveness, and

optimize care delivery strategies.

The growing

complexity of healthcare data and increasing demand for evidence-based

decision-making are strengthening the importance of analytics platforms.

Organizations increasingly rely on predictive and prescriptive analytics to

improve patient outcomes and manage healthcare costs.

Additionally,

analytics solutions support regulatory reporting, quality measurement programs,

risk adjustment initiatives, and value-based reimbursement models.

As healthcare organizations continue embracing data-driven care strategies, analytics functionality is expected to remain a cornerstone of population health management solutions.

The

Healthcare Providers Segment Is Expected to Lead the Market by End User

Healthcare

providers account for the largest share of the population health management

market.

Hospitals,

physician groups, integrated delivery networks, accountable care organizations,

and multi-specialty healthcare systems increasingly utilize PHM solutions to

improve patient outcomes, enhance care coordination, and achieve value-based

care objectives.

Providers face

growing pressure to reduce healthcare costs while maintaining high standards of

care quality. Population health management platforms help address these

challenges by enabling proactive patient engagement, preventive care

interventions, and evidence-based clinical decision-making.

Furthermore,

providers are increasingly leveraging PHM technologies to manage chronic

disease populations, reduce hospital readmissions, improve medication

adherence, and enhance patient satisfaction.

As healthcare delivery models continue evolving toward patient-centered and outcome-driven approaches, providers are expected to remain the largest end-user segment.

The following

segments are part of an in-depth analysis of the global Population Health

Management market:

|

Market Segments |

|

|

By Component |

∙ Software |

|

By

Deployment Mode |

∙ Cloud-Based |

|

By

Function |

∙ Data Integration

& Management |

|

By End User |

∙ Healthcare Providers |

Population

Health Management Market Share Analysis By Region

North America is

projected to dominate the global population health management market,

accounting for approximately 41.8% of total market revenue in 2026.

The region

benefits from advanced healthcare IT infrastructure, widespread adoption of

value-based care models, extensive electronic health record implementation, and

strong government support for healthcare digitization initiatives. The United

States remains the largest contributor due to significant investments in

healthcare analytics, interoperability solutions, and care management

platforms.

Europe

represents another major market driven by increasing healthcare modernization

efforts, aging populations, and growing adoption of digital health

technologies. Countries such as Germany, the United Kingdom, France, and the

Netherlands are actively implementing population health initiatives to improve

healthcare efficiency and outcomes.

Asia-Pacific is

expected to witness the fastest growth during the forecast period. Rapid

healthcare infrastructure development, expanding healthcare expenditures,

increasing chronic disease prevalence, and growing digital health adoption are

fueling regional demand.

China, India,

Japan, South Korea, and Australia are investing heavily in healthcare

information systems, telehealth platforms, and population health programs aimed

at improving healthcare accessibility and efficiency.

Meanwhile, Latin America and the Middle East & Africa are gradually expanding healthcare digitization efforts, creating additional growth opportunities for market participants.

Population

Health Management Market Competition Landscape Analysis

The global

population health management market is highly competitive and characterized by

rapid technological innovation, strategic partnerships, mergers and

acquisitions, and expanding healthcare analytics capabilities.

Leading

companies are investing heavily in artificial intelligence, predictive

analytics, interoperability solutions, cloud-based healthcare platforms, and

patient engagement technologies. These innovations are helping organizations

improve care coordination, optimize resource utilization, and enhance clinical

outcomes.

Strategic

collaborations between healthcare providers, payers, technology vendors, and

government agencies are becoming increasingly common as stakeholders seek

integrated population health solutions.

Market

participants are also focusing on improving data interoperability, expanding

real-time analytics capabilities, and integrating social determinants of health

into population health management platforms.

As healthcare systems increasingly prioritize preventive care and value-based healthcare delivery, competition is expected to intensify across the market.

Global Population

Health Management Market Recent Developments News:

∙ In April 2026,

healthcare technology providers expanded AI-powered predictive analytics

capabilities within population health management platforms.

∙ In February

2026, several healthcare systems increased investments in value-based care

technologies to improve care coordination and patient outcomes.

∙ In November

2025, digital health companies introduced enhanced interoperability solutions

aimed at improving healthcare data integration.

∙ In August

2025, healthcare organizations expanded remote patient monitoring programs

supported by population health analytics platforms.

∙ In June 2025, technology vendors launched advanced social determinants of health analytics tools to support holistic population health strategies.

The Global

Population Health Management Market is Dominated by a Few Large Companies, Such

As

∙ Oracle Health

∙ Veradigm LLC

∙ Optum, Inc.

∙ Health Catalyst, Inc.

∙ Arcadia Solutions, LLC

∙ Innovaccer Inc.

∙ Athenahealth, Inc.

∙ eClinicalWorks LLC

∙ Epic Systems Corporation

∙ Koninklijke Philips N.V.

∙ IBM Corporation

∙ Conifer Health Solutions, LLC

∙ Medecision, Inc.

∙ Cotiviti, Inc.

∙ Cerner Population Health (Oracle Health)

∙ Others

Frequently Asked Questions

Swetal (Research Analyst)

Swetal is a Research Analyst with 4+ years of experience specializing in healthcare market research, medical devices, healthcare IT, and medical technology industry analysis. Her expertise includes competitive intelligence, secondary research, market trend forecasting, and healthcare business insights across global healthcare ecosystems.

She contributes to advanced market research reports by analyzing regulatory frameworks, emerging healthcare technologies, competitive landscapes, and innovation trends shaping the medical industry. With a strong focus on accurate market intelligence, strategic insights, and healthcare industry trends, Swetal supports businesses in making informed, data-backed decisions in a rapidly transforming healthcare environment.

1.

Global Population Health

Management Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Population Health Management Market Scope and Market

Estimation

1.2.1.

Global Population Health

Management Overall Market Size (US$ Billion), Market CAGR (%), Market Forecast

(2026 - 2034)

1.2.2.

Global Population Health

Management Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2034

1.3. Market Segmentation

1.3.1.

Component of Global Population

Health Management Market

1.3.2.

Deployment Mode of Global

Population Health Management Market

1.3.3.

Function of Global Population

Health Management Market

1.3.4.

End User of Global Population

Health Management Market

1.3.5.

Region of Global Population

Health Management Market

2.

Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Billion) Analysis 2021 – 2025 and Forecast, 2026

– 2034

2.4. Demand and Opportunity Assessment

2.5. Key Developments

2.6. Overview of Regulatory Landscape and Value-Based Care Framework

2.7. Market Entry Strategies

2.8. Market Dynamics

2.8.1.

Drivers

2.8.2.

Limitations

2.8.3.

Opportunities

2.8.4.

Impact Analysis of Drivers and

Restraints

2.9. Porter’s Five Forces Analysis

2.10.

PEST Analysis

3.

Global Population Health

Management Market Estimates & Historical Trend Analysis (2021 - 2025)

4.

Global Population Health

Management Market Estimates & Forecast Trend Analysis, by Component

4.1. Global Population Health Management Market Revenue (US$ Billion)

Estimates and Forecasts, by Component, 2021 - 2034

4.1.1.

Software

4.1.2.

Services

4.1.3.

Platforms

5.

Global Population Health

Management Market Estimates & Forecast Trend Analysis, by Deployment Mode

5.1. Global Population Health Management Market Revenue (US$ Billion)

Estimates and Forecasts, by Deployment Mode, 2021 - 2034

5.1.1.

Cloud-Based

5.1.2.

On-Premises

5.1.3.

Hybrid

6.

Global Population Health

Management Market Estimates & Forecast Trend Analysis, by Function

6.1. Global Population Health Management Market Revenue (US$ Billion)

Estimates and Forecasts, by Function, 2021 - 2034

6.1.1.

Data Integration &

Management

6.1.2.

Patient Engagement

6.1.3.

Care Coordination

6.1.4.

Risk Stratification

6.1.5.

Healthcare Analytics

6.1.6.

Clinical Decision Support

6.1.7.

Financial Management

6.1.8.

Others

7.

Global Population Health

Management Market Estimates & Forecast Trend Analysis, by End User

7.1. Global Population Health Management Market Revenue (US$ Billion)

Estimates and Forecasts, by End User, 2021 - 2034

7.1.1.

Healthcare Providers

7.1.2.

Healthcare Payers

7.1.3.

Government Healthcare

Organizations

7.1.4.

Employer Groups

7.1.5.

Accountable Care Organizations

7.1.6.

Others

8.

Global Population Health

Management Market Estimates & Forecast Trend Analysis, by Region

8.1. Global Population Health Management Market Revenue (US$ Billion)

Estimates and Forecasts, by Region, 2021 - 2034

8.1.1.

North America

8.1.2.

Europe

8.1.3.

Asia Pacific

8.1.4.

Middle East & Africa

8.1.5.

Latin America

9.

North America Population

Health Management Market: Estimates & Forecast Trend Analysis

9.1. North America Population Health Management Market Assessments &

Key Findings

9.1.1.

North America Population Health

Management Market Introduction

9.1.2.

North America Population Health

Management Market Size Estimates and Forecast (2021 - 2034)

9.1.2.1.

By Component

9.1.2.2.

By Deployment Mode

9.1.2.3.

By Function

9.1.2.4.

By End User

9.1.2.5.

By Country

9.1.2.5.1.

U.S.

9.1.2.5.2.

Canada

10. Europe Population Health Management Market: Estimates & Forecast

Trend Analysis

10.1.

Europe Population Health

Management Market Assessments & Key Findings

10.1.1.

Europe Population Health

Management Market Introduction

10.1.2.

Europe Population Health

Management Market Size Estimates and Forecast (2021 - 2034)

10.1.2.1.

By Component

10.1.2.2.

By Deployment Mode

10.1.2.3.

By Function

10.1.2.4.

By End User

10.1.2.5.

By Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7.

Rest of Europe

11. Asia Pacific Population Health Management Market: Estimates &

Forecast Trend Analysis

11.1.

Asia Pacific Market Assessments

& Key Findings

11.1.1.

Asia Pacific Population Health

Management Market Introduction

11.1.2.

Asia Pacific Population Health

Management Market Size Estimates and Forecast (2021 - 2034)

11.1.2.1.

By Component

11.1.2.2.

By Deployment Mode

11.1.2.3.

By Function

11.1.2.4.

By End User

11.1.2.5.

By Country

11.1.2.5.1.

China

11.1.2.5.2.

Japan

11.1.2.5.3.

India

11.1.2.5.4.

Australia

11.1.2.5.5.

South Korea

11.1.2.5.6.

Rest of Asia Pacific

12. Middle East & Africa Population Health Management Market:

Estimates & Forecast Trend Analysis

12.1.

Middle East & Africa Market

Assessments & Key Findings

12.1.1.

Middle East & Africa

Population Health Management Market Introduction

12.1.2.

Middle East & Africa

Population Health Management Market Size Estimates and Forecast (2021 - 2034)

12.1.2.1.

By Component

12.1.2.2.

By Deployment Mode

12.1.2.3.

By Function

12.1.2.4.

By End User

12.1.2.5.

By Country

12.1.2.5.1.

UAE

12.1.2.5.2.

Saudi Arabia

12.1.2.5.3.

South Africa

12.1.2.5.4.

Rest of MEA

13. Latin America Population Health Management Market: Estimates &

Forecast Trend Analysis

13.1.

Latin America Market

Assessments & Key Findings

13.1.1.

Latin America Population Health

Management Market Introduction

13.1.2.

Latin America Population Health

Management Market Size Estimates and Forecast (2021 - 2034)

13.1.2.1.

By Component

13.1.2.2.

By Deployment Mode

13.1.2.3.

By Function

13.1.2.4.

By End User

13.1.2.5.

By Country

13.1.2.5.1.

Brazil

13.1.2.5.2.

Mexico

13.1.2.5.3.

Argentina

13.1.2.5.4.

Rest of LATAM

14. Competition Landscape

14.1.

Global Population Health

Management Market Product Mapping

14.2.

Global Population Health

Management Market Concentration Analysis

14.3.

Global Population Health

Management Market Tier Structure Analysis

14.4.

Global Population Health

Management Market Share Analysis (2025)

15. Company Profiles

15.1.

Oracle Health

15.1.1.

Company Overview & Key

Stats

15.1.2.

Financial Performance &

KPIs

15.1.3.

Product Portfolio

15.1.4.

SWOT Analysis

15.1.5.

Business Strategy & Recent

Developments

15.2.

Veradigm LLC

15.3.

Optum, Inc.

15.4.

Health Catalyst, Inc.

15.5.

Arcadia Solutions, LLC

15.6.

Innovaccer Inc.

15.7.

Athenahealth, Inc.

15.8.

eClinicalWorks LLC

15.9.

Epic Systems Corporation

15.10.

IBM Corporation

15.11.

Philips N.V.

15.12.

Others

16. Research Findings & Conclusion

17. Assumption & Acronyms Used

18. Research Methodology

18.1.

External Databases

18.2.

Internal Proprietary

Database

18.3.

Primary Research

18.4.

Secondary Research

18.5.

Assumptions

18.6.

Limitations

18.7.

Report FAQs

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables