Razor and Blade Market Size and Forecast (2020–2033), Global and Regional Growth, Trend, Share, and Industry Analysis Report Coverage: By Product Type (Cartridge Razors, Disposable Razors, Safety Razors, Electric Shavers, Straight Razors), By Consumer Segment (Men, Women), By Distribution Channel (Hypermarkets/Supermarkets, Retail Pharmacies & Drug Stores, Online Channels, Specialty Stores), and Geography

2025-12-19

Consumer Products

Jaya Bundele (Research Analyst)

Description

Razor and

Blade Market Overview

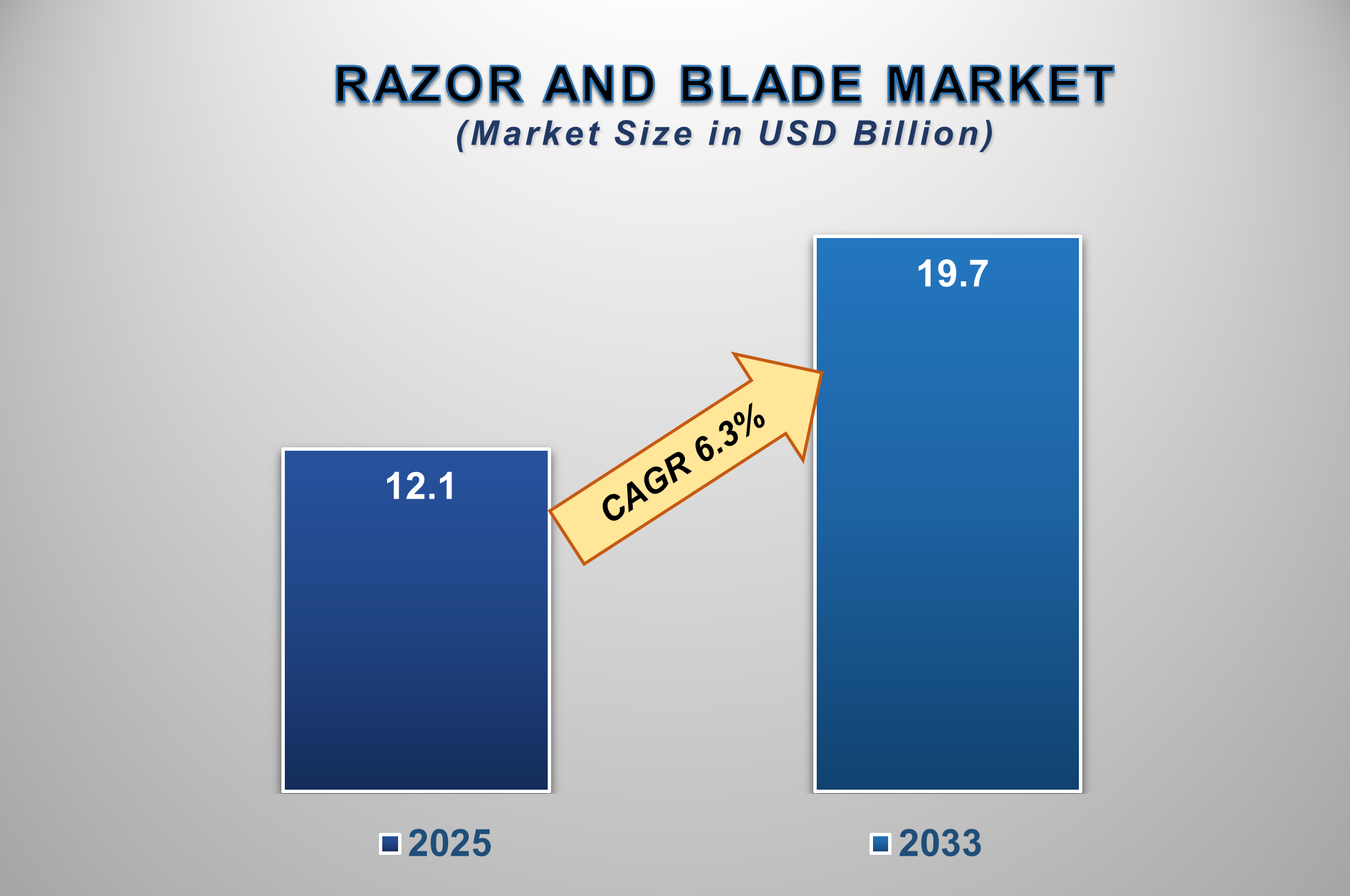

The Razor and Blade Market is poised for steady growth from 2025 to 2033, driven by evolving grooming habits, rising emphasis on personal care and hygiene, and continuous innovation in shaving technology. The market is expected to be valued at USD 12.1 billion in 2025 and is projected to reach USD 19.7 billion by 2033, registering a CAGR of 6.3% during the forecast period.

The market encompasses a range of shaving solutions,

including systems (razor handles and replaceable blade cartridges), disposable

razors, and electric shavers, designed for both men and women. The core

"razor-and-blade" business model, where razors are sold at a low

margin to drive recurring sales of high-margin blades, continues to underpin

the industry.

Growth is fueled by increasing disposable incomes,

especially in emerging economies, and a cultural shift towards well-groomed

appearances in both personal and professional spheres. The men's segment

remains dominant, while the women's segment is growing rapidly due to

heightened awareness and product specialization. North America and Europe are

mature markets with high penetration of premium products, while the

Asia-Pacific region is emerging as the fastest-growing market due to its vast

population and increasing adoption of Western grooming trends.

Razor and Blade Market Drivers and Opportunities

Rising Male Grooming Consciousness and Premiumization Are

Primary Market Drivers

The global increase in male engagement with personal

grooming is a fundamental market driver. Beyond basic shaving, men are

increasingly adopting detailed skincare and beard-grooming routines, driving

demand for specialized razors, trimmers, and premium blades with lubricating

strips and skin guards. The trend of beard styling has also catalyzed sales of

precision trimmers and specialized kits. Simultaneously, the premiumization

trend sees consumers willing to pay more for advanced features such as flexball

technology, multiple-blade cartridges for a closer shave, and subscription

services that deliver curated products to their doorstep. This shift from

utilitarian shaving to an experiential, self-care ritual is expanding market

value.

Growth in Female Shaving and Subscription E-commerce Models

Is Accelerating Market Adoption

The women's shaving segment is a high-growth area, driven

by evolving beauty standards, increased participation in fitness and athletics,

and greater marketing focus on female-specific designs. Products featuring

ergonomic handles for contoured areas, moisturizing strips, and Venus-style

cartridges are gaining strong traction. Furthermore, the direct-to-consumer

(DTC) subscription model, pioneered by brands like Dollar Shave Club and

Harry's, has revolutionized the market. These models offer convenience, cost

savings, and personalized experiences, disrupting traditional retail channels

and building strong customer loyalty. The expansion of e-commerce globally has

made these models and a wider variety of products accessible, further

accelerating market penetration.

Untapped Potential in Emerging Markets and Innovation in

Sustainable & Connected Products Present Significant Opportunities

Emerging markets in Asia-Pacific, Latin America, and Africa

present substantial growth opportunities due to large youth populations,

urbanization, and rising disposable incomes. Increasing penetration of modern

retail and e-commerce platforms is making branded shaving products more

accessible. Innovation remains a key opportunity area, with a strong focus on

sustainable products (e.g., recyclable blades, biodegradable handles,

plastic-free packaging) to meet eco-conscious consumer demand. Additionally, the

integration of technology through connected electric shavers with app-based

skin coaching, battery-life tracking, and personalized settings offers a

pathway for differentiation and premium pricing. For manufacturers,

opportunities lie in developing affordable yet effective product lines for

price-sensitive regions and forging partnerships with online beauty and

grooming platforms.

Razor and Blade Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 12.1 Billion |

|

Market Forecast in 2033 |

USD 19.7 Billion |

|

CAGR % 2025-2033 |

6.3% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Product Portfolio,

Technological Analysis, Company Market Share, Company Heatmap, Pricing

Analysis, Growth Factors and more |

|

Segments Covered |

●

By Product Type ●

By Consumer

Segment ●

By Distribution

Channel |

|

Regional Scope |

●

North America, ●

Europe, ●

APAC, ●

Latin America ●

Middle East and

Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19)

UAE |

Razor and Blade Market Report Segmentation

Analysis

The

global Razor and Blade Market is segmented by Product Type, Consumer Segment,

Distribution Channel, and Region.

Cartridge Razors Are

Anticipated to Command the Largest Market Share in 2025

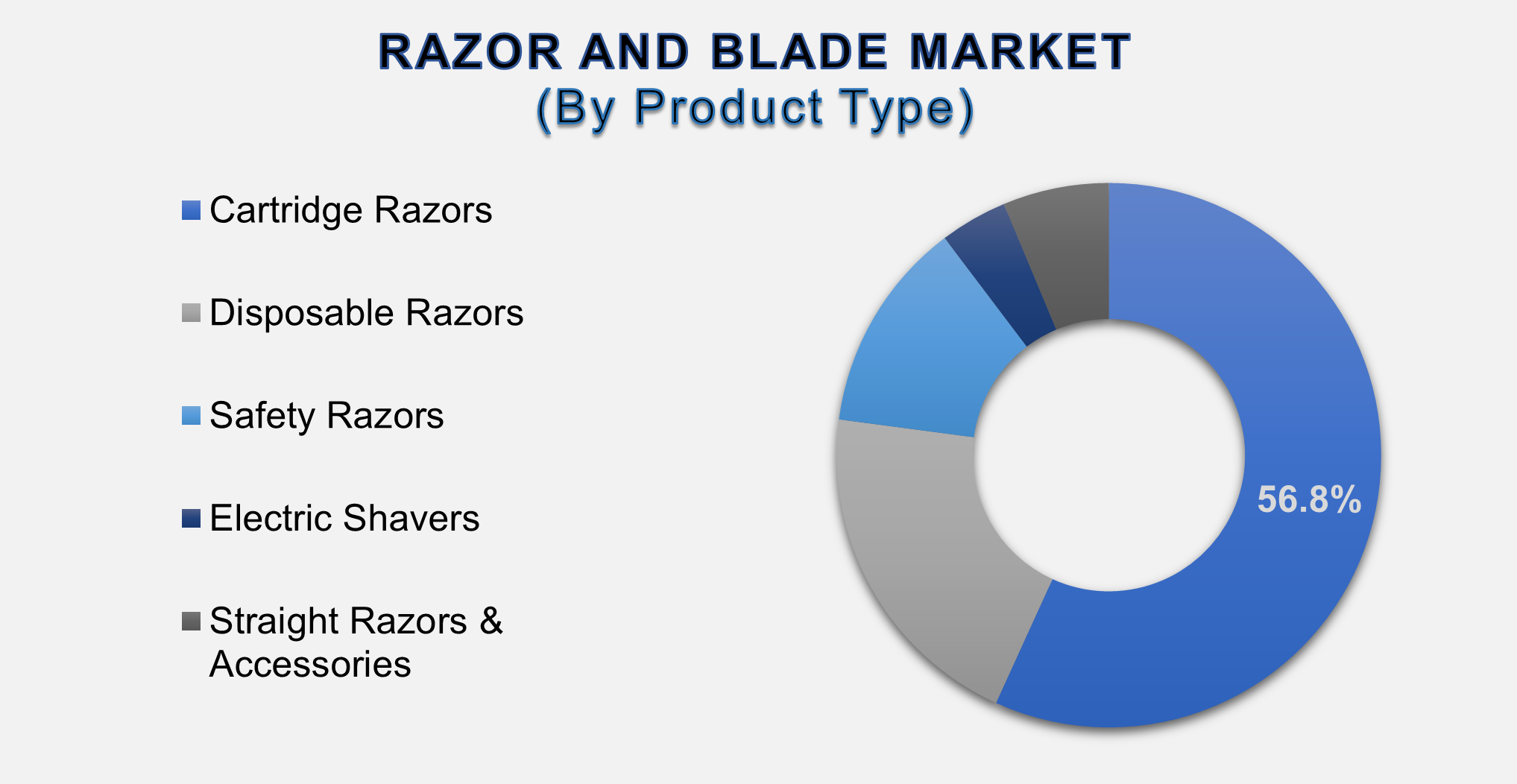

The Product Type segment is divided into Cartridge Razors, Disposable Razors, Safety Razors, Electric Shavers, and Straight Razors & Accessories. Cartridge razors dominate the Product Type segment, underpinned by the entrenched "razor-and-blade" business model of leading players. Their market leadership is anchored in providing a superior shaving experience through multi-blade technology, pivoting heads, and lubricating strips that reduce irritation and offer a closer shave than disposable alternatives. Consumers exhibit high brand loyalty within these ecosystems (e.g., Gillette's Fusion, ProGlide; Schick's Hydro). Continuous innovation, such as adding more blades, skin guards, and heating technology, along with aggressive marketing and subscription bundling, ensures consistent repurchase of proprietary blade cartridges. This segment's profitability and recurring revenue stream solidify its leading position.

The Men's Segment Holds

the Largest Share by Consumer Segment

The

men's segment is the traditional and largest consumer base for razors and

blades. Its dominance stems from daily shaving habits among a large portion of

the adult male population globally. The segment is highly driven by marketing,

brand loyalty, and continuous product innovation aimed at delivering the

"perfect shave." Furthermore, the rise of beard culture has not

diminished sales but diversified them, creating demand for precision trimmers

and hybrid razor/trimmer devices for detailed styling. High spending on premium

grooming products and the early adoption of subscription services further

cement men as the primary revenue generators for the market.

Hypermarkets/Supermarkets

Lead the Distribution Channel Segment

Hypermarkets

and supermarkets hold the dominant share in the Distribution Channel segment,

driven by high footfall, impulse purchases, and the convenience of one-stop

shopping. These stores offer extensive shelf space for a wide range of brands

and price points, from value disposables to premium systems. They remain the

primary touchpoint for first-time buyers and those who have not migrated to

online subscriptions. The ability to physically see and compare products,

coupled with frequent promotional discounts and bundle offers, makes this

channel the most accessible for the mass market, ensuring its continued

leadership despite the rapid growth of online sales.

The following segments are

part of an in-depth analysis of the global Razor and Blade Market:

|

Market

Segments |

|

|

By Product

Type |

●

Cartridge Razors ●

Disposable Razors ●

Safety Razors ●

Electric Shavers ●

Straight Razors

& Accessories |

|

By Consumer

Segment |

●

Men ●

Women |

|

By Distribution Channel |

●

Hypermarkets/Supermarkets ●

Retail Pharmacies

& Drug Stores ●

Online Channels ●

Specialty Stores |

Razor and Blade Market Share Analysis by Region

The North America region

is anticipated to hold the largest portion of the Razor and Blade Market

globally throughout the forecast period.

North

America's leadership is driven by high per capita spending on grooming products, early and widespread adoption of premium

and subscription shaving solutions, and the presence of major market incumbents

like Procter & Gamble (Gillette) and Edgewell Personal Care (Schick). The

region has a mature but innovative market where consumers regularly upgrade to

the latest technology. The Direct-to-Consumer (DTC) model is deeply entrenched,

with a significant percentage of sales occurring online. Furthermore, strong

marketing campaigns and a culture that emphasizes personal grooming for

professional and social success sustain high-volume and high-value sales,

keeping North America at the forefront of the global market.

Razor and Blade Market Competition Landscape

Analysis

The global market is highly

consolidated, dominated by a few multinational giants, though challenged by

agile DTC brands. Competition is intense, based on brand equity, continuous

R&D in blade technology, marketing spend, and distribution reach. Traditional

leaders compete by launching technologically advanced systems, while DTC brands

focus on value, convenience, and community building. Sustainability is becoming

a key battleground, with companies investing in recyclable products and reduced

plastic use. Strategic acquisitions of niche brands and expansion into women's

grooming and adjacent skincare categories are common competitive strategies.

Global Razor and Blade Market Recent Developments News:

- In February 2025, Procter & Gamble launched GilletteLabs with

Heated Razor technology 2.0, featuring an enhanced warming bar for a

closer shave.

- In November 2024, Harry's Inc. expanded into the women's skincare

segment with the launch of a line of shave gels and post-shave balms.

- In September 2024, Philips Norelco introduced its Series 9000

electric shaver with AI-powered skin sensor technology, adapting to beard

density in real time.

- In June 2024, Edgewell Personal Care (Schick) announced a strategic

partnership with a major European retail chain for exclusive product

bundles.

The Global Razor and Blade Market Is Dominated by

a Few Large Companies, such as

●

The Procter &

Gamble Company (Gillette)

●

Edgewell Personal Care

●

BIC

●

Energizer Holdings,

Inc.

●

Harry's Inc.

●

Dorco Co., Ltd.

●

Supermax

●

Société Bic S.A.

●

Feather Safety Razor

Co., Ltd.

●

Koninklijke Philips NV.

●

Panasonic Corporation

●

Braun GmbH

●

Beiersdorf AG (Nivea

Men)

● Other Prominent Players

Frequently Asked Questions

Jaya Bundele (Research Analyst)

Jaya Bundele is a skilled Research Analyst with 4+ years of experience in market intelligence, consumer insights, competitive analysis, and industry forecasting across the consumer goods, agriculture, and food & beverage sectors. She specializes in market sizing, trend analysis, growth opportunity mapping, and strategic secondary research for global and regional markets.

Her expertise lies in transforming complex industry data into actionable business strategies that help organizations identify emerging trends, understand customer behavior, and gain a competitive edge. With a strong focus on data-driven insights, business intelligence, and future market trends, Jaya delivers high-quality research solutions aligned with evolving industry demands and market dynamics.

1. Global Razor and Blade

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Razor and Blade Market Scope and Market Estimation

1.2.1.Global Electronic Toll

Collection Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025

- 2033)

1.2.2.Global Razor and Blade

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

1.3.

Market

Segmentation

1.3.1.Product Type of Global Razor

and Blade Market

1.3.2.Consumer Segment of Global

Razor and Blade Market

1.3.3.Distribution Channel of Global

Razor and Blade Market

1.3.4.Region of Global Razor and

Blade Market

2. Executive

Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2020 – 2024 and forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Key

Developments

2.6.

Market

Entry Strategies

2.7.

Market

Dynamics

2.7.1.Drivers

2.7.2.Limitations

2.7.3.Opportunities

2.7.4.Impact Analysis of Drivers

and Restraints

2.8.

Porter’s

Five Forces Analysis

2.9.

Pricing

Analysis

2.10.

PEST

Analysis

3. Global

Razor and Blade Market Estimates

& Historical Trend Analysis (2020 - 2024)

4. Global

Razor and Blade Market Estimates

& Forecast Trend Analysis, by Product Type

4.1.

Global

Razor and Blade Market Revenue (US$ Bn) Estimates and Forecasts, by Product

Type, 2020 - 2033

4.1.1.Cartridge Razors

4.1.2.Disposable Razors

4.1.3.Safety Razors

4.1.4.Electric Shavers

4.1.5.Straight Razors &

Accessories

5. Global

Razor and Blade Market Estimates

& Forecast Trend Analysis, by Consumer Segment

5.1.

Global

Razor and Blade Market Revenue (US$ Bn) Estimates and Forecasts, by Consumer

Segment, 2020 - 2033

5.1.1.Men

5.1.2.Women

6. Global

Razor and Blade Market Estimates

& Forecast Trend Analysis, by Distribution Channel

6.1.

Global

Razor and Blade Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution

Channel 2020 - 2033

6.1.1.Hypermarkets/Supermarkets

6.1.2.Retail Pharmacies &

Drug Stores

6.1.3.Online Channels

6.1.4.Specialty Stores

7. Global

Razor and Blade Market Estimates

& Forecast Trend Analysis, by region

7.1.

Global

Razor and Blade Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2020

- 2033

7.1.1.North America

7.1.2.Europe

7.1.3.Asia Pacific

7.1.4.Middle East & Africa

7.1.5.Latin America

8. North America Razor

and Blade Market: Estimates &

Forecast Trend Analysis

8.1.

North

America Razor and Blade Market Assessments & Key Findings

8.1.1.North America Razor and

Blade Market Introduction

8.1.2.North America Razor and

Blade Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

8.1.2.1. By Product

Type

8.1.2.2. By Consumer

Segment

8.1.2.3. By Distribution

Channel

8.1.2.4.

By

Country

8.1.2.4.1. The U.S.

8.1.2.4.2. Canada

9. Europe Razor

and Blade Market: Estimates &

Forecast Trend Analysis

9.1.

Europe

Razor and Blade Market Assessments & Key Findings

9.1.1.Europe Razor and Blade

Market Introduction

9.1.2.Europe Razor and Blade

Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

9.1.2.1. By Product

Type

9.1.2.2. By Consumer

Segment

9.1.2.3. By Distribution

Channel

9.1.2.4.

By

Country

9.1.2.4.1.

Germany

9.1.2.4.2.

Italy

9.1.2.4.3.

U.K.

9.1.2.4.4.

France

9.1.2.4.5.

Spain

9.1.2.4.6.

Switzerland

9.1.2.4.7. Rest

of Europe

10. Asia Pacific Razor

and Blade Market: Estimates &

Forecast Trend Analysis

10.1.

Asia

Pacific Market Assessments & Key Findings

10.1.1.

Asia

Pacific Razor and Blade Market Introduction

10.1.2.

Asia

Pacific Razor and Blade Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

10.1.2.1. By Product

Type

10.1.2.2. By Consumer

Segment

10.1.2.3. By Distribution

Channel

10.1.2.4.

By

Country

10.1.2.4.1. China

10.1.2.4.2. Japan

10.1.2.4.3. India

10.1.2.4.4. Australia

10.1.2.4.5. South Korea

10.1.2.4.6. Rest of Asia Pacific

11. Middle East & Africa Razor

and Blade Market: Estimates &

Forecast Trend Analysis

11.1.

Middle

East & Africa Market Assessments & Key Findings

11.1.1.

Middle East & Africa Razor and Blade Market Introduction

11.1.2.

Middle East & Africa Razor and Blade Market Size Estimates

and Forecast (US$ Billion) (2020 - 2033)

11.1.2.1. By Product

Type

11.1.2.2. By Consumer

Segment

11.1.2.3. By Distribution

Channel

11.1.2.4.

By

Country

11.1.2.4.1. UAE

11.1.2.4.2. Saudi

Arabia

11.1.2.4.3. South

Africa

11.1.2.4.4. Rest

of MEA

12. Latin America

Razor and Blade Market: Estimates &

Forecast Trend Analysis

12.1.

Latin

America Market Assessments & Key Findings

12.1.1.

Latin

America Razor and Blade Market Introduction

12.1.2.

Latin

America Razor and Blade Market Size Estimates and Forecast (US$ Billion) (2020

- 2033)

12.1.2.1. By Product

Type

12.1.2.2. By Consumer

Segment

12.1.2.3. By Distribution

Channel

12.1.2.4.

By

Country

12.1.2.4.1. Brazil

12.1.2.4.2. Argentina

12.1.2.4.3. Mexico

12.1.2.4.4. Rest

of LATAM

13. Country Wise Market:

Introduction

14.

Competition

Landscape

14.1.

Global

Razor and Blade Market Product Mapping

14.2.

Global

Razor and Blade Market Concentration Analysis, by Leading Players / Innovators

/ Emerging Players / New Entrants

14.3.

Global

Razor and Blade Market Tier Structure Analysis

14.4.

Global

Razor and Blade Market Concentration & Company Market Shares (%) Analysis,

2024

15.

Company

Profiles

15.1.

The Procter & Gamble Company (Gillette)

15.1.1.

Company

Overview & Key Stats

15.1.2.

Financial

Performance & KPIs

15.1.3.

Product

Portfolio

15.1.4.

SWOT

Analysis

15.1.5.

Business

Strategy & Recent Developments

* Similar details would be provided for all the players

mentioned below

15.2. Edgewell

Personal Care

15.3. BIC

15.4. Energizer

Holdings, Inc.

15.5. Harry's Inc.

15.6. Dorco Co.,

Ltd.

15.7. Supermax

15.8. Société Bic

S.A.

15.9. Feather

Safety Razor Co., Ltd.

15.10. Koninklijke

Philips N.V.

15.11. Panasonic

Corporation

15.12. Braun GmbH

15.13. Beiersdorf AG

(Nivea Men)

15.14. Other

Prominent Players

16. Research

Methodology

16.1.

External

Transportations / Databases

16.2.

Internal

Proprietary Database

16.3.

Primary

Research

16.4.

Secondary

Research

16.5.

Assumptions

16.6.

Limitations

16.7.

Report

FAQs

17. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables