Printed Tape Market Size and Forecast (2025–2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Material (Polypropylene, Polyvinyl Chloride, Others), By End-use (Food & Beverage, Consumer Durables, Transportation & Logistics, others), and Geography

2025-12-18

Packaging Industry

Jaya Bundele (Research Analyst)

Description

Printed

Tape Market Overview

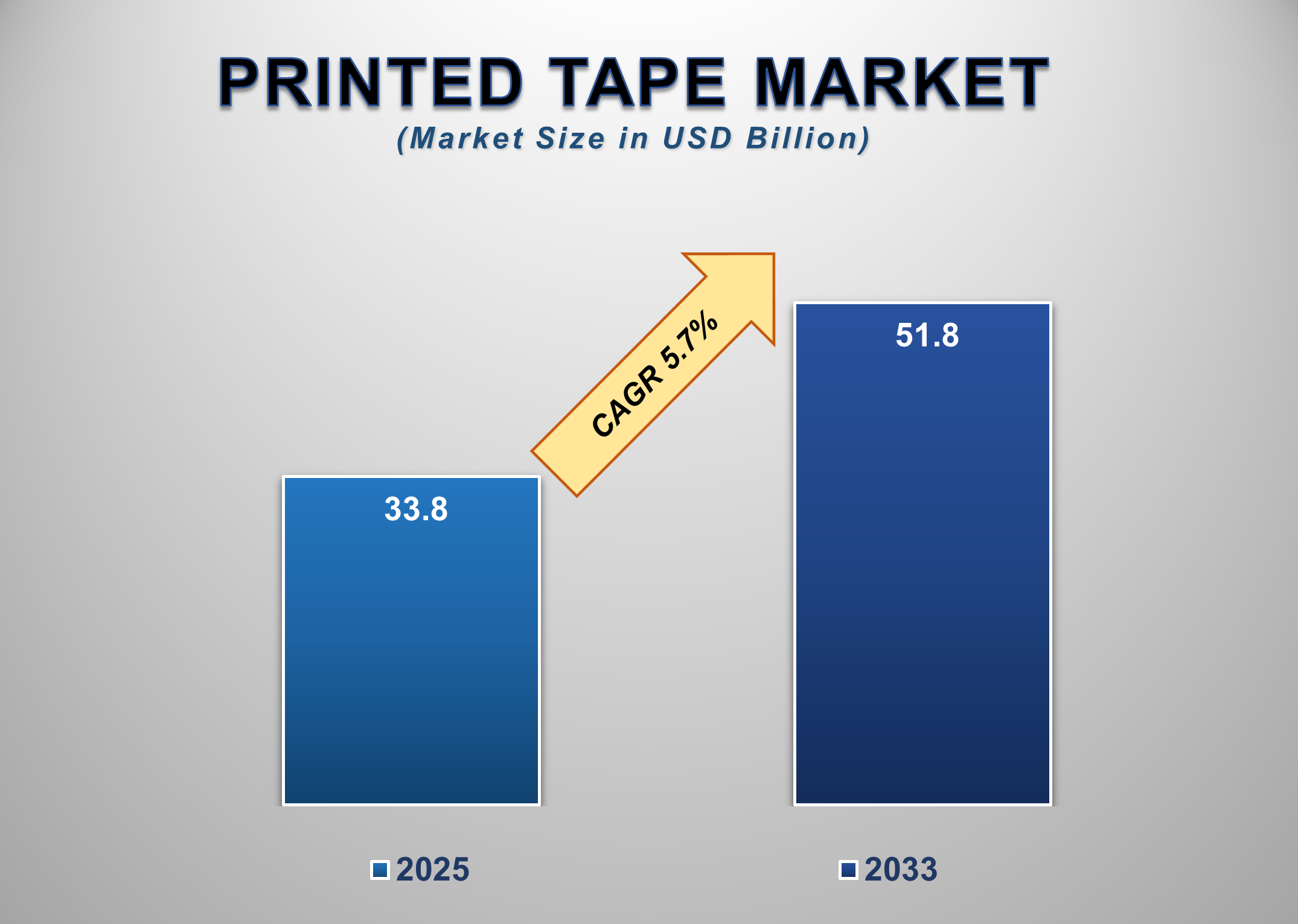

The global Printed Tape Market is witnessing steady expansion as industries increasingly prioritize branded packaging, traceability, product differentiation, and regulatory-compliant labeling. Valued at USD 33.8 billion in 2025, the market is projected to reach USD 51.8 billion by 2033, reflecting a CAGR of 5.7% during the forecast period. Printed tapes used for sealing, branding, identification, safety messaging, and logistics operations have become integral across manufacturing, retail, e-commerce, and distribution channels. The surge in global goods movement, growth of digital commerce platforms, and rise of automated packaging processes are accelerating adoption, especially in fast-moving sectors like food & beverages and transportation & logistics.

Printed tapes also serve as an

economical branding solution compared to pre-printed packaging boxes, allowing

companies to enhance visibility without increasing packaging complexity. The

ability to integrate barcodes, QR codes, batch details, and security features

is further elevating demand across compliance-heavy industries.

Printed

Tape Market Drivers and Opportunities

Rising Need for Branded and

Tamper-Evident Packaging Is Driving the Printed Tape Market Growth

Brand recognition and

reputational consistency across supply chains have become critical for

companies operating in increasingly competitive global markets. Printed tapes

offer a cost-effective and prominent surface for branding, logo placement, and

promotional messaging without requiring changes in primary packaging. This

feature makes them highly attractive to mid-sized and large enterprises seeking

packaging uniformity at scale. As consumer purchase decisions become more

influenced by recognizable packaging, businesses across food & beverage,

FMCG, electronics, and e-commerce sectors are adopting printed tapes to

reinforce brand identity during transit. Tamper-evident and security-integrated

printed tapes are another major growth driver, especially in pharmaceuticals,

electronics, and high-value consumer goods. The ability to incorporate

anti-counterfeit patterns, batch numbers, holographic prints, and void

messaging enhances shipment integrity while meeting regulatory compliance

requirements. E-commerce penetration continues to surge worldwide, increasing

parcel volumes and heightening the need for secure, traceable, and visually

distinct packaging. Printing technologies such as flexography, digital

printing, and UV-cured inks further enable high-resolution customization, color

accuracy, and rapid changeovers, making short-run and on-demand printing more

viable for brands. As supply chains globalize and product authentication

becomes more complex, the combined value proposition of branding, security, and

cost-efficiency is driving sustained adoption of printed tapes across

industries.

Expansion of E-commerce and

Logistics Networks Is Fueling Demand for Printed Tape Worldwide

The global expansion of

e-commerce platforms, parcel delivery services, and third-party logistics

networks is significantly boosting demand for printed tapes. With billions of

packages shipped annually, companies are increasingly utilizing printed tapes for

brand visibility, package tracking, and handling instructions. As customers

expect faster deliveries and enhanced unboxing experiences, logistics-dependent

industries are leveraging printed tapes to improve operational efficiency and

brand connection. Printed tapes help logistics operators convey essential

information such as “Fragile,” “Handle with Care,” or directional arrows,

reducing product damage and improving warehouse handling accuracy. Moreover,

the rise of automated sorting systems in distribution centers requires clear

visual cues and scannable elements on packaging; printed tapes serve as an

optimal solution by integrating barcodes and QR codes that support traceability

at each touchpoint.

Sustainability trends are also

reshaping the logistics industry’s use of tapes. Many companies are

transitioning to recyclable polypropylene and eco-friendly water-based inks.

These advancements align with global commitments to green packaging and help reduce

environmental impact without compromising performance. As global shipping

volumes continue to grow, driven by cross-border e-commerce, retail

modernization, and digital marketplaces, the need for durable, informative, and

brand-enhancing printed tapes is expected to rise substantially through 2033.

Growing Adoption of Printed

Tape Solutions in Emerging Manufacturing Economies Is Creating Significant

Market Opportunities Globally

Emerging economies in

Asia-Pacific, Latin America, and Eastern Europe are witnessing accelerated

industrialization, growth in manufacturing output, and expansion of

export-driven sectors, all contributing to expanding opportunities for printed

tape manufacturers. As factories modernize and adopt automated packaging lines,

printed tapes are increasingly relied upon for identification, branding, and

compliance labeling across high-volume industries such as food processing,

consumer durables, automotive components, and textiles. In regions like

Southeast Asia and India, rapid urbanization and the proliferation of modern

retail chains are driving the demand for packaged goods, consequently

increasing tape consumption. Small and medium-sized enterprises (SMEs) are also

transitioning from generic sealing tape to customized printed solutions to

enhance product differentiation and reduce counterfeiting risks. Government

policies that promote domestic manufacturing, including Make in India, Thailand

4.0, and Vietnam’s industrial expansion programs, further amplify demand for

supply chain packaging materials. As international trade volumes rise,

exporters in emerging markets use printed tapes to comply with

destination-country labeling norms and improve shipment identification for

logistics partners. The growing availability of low-cost digital printing

solutions and local converting facilities is enabling faster turnaround times

and improved customization capabilities. Collectively, these trends position

emerging economies as attractive markets for capacity expansion, partnerships,

and product diversification within the printed tape industry.

Printed Tape Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 33.8 Billion |

|

Market Forecast in 2033 |

USD 51.8 Billion |

|

CAGR % 2025-2033 |

5.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption,

Company Share, Company Heatmap, Company Production Capacity, Growth Factors,

and more |

|

Segments Covered |

●

By Material, By

End-use |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Printed Tape Market Report Segmentation Analysis

Based on segmentation, the

Printed Tape Market is categorized by Material, by End-use, and by Region.

The Polypropylene Segment

Accounted for the Largest Market Share in the Global Printed Tape Market

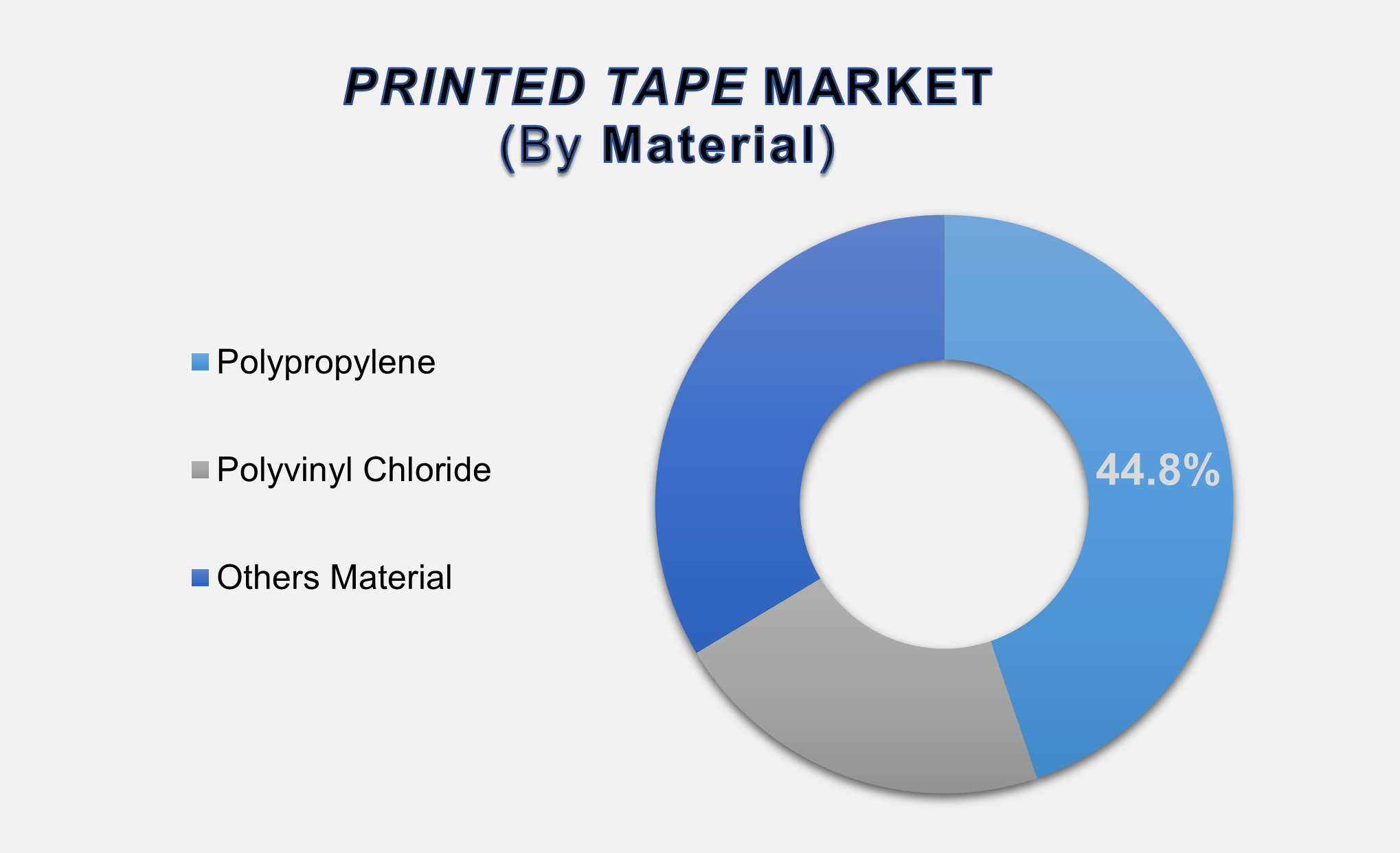

The polypropylene segment, contributing 44.8% of the global market, remains the leading material due to its excellent tensile strength, moisture resistance, affordability, and compatibility with high-resolution printing processes. Polypropylene tapes are widely used for carton sealing, branding, and product identification across high-volume industries such as food & beverage, electronics, and consumer goods. Their ability to support vibrant colors and maintain adhesive consistency across varying temperatures makes them suitable for both manual and automated packaging lines. As sustainability becomes increasingly central to packaging decisions, polypropylene’s recyclability further strengthens its market position. Continuous advancements in BOPP films, water-based inks, and adhesive technologies are enhancing durability and visual sharpness, boosting adoption across retail and logistics. With growing industrial output and e-commerce activity, demand for polypropylene-printed tapes is expected to remain dominant throughout the forecast period.

Food & Beverage Segment

Accounted for the Largest Share in the Global Printed Tape Market

The food & beverage sector

represents the largest end-use category, driven by the need for branded

packaging, batch identification, and clear handling instructions across

distribution chains. As packaged food consumption rises globally, especially in

APAC and North America, manufacturers are increasingly adopting printed tapes

to improve product visibility, enhance operational traceability, and support

temperature-sensitive logistics. Printed tapes are frequently used to display

safety warnings, freshness indicators, and regulatory compliance details. For

FMCG brands with high market competition, printed sealing tapes serve as a

low-cost, high-visibility branding tool that strengthens shelf presence and

customer recall. The expanding penetration of ready-to-eat meals, beverages,

and processed foods—coupled with rapid growth in modern retail and e-commerce

grocery delivery—is further amplifying tape usage. This segment will continue

to dominate, supported by stringent food labeling requirements and continuous innovation

in moisture-resistant and tamper-evident tape formats.

The following segments are

part of an in-depth analysis of the global Printed Tape Market:

|

Market

Segments |

|

|

By Material |

●

Polypropylene ●

Polyvinyl Chloride ●

Others Material |

|

By End Use |

●

Food & Beverage ●

Consumer Durables ●

Transportation &

Logistics ●

Others End Use |

Printed

Tape Market Share Analysis by Region

The

Asia Pacific region is projected to hold the largest share of the global

Printed Tape market over the forecast period.

Asia-Pacific accounted for 49.4%

of the global printed tape market, making it the largest and most influential

regional segment. APAC's leadership is underpinned by high manufacturing

activity, strong export volumes, and rapid growth in packaging-intensive

sectors like food processing, consumer durables, and transportation &

logistics. China, India, Indonesia, and Vietnam are major contributors, with

massive production ecosystems and extensive use of printed tapes for branding,

shipment labeling, and material handling. Competitive labor costs, availability

of raw materials, and strong investment inflows into industrial automation

strengthen the region’s dominance. Growing adoption of modern retail and the

booming e-commerce sector further expands demand for high-quality printed

tapes.

Meanwhile, North America is

expected to witness the fastest CAGR, driven by stringent quality standards,

technological upgrades in printing, and demand for sustainable packaging.

Europe remains a mature market with an emphasis on eco-friendly materials and

regulatory-compliant labeling.

Printed Tape Market Competition Landscape Analysis

The Printed Tape Market is moderately fragmented, with

global players competing alongside regional manufacturers offering customized

and cost-efficient solutions. Leading companies focus on expanding production

capabilities, launching eco-friendly adhesive technologies, and integrating

advanced printing methods such as UV digital and flexographic systems.

Strategic partnerships with logistics providers, packaging converters, and FMCG

companies are common to strengthen market penetration.

Global Printed Tape Market Recent Developments News:

- In

September 2024, Shurtape

Technologies, LLC, acquired

Preferred Finishing Technologies, LLC, a specialist in inkjet dye

sublimation printing and fabric finishing. This strategic acquisition

formalizes and strengthens the companies' long-standing 15-year

partnership, expanding Shurtape's capabilities in advanced textile

manufacturing.

- In

August 2024, Shurtape Technologies, LLC, redesigned its premium DC 181 HVAC

tape to feature red lettering on a metallic film background. This product

enhancement directly addresses inspector preferences for "red-letter

tape" during HVAC system inspections, improving compliance visibility

and market alignment.

The Global Printed Tape Market is dominated by a few

large companies, such as

●

3M Company

●

Avery Dennison

●

Brady Corporation

●

CCL Industries

●

HellermannTyton

●

Panduit

●

Seton Identification

Products

●

Tesa SE

●

Uline

●

Weber Packaging

●

Stamptech

●

Nadco Tapes &

Labels

●

Jet Label

●

Pacproinc

●

Walle

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Printed Tape Market

Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Printed Tape Market Scope and Market Estimation

1.2.1.Global Printed Tape Overall

Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2.Global Printed Tape Market

Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Material of Global Printed

Tape Market

1.3.2.End Use of Global Printed

Tape Market

1.3.3.Region of Global Printed

Tape Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.Drivers

2.6.2.Limitations

2.6.3.Opportunities

2.6.4.Impact Analysis of Drivers

and Restraints

2.7.

Emerging

Trends for Printed Tape Market

2.8.

Porter’s

Five Forces Analysis

2.9.

PEST

Analysis

2.10.

Key

Regulation

3. Global

Printed Tape Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Printed Tape Market Estimates

& Forecast Trend Analysis, by Material

4.1.

Global

Printed Tape Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2020

- 2033

4.1.1.Polypropylene

4.1.2.Polyvinyl Chloride

4.1.3.Others Material

5. Global

Printed Tape Market Estimates

& Forecast Trend Analysis, by End Use

5.1.

Global

Printed Tape Market Revenue (US$ Bn) Estimates and Forecasts, by End Use, 2020

- 2033

5.1.1.Food & Beverage

5.1.2.Consumer Durables

5.1.3.Transportation &

Logistics

5.1.4.Others End Use

6. Global

Printed Tape Market Estimates

& Forecast Trend Analysis, by Region

6.1.

Global

Printed Tape Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 -

2033

6.1.1.North America

6.1.2.Europe

6.1.3.Asia Pacific

6.1.4.Middle East & Africa

6.1.5.Latin America

7. North America Printed

Tape Market: Estimates & Forecast

Trend Analysis

7.1.

North

America Printed Tape Market Assessments & Key Findings

7.1.1.North America Printed Tape

Market Introduction

7.1.2.North America Printed Tape

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

7.1.2.1. By Material

7.1.2.2. By End Use

7.1.2.3.

By

Country

7.1.2.3.1. The U.S.

7.1.2.3.2. Canada

8. Europe Printed

Tape Market: Estimates & Forecast

Trend Analysis

8.1.

Europe

Printed Tape Market Assessments & Key Findings

8.1.1.Europe Printed Tape Market

Introduction

8.1.2.Europe Printed Tape Market

Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Material

8.1.2.2. By End Use

8.1.2.3.

By

Country

8.1.2.3.1.

Germany

8.1.2.3.2.

Italy

8.1.2.3.3.

U.K.

8.1.2.3.4.

France

8.1.2.3.5.

Spain

8.1.2.3.6.

Switzerland

8.1.2.3.7. Rest

of Europe

8.1.2.3.8.

9. Asia Pacific Printed

Tape Market: Estimates & Forecast

Trend Analysis

9.1.

Asia

Pacific Market Assessments & Key Findings

9.1.1.Asia Pacific Printed Tape

Market Introduction

9.1.2.Asia Pacific Printed Tape

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Material

9.1.2.2. By End Use

9.1.2.3.

By

Country

9.1.2.3.1.

China

9.1.2.3.2.

Japan

9.1.2.3.3.

India

9.1.2.3.4.

Australia

9.1.2.3.5.

South

Korea

9.1.2.3.6. Rest of Asia Pacific

10. Middle East & Africa Printed

Tape Market: Estimates & Forecast

Trend Analysis

10.1.

Middle

East & Africa Market Assessments & Key Findings

10.1.1.

Middle East & Africa Printed Tape Market Introduction

10.1.2.

Middle East & Africa Printed Tape Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

10.1.2.1. By Material

10.1.2.2. By End Use

10.1.2.3.

By

Country

10.1.2.3.1. UAE

10.1.2.3.2. Saudi

Arabia

10.1.2.3.3. South

Africa

10.1.2.3.4. Rest

of MEA

11. Latin America

Printed Tape Market: Estimates &

Forecast Trend Analysis

11.1.

Latin

America Market Assessments & Key Findings

11.1.1.

Latin

America Printed Tape Market Introduction

11.1.2.

Latin

America Printed Tape Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Material

11.1.2.2. By End Use

11.1.2.3.

By

Country

11.1.2.3.1. Brazil

11.1.2.3.2. Argentina

11.1.2.3.3. Mexico

11.1.2.3.4. Rest

of LATAM

12. Country Wise Market:

Introduction

13.

Competition

Landscape

13.1.

Global

Printed Tape Market Material Mapping

13.2.

Global

Printed Tape Market Concentration Analysis, by Leading Players / Innovators /

Emerging Players / New Entrants

13.3.

Global

Printed Tape Market Tier Structure Analysis

13.4.

Global

Printed Tape Market Concentration & Company Market Shares (%) Analysis, 2024

14.

Company

Profiles

14.1.

3M

14.1.1.

Company

Overview & Key Stats

14.1.2.

Financial

Performance & KPIs

14.1.3.

Material

Portfolio

14.1.4.

SWOT

Analysis

14.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

14.2. Avery

Dennison

14.3. Brady

Corporation

14.4. CCL

Industries

14.5. HellermannTyton

14.6. Panduit

14.7. Seton

Identification Products

14.8. Tesa SE

14.9. Uline

14.10. Weber

Packaging

14.11. Stamptech

14.12. Nadco

Tapes & Labels

14.13. Jet

Label

14.14. Pacproinc

14.15. Walle

14.16. Others

15. Research

Methodology

15.1.

External

Transportations / Databases

15.2.

Internal

Proprietary Database

15.3.

Primary

Research

15.4.

Secondary

Research

15.5.

Assumptions

15.6.

Limitations

15.7.

Report

FAQs

16. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables