Radio Frequency Components Market Size and Forecast (2026 - 2034), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage; By Component (RF Filters, RF Power Amplifiers, RF Switches, RF Duplexers, RF Modulators & Demodulators, RF Transceivers and Others); By Frequency Band (Low Frequency, High Frequency, Very High Frequency, Ultra-High Frequency, Super High Frequency); By Application (Mobile Devices, Telecom Infrastructure, Automotive, Consumer Electronics, Aerospace & Defense, Industrial and Others); By End-use (Telecom Operators, Device Manufacturers, Automotive OEMs, Defense & Aerospace Organizations, Enterprises and Others) and Geography

2026-03-11

Semiconductor and Electronics

Ekta Chaurasia (Team Lead)

Description

Radio Frequency Components Market Overview

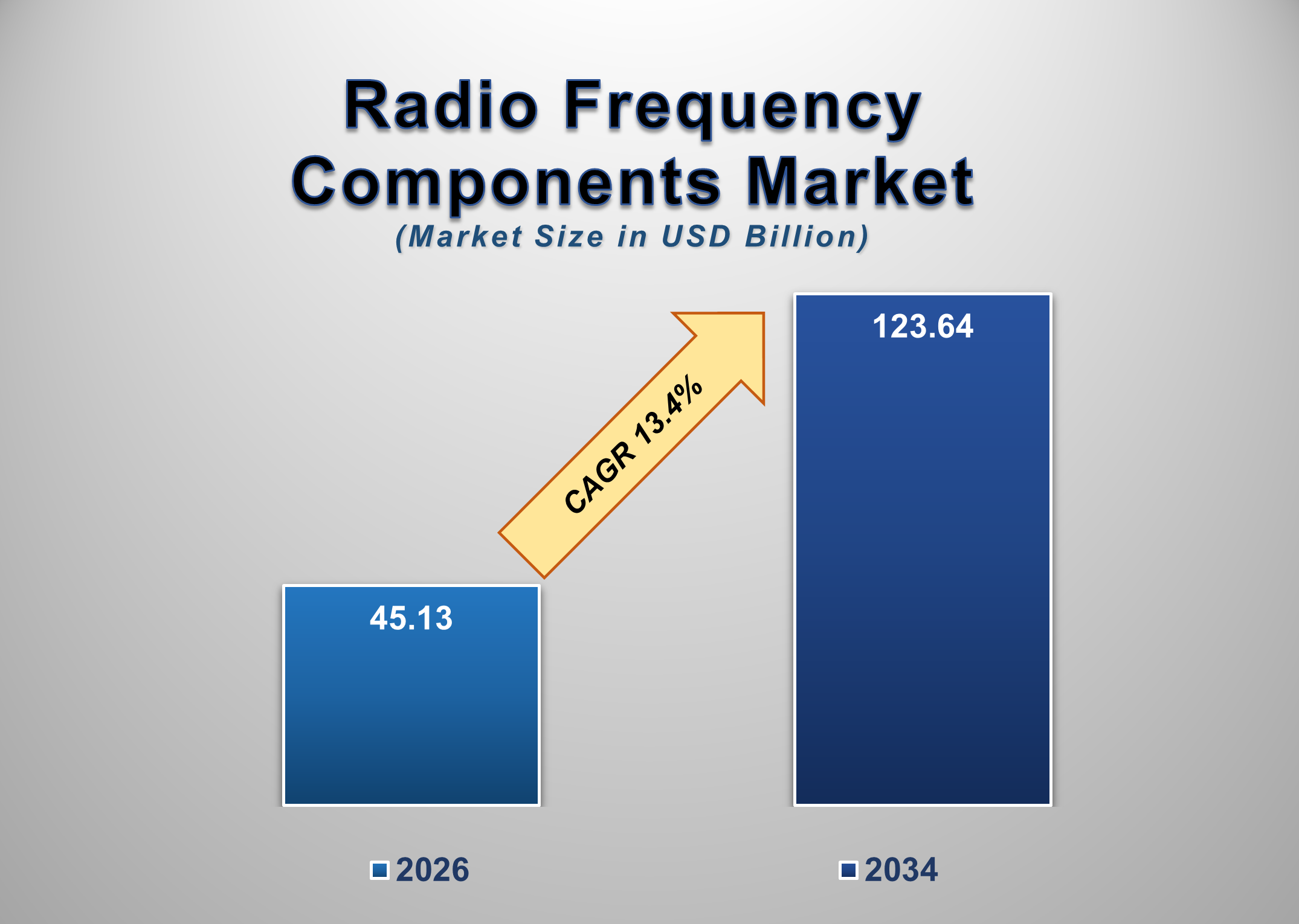

The global Radio Frequency (RF) Components Market is expanding steadily as wireless communication technologies evolve and digital connectivity becomes embedded across industries. In 2026, the market is estimated at USD 45.13 billion 2026 and is projected to reach approximately USD 123.64 billion by 2034, registering a CAGR of 13.4% during the forecast period.

RF components are critical electronic building blocks that enable transmission and reception of electromagnetic signals across defined frequency ranges. These components are integrated into smartphones, wireless routers, cellular base stations, satellite systems, radar platforms, connected vehicles, and industrial communication equipment. Core RF elements such as filters, amplifiers, switches, and transceivers manage signal strength, reduce interference, and ensure stable wireless connectivity.

As global communication standards transition toward 5G and beyond, devices require support for multiple bands and higher spectrum efficiency. This shift significantly increases RF design complexity and content per device. The ongoing convergence of telecommunications, automotive electronics, IoT systems, and satellite communication networks is expected to sustain long-term demand for advanced RF solutions.

Radio Frequency Components Market Drivers and Opportunities

Expansion of 5G Networks and Higher Spectrum Utilization are expected to accelerate the Radio Frequency Components market growth

The deployment of 5G infrastructure worldwide is a major structural driver for RF component demand. Compared to previous generations of wireless technology, 5G operates across broader and higher-frequency spectrums, including sub-6 GHz and millimeter-wave bands. Supporting these frequencies requires highly efficient RF filters, power amplifiers, and antenna tuning systems capable of handling increased bandwidth and complex signal aggregation.

Modern smartphones now incorporate significantly more RF content to accommodate multiple frequency bands and carrier aggregation technologies. Additionally, 5G base stations rely on massive MIMO configurations, which increase the number of RF signal chains required per unit. As global 5G subscriptions continue to expand into billions of users, network densification and small cell deployments further stimulate demand for high-performance RF modules.

The continuous allocation of new spectrum bands by regulatory authorities in North America, Europe, and Asia-Pacific is reinforcing the need for frequency-specific RF solutions. Consequently, spectrum expansion combined with 5G rollouts is expected to remain a primary growth engine for the market.

Proliferation of Connected Devices and Advanced Automotive Communication Systems is a key driver shaping the global Radio Frequency Components market

The number of connected devices worldwide continues to rise rapidly, fueled by IoT integration, wearable technology, smart home ecosystems, and industrial automation platforms. Each connected device requires embedded RF circuitry to enable wireless communication across Wi-Fi, Bluetooth, cellular, or proprietary frequency bands.

The automotive industry is increasingly incorporating RF-enabled systems to support connected car services, navigation, telematics, vehicle-to-everything (V2X) communication, and advanced driver assistance systems (ADAS). As vehicles become more software-defined and connectivity-centric, the RF content within each vehicle is rising steadily.

Electric vehicles and autonomous driving platforms demand real-time data exchange with infrastructure and cloud systems, further reinforcing the importance of reliable RF modules. Industrial wireless communication networks, including private 5G and IoT deployments, are also contributing to incremental demand. This widespread adoption of wireless-enabled technologies across sectors is strengthening the structural foundation of the RF components market.

Satellite Broadband Expansion and Defense Communication Modernization present significant opportunities in the global Radio Frequency Components market

The emergence of low-earth orbit (LEO) satellite networks and modernization of military communication systems are creating new avenues for RF component manufacturers. Satellite broadband constellations require components capable of operating at high-frequency bands such as Ku and Ka, demanding advanced signal processing and amplification technologies.

Defense agencies are investing heavily in next-generation radar systems, electronic surveillance equipment, secure tactical communication networks, and unmanned aerial systems. These platforms depend on highly reliable RF semiconductors capable of performing in extreme operational environments.

In addition, the commercialization of space-based internet services is increasing the need for radiation-resistant RF components and specialized high-frequency amplifiers. As both public and private sectors intensify investments in satellite connectivity and defense electronics, long-term growth opportunities are expected to expand across high-frequency RF solutions.

Radio Frequency Components Market Scope

Segments Covered

Radio Frequency Components Market Report Segmentation Analysis

The Radio Frequency Components Market is segmented based on component type, operating frequency band, application, end-use, and geography.

RF Filters Account for the Largest Share within the Component Segment

Among components, RF filters contribute significantly to market revenue due to their essential role in isolating desired frequencies and minimizing interference across complex communication systems. As multi-band devices become standard, the number of filters integrated into each device continues to increase. Power amplifiers are also witnessing strong demand, particularly in high-frequency applications where signal strength optimization is critical.

Ultra-High Frequency (UHF) Segment Leads by Frequency Band

The UHF band remains widely adopted in mobile communication and broadcasting applications, making it a dominant segment. However, super high frequency bands are gaining momentum as 5G millimeter-wave networks and advanced radar systems require higher spectrum operation.

Mobile Devices Represent the Largest Application Segment

Smartphones and connected mobile devices account for a substantial portion of RF component demand due to continuous product innovation and feature integration. Telecom infrastructure deployment is another major contributor, particularly with the rollout of new base stations and network densification projects.

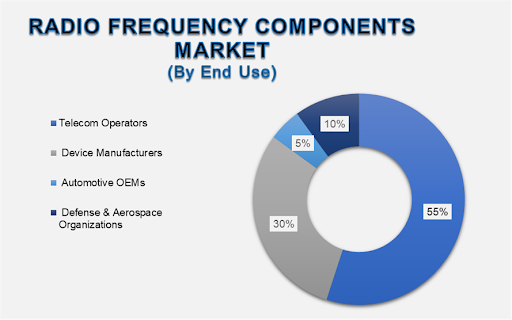

Device Manufacturers Dominate the End-use Segment

Device manufacturers constitute the largest end-use category as they integrate RF modules into consumer electronics and communication devices at large production volumes. Telecom operators and defense organizations also contribute significantly through infrastructure upgrades and system modernization programs.

Radio Frequency Components Market Share Analysis by Region

North America is anticipated to maintain the largest market share throughout the forecast period, supported by advanced semiconductor manufacturing capabilities, strong 5G adoption, and substantial defense technology investments.

Europe holds a considerable share due to automotive electronics innovation and steady telecom modernization. Asia-Pacific is projected to register the fastest growth rate, driven by large-scale electronics manufacturing, rapid 5G deployment, and increasing domestic semiconductor production capacity in countries such as China, South Korea, and Japan.

Latin America and the Middle East & Africa are emerging markets with expanding telecom infrastructure investments and rising mobile connectivity demand.

Global Radio Frequency Components Market Recent Developments News:

In 2025, several RF semiconductor manufacturers expanded production facilities to meet growing demand for 5G-compatible power amplifiers and filters.

In 2024, automotive OEMs increased integration of advanced RF modules to support connected vehicle communication systems.

In early 2025, satellite broadband providers invested in high-frequency RF technologies to enhance global connectivity coverage.

The Global Radio Frequency Components Market is dominated by a few large companies, such as

Broadcom Inc.

Qualcomm Technologies

Skyworks Solutions

Qorvo Inc.

Murata Manufacturing

NXP Semiconductors

Analog Devices Inc.

Infineon Technologies

Texas Instruments

STMicroelectronics

Renesas Electronics

MACOM Technology Solutions

Microchip Technology

Toshiba Electronic Devices

Other Prominent Players

Frequently Asked Questions

Ekta Chaurasia (Team Lead)

Ekta Chaurasia is a highly experienced Team Lead at M2Square Consultancy with over 7 years of expertise in market research, strategic consulting, competitive benchmarking, and business intelligence solutions. She specializes in ICT, semiconductors & electronics, automotive & transportation, and industrial machinery markets.

She leads end-to-end global research projects focused on market trends, industry analysis, growth forecasting, customer insights, and strategic decision-making. Known for her analytical leadership and industry expertise, Ekta helps businesses uncover growth opportunities, evaluate competitive landscapes, and stay ahead in rapidly evolving markets through accurate and insight-driven research.

Radio Frequency Components Market

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables